Kidney Stones Management Devices Market Size 2024-2028

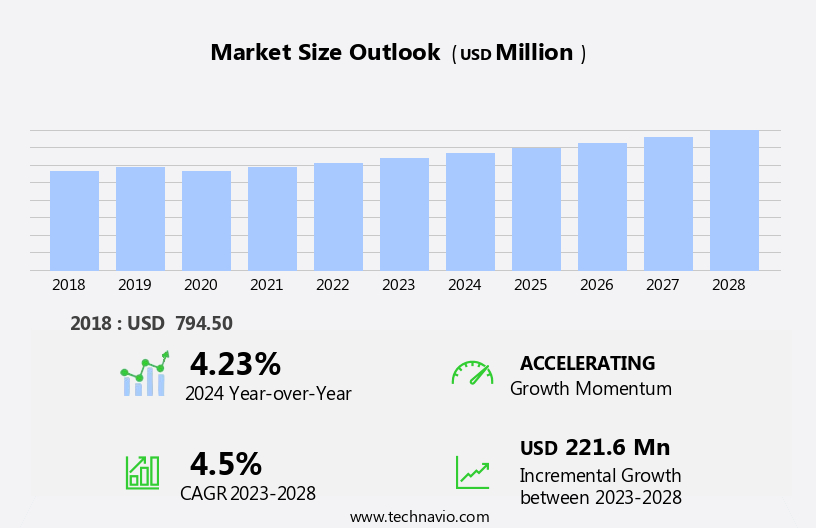

The kidney stones management devices market size is forecast to increase by USD 221.6 million, at a CAGR of 4.5% between 2023 and 2028.

- The market is witnessing significant advancements in technologies, revolutionizing the treatment landscape. Innovations in imaging technologies, such as digital flexible ureteroscopes, are gaining popularity due to their ability to provide real-time visualization during minimally invasive procedures. However, the high cost of treatment remains a substantial challenge for both patients and healthcare providers, potentially limiting market growth. Despite this hurdle, opportunities exist for companies to capitalize on the technological advancements and address affordability concerns through cost-effective solutions and financing options.

- By focusing on these opportunities and navigating the cost challenge effectively, market participants can position themselves for success in the evolving market.

What will be the Size of the Kidney Stones Management Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The kidney stones management market continues to evolve, driven by advancements in technology and growing demand for minimally invasive treatments. Cystine stones, one of the less common types of kidney stones, pose unique challenges due to their chemical composition. To address this, innovations in lithotripsy technology, such as kidney stone fragmentation devices, have emerged, enabling effective treatment. Patient monitoring plays a crucial role in the management of kidney stones, with imaging techniques like ultrasound guidance and CT scans facilitating accurate diagnosis and follow-up. The recurrence of kidney stones is a significant concern, necessitating ongoing research and development in this area.

Ureteroscopy procedure, a minimally invasive surgical method, has gained popularity in the treatment of kidney stones. Postoperative care, including nephrostomy tube placement and ureteral stent usage, ensures proper healing and reduces complications. Extracorporeal shock wave technology, a non-invasive treatment option, offers significant advantages in terms of procedure success rate and recovery time. However, managing pain during and after the procedure is essential, with pain management techniques playing a critical role. Uric acid stones, calcium oxalate stones, and struvite stones each present distinct challenges, necessitating tailored treatment approaches. The quality of life and patient satisfaction are key considerations, with treatment duration being a significant factor in the overall patient experience.

Continuous advancements in technology, such as the kidney stone laser and percutaneous nephrolithotomy, offer promising solutions for the effective management of kidney stones. Complication management and stone burden reduction remain key areas of focus, ensuring the best possible outcomes for patients.

How is this Kidney Stones Management Devices Industry segmented?

The kidney stones management devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Method

- URS

- ESWL

- PCNL

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

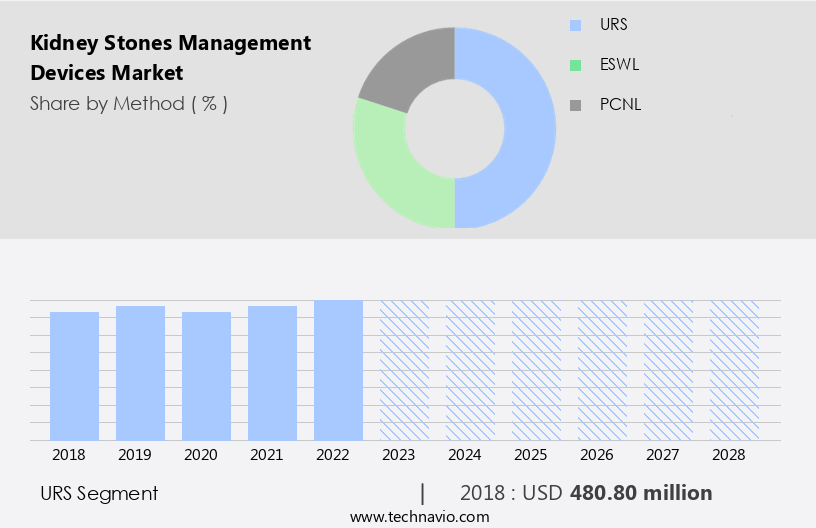

By Method Insights

The urs segment is estimated to witness significant growth during the forecast period.

