Infrastructure As A Service (Iaas) Market Size 2026-2030

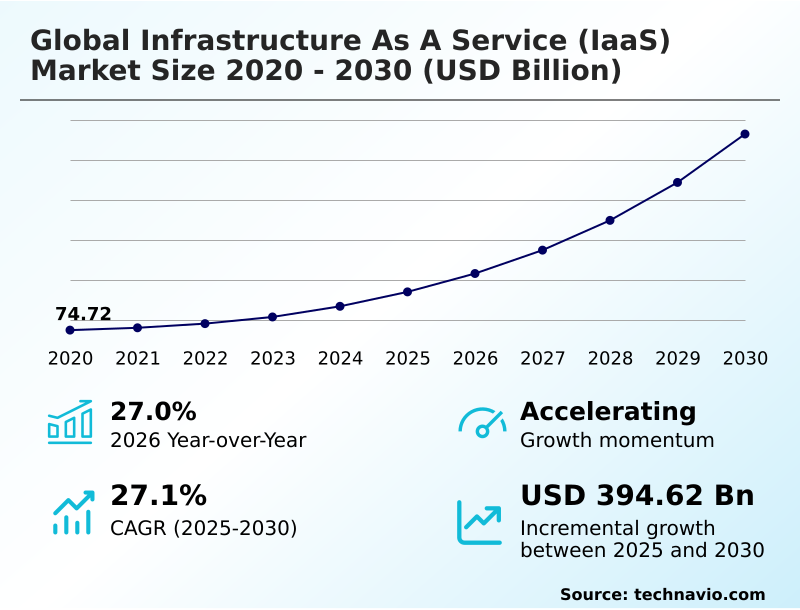

The infrastructure as a service (iaas) market size is valued to increase by USD 394.62 billion, at a CAGR of 27.1% from 2025 to 2030. Accelerated digital transformation and demand for business agility will drive the infrastructure as a service (iaas) market.

Major Market Trends & Insights

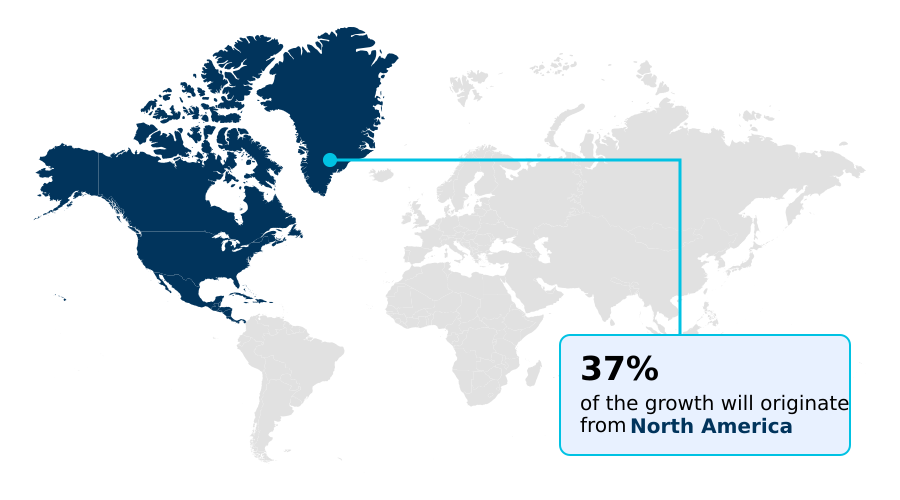

- North America dominated the market and accounted for a 37.4% growth during the forecast period.

