Level 4 Autonomous Vehicles Market Size 2026-2030

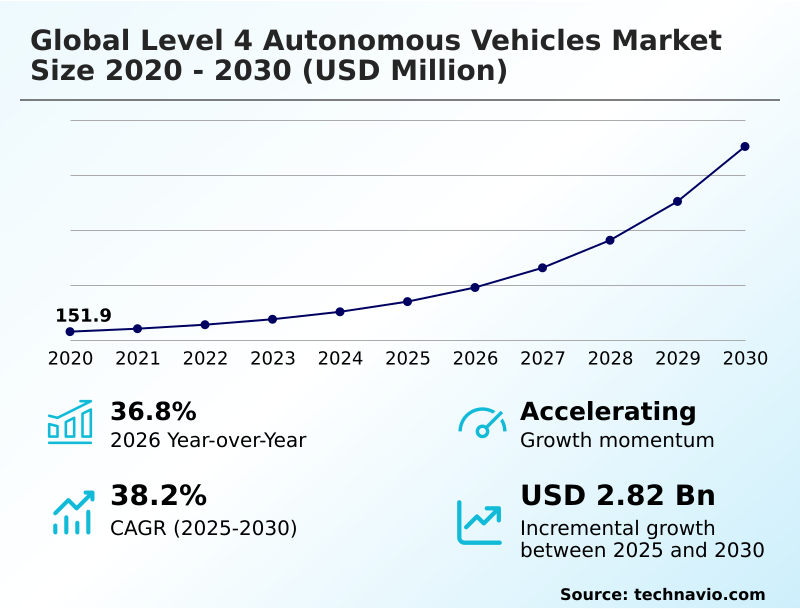

The level 4 autonomous vehicles market size is valued to increase by USD 2.82 billion, at a CAGR of 38.2% from 2025 to 2030. Technological advancements in perception and artificial intelligence will drive the level 4 autonomous vehicles market.

Major Market Trends & Insights

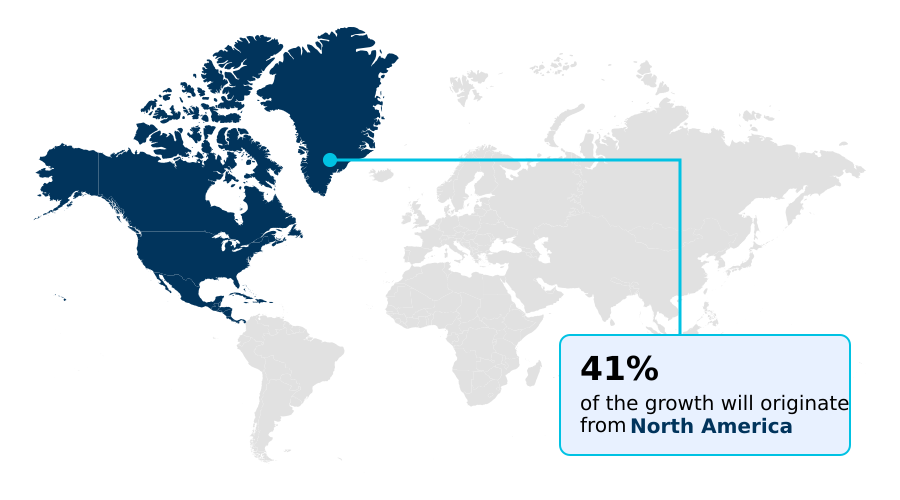

- North America dominated the market and accounted for a 40.8% growth during the forecast period.

