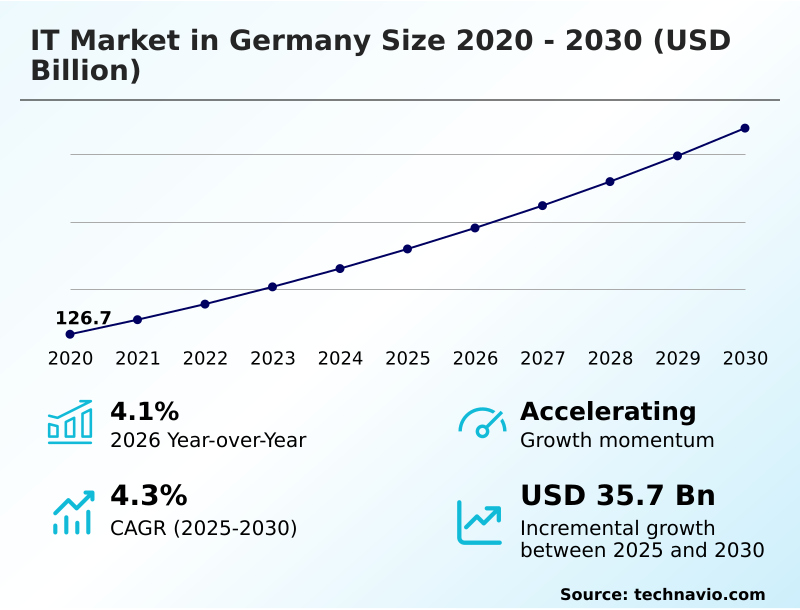

Germany IT Market Size 2026-2030

The germany it market size is valued to increase by USD 35.7 billion, at a CAGR of 4.3% from 2025 to 2030. Strategic pivot toward digital sovereignty and sovereign cloud infrastructure will drive the germany it market.