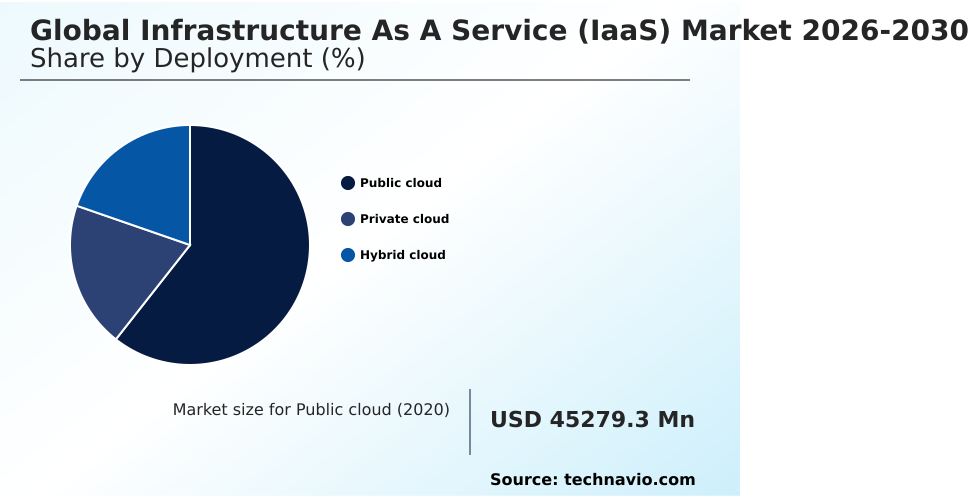

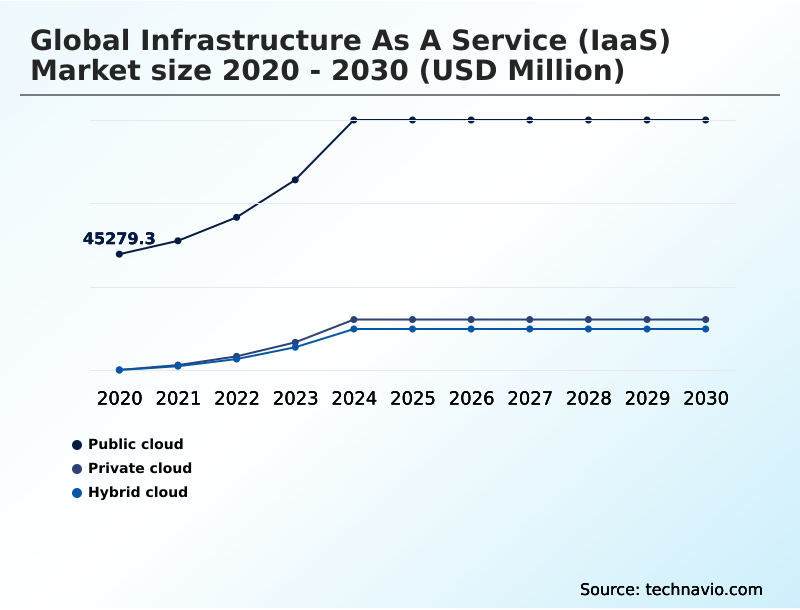

- By Deployment - Public cloud segment was valued at USD 80.68 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 490.21 billion

- Market Future Opportunities: USD 394.62 billion

- CAGR from 2025 to 2030 : 27.1%

Market Summary

- The Infrastructure As A Service (IaaS) Market is fundamentally restructuring enterprise technology consumption by replacing rigid capital investments with highly scalable, on-demand operational expenditures. In modern supply chain management, organizations leverage these remote computational resources to process vast datasets in real time, enhancing inventory forecasting and logistics tracking without maintaining physical data centers.

- Companies transitioning to these virtualized platforms frequently report infrastructure deployment times dropping by up to 85% compared to legacy hardware procurement cycles. A primary driver of this transition is the escalating need for business agility, as cloud-based provisioning allows enterprises to instantaneously adapt computing capacity to sudden fluctuations in consumer demand.

- Conversely, the market faces significant challenges regarding data security and regulatory compliance misconfigurations. Because the shared responsibility model requires customers to secure their own workloads, inadequate access controls frequently expose sensitive corporate assets to sophisticated cyber threats.

