IT Outsourcing Market Size 2026-2030

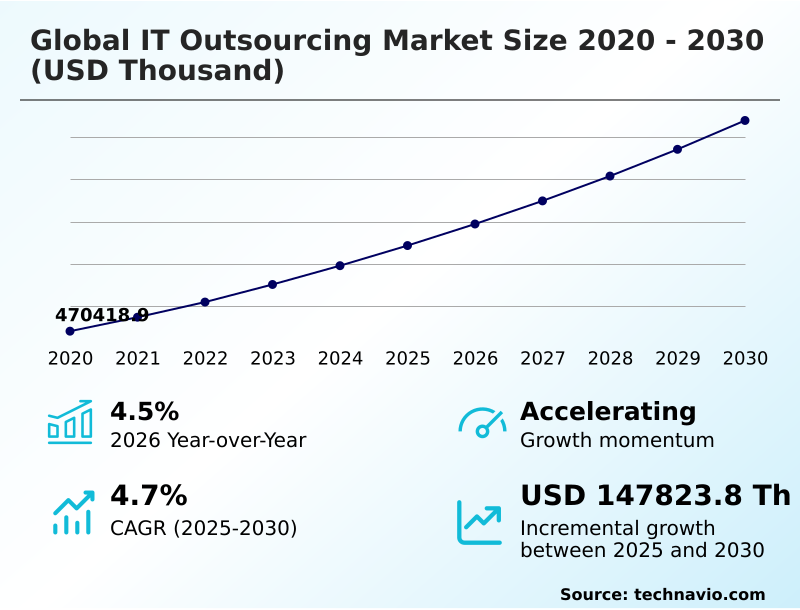

The it outsourcing market size is valued to increase by USD 147.82 million, at a CAGR of 4.7% from 2025 to 2030. Generative AI integration and AI-native service delivery will drive the it outsourcing market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 34.2% growth during the forecast period.

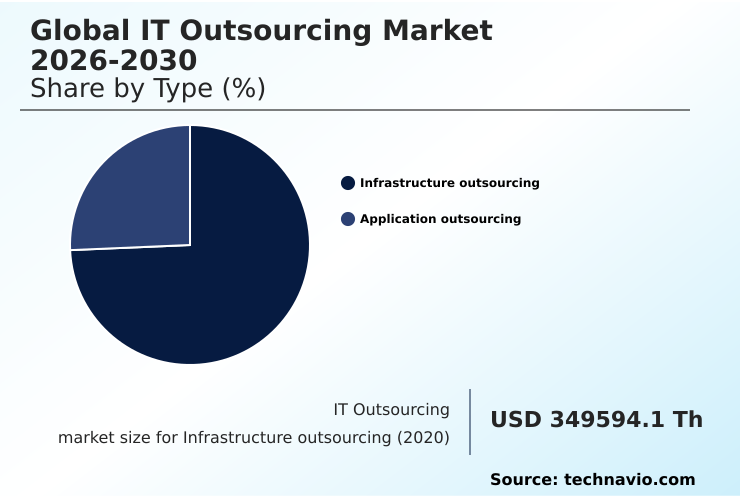

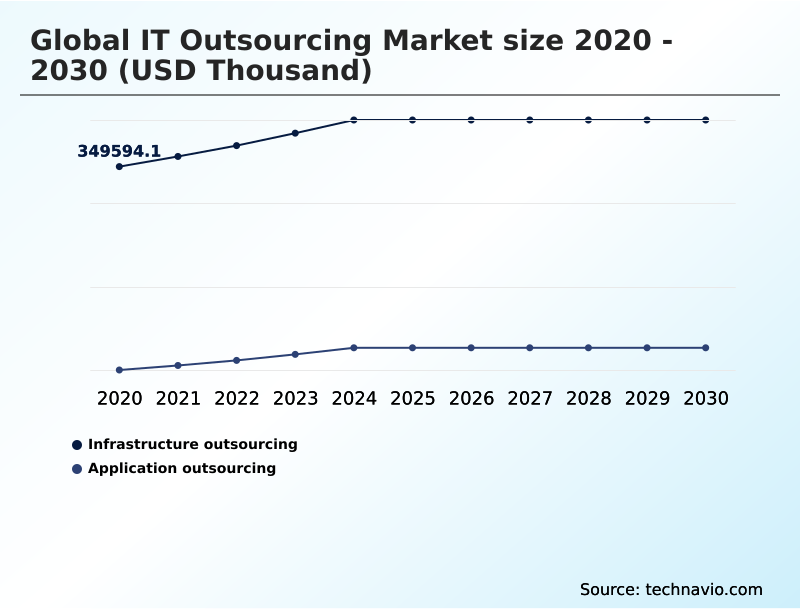

- By Type - Infrastructure outsourcing segment was valued at USD 402.02 million in 2024