Major Market Trends & Insights

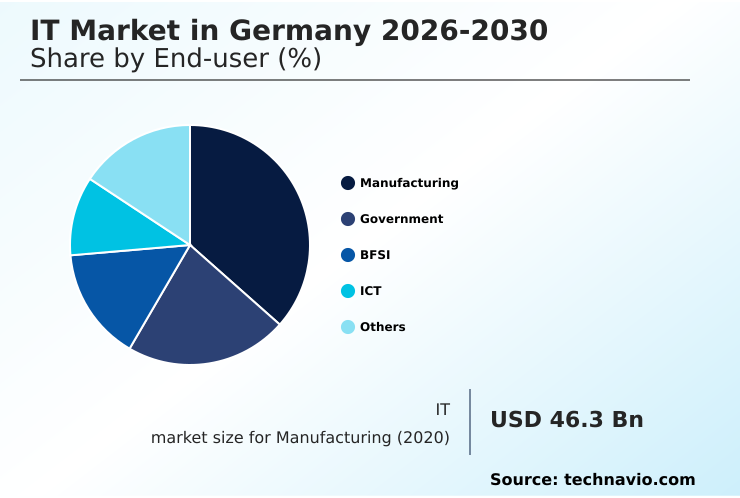

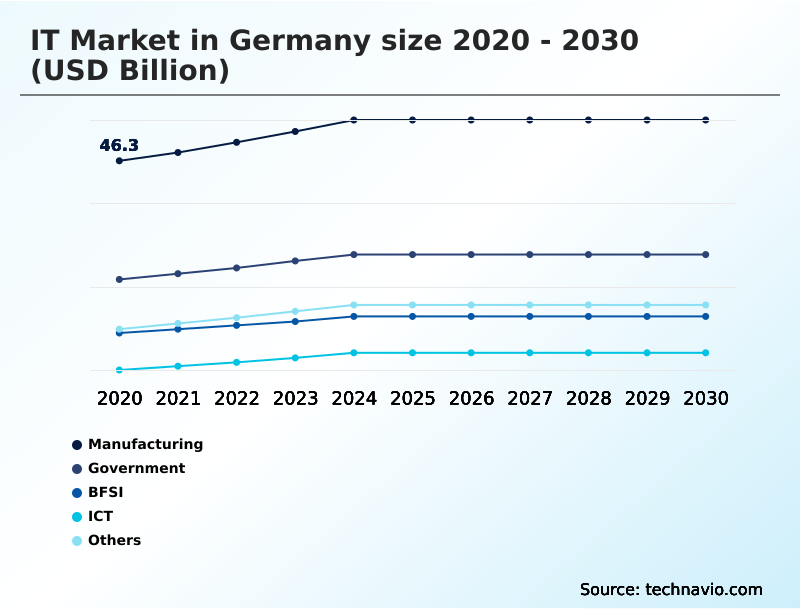

- By End-user - Manufacturing segment was valued at USD 52.7 billion in 2024

- By Application - Large enterprise segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 60.9 billion

- Market Future Opportunities: USD 35.7 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The IT market in Germany is defined by a strategic push toward technological self-determination and advanced industrial modernization. A core focus is the development of a sovereign cloud infrastructure, compelling organizations to prioritize data residency controls and adopt sovereign-compliant service models.

- Concurrently, the manufacturing backbone is undergoing a transformation through the widespread adoption of industrial artificial intelligence and digital twin technology to enhance supply chain resilience and operational efficiency. For instance, a mid-sized automotive supplier might leverage a sovereign industrial AI cloud to run simulations, optimizing production lines with software-defined automation without compromising sensitive design data.

- This innovation is tempered by significant regulatory pressures, including stringent NIS2 directive compliance and the implementation of the EU AI Act, which demand robust cybersecurity resilience.

- Enterprises are navigating this complex landscape by investing in managed security services and zero-trust architecture, balancing the drive for innovation through generative AI integration with the critical need for compliance and security in an increasingly interconnected ecosystem. This dynamic creates both challenges and opportunities for providers of industrial software development and hybrid work environments.

What will be the Size of the Germany IT Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Germany IT Market Segmented?

The germany it industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Manufacturing

- Government

- BFSI

- ICT

- Others

- Application

- Large enterprise

- SMEs

- Service

- Hosted service

- Managed service

- Geography

- Europe

- Germany

- Europe

By End-user Insights

The manufacturing segment is estimated to witness significant growth during the forecast period.

The manufacturing sector is advancing its IT strategy, shifting toward software-defined production to maintain a competitive edge. This transition involves the deep integration of industrial artificial intelligence and digital twin technology, enabling predictive maintenance models and enhancing operational efficiency.

The adoption of high-performance computing resources and industrial SaaS solutions is accelerating, particularly among small and mid-sized enterprises aiming to improve automated quality control. A key focus is on operational technology cybersecurity to protect interconnected smart factories.

As firms pursue software-defined automation, nearly 20% of IT spending is now allocated to defensive infrastructure, including zero-trust architecture.

This investment in cybersecurity resilience underscores the sector's commitment to securing its increasingly complex and digitized production environments, which rely on intelligent smart meter gateways.

The Manufacturing segment was valued at USD 52.7 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The IT market in Germany 2026-2030 is experiencing a multifaceted transformation, with growth in IT market in Germany 2026-2030 application development services being driven by the need for enterprise software modernization. A central theme is the rising IT market in Germany 2026-2030 sovereign cloud adoption rates, as organizations prioritize data control.

- This is closely linked to the demand for enhanced IT market in Germany 2026-2030 cybersecurity resilience, fueling IT market in Germany 2026-2030 managed security services growth. The IT market in Germany 2026-2030 impact of nis2 directive is significant, mandating stricter security protocols across numerous sectors.

- In manufacturing, firms are navigating IT market in Germany 2026-2030 industrial ai implementation challenges while leveraging IT market in Germany 2026-2030 digital twin simulation for manufacturing to improve efficiency, with some achieving double-digit reductions in prototyping costs.

