Infusion Therapy Devices Market Size 2024-2028

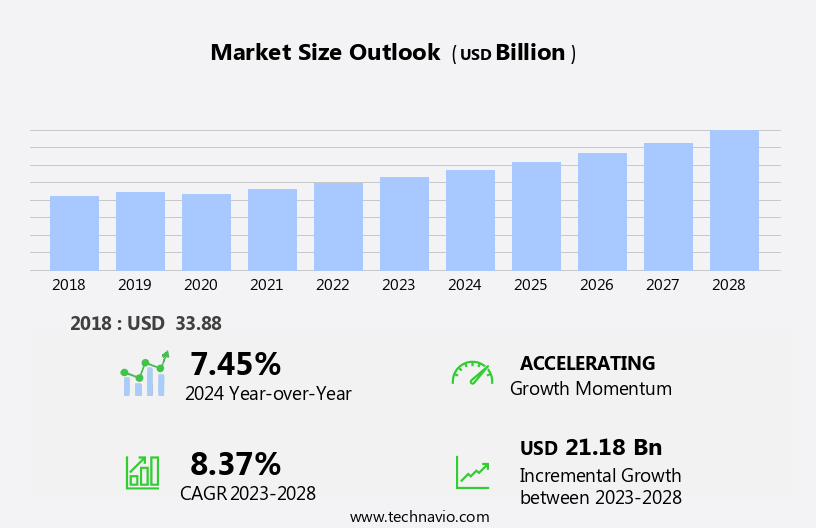

The infusion therapy devices market size is forecast to increase by USD 21.18 billion, at a CAGR of 8.37% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing prevalence of chronic diseases necessitating long-term infusion therapy. This trend is particularly prominent in the aging population, as they are more susceptible to chronic conditions such as diabetes, cancer, and neurological disorders. Another key driver is the emergence of smart infusion therapy devices, which offer advanced features such as remote monitoring, connectivity, and automated dosing. These innovations enhance patient safety, improve treatment outcomes, and increase healthcare provider efficiency. However, the market also faces challenges, primarily the high upfront costs associated with infusion pumps and equipment procurement. This financial burden can limit market penetration, particularly in developing regions and among economically disadvantaged populations.

- Furthermore, regulatory requirements and reimbursement policies add complexity to the market landscape, necessitating close collaboration between manufacturers, healthcare providers, and payers to ensure access to these life-enhancing technologies. Companies seeking to capitalize on market opportunities must navigate these challenges effectively, focusing on cost reduction strategies, value-based pricing, and regulatory compliance. By doing so, they can position themselves as trusted partners in the healthcare ecosystem, driving growth and innovation in the market.

What will be the Size of the Infusion Therapy Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and growing applications across various sectors. Needle-free injection systems and portable infusion devices are increasingly popular, offering convenience and improved patient comfort. Infusion pump technology, including volume control infusion and rate-adjustable infusions, enables precise medication delivery. Bolus injection delivery and occlusion detection systems ensure efficient and safe infusion processes. Drug delivery systems, incorporating pressure sensors for accuracy and alarm system features, enhance patient safety. Single-use infusion pumps and disposable infusion sets facilitate sterile device handling. Clinical trial applications and remote patient monitoring expand the market's reach.

Infusion therapy technology advances with ambulatory infusion pumps, wireless data transmission, and medication error reduction. Air-in-line detection and fluid flow regulation optimize battery life. Home infusion therapy and multichannel infusion pumps cater to diverse patient needs. Market dynamics remain fluid, with ongoing research and development in infusion pump technology, bolus injection delivery, and patient monitoring sensors. The focus on patient safety mechanisms, such as occlusion detection systems and alarm systems, continues to drive innovation. The market is a dynamic and evolving landscape, with new applications and technologies continually emerging.

How is this Infusion Therapy Devices Industry segmented?