The kidney stones management market is witnessing significant advancements with the increasing prevalence of kidney stones and the development of innovative technologies. Cystine stones, a rare type of kidney stone, are managed through various methods such as stone fragmentation devices and surgical stone removal. Patient monitoring and imaging techniques play a crucial role in diagnosing and managing kidney stones. Ureteroscopy procedure, a minimally invasive surgery, is used for small stones in the ureter, with success rates reaching up to 95%. Extracorporeal shock wave lithotripsy (ESWL) is another popular treatment option for kidney stones, particularly for those with uric acid or calcium oxalate composition.

Recurrence of kidney stones remains a concern, leading to the development of devices and techniques for stone burden reduction and complication management. Imaging techniques like ultrasound, CT scan, and x-ray fluoroscopy are used for preoperative assessment and postoperative care. Ureteral stent placement and nephrostomy tube insertion are common postoperative care measures. Minimally invasive surgeries like percutaneous nephrolithotomy and laparoscopic surgery are gaining popularity due to shorter recovery times and reduced complications. Pain management techniques, including analgesics and anesthesia, are essential during surgical procedures. Quality of life and patient satisfaction are key considerations in kidney stone management. Procedure success rates, treatment duration, and device efficacy are critical factors influencing market trends.

Urologists and researchers continue to explore new methods for managing kidney stones, including urinary tract infection treatment and the use of kidney stone lasers. The market is expected to grow as the demand for effective and minimally invasive treatments increases.

The URS segment was valued at USD 480.80 million in 2018 and showed a gradual increase during the forecast period.

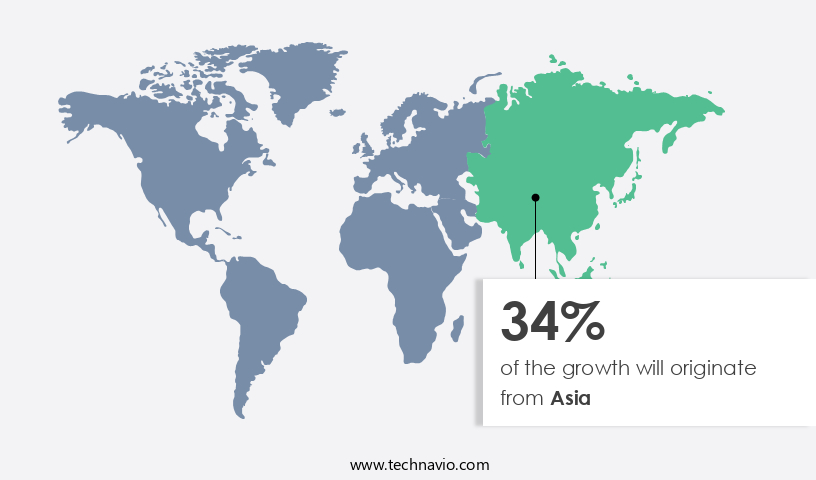

Regional Analysis

Asia is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the US and Canadian market for kidney stones management devices, the demand for advanced medical technologies is high due to the increasing prevalence of kidney stones. Approximately 100,000 people in Canada per one million population experience kidney stones at some point in their lives. The adoption of minimally invasive treatments like ureteroscopy (URS) and extracorporeal shock wave lithotripsy (ESWL) is increasing, driven by their effectiveness in managing various types of kidney stones, including cystine, uric acid, calcium oxalate, and struvite. Patient monitoring, imaging techniques, and pain management techniques are essential components of kidney stones management, ensuring proper diagnosis, treatment, and postoperative care.