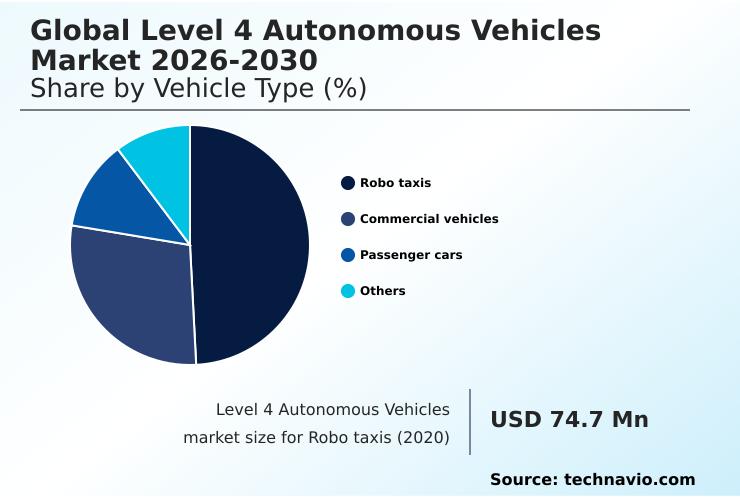

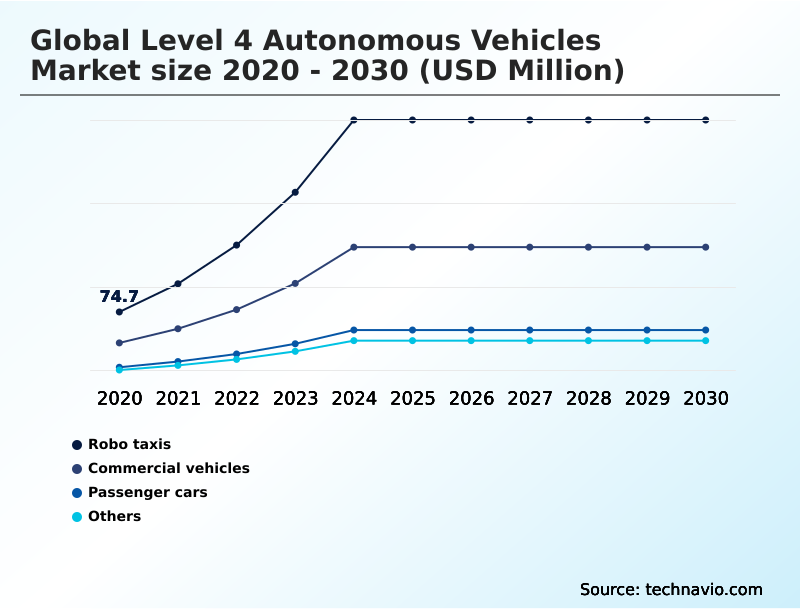

- By Vehicle Type - Robo taxis segment was valued at USD 270.2 million in 2024

- By Component - Hardware segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.37 billion

- Market Future Opportunities: USD 2.82 billion

- CAGR from 2025 to 2030 : 38.2%

Market Summary

- The level 4 autonomous vehicles market is defined by vehicles capable of high driving automation within a specific operational design domain, eliminating the need for human intervention in geofenced locations. This progress is built upon sophisticated sensor suites and powerful onboard computers that run complex artificial intelligence algorithms for real-time decision making.

- Key drivers include significant operational cost reductions in logistics and delivery, where a logistics firm might leverage autonomous trucking for long-haul logistics to address driver shortages and achieve up to 14% in fuel savings.

- However, the path to mass adoption is constrained by challenges such as fragmented regulatory frameworks, cybersecurity measures, and the critical need to build public perception and trust. The successful deployment of driverless trucks and robotaxi services depends on developing fault-tolerant perception systems and robust vehicle-to-everything (v2x) communication within smart infrastructure, ensuring both safety and efficiency.

- This technological shift is compelling businesses to reconsider their mobility and supply chain strategies, focusing on the economic and safety benefits of removing the human driver from the equation in controlled environments.

What will be the Size of the Level 4 Autonomous Vehicles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Level 4 Autonomous Vehicles Market Segmented?

The level 4 autonomous vehicles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Vehicle type

- Robo taxis

- Commercial vehicles

- Passenger cars

- Others

- Component

- Hardware

- Software

- Services

- Propulsion

- Electric

- Hybrid

- Internal combustion engine

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- South Korea

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The robo taxis segment is estimated to witness significant growth during the forecast period.

The robotaxi segment is pivotal to the evolution of shared mobility services, transitioning from pilot programs to initial driverless operations. These vehicles rely on sophisticated sensor suites and onboard computers running advanced artificial intelligence algorithms to navigate complex urban routes.