- By Service - Software as a service segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 147.82 million

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The IT outsourcing market is undergoing a significant transformation, moving beyond traditional cost-saving engagements to become a strategic enabler of digital innovation. This evolution is driven by the increasing need for specialized expertise in areas like generative artificial intelligence, cloud-native services, and cybersecurity.

- As organizations adopt multi-sourcing strategies, they are shifting from monolithic contracts to agile partnerships that leverage niche capabilities. A key aspect of this shift is the adoption of outcome-based pricing, where provider compensation is tied to measurable business impacts.

- For instance, a manufacturing firm might engage a service provider to implement an AI-driven predictive maintenance system for its supply chain, with payments linked to verified reductions in equipment downtime and operational cost savings of up to 15%. This value-driven approach fosters a more collaborative environment, where outsourced teams function as integrated extensions of the core business.

- The rise of global capability centers further redefines the client-provider relationship, enabling companies to maintain control over intellectual property while accessing a global talent pool. This market is also shaped by a heightened focus on ESG criteria, making sustainability a critical factor in vendor selection processes, particularly in North America and Europe.

What will be the Size of the IT Outsourcing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the IT Outsourcing Market Segmented?

The it outsourcing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Infrastructure outsourcing

- Application outsourcing

- Service

- Software as a service

- Infrastructure as a service

- Platform as a service

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- India

- China

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The infrastructure outsourcing segment is estimated to witness significant growth during the forecast period.

The IT outsourcing market is segmented by type, service, end-user, and geography. Infrastructure outsourcing involves delegating physical and virtual asset management, including cloud environments and network security, to external providers. This approach helps mitigate capital expenditures on proprietary server farms.

The shift to hybrid and multi-cloud architectures requires partners proficient in integrating legacy systems with modern software-defined networking.

The application outsourcing segment includes the development, maintenance, and management of software applications, enabling enterprises to access specialized talent and advanced methodologies like agile development and DevOps integration.

These services accelerate time-to-market for digital products and modernize outdated systems for enhanced performance and security. The end-user segments comprise large enterprises and SMEs, with the latter increasingly leveraging outsourcing for digital maturity.

The service segment includes software-as-a-service (SaaS), platform-as-a-service (PaaS), and infrastructure-as-a-service (IaaS), providing varied levels of control and management.

The Infrastructure outsourcing segment was valued at USD 402.02 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How IT Outsourcing Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the IT outsourcing market is diverse, with North America and APAC representing the largest segments, contributing 32.79% and 34.23% to the global incremental growth, respectively.

North America, driven by the US and Canada, continues to be a primary revenue generator, focusing on high-value services like AI integration and cloud-native application development.

The region's high labor costs and talent shortages compel firms to seek external expertise for complex tasks. APAC is the fastest-growing region, with India and China leading as both major suppliers and consumers of IT services.

This region is shifting from labor arbitrage to high-end R&D and intellectual property creation, supported by government initiatives and a vast talent pool.

Europe remains a mature market focused on data sovereignty and nearshoring, while South America and the Middle East and Africa are emerging as strategic nearshore and high-investment hubs, respectively.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