The success rate of procedures like percutaneous nephrolithotomy (PCNL) and lithotripsy technology plays a significant role in patient satisfaction and quality of life. Complication management, stone burden reduction, and urinary tract infection treatment are also crucial aspects of the market. The use of imaging techniques like ultrasound guidance, CT scan, and X-ray fluoroscopy aids in accurate diagnosis and treatment planning. Nephrostomy tubes, ureteral stents, and preoperative assessments are essential for effective postoperative care and recovery time management. The market's growth is further driven by the availability of advanced healthcare infrastructure and the presence of leading companies. The focus on minimally invasive surgery and continuous advancements in device efficacy contribute to the market's evolution.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of technological innovations aimed at diagnosing, treating, and preventing the formation and recurrence of kidney stones. This market has witnessed significant advancements in recent years, driven by the increasing prevalence of kidney stones and the growing demand for minimally invasive and effective treatment options. One of the most noteworthy trends in this market is the development of extracorporeal shock wave lithotripsy (ESWL) devices. These non-invasive systems utilize high-energy shock waves to fragment kidney stones, allowing for their easy removal from the body. Another area of growth is the use of ureteroscopes and lasers for the removal of stones located in the ureter or renal pelvis. Moreover, the integration of imaging technologies, such as CT scans and ultrasounds, into kidney stones management devices has significantly improved diagnostic accuracy and treatment planning. Additionally, the ongoing research and development of minimally invasive surgical techniques, such as laparoscopic and robotic-assisted procedures, are expected to further expand the market's scope. The application of these advanced technologies extends beyond hospitals and clinics to include ambulatory surgical centers and home healthcare settings. This trend towards decentralized care delivery models is driven by the need for cost-effective and convenient treatment options for patients. In conclusion, the market continues to evolve, offering innovative solutions for the diagnosis, treatment, and prevention of kidney stones. The integration of advanced imaging technologies, minimally invasive surgical techniques, and decentralized care delivery models are key drivers of market growth and innovation.

What are the key market drivers leading to the rise in the adoption of Kidney Stones Management Devices Industry?

- The significant advancements in kidney stones treatment technologies serve as the primary market driver.

- Kidney stones management devices have seen significant advancements in the past three decades, revolutionizing the treatment landscape. Traditional open surgical procedures have largely been replaced by minimally invasive techniques such as Shock Wave Lithotripsy (SWL), ureteroscopy (URS), and percutaneous nephrolithotomy (PCNL). These innovations have improved treatment efficacy and patient comfort. Holmium laser technology has been a game-changer in the field, enabling the widespread adoption of URS for kidney stones treatment. This technology offers precision, flexibility, and reduced complications compared to open surgeries. Moreover, the development of miniaturized surgeries and disposable ureteroscopes has further enhanced the procedure's safety and accessibility.

- CT scans play a crucial role in the diagnosis and management of kidney stones, ensuring accurate identification and proper treatment planning. Pain management techniques, including anesthesia and analgesics, are also essential components of kidney stones treatment, ensuring patient comfort during procedures. Calcium oxalate stones are the most common type of kidney stones, and these devices are designed to effectively manage their treatment. However, the presence of urinary tract infections can complicate the treatment process and necessitate additional considerations. In conclusion, the market is driven by continuous research and development efforts aimed at improving treatment procedures, patient comfort, and overall outcomes.

- The adoption of advanced technologies, such as holmium laser and miniaturized surgeries, has significantly impacted the field, making treatments more effective and accessible.

What are the market trends shaping the Kidney Stones Management Devices Industry?

- The growing popularity of digital flexible ureteroscopes represents a significant market trend in the medical industry. These advanced medical devices offer enhanced imaging capabilities and greater maneuverability compared to traditional rigid ureteroscopes.

- In the realm of urology, advancements have been significant, particularly in the area of ureteroscopy (URS). Digital flexible ureteroscopes have emerged as a preferred choice over traditional fiber-optic ureteroscopes, offering several advantages. With higher maneuverability and superior visibility, digital flexible ureteroscopes enable better access to the ureter and kidney, leading to increased clarity and superior magnification. This results in a higher percentage of cases where the entire collecting system can be visualized. Moreover, the mean operating time for digital flexible ureteroscopes is less than that of fiber-optic ureteroscopes, while maintaining similar stone clearance rates. However, fiber-optic fibers lack durability and are more susceptible to breakage during passage through the ureter and extreme deflection.

- Stone fragmentation devices, such as extracorporeal shock wave lithotripsy (ESWL), and patient monitoring techniques, including imaging, play crucial roles in managing kidney stones. ESWL is a non-invasive procedure that uses high-energy shock waves to fragment the stones, while patient monitoring ensures effective postoperative care and kidney stone recurrence prevention. The success rate of these procedures depends on various factors, including the size, location, and composition of the stones. Cystine stones, for instance, are more challenging to treat due to their chemical composition. Therefore, ongoing research and development efforts are focused on improving these technologies and enhancing their efficacy.

What challenges does the Kidney Stones Management Devices Industry face during its growth?

- The escalating costs of treatment represent a significant barrier to the expansion and growth of the industry.