Success hinges on a fault-tolerant perception system capable of precise object recognition and classification and predictive behavior prediction of pedestrians and other vehicles.

While public acceptance varies, with some surveys showing nearly three times higher interest in certain APAC regions compared to North America, the focus remains on safety.

Advanced computer vision algorithms and cybersecurity measures are critical for building trust and enabling scalable autonomous shuttles for logistics and delivery in densely populated areas.

The Robo taxis segment was valued at USD 270.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Level 4 Autonomous Vehicles Market Demand is Rising in North America Get Free Sample

The geographic landscape for level 4 autonomy is varied, with distinct regional strategies shaping deployment. North America leads in real-world testing of geofenced mobility, particularly for robotaxis, though progress is moderated by geopolitical tensions impacting supply chains.

In contrast, APAC, driven by government mandates aiming for 30% of new vehicles to have advanced automation, excels in large-scale urban mobility solutions and is rapidly developing smart infrastructure with vehicle-to-everything (v2x) capabilities.

This region's focus on connected mobility is accelerating commercialization. Europe prioritizes regulatory harmonization and public transport applications, leveraging advanced driver assistance systems (adas) as a bridge to full autonomy.

Real-time decision making in these vehicles is powered by centralized computing units running complex machine learning algorithms, tailored to each operational design domain.

This regional divergence necessitates tailored market-entry strategies that account for differing regulatory climates and infrastructure readiness, impacting overall supply chain resilience.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The successful integration of level 4 autonomy hinges on addressing specific use cases and their inherent complexities. In urban environments, the economic viability of level 4 robotaxis depends on overcoming significant operational challenges and navigating public trust challenges in self-driving technology.

- Concurrently, the logistics sector is keenly focused on autonomous trucking for long-haul logistics, where the potential for cost reduction with autonomous freight is a primary driver, though this faces regulatory hurdles for driverless truck deployment. The technological backbone for these applications is advancing rapidly.

- The use of generative AI for autonomous driving simulation allows for extensive validation, as virtual environments can cover millions of scenarios and reduce physical testing needs by more than 50% compared to traditional methods. Advances in sensor fusion for adverse weather navigation are critical for operational reliability, while robust path planning algorithms for unpredictable scenarios enhance safety.

- However, the industry must still confront major systemic issues. These include establishing clear sae level 4 autonomous vehicle testing standards, mitigating cybersecurity risks in connected autonomous vehicles, and creating definitive legal liability frameworks for autonomous accidents.

- The implementation of v2x communication for urban traffic efficiency is essential for optimizing traffic flow, while the design of intuitive human-machine interface design for level 4 is key for systems requiring occasional human interaction.

- Ultimately, whether for last-mile delivery automation with autonomous pods or integrating level 4 systems in passenger cars, the path forward requires a holistic approach that balances innovation with public safety and regulatory consensus, especially concerning data management for AI training in autonomy.

What are the key market drivers leading to the rise in the adoption of Level 4 Autonomous Vehicles Industry?

- Technological advancements in perception and artificial intelligence are the key drivers of market growth.

- Economic viability is a primary market driver, with commercial applications demonstrating clear pathways to operational cost reduction.

- In hub-to-hub logistics, driverless trucks operating on autonomous freight corridors can achieve up to 14% in fuel savings and significantly enhance road safety enhancement. Similarly, the expansion of robotaxi services and ride-hailing networks is creating new revenue streams.

- These deployments are made possible by strategic partnerships between technology developers and vehicle manufacturers, leveraging powerful high-performance system-on-chips (socs) and efficient electric propulsion systems.

- The focus on specific use cases like last-mile delivery and long-haul trucking allows for targeted deployment, accelerating the realization of benefits such as traffic efficiency improvement and reduced operational expenses, thereby stimulating further investment and market expansion.

What are the market trends shaping the Level 4 Autonomous Vehicles Industry?

- Advancements in sensor technology and artificial intelligence are a key upcoming market trend. These innovations are critical for enhancing vehicle perception and decision-making capabilities.