The infusion therapy devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Homecare settings

- Clinics and ASCs

- Product

- Infusion pumps

- Consumables

- accessories

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

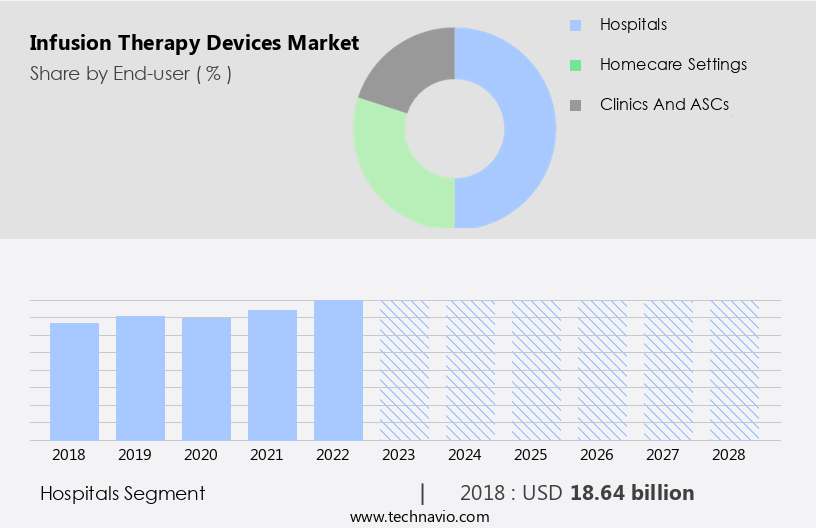

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

In the healthcare sector, hospitals serve as significant contributors to the growth of the market. Hospitals, particularly multispecialty hospitals and hospital groups, are prominent consumers due to their large size and extensive range of inpatient and outpatient services. With over 500 hospital beds, these institutions accommodate a substantial number of patients and generate substantial revenue. They procure medical products and consumables in bulk, fostering close relationships with suppliers, reimbursement authorities, and government organizations. Their advanced medical infrastructure caters to the complex surgeries and treatments in outpatient settings. Infusion therapy devices play a crucial role in these healthcare facilities.

Electronic infusion control systems and syringe pump mechanisms ensure precise medication delivery. Infusion device maintenance and single-use infusion pumps minimize the risk of infection and cross-contamination. PCA pump programming simplifies medication administration for patients. Clinical trial applications of infusion therapy devices facilitate research and development. Sterile device handling, pressure sensors' accuracy, and needle-free injection systems enhance patient safety. Portable infusion devices offer flexibility and convenience. Drug delivery systems and infusion pump technology enable the administration of various medications. Bolus injection delivery, iv administration sets, and occlusion detection systems ensure efficient and effective therapy. Disposable infusion sets and volume control infusion systems reduce the risk of medication errors.

Alarm system features, ambulatory infusion pumps, remote patient monitoring, multichannel infusion pumps, medication error reduction, air-in-line detection, fluid flow regulation, battery life optimization, and patient monitoring sensors contribute to improved patient care and outcomes. Home infusion therapy and rate-adjustable infusion systems expand access to infusion therapy beyond hospital settings. Wireless data transmission and drug compatibility testing facilitate seamless integration with electronic health records. Infusion therapy protocols standardize care and optimize resource utilization.

The Hospitals segment was valued at USD 18.64 billion in 2018 and showed a gradual increase during the forecast period.