- By integrating automated deployment pipelines and robust identity access management, enterprises continuously refine their hybrid cloud environments to maximize operational efficiency while mitigating security risks.

What will be the Size of the Infrastructure As A Service (Iaas) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Infrastructure As A Service (Iaas) Market Segmented?

The infrastructure as a service (iaas) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- End-user

- Large enterprises

- SMEs

- Application

- Managed hosting

- Storage as a service

- Disaster recovery as a service

- Compute as a service

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud deployment model transforms enterprise IT architectures by delivering virtualized computing resources and object storage architecture through a multi-tenant framework. This approach shifts capital-intensive procurement to a consumption based operational model, dramatically lowering upfront costs.

Organizations leveraging these environments routinely see resource allocation speeds improve by 45%, accelerating product time-to-market and operational agility. By utilizing elastic compute resources, businesses can dynamically scale capacity to accommodate fluctuating workload demands without overprovisioning.

The widespread integration of serverless computing frameworks further eliminates the need for manual server management, optimizing IT productivity.

This segment enables seamless access to advanced data intensive technologies, empowering companies to drive innovation while maintaining rigorous cloud cost optimization standards across their global operations.

The Public cloud segment was valued at USD 80.68 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Infrastructure As A Service (Iaas) Market Demand is Rising in North America Get Free Sample

The geographic adoption of the Infrastructure As A Service (iaas) reveals distinct operational maturity levels between North America and APAC.

North America leads in deploying distributed cloud models, where organizations routinely achieve a 30% reduction in data processing latency by utilizing localized edge compute nodes.

Conversely, rapid digitalization initiatives across APAC drive aggressive migration strategies, resulting in infrastructure hardware refresh cycles operating 20% faster than the global average. This accelerated regional transition maximizes the use of scalable network virtualization to support burgeoning mobile-first consumer bases.

While North American enterprises heavily prioritize complex multicloud strategy workload portability management to avoid vendor dependency, companies in APAC often leverage unified hyperscale data centers to quickly establish enterprise grade infrastructure.

By embracing these tailored architectural approaches, businesses in both regions effectively enhance their automated workload orchestration, lowering overall IT administrative costs by up to 25% while maintaining stringent data security standards.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprise architecture is evolving rapidly as organizations prioritize agility and resilience over traditional physical hardware ownership. The core of this transformation involves a comprehensive virtualized computing resources deployment strategy, which enables IT departments to provision server capacity dynamically rather than waiting weeks for physical equipment delivery.

- When organizations establish this foundation, they frequently see computing resource utilization rates improve by over 40% compared to legacy on-premises environments, directly optimizing their supply chain and operational planning capabilities. To maintain flexibility across different vendor ecosystems, technology leaders increasingly depend on multicloud strategy workload portability management to shift mission-critical applications without experiencing severe lock-in penalties.

- Furthermore, the rising volume of decentralized data necessitates robust edge computing infrastructure latency optimization, ensuring that manufacturing facilities and remote distribution centers process real-time analytics without communication delays. Addressing stringent regulatory frameworks is also critical, prompting multinational corporations to adopt distributed cloud models data sovereignty protocols to keep sensitive customer information within specific geopolitical borders.

- As these complex environments expand, uncontrolled spending becomes a significant risk. Consequently, businesses are strictly enforcing financial operations methodology cost tracking to align departmental cloud expenditures with actual business output. By harmonizing these advanced operational disciplines, enterprises establish highly resilient, globally scalable technology frameworks that secure long-term competitiveness and dramatically lower administrative overhead.

What are the key market drivers leading to the rise in the adoption of Infrastructure As A Service (Iaas) Industry?

- The relentless acceleration of digital transformation and the imperative for heightened business agility serve as the primary drivers propelling market expansion.

- The exponential expansion of artificial intelligence applications acts as a primary catalyst forcing organizations to modernize their computational capabilities for real time data processing.