- However, IT market in Germany 2026-2030 data center grid capacity constraints and the IT market in Germany 2026-2030 specialized it workforce shortage pose substantial hurdles. Concurrently, IT market in Germany 2026-2030 smb digitalization trends are accelerating, supported by demand for strong IT market in Germany 2026-2030 it consulting services demand.

- The landscape is further shaped by IT market in Germany 2026-2030 ai act compliance costs, the migration to IT market in Germany 2026-2030 cloud-native environment migration, and rising IT market in Germany 2026-2030 industrial iot platform adoption.

- Key growth areas include IT market in Germany 2026-2030 public sector digital transformation, IT market in Germany 2026-2030 financial services technology spending, IT market in Germany 2026-2030 5g network slicing use cases, and the deployment of IT market in Germany 2026-2030 software-defined infrastructure solutions alongside IT market in Germany 2026-2030 green data center investments.

What are the key market drivers leading to the rise in the adoption of Germany IT Industry?

- A strategic pivot toward digital sovereignty and the development of sovereign cloud infrastructure is the key driver stimulating market growth.

- Market growth is propelled by a concentrated push toward digital sovereignty, compelling investments in localized infrastructure with strict data residency controls.

- This governmental focus on a digital sovereignty mandate has led to initiatives such as sovereign cloud hubs, which are critical for the public sector and regulated industries.

- A second major driver is the integration of industrial AI and digital twin for port operations, which helps maintain global competitiveness and address labor shortages; implementing these technologies can reduce pre-production testing costs by over 20%.

- The third driver is intensifying regulatory pressure, with the NIS2 directive bringing over 29,000 companies under new supervision.

- This creates a mandatory investment cycle in cybersecurity, including automated threat detection tools and sovereign-compliant service models, to meet stringent new compliance and reporting standards.

What are the market trends shaping the Germany IT Industry?

- The ascendance of artificial intelligence as the primary vector for enterprise transformation is emerging as a defining market trend. This shift signifies a move from experimental adoption to the strategic integration of AI in core business operations.

- Key market trends reflect a structural reorganization around intelligent and resilient systems. The strategic adoption of generative AI integration is shifting from pilot programs to core business functions, with 86% of tech startups identifying AI as the year's most defining trend. This is driving the development of AI-powered tutoring platforms and autonomous technologies.

- Concurrently, the cybersecurity sector is evolving toward proactive resilience, spurred by a historical peak in ransomware incidents and new regulatory mandates. This has led to a significant rise in contracts for managed detection and response and the adoption of zero-trust access management.

- Furthermore, sustainability is a dominant trend, with a focus on green data center innovation, circular economy for IT, and waste heat utilization, transforming digital infrastructure into an active component of the energy transition, supported by software-defined networking and AI-driven network optimization.

What challenges does the Germany IT Industry face during its growth?

- Structural shortages in the specialized IT workforce present a key challenge, affecting the pace of industry growth and digital transformation initiatives.

- The market faces significant operational and structural challenges that temper its growth trajectory. A primary constraint is the structural shortage of skilled professionals, with approximately 109,000 IT positions remaining unfilled, and the average time to fill a specialized role is nearly eight months, which severely hampers project timelines.

- Another challenge is the complexity of regulatory compliance, particularly with the EU AI Act, which introduces administrative burdens and potential financial penalties that cause some firms to delay innovation.

- Furthermore, infrastructural bottlenecks, including severe power grid limitations and long high-voltage connection lead times for data centers, are hindering the expansion of the high-performance computing resources needed to support the nation's digital ambitions. These constraints impact everything from industrial software development to health data use act implementation.