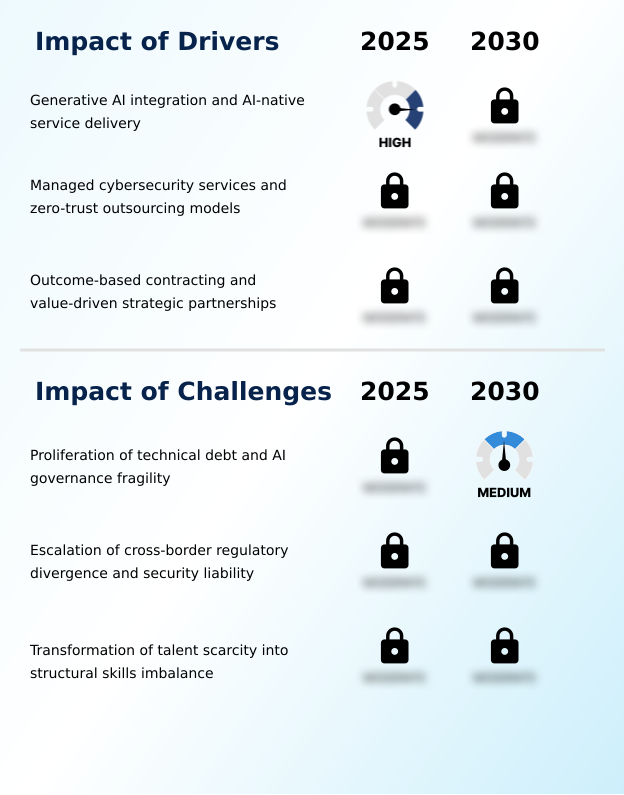

- The IT outsourcing market is at a pivotal juncture, where the impact of generative AI on IT outsourcing models is reshaping service delivery. This transition, however, introduces challenges in managing technical debt in legacy systems, making application modernization a critical focus.

- In response, organizations are realizing the benefits of sovereign cloud for data residency, which addresses escalating concerns over cross-border regulatory divergence in outsourcing. To fortify security, the role of zero-trust models in outsourced security is becoming standard practice. Strategically, businesses are comparing nearshore vs.

- offshore IT outsourcing strategies to balance cost, agility, and time-zone alignment, a decision now complicated by the structural skills imbalance for site reliability engineering. The question of how AI governance affects outsourcing partnerships is central to new contracts, which are increasingly implementing outcome-based pricing in service contracts.

- These performance-based models for infrastructure management, sometimes tracked with digital twins for tracking outsourcing KPIs, promise greater value alignment. Concurrently, the upskilling workforce for cloud-native environments is a non-negotiable investment. Firms are deploying DevSecOps in a multi-sourcing strategy and using agentic workflow automation in business process outsourcing to enhance efficiency.

- The rise of low-code platforms is also democratizing development, with some firms reporting project accelerations twice that of traditional methods. Using global capability centers and integrating sustainable technology are becoming key differentiators.

What are the key market drivers leading to the rise in the adoption of IT Outsourcing Industry?

- The integration of generative AI and the shift toward AI-native service delivery models are key drivers propelling market growth.

- The IT outsourcing market is propelled by the rapid integration of generative artificial intelligence and the evolution of AI-native service delivery.

- This driver is characterized by automated workflows where AI-driven co-pilots and code generators significantly accelerate project timelines, forcing providers to modernize operating models with proprietary AI tools.

- Another key driver is the rise of managed cybersecurity services and zero-trust outsourcing models. Escalating cyber threats and complex regulations have made specialized security outsourcing a priority, with providers offering end-to-end solutions.

- This shift is supported by fiscal policies in key regions, such as the establishment of a uniform safe harbor margin of 15.5% for IT services, which provides stability for large-scale international operations.

- Finally, the strategic evolution toward outcome-based contracting and value-driven partnerships continues to fuel growth, linking compensation to measurable business results and incentivizing innovation.

What are the market trends shaping the IT Outsourcing Industry?

- The growth of sovereign cloud infrastructure services is an upcoming market trend, driven by the increasing need for data localization and compliance with regional regulations.

- Key trends are reshaping the IT outsourcing market, with a significant structural realignment toward sovereign cloud infrastructure. This shift is driven by the need for digital independence and compliance with data residency requirements, with spending on sovereign cloud solutions increasing by 35.6% in some regions.

- The adoption of outcome-based managed services is another critical trend, as over 50% of new contracts now tie compensation to performance metrics, reflecting a move toward value-driven partnerships. This requires advanced data analytics for tracking KPIs like system uptime and digital transformation velocity.

- Furthermore, the integration of sustainable technology and green outsourcing mandates is becoming standard, with providers selected based on their carbon footprint and ability to optimize cloud resources. This push for circular IT and green coding initiatives aligns with corporate net-zero goals, transforming digital transformation into a driver of environmental stewardship.

What challenges does the IT Outsourcing Industry face during its growth?

- The proliferation of technical debt and the fragility of AI governance frameworks present a key challenge to the industry's growth trajectory.