- Key market trends are centered on rapid technological maturation, particularly within the software stack. The use of generative AI models is accelerating data-driven development, allowing for extensive validation and verification of perception and decision-making capabilities in simulated environments, reducing physical testing timelines by over 40%. Concurrently, advancements in sensor fusion techniques are enhancing system reliability.

- Innovations like solid-state lidar and 4D imaging radar are combined with advanced deep learning models to improve route planning and optimization. This integration is crucial for refining path planning algorithms and localization technology, enabling smoother and safer in-vehicle functions.

- This focus on software and AI-driven simulation represents a strategic shift toward creating more robust and scalable autonomous systems capable of handling complex, real-world scenarios with greater precision.

What challenges does the Level 4 Autonomous Vehicles Industry face during its growth?

- Navigating the labyrinth of regulatory and legal frameworks is a key challenge affecting industry growth.

- Significant challenges persist, primarily in navigating fragmented regulatory frameworks and overcoming low public perception and trust. In some regions, 66% of the public still expresses fear of high driving automation, a sentiment that impedes widespread adoption. The absence of harmonized data sharing protocols complicates efforts to establish clear legal liability, an issue further compounded by underlying infrastructure deficits.

- Developing a seamless human-machine interface for purpose-built autonomous vehicles remains a complex task. The industry must address these issues systematically, from mandating black box data recorders to facilitating AI-driven urban planning, to build the necessary confidence for deploying sae level 4 autonomy at scale.

- This includes ensuring the reliability of core technologies like autonomous braking systems, especially for sidewalk delivery robots operating in pedestrian-heavy areas.