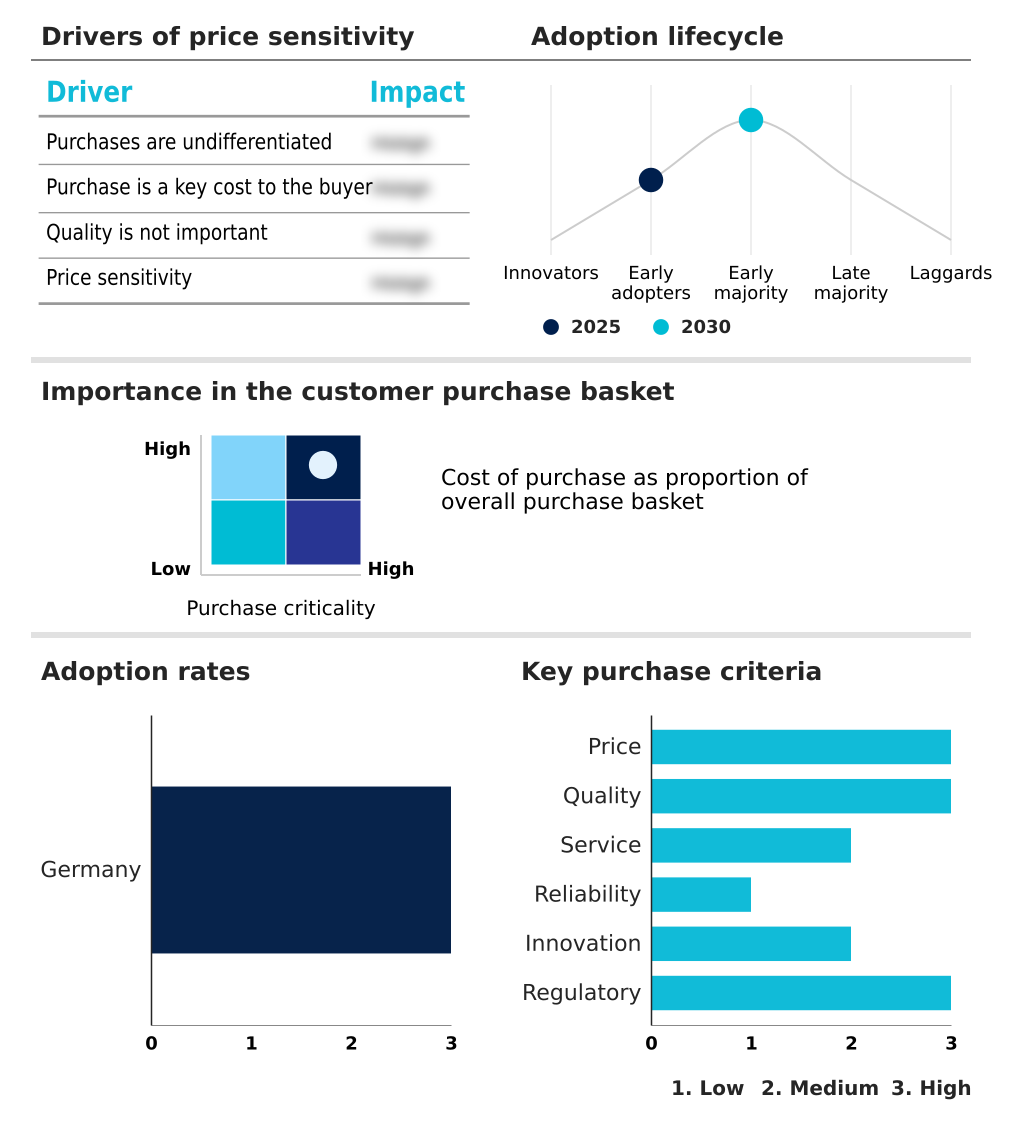

Exclusive Technavio Analysis on Customer Landscape

The germany it market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the germany it market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Germany IT Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, germany it market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Key offerings include IT consulting, digital transformation, cloud infrastructure, cybersecurity resilience, and specialized enterprise software platforms for diverse industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- BearingPoint Holding BV

- Capgemini SE

- CGI Inc.