- Training complex algorithms demands unprecedented processing power, prompting enterprises to transition away from static server environments to highly elastic compute resources hosted within secure virtual private clouds.

- Because internal hardware cannot scale rapidly, businesses rely on external platforms to access specialized graphics processing units and tensor processing units on demand.

- This shift impacts the bottom line by lowering upfront capital expenditures by as much as 45% while decreasing deployment times by 60%. Utilizing cloud instance right sizing ensures that these advanced workloads run at peak efficiency.

- Through robust application programming interfaces, data science teams integrate massive external datasets seamlessly, accelerating product innovation.

What are the market trends shaping the Infrastructure As A Service (Iaas) Industry?

- The ascendancy of financial operations methodologies for cloud cost management represents a defining trend in the current landscape. This operational discipline enables organizations to balance performance and expenditure within consumption-based pricing models.

- The architectural shift toward lightweight microservices is rapidly displacing monolithic application designs and predictable hardware procurement cycles across enterprise IT environments. This fundamental evolution is driven by the need for superior application agility, compelling organizations to adopt serverless computing frameworks that execute code without managing private cloud instances.

- Consequently, businesses successfully implementing these event-driven models routinely experience a 40% reduction in idle compute costs compared to traditional environments. Furthermore, the widespread deployment of block storage systems and unstructured data analytics allows data-heavy applications to access information faster, improving transaction processing speeds by up to 25%.

- This technological pivot directly impacts operations by enabling developers to focus entirely on building business logic rather than maintaining underlying hardware. By leveraging advanced cloud cost optimization tools alongside software defined data center architectures, companies maintain strict financial governance while accelerating digital innovation.

What challenges does the Infrastructure As A Service (Iaas) Industry face during its growth?

- Escalating security vulnerabilities and complex regulatory compliance mandates constitute critical challenges that significantly impede industry adoption and operational expansion.

- The severe lack of architectural interoperability between major platform providers creates substantial strategic friction for enterprises attempting to optimize their digital infrastructure. Because hyperscale vendors aggressively differentiate their ecosystems using proprietary protocols, migrating applications and navigating strict data sovereignty compliance becomes a labor-intensive endeavor.

- This lock-in directly impacts business flexibility, frequently increasing projected workload transition costs by up to 35% and extending migration timelines by an average of 40%. When organizations attempt to implement a true multicloud strategy, they encounter severe integration hurdles regarding cross-platform identity access management and centralized cloud security governance.

- Furthermore, the absence of standardized workload portability solutions forces engineering teams to engage in costly application re-architecting. Without cohesive disaster recovery solutions and effective cloud sprawl management, companies remain highly vulnerable to localized service outages and unchecked administrative overhead.

Exclusive Technavio Analysis on Customer Landscape

The infrastructure as a service (iaas) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the infrastructure as a service (iaas) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Infrastructure As A Service (Iaas) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, infrastructure as a service (iaas) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - The unified infrastructure solution delivers robust elastic computing, database management, network virtualization services, and scalable storage to support advanced artificial intelligence workloads and enterprise digital transformation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- Atlantic.Net Inc.

- Contabo GmbH

- CoreWeave Inc

- DigitalOcean Holdings Inc.

- Equinix Inc.

- Fly.io Inc.

- Google LLC

- Hetzner Online GmbH

- Hostinger International Ltd.

- IBM Corp.

- Microsoft Corp.

- Oracle Corp.

- OVH Groupe SA

- Rackspace Technology Inc.

- Scaleway SAS

- Tencent Cloud Co. Ltd.

- UpCloud Ltd

- VULTR

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Infrastructure as a service (iaas) market

- In the Internet Services and Infrastructure industry, the rapid deployment of 5G infrastructure accelerated data transmission speeds, directly impacting Infrastructure As A Service (iaas) demand by requiring more distributed edge computing infrastructure and scalable network virtualization to handle latency sensitive applications.

