Latin America Cloud Computing Market Size 2026-2030

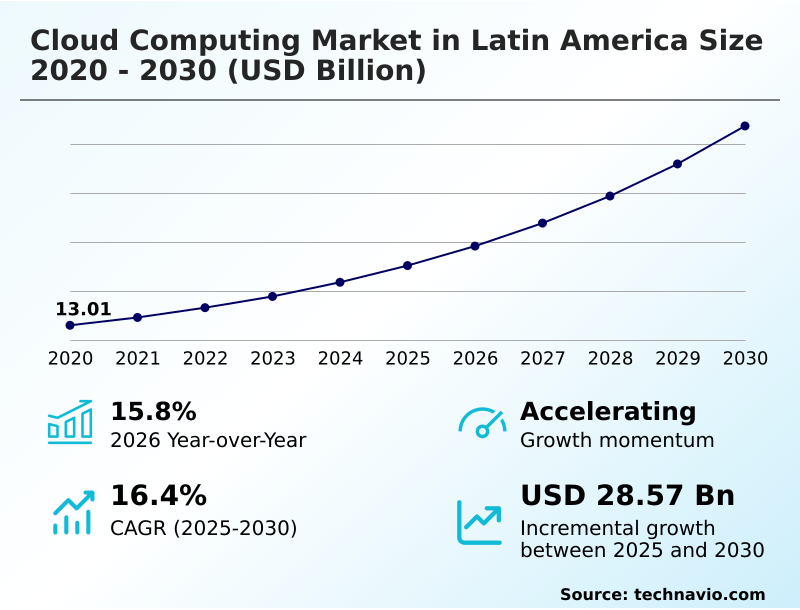

The latin america cloud computing market size is valued to increase by USD 28.57 billion, at a CAGR of 16.4% from 2025 to 2030. Increased inclination toward cloud computing for cost-cutting will drive the latin america cloud computing market.