- Kidney stones, a common urological condition, account for the second most expensive treatment among similar conditions. The average costs for Percutaneous Nephrolithotomy (PCNL), Extracorporeal Shock Wave Lithotripsy (ESWL), and Ureteroscopic Stone Removal (URS) are approximately USD 3,800, USD 2,400, and USD 2,100, respectively. These costs include direct treatment expenses, consultation fees, and re-treatment charges. Advancements in technology have significantly increased the cost of kidney stones management devices. The digital flexible URS is a crucial component of endourology. However, the high cost of digital ureteroscopes is a significant concern. The price range for reusable digital ureteroscopes is between USD 23,000 and USD 26,000, excluding manufacturer contracts.

- Beyond the purchasing cost, the processing, maintenance, and repair expenses add to the overall cost. Uric acid stones, a common type of kidney stones, cause severe renal colic pain. To manage renal colic pain effectively, healthcare providers use various kidney stones management devices such as lithotripsy technology, ultrasound guidance, and X-ray fluoroscopy. These devices aid in surgical stone removal, stone burden reduction, and complication management. Lithotripsy technology, which uses shock waves to break down kidney stones, is a popular treatment option. Ultrasound guidance is essential during the procedure to ensure accurate stone localization. X-ray fluoroscopy is used for preoperative assessment and post-procedure evaluation.

- In conclusion, the high cost of kidney stones management devices, including digital ureteroscopes, significantly impacts the overall treatment cost. However, these devices play a crucial role in effectively managing kidney stones and alleviating renal colic pain.

Exclusive Customer Landscape

The kidney stones management devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the kidney stones management devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, kidney stones management devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allengers Medical Systems Ltd. - The company specializes in providing medical solutions for kidney stone management through innovative devices, including Ureteral Stents and Inlay Optima.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allengers Medical Systems Ltd.

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Coloplast AS

- Convergent Laser Technologies

- Cook Group Inc.

- DirexGroup

- Dornier MedTech GmbH

- E M S Electro Medical Systems S A

- EDAP TMS

- ELMED Medical Systems

- Inceler Medikal Co. Ltd.

- KARL STORZ SE and Co. KG

- Lumenis Be Ltd.

- Medispec Ltd.

- Olympus Corp.

- Richard Wolf GmbH

- Siemens AG

- Stryker Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Kidney Stones Management Devices Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the US Food and Drug Administration (FDA) approval of its new reusable lithotripsy system, the Dornier Duo D-Power, for the extracorporeal shock wave lithotripsy (ESWL) treatment of kidney stones. This approval marked a significant technological advancement in kidney stone management devices (Medtronic Press Release, 2024).

- In March 2024, Boston Scientific Corporation, a leading medical device company, entered into a strategic partnership with Cook Medical, a global medical technology company, to co-develop and commercialize a new generation of ureteroscopes for the treatment of kidney stones. This collaboration aimed to combine Boston Scientific's urology expertise with Cook Medical's ureteroscope technology (Boston Scientific Press Release, 2024).

- In May 2024, Merit Medical Systems, Inc., a leading manufacturer and marketer of medical devices, completed the acquisition of S.R.I. Medical Systems, a privately held company specializing in urological and nephrology devices, including the Stone Cone and LithoTrip systems for kidney stone management. This acquisition expanded Merit Medical's product portfolio and market presence in the market (Merit Medical Systems Press Release, 2024).

- In April 2025, Fresenius Medical Care AG & Co. KGaA, the world's leading provider of dialysis products and services, received FDA approval for its new lithotripsy system, the LithoStone, which integrates with its existing dialysis machines. This approval marked a significant geographic expansion for Fresenius Medical Care, as the LithoStone system was initially developed for European markets (Fresenius Medical Care Press Release, 2025).

Research Analyst Overview

- The market encompasses various technologies, including ultrasonic lithotripsy, shock wave lithotripsy, laser lithotripsy, and pneumatic lithotripsy. Treatment cost and patient demographics influence the choice of device features, such as anesthesia type and pulse duration. Device design and treatment parameters, including shock wave energy source and frequency settings, impact the effectiveness of these technologies. Holmium laser and thulium laser lithotripsy offer advantages for treating stones in specific locations, while surgical approach, such as rigid ureteroscopy and flexible ureteroscopy, vary based on stone burden and size. Clinical trials evaluate long-term outcomes and device safety, while medical imaging aids in diagnosing and monitoring stone composition and recurrence prevention.

- Stone composition and location, along with patient factors, influence treatment protocols. Device safety and hospital stay are crucial considerations for healthcare providers and patients. Energy source and power settings are essential factors in the successful fragmentation of stones, making them vital aspects of kidney stone management devices.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Kidney Stones Management Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

147 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 221.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Germany, UK, China, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Kidney Stones Management Devices Market Research and Growth Report?

- CAGR of the Kidney Stones Management Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the kidney stones management devices market growth of industry companies

We can help! Our analysts can customize this kidney stones management devices market research report to meet your requirements.

RIA -

RIA -