- DATEV eG

- Diebold Nixdorf Incorp.

- Fujitsu Ltd.

- HARTING Technology Group

- IBM Corp.

- Infineon Technologies AG

- Infosys Ltd.

- Nemetschek SE

- NTT DATA Corp.

- Robert Bosch GmbH

- SAP SE

- Siemens AG

- Software AG

- Sopra Steria Group SA

- T-Systems International GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Germany it market

- In November, 2024, Google announced a substantial investment to expand its data center infrastructure, focusing on a new facility in Dietzenbach and the expansion of its Hanau campus to meet growing AI and cloud service demands.

- In October, 2024, Deutsche Telekom and NVIDIA unveiled a sovereign industrial AI cloud in Berlin, designed to support large-scale simulations and digital twin technology for the nation's industrial sector.

- In September, 2024, a consortium of leading companies launched the 'Made for Germany' initiative, committing significant capital toward research, development, and digital transformation projects through 2028.

- In January, 2025, the German and French governments held a summit to advance a joint task force on European digital sovereignty, aiming to bolster the continent's competitiveness and reduce technological dependencies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Germany IT Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 193 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 35.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | Germany |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The IT market in Germany is undergoing a foundational shift, driven by the dual imperatives of digital sovereignty and industrial competitiveness. This evolution is marked by strategic investments in sovereign cloud infrastructure and the aggressive integration of industrial artificial intelligence, particularly within the nation's manufacturing core.

- A recent survey indicating that 86% of technology startups view AI as the year's defining trend reflects a market-wide consensus that is now translating into boardroom strategy, where budgets are reallocated for the development of predictive maintenance models and software-defined automation. Enterprises are navigating this transition by adopting digital twin technology and migrating legacy ERP systems to more agile platforms.

- The entire ecosystem is focused on achieving operational technology cybersecurity and ensuring NIS2 directive compliance through robust managed security services and zero-trust architecture.

- This complex environment, which also prioritizes green data center innovation and circular IT hardware, demands a holistic approach to technology adoption, balancing innovation with the stringent requirements of a regulated and resource-conscious market, including the adoption of 5G standalone networks and autonomous warehouse robotics.

What are the Key Data Covered in this Germany IT Market Research and Growth Report?

-

What is the expected growth of the Germany IT Market between 2026 and 2030?

-

USD 35.7 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Manufacturing, Government, BFSI, ICT, and Others), Application (Large enterprise, and SMEs), Service (Hosted service, and Managed service) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Strategic pivot toward digital sovereignty and sovereign cloud infrastructure, Structural shortages in specialized IT workforce

-

-

Who are the major players in the Germany IT Market?

-

Accenture Plc, Atos SE, BearingPoint Holding BV, Capgemini SE, CGI Inc., DATEV eG, Diebold Nixdorf Incorp., Fujitsu Ltd., HARTING Technology Group, IBM Corp., Infineon Technologies AG, Infosys Ltd., Nemetschek SE, NTT DATA Corp., Robert Bosch GmbH, SAP SE, Siemens AG, Software AG, Sopra Steria Group SA and T-Systems International GmbH

-

Market Research Insights

- Market dynamics are shaped by a pronounced tension between ambitious innovation and pressing operational constraints. The strategic adoption of enterprise-wide artificial intelligence and cloud-native environments is a key priority, yet progress is often impeded by significant talent gaps. For example, the average time to fill a specialized IT position remains over seven months, delaying critical projects.

- In response to a heightened threat landscape, enterprises now allocate approximately 18% of their IT budgets to defensive initiatives, favoring managed security services and zero-trust access management.

- This environment fosters demand for FinOps-as-a-service modules to control costs in complex multi-cloud environments and drives investment in transformation incentive programs that accelerate the modernization of legacy systems, creating a market where efficiency and security are paramount.

We can help! Our analysts can customize this germany it market research report to meet your requirements.

RIA -

RIA -