- The IT outsourcing market faces significant challenges, primarily the proliferation of technical debt and the fragility of AI governance. The rapid deployment of proprietary AI solutions by outsourcing providers creates complexities around intellectual property and exit planning, while the need for human-in-the-loop oversight adds non-discretionary costs. Another major challenge is the escalation of cross-border regulatory divergence and security liability.

- Navigating overlapping data privacy laws and the multiplied entry points from distributed cloud architectures force partners to assume greater legal responsibility, increasing the cost of compliance audits. Finally, the transformation of talent scarcity into a structural skills imbalance is a critical restraint.

- While a large technical workforce exists, there is a shortage of professionals with dual expertise in managing cloud-native environments and AI-optimized servers, with at least 80% of enterprises now moving toward deploying autonomous AI agents.

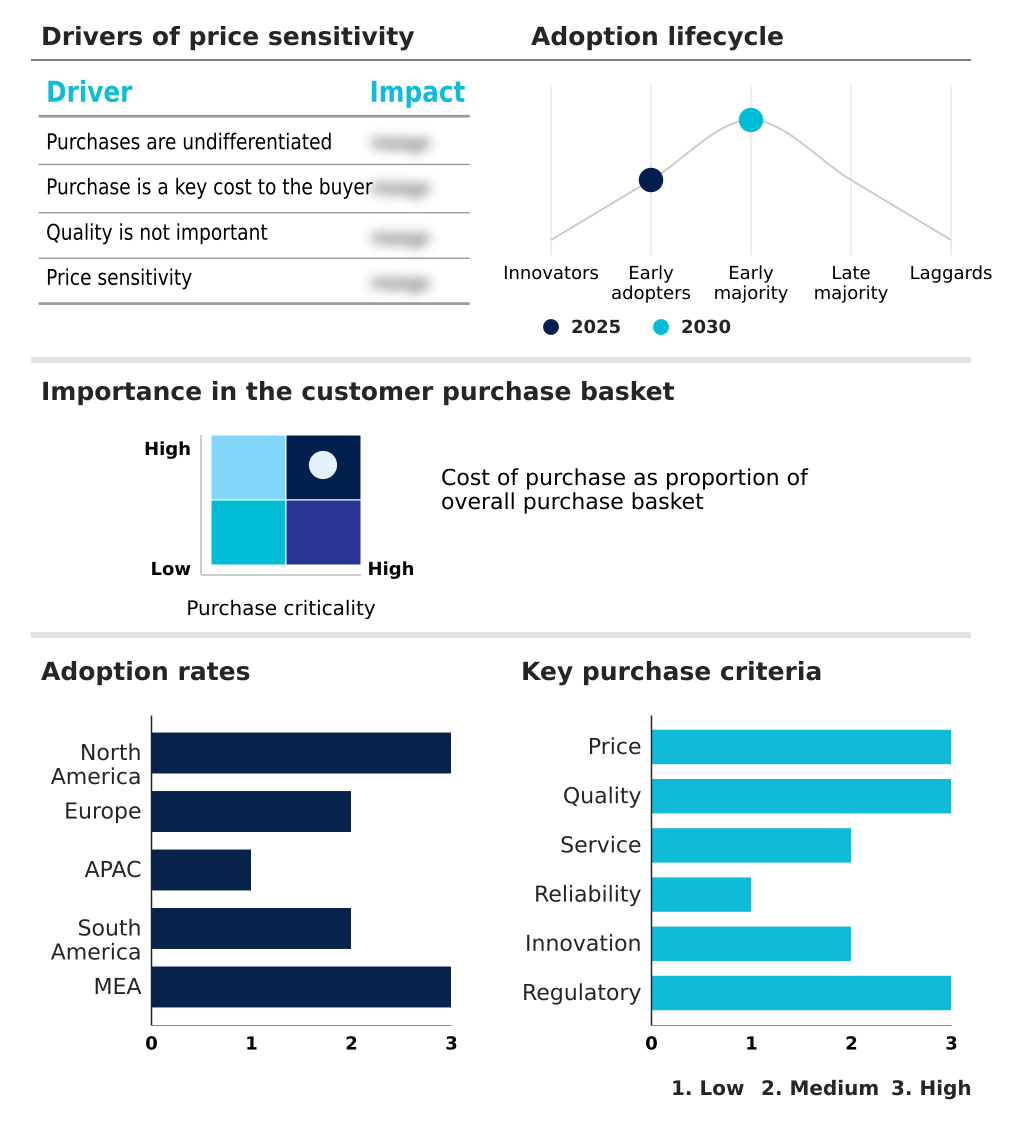

Exclusive Technavio Analysis on Customer Landscape

The it outsourcing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the it outsourcing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of IT Outsourcing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, it outsourcing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Delivering application outsourcing and infrastructure managed services to support enterprise digital transformation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Capgemini SE

- CGI Inc.