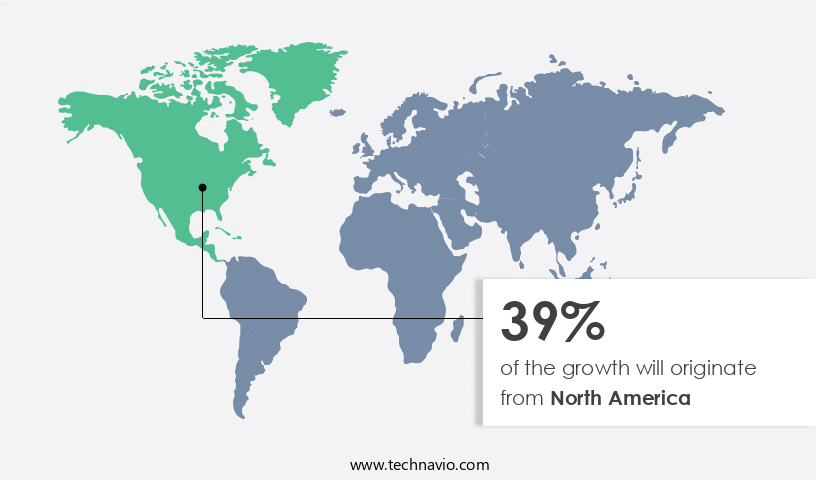

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic the market, North America emerges as a leading region, marked by advanced healthcare infrastructure, a large patient population with chronic conditions, and increasing adoption of home-based medical treatments. The United States and Canada, in particular, exhibit high demand due to the prevalence of diseases such as cancer, autoimmune disorders, and infectious diseases. Factors fueling market growth include rising healthcare expenditure, favorable reimbursement policies, and technological advancements. Infusion pump technology innovations, remote patient monitoring, and healthcare IT solutions enable safe and effective infusion therapy delivery. Single-use infusion pumps, disposable infusion sets, and volume control infusions cater to the need for medication error reduction and sterile device handling.

Pressure sensors ensure accuracy, while occlusion detection systems and air-in-line detection prevent complications. Alarm system features and patient monitoring sensors enhance patient safety. Ambulatory infusion pumps and wireless data transmission enable remote care, while medication compatibility testing and infusion therapy protocols ensure optimal drug delivery. Battery life optimization and patient safety mechanisms further add value. Home infusion therapy, rate-adjustable infusions, and multichannel infusions cater to diverse patient needs.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Infusion Therapy Devices Industry?

- The rising incidence of chronic diseases serves as the primary catalyst for market growth.

- The market experiences significant growth due to the rising prevalence of chronic conditions, such as cancer, diabetes, and heart disease. Infusion therapy plays a crucial role in treating various medical conditions by delivering fluids, electrolytes, and medications to patients. According to the International Diabetes Federation (IDF), the diabetes population is projected to reach 700 million by 2045. Diabetes patients often require intravenous therapy and vein access for glucose management, making the increasing diabetes prevalence a significant driver for the demand for IV therapy and vein access during the forecast period. Infusion therapy devices incorporate advanced technologies like electronic infusion control systems and syringe pump mechanisms to ensure accurate and efficient medication delivery.

- Single-use infusion pumps and PCA pump programming offer convenience and ease of use for healthcare providers. Infusion device maintenance is essential to ensure the accuracy and reliability of these devices, with pressure sensors playing a critical role in maintaining optimal infusion pressure. Clinical trial applications of infusion therapy devices are also increasing, further expanding their market potential. Sterile device handling is a crucial aspect of infusion therapy, ensuring patient safety and reducing the risk of infections. Overall, the market is expected to continue its growth trajectory, driven by the increasing demand for advanced medical devices and the rising prevalence of chronic conditions.

What are the market trends shaping the Infusion Therapy Devices Industry?

- Smart infusion therapy devices are gaining increasing popularity in the healthcare market, representing an emerging trend in this industry. These advanced devices offer enhanced patient care and improved treatment outcomes through features such as remote monitoring, automated delivery, and real-time data analysis.

- Infusion therapy devices are advanced drug delivery systems that integrate needle-free injection systems, portable infusion pumps, and occlusion detection systems to ensure precise and accurate medication administration. These devices utilize infusion pump technology to deliver medication via iv administration sets, with options for both continuous and bolus injection delivery. Smart infusion therapy devices offer a harmonious blend of technology and healthcare, enabling hospitals to manage drug libraries and software programs for efficient medication administration. The pharmacy department, in collaboration with the therapeutics committee, inputs and manages the drug library.

- Clinicians can select the desired drug and concentration from the library, program the device, and receive alerts through alarms for any dosage overrides. The adoption of these devices is driven by the need for error prevention in medication administration, ensuring a safer and more efficient healthcare environment.

What challenges does the Infusion Therapy Devices Industry face during its growth?

- The significant upfront expenses related to the acquisition of infusion pumps and associated equipment represent a major challenge to the industry's growth trajectory.