Major Market Trends & Insights

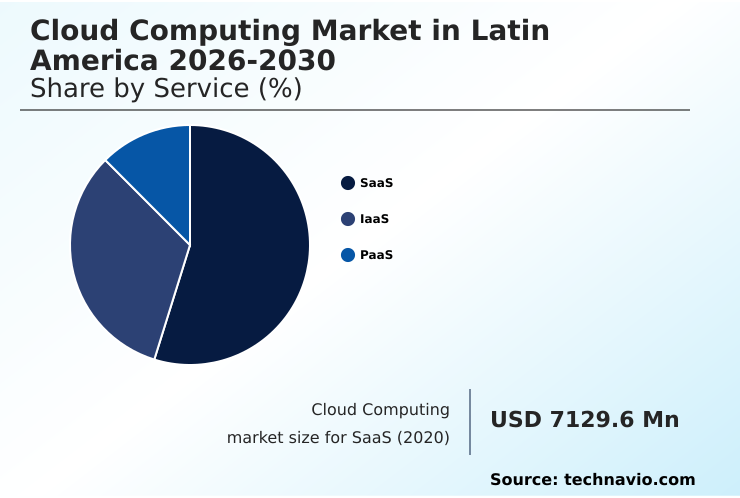

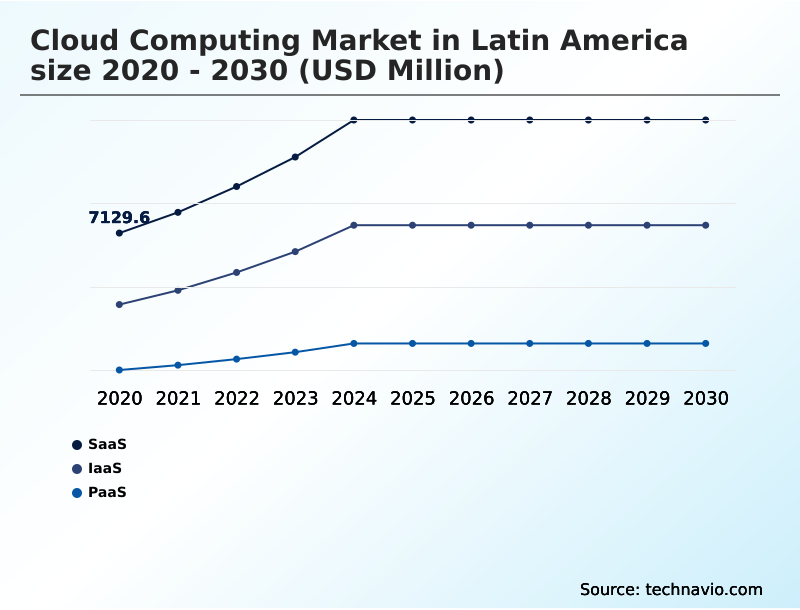

- By Service - SaaS segment was valued at USD 11.68 billion in 2024

- By Deployment - Public cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 40.77 billion

- Market Future Opportunities: USD 28.57 billion

- CAGR from 2025 to 2030 : 16.4%

Market Summary

- The cloud computing market in Latin America is a critical enabler of economic modernization, moving beyond basic infrastructure to support sophisticated digital ecosystems. It allows businesses to pivot from high capital expenditure on physical hardware to flexible operational spending models, boosting agility.

- A key driver is the need for operational resilience; for example, a manufacturing firm can use cloud-based supply chain platforms for real-time visibility, mitigating disruptions from logistical bottlenecks and improving inventory management by over 20%. This shift fosters innovation in areas like FinTech and e-commerce.

- The market is also characterized by a trend toward hybrid and multi-cloud strategies, allowing organizations to optimize workloads for cost, performance, and data sovereignty compliance. Implementing a zero trust security model is a priority, as is leveraging cloud-native development for scalable applications.

- However, challenges such as system integration with legacy platforms and a shortage of specialized skills persist, requiring strategic partnerships and investment in workforce training to unlock the full potential of cloud adoption.

What will be the Size of the Latin America Cloud Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Latin America Cloud Computing Market Segmented?

The latin america cloud computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service

- SaaS

- IaaS

- PaaS

- Deployment

- Public cloud

- Private cloud

- End-user

- Large enterprises

- SMEs

- Geography

- Latin America

By Service Insights

The saas segment is estimated to witness significant growth during the forecast period.

The market is segmented by service, where SaaS, PaaS, and IaaS address distinct business needs. Effective identity and access management is a cornerstone for all services, ensuring secure access across a hybrid IT environment.

Solutions are optimized for real-time data processing and feature elastic resource scaling to manage demand. A key consideration in multi-region deployment strategy is ensuring low-latency connectivity and efficient workload balancing.

Providers are focusing on robust data encryption standards to meet security demands, often leveraging regulatory compliance automation to navigate complex rules.

The goal is to provide a secure remote work infrastructure, with cybersecurity threat intelligence feeds integrated into platforms, improving threat detection by over 20% compared to legacy systems.

The SaaS segment was valued at USD 11.68 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the cloud computing market in Latin America 2026-2030 involves nuanced evaluations of service models and architectures. The debate over SaaS vs PaaS for Latin American startups highlights the trade-off between turnkey solutions and development flexibility. For larger firms, understanding IaaS pricing models for enterprise workloads is crucial for managing costs.

- A critical discussion is the public vs private cloud security compliance trade-off, with many opting for hybrid approaches to meet cloud computing market in Latin America 2026-2030 data sovereignty rules. Specific sectors have unique needs, leading to the rise of multi-cloud strategy for financial services to enhance resilience.

- Edge computing use cases in manufacturing are expanding for real-time factory floor analytics. The adoption of DevOps automation in hybrid cloud environments is essential for efficiency. Security remains a top concern, with a focus on cloud-native application security best practices. Architects are choosing serverless computing for scalable web applications to manage variable traffic.