- Cognizant Technology Solution

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Hexaware Technologies Ltd.

- IBM Corp.

- Infosys Ltd.

- Leidos Holdings Inc.

- Mphasis Ltd.

- NTT DATA Corp.

- Stefanini Group

- Tata Consultancy Services

- Tech Mahindra Ltd.

- Unisys Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in It outsourcing market

- In March 2025, Accenture Plc expanded its strategic partnership with Microsoft to launch a forward-deployed engineering practice, aiming to help enterprises rapidly operationalize AI across their operations.

- In February 2025, Infosys announced a strategic partnership with Citizens Financial Group to launch an AI-first Innovation Hub, seeking to accelerate agentic AI-led transformation across banking operations and customer experience.

- In February 2025, the Indian government's Union Budget introduced a uniform safe harbor margin of 15.5% for IT services, providing fiscal predictability for large-scale international security and data processing operations.

- In January 2025, industry reports confirmed that the move toward value-linked models has introduced new legal and operational considerations around data integrity and shared liability allocation in over 50% of new contracts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled IT Outsourcing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 147823.8 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, The Netherlands, Italy, Spain, India, China, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The IT outsourcing market is fundamentally shifting towards high-value, strategic partnerships. The integration of generative artificial intelligence and AI-native service delivery is now a core component, moving beyond simple cost arbitrage. Organizations are leveraging AI-driven co-pilots and code generators to accelerate project timelines, while automated testing and predictive analytics enhance system reliability.

- This evolution necessitates robust AI governance to manage technical debt and ensure intellectual property clarity. A significant trend is the adoption of sovereign cloud infrastructure to comply with data residency mandates, a boardroom-level concern that directly impacts global strategy and risk management. This move is complemented by the implementation of zero-trust outsourcing models for heightened security.

- As firms adopt these advanced cloud-native services, many are achieving over 30% improvement in deployment frequencies. The market's future hinges on the ability of providers to offer not just technical execution but also strategic guidance through complex transformations involving agentic workflows, DevSecOps, and site reliability engineering.

What are the Key Data Covered in this IT Outsourcing Market Research and Growth Report?

-

What is the expected growth of the IT Outsourcing Market between 2026 and 2030?

-

USD 147.82 million, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Infrastructure outsourcing, and Application outsourcing), Service (Software as a service, Infrastructure as a service, and Platform as a service), End-user (Large enterprises, and SMEs) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Generative AI integration and AI-native service delivery, Proliferation of technical debt and AI governance fragility

-

-

Who are the major players in the IT Outsourcing Market?

-

Accenture Plc, Atos SE, Capgemini SE, CGI Inc., Cognizant Technology Solution, DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., Hewlett Packard Enterprise Co., Hexaware Technologies Ltd., IBM Corp., Infosys Ltd., Leidos Holdings Inc., Mphasis Ltd., NTT DATA Corp., Stefanini Group, Tata Consultancy Services, Tech Mahindra Ltd., Unisys Corp. and Wipro Ltd.

-

Market Research Insights

- The dynamics of the IT outsourcing market are increasingly shaped by a strategic pivot toward value-driven partnerships and performance-based models. Over 50% of new outsourcing contracts are now structured around outcome-based metrics, a significant shift from traditional billing.

- This evolution is fueled by the need for tangible business results, where shared-risk agreements and managed cybersecurity services incentivize providers to drive innovation and reduce operational costs. The adoption of DevOps practices and SecOps is allowing organizations to consolidate vendor landscapes for better oversight, with some achieving a 15% reduction in total cost of ownership.

- This trend is particularly influential for managed services, forcing providers to adopt leaner squads that utilize advanced methodologies for continuous delivery. As organizations align IT spending with measurable KPIs, the role of outcome-based delivery remains a fundamental component of market differentiation.

We can help! Our analysts can customize this it outsourcing market research report to meet your requirements.

RIA -

RIA -