- Infusion therapy devices, including volume control infusion pumps and multichannel infusion systems, play a crucial role in delivering medications, fluids, and nutrients to patients in various settings. These devices come with advanced features such as alarm systems, remote patient monitoring, medication error reduction, air-in-line detection, and fluid flow regulation. However, the high upfront costs of procuring these devices pose a significant challenge to both patients and healthcare providers. Infusion pumps can cost anywhere between USD100 and USD1,000, making the initial investment substantial.

- For patients, this financial barrier can hinder access to necessary care, especially for those with limited financial resources or insufficient insurance coverage. Co-payments, deductibles, and coverage limitations can further increase out-of-pocket expenses, even with insurance. Despite these challenges, the market for infusion therapy devices continues to grow due to the benefits these devices offer, such as improved patient outcomes, enhanced safety, and increased convenience.

Exclusive Customer Landscape

The infusion therapy devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the infusion therapy devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, infusion therapy devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ace medical - This company specializes in advanced infusion therapy devices, including the Pulse Spray infusion system with pressure response outlets for optimal fluid distribution, the Uni Fuse infusion catheter for catheter-directed thrombolysis, and the SpeedLyser PROTM Infusion System. These innovative devices enhance medical treatment efficacy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ace medical

- AngioDynamics Inc.

- Avanos Medical Inc.

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Company

- Canafusion Technologies Inc.

- Cardinal Health Inc.

- Chemyx Inc.

- ERENLER MEDIKAL SAN. TIC. LTD. STI.

- Fresenius SE and Co. KGaA

- ICU Medical Inc.

- IRadimed Corp.

- Medtronic

- Poly Medicure Ltd.

- Smith and Nephew plc

- Tekni Plex Inc.

- Teleflex Inc.

- Terumo Corp.

- Vygon SAS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Infusion Therapy Devices Market

- In January 2024, Fresenius Kabi, a leading global health care company, launched the Space Infusion System, a compact and lightweight infusion device designed for home use (Fresenius Kabi press release). This innovation aims to improve patient mobility and convenience.

- In March 2024, Becton, Dickinson and Company (BD) announced a strategic partnership with Merck KGaA to develop and commercialize a new generation of wearable infusion pumps (BD press release). This collaboration combines BD's expertise in medical technology and Merck KGaA's knowledge in pharmaceuticals, aiming to enhance patient care.

- In May 2024, Grifols, a global healthcare company, acquired the infusion devices business of Hospira, Inc., a Pfizer company, for approximately USD1.65 billion (Grifols press release). This acquisition strengthened Grifols' position in the market, expanding its product portfolio and enhancing its global presence.

- In April 2025, the U.S. Food and Drug Administration (FDA) approved Medtronic's new portable infusion pump, the MiniMedTM 780G, featuring advanced insulin delivery and glucose sensing capabilities (Medtronic press release). This approval marked a significant technological advancement in the market, offering enhanced patient control and convenience.

Research Analyst Overview

- The market is characterized by continuous advancements in technology, with a focus on enhancing patient safety, convenience, and medication accuracy. Smart infusion pumps, equipped with data logging capabilities, patient education materials, and remote diagnostics, are increasingly popular. Infusion site care and infection control practices are essential considerations, with device lifespan and material biocompatibility playing crucial roles. Healthcare providers prioritize medication administration training and dosing regimen optimization, while cost-effectiveness analysis and network connectivity are key trends. Drug concentration calculation, software upgrades, user interface design, and calibration procedures are essential for ensuring drug delivery accuracy and quality control testing.

- Advanced infusion technology includes syringe pump design, clinical workflow integration, and extended care solutions, all aimed at improving patient comfort and infection control practices. Regulatory approval processes and medication administration remain critical aspects of the market, with a growing emphasis on patient self-management and infusion line management. Drug stability considerations and medication administration techniques are essential for maintaining optimal patient outcomes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Infusion Therapy Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.37% |

|

Market growth 2024-2028 |

USD 21.18 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.45 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Infusion Therapy Devices Market Research and Growth Report?

- CAGR of the Infusion Therapy Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the infusion therapy devices market growth of industry companies

We can help! Our analysts can customize this infusion therapy devices market research report to meet your requirements.

RIA -

RIA -