- A major operational hurdle is migrating legacy ERP to a cloud platform. For innovation, AI workload optimization on public cloud and deploying data analytics platform as a service are key. SMEs, in particular, must develop a cloud disaster recovery plan for SMEs. Firms are carefully managing opex in a multi-cloud architecture.

- The benefits of PaaS for agile development, the need for IaaS for high-performance computing needs, and leveraging SaaS solutions for supply chain visibility are all part of the discourse.

- The private cloud benefits for data privacy and public cloud scalability for e-commerce are also key considerations, with companies using SaaS for supply chain seeing a 15% better on-time delivery rate than those without.

What are the key market drivers leading to the rise in the adoption of Latin America Cloud Computing Industry?

- An increased inclination toward cloud computing for cost-cutting, particularly through the shift to operational expenditure models, is a key driver for market expansion.

- A significant driver is the comprehensive digital transformation framework being adopted by enterprises, which increasingly relies on an operational expenditure model. This transition is facilitated by specialized cloud migration services and ongoing managed cloud services.

- The focus on data sovereignty compliance and secure DevSecOps implementation is paramount, particularly for running sensitive AI and ML workloads. The need for powerful big data analytics platforms is fueling SME cloud adoption.

- Furthermore, offerings like disaster recovery as a service and secure virtual desktop infrastructure are crucial for business resilience.

- Effective cloud financial management and API gateway management ensure that costs are controlled, with some firms reporting a 15% reduction in unplanned IT spending.

What are the market trends shaping the Latin America Cloud Computing Industry?

- A prominent market trend is the advent of private cloud deployments for enhanced data security. This approach addresses rising concerns over data sovereignty and cyber threats.

- Key market trends include the adoption of serverless architecture and container orchestration to accelerate cloud-native development. This supports a flexible enterprise cloud strategy that balances public cloud security with the control of private cloud deployment. Successful hybrid cloud integration and multi-cloud management are becoming critical differentiators. There is also a notable shift toward edge computing deployment for localized processing.

- The growth in PaaS application development and sophisticated SaaS integration solutions is empowering businesses, while IaaS cost optimization remains a priority, with some organizations reducing infrastructure TCO by up to 25% through optimized resource management and architectural modernization.

What challenges does the Latin America Cloud Computing Industry face during its growth?

- System integration complexities, particularly when connecting legacy systems with modern cloud environments, present a key challenge that can degrade market growth.

- A primary challenge is ensuring IT infrastructure agility while maintaining robust security. Achieving effective cloud security posture management across hybrid environments is complex. The implementation of a zero trust security model requires significant architectural changes, impacting server workload security.

- While capital expenditure reduction is a goal, the costs of data center modernization and achieving high resource utilization efficiency can be substantial. Ensuring service scalability on demand without compromising performance is another hurdle. Technologies like network virtualization, software-defined storage, and storage virtualization software present their own integration challenges, alongside unified endpoint management and comprehensive business continuity planning.