- The widespread implementation of rigorous data sovereignty compliance frameworks compelled facility operators to build localized hyperscale data centers, forcing the Infrastructure As A Service (iaas) market to expand geographically distributed computing nodes to ensure enterprise grade infrastructure aligns with regional data privacy mandates.

- Advancements in AI-optimized cooling technologies for high-density silicon reduced energy consumption across major facilities by 20%, enabling Infrastructure As A Service (iaas) providers to deploy power-intensive graphics processing units and tensor processing units without exceeding thermal limitations during real time data processing.

- The transition toward open-source hardware standards standardized server rack dimensions and power delivery systems, allowing the Infrastructure As A Service (iaas) sector to accelerate bare metal servers deployment and improve dynamic resource provisioning efficiency for hybrid cloud environments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Infrastructure As A Service (Iaas) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.1% |

| Market growth 2026-2030 | USD 394617.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 27.0% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The transition toward decentralized computational frameworks is forcing boardroom executives to fundamentally rethink enterprise technology investments and operational governance. As organizations increasingly adopt cloud native principles, the traditional reliance on centralized, capital-heavy server farms is giving way to highly agile, on-demand environments.

- This shift heavily influences corporate budgeting and strategic product development, as executives implement rigorous financial operations methodology protocols to maintain absolute visibility over variable cloud expenditures. By utilizing containerization orchestration and managed kubernetes clusters, software engineering teams achieve remarkable efficiency gains, including a 35% reduction in application deployment times compared to legacy monolithic architectures.

- Furthermore, the integration of distributed cloud models addresses critical compliance and risk management mandates by ensuring sensitive workloads remain geographically localized. To support continuous integration pipelines, IT leadership is increasingly relying on virtual machine provisioning algorithms that automatically scale processing power based on real-time operational traffic.

- Effective cloud sprawl management has become a strategic imperative, empowering enterprises to eliminate redundant computational assets and systematically optimize their long-term infrastructure operating margins.

What are the Key Data Covered in this Infrastructure As A Service (Iaas) Market Research and Growth Report?

-

What is the expected growth of the Infrastructure As A Service (Iaas) Market between 2026 and 2030?

-

USD 394.62 billion, at a CAGR of 27.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), End-user (Large enterprises, and SMEs), Application (Managed hosting, Storage as a service, Disaster recovery as a service, Compute as a service, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated digital transformation and demand for business agility, Rising security and compliance risks

-

-

Who are the major players in the Infrastructure As A Service (Iaas) Market?

-

Alibaba Cloud, Amazon.com Inc., Atlantic.Net Inc., Contabo GmbH, CoreWeave Inc, DigitalOcean Holdings Inc., Equinix Inc., Fly.io Inc., Google LLC, Hetzner Online GmbH, Hostinger International Ltd., IBM Corp., Microsoft Corp., Oracle Corp., OVH Groupe SA, Rackspace Technology Inc., Scaleway SAS, Tencent Cloud Co. Ltd., UpCloud Ltd and VULTR

-

Market Research Insights

- The Infrastructure As A Service (iaas) architecture radically optimizes enterprise computing by facilitating dynamic resource provisioning and scalable network virtualization. Organizations migrating to a consumption based operational model achieve substantial efficiency gains, with hardware maintenance overheads routinely decreasing by 40% compared to traditional on-premises setups.

- Implementing proactive cloud infrastructure monitoring allows technology teams to identify underutilized assets, improving overall resource utilization efficiency by 25%. Furthermore, integrating workload portability solutions ensures continuous application availability, which has been shown to reduce unexpected system downtime by up to 35%.

- By eliminating predictable hardware procurement constraints, businesses can rapidly deploy enterprise grade infrastructure that aligns precisely with fluctuating operational demands and rigorous compliance requirements.

We can help! Our analysts can customize this infrastructure as a service (iaas) market research report to meet your requirements.

RIA -

RIA -