Exclusive Technavio Analysis on Customer Landscape

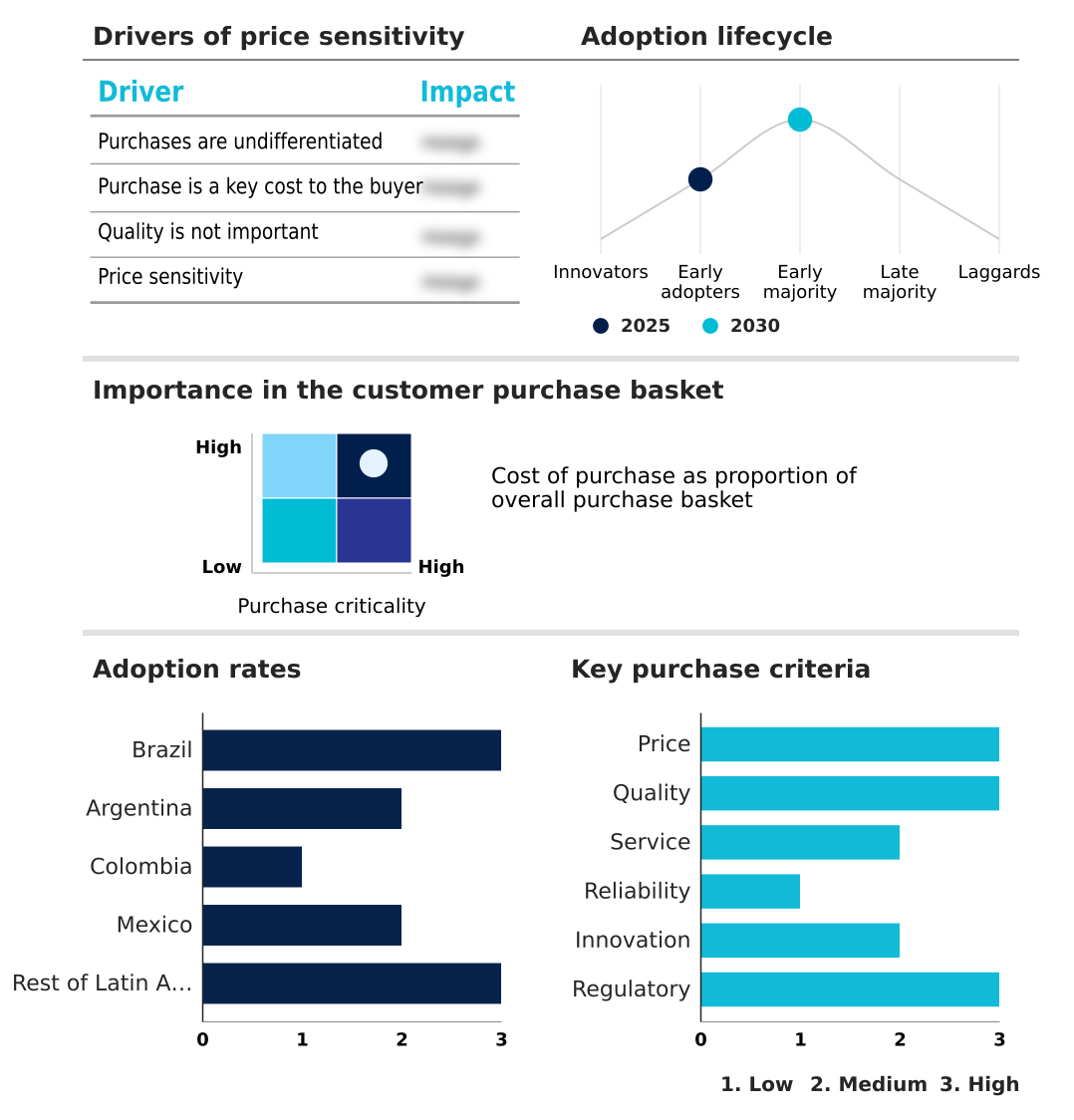

The latin america cloud computing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the latin america cloud computing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Latin America Cloud Computing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, latin america cloud computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - Provides elastic computing, database, and large-scale AI modeling services via a globally accessible public cloud platform known for its extensive infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- Capgemini SE

- Cisco Systems Inc.

- Citrix Systems Inc.

- Deloitte Touche Tohmatsu Ltd.

- Google LLC

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Infosys Ltd.

- Microsoft Corp.

- Oracle Corp.

- Rackspace Technology Inc.

- Salesforce Inc.

- SAP SE

- Telefonica SA

- VMware Inc.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Latin america cloud computing market

- In October 2024, Amazon.com Inc. launched a new AWS Local Zone in Bogota, Colombia, to deliver single-digit millisecond latency for applications such as real-time gaming and live video streaming.

- In January 2025, Microsoft Corp. and Telefonica SA announced a strategic collaboration to accelerate digital transformation for SMEs across Brazil and Mexico, integrating Azure AI services with Telefonica's connectivity solutions.

- In March 2025, Google LLC acquired a regional cloud migration specialist in Argentina to bolster its professional services capabilities and support enterprise cloud adoption in the Southern Cone.

- In May 2025, the government of Brazil, in partnership with IBM Corp., launched a national skilling initiative to train 50,000 developers and IT professionals in hybrid cloud and AI technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Latin America Cloud Computing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 215 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.4% |

| Market growth 2026-2030 | USD 28565.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.8% |

| Key countries | Brazil, Argentina, Colombia, Mexico and Rest of Latin America |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by advanced architectural patterns. Serverless architecture and container orchestration are central to cloud-native development, while infrastructure as code automates deployments. A key boardroom decision involves balancing hybrid cloud integration with multi-cloud management to avoid lock-in. Edge computing deployment is growing for low-latency connectivity.

- Security is paramount, with a zero trust security model, DevSecOps implementation, and cloud security posture management becoming standard. This includes server workload security, cloud access security broker solutions, and identity and access management for unified endpoint management. Technologies like network virtualization, software-defined wide area network, and software-defined storage enabled by storage virtualization software are foundational.

- For operations, disaster recovery as a service, IT infrastructure monitoring through application performance monitoring and IT service management tools, and managing automated billing systems are critical. Data loss prevention and data encryption standards protect AI and ML workloads and big data analytics platforms, with some firms reducing data breach incidents by 30% through these integrated strategies.

- API gateway management, real-time data processing, elastic resource scaling, workload balancing, and virtual desktop infrastructure complete the modern cloud stack, all while ensuring data sovereignty compliance.

What are the Key Data Covered in this Latin America Cloud Computing Market Research and Growth Report?

-

What is the expected growth of the Latin America Cloud Computing Market between 2026 and 2030?

-

USD 28.57 billion, at a CAGR of 16.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (SaaS, IaaS, and PaaS), Deployment (Public cloud, and Private cloud), End-user (Large enterprises, and SMEs) and Geography (Latin America)

-

-

Which regions are analyzed in the report?

-

Latin America

-

-

What are the key growth drivers and market challenges?

-

Increased inclination toward cloud computing for cost-cutting, System integration issues degrading market growth

-

-

Who are the major players in the Latin America Cloud Computing Market?

-

Alibaba Cloud, Amazon.com Inc., Capgemini SE, Cisco Systems Inc., Citrix Systems Inc., Deloitte Touche Tohmatsu Ltd., Google LLC, HCL Technologies Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., IBM Corp., Infosys Ltd., Microsoft Corp., Oracle Corp., Rackspace Technology Inc., Salesforce Inc., SAP SE, Telefonica SA, VMware Inc. and Wipro Ltd.

-

Market Research Insights

- The market is defined by a strategic shift to an operational expenditure model, prioritizing capital expenditure reduction and resource utilization efficiency. This drives SME cloud adoption and large-scale enterprise cloud strategy initiatives. A modern digital transformation framework leverages cloud migration services and managed cloud services for data center modernization and greater IT infrastructure agility. Service scalability on demand is critical.

- SaaS integration solutions are key for CRM platform integration and ERP system migration, while PaaS application development accelerates innovation. IaaS cost optimization is achieved through better cloud financial management and regulatory compliance automation. Public cloud security and private cloud deployment support a hybrid IT environment and multi-region deployment strategy to reduce regional data center latency.

- This is crucial for business continuity planning, remote work infrastructure, and integrating supply chain optimization software, cloud-based data analytics, AI model training on cloud, IoT platform connectivity, and cybersecurity threat intelligence, with firms improving compliance reporting efficiency by 40%.

We can help! Our analysts can customize this latin america cloud computing market research report to meet your requirements.

RIA -

RIA -