Exclusive Technavio Analysis on Customer Landscape

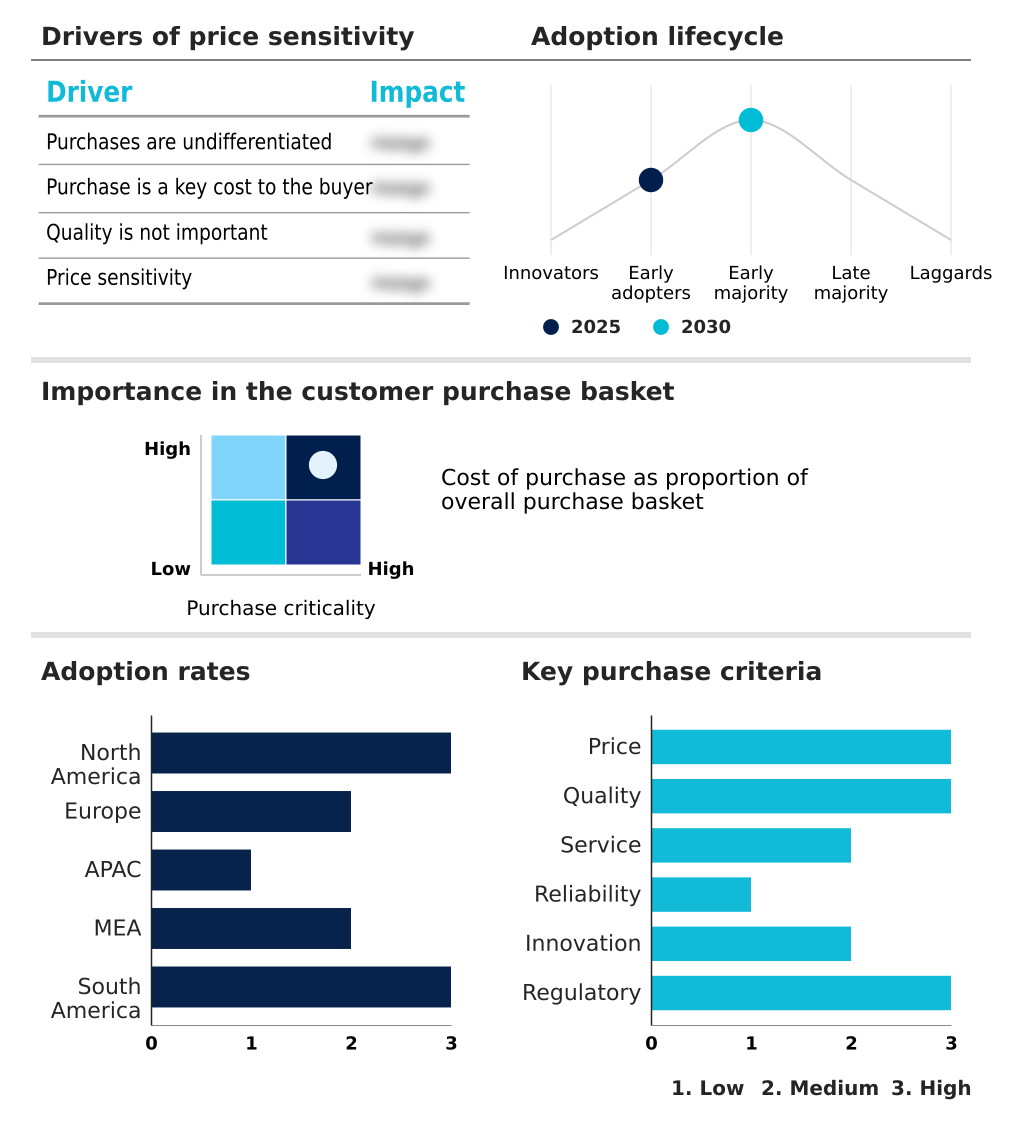

The level 4 autonomous vehicles market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the level 4 autonomous vehicles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Level 4 Autonomous Vehicles Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, level 4 autonomous vehicles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Volvo - These offerings center on commercialized driverless ride-hailing services, leveraging mature AI systems for scalable autonomous mobility within defined urban zones.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- Aptiv Plc

- Aurora Innovation Inc.

- AutoX Inc.

- Baidu Inc.

- BMW AG

- Ford Motor Co.

- Mercedes Benz Group AG

- Mobileye Technologies Ltd.

- Motional Inc.

- Nuro Inc.

- Pony.ai

- Toyota Motor Corp.

- Volkswagen AG

- Waymo LLC

- WeRide

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Level 4 autonomous vehicles market

- In September 2024, the United States government initiated a proposal to prohibit the import and sale of connected vehicles and their components from specific countries, citing national security concerns, with the ban targeting software by 2027 and hardware by 2030.

- In February 2025, Beep announced a partnership with the Orlando International Airport to deploy a fleet of Level 4 electric shuttles, connecting the main terminal with a new south terminal complex and rental car facilities on dedicated roadways.

- In March 2025, WeRide and Renault Group offered a public trial of an autonomous Robobus service in Barcelona, demonstrating a real-world application of level 4 technology in public transportation.

- In April 2025, Aurora launched its first fully autonomous long-haul commercial rides between Dallas and Houston, Texas, showcasing the real-world application and economic potential of its technology for the freight sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Level 4 Autonomous Vehicles Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 38.2% |

| Market growth 2026-2030 | USD 2820.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 36.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, South Korea, India, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market for high driving automation is advancing beyond research into commercially viable applications, focusing on robotaxi services and autonomous freight corridors. This evolution is predicated on the integration of advanced sensor suites, high-resolution cameras, and powerful onboard computers capable of processing up to 25 gigabytes of data per minute.

- Progress is contingent on the sophistication of the software stack, which leverages artificial intelligence algorithms and machine learning algorithms for localization technology and path planning algorithms. For boardroom-level strategy, a critical consideration is the need for co-investment in smart infrastructure, as the reliability of geofenced locations depends on robust vehicle-to-everything (v2x) communication.

- The deployment of driverless trucks and autonomous shuttles within a defined operational design domain presents clear business cases in logistics and delivery. Success requires not only technological maturity, from autonomous braking systems to centralized computing units, but also navigating the shift toward electric propulsion systems and managing the deployment of purpose-built autonomous vehicles within emerging ride-hailing networks.

What are the Key Data Covered in this Level 4 Autonomous Vehicles Market Research and Growth Report?

-

What is the expected growth of the Level 4 Autonomous Vehicles Market between 2026 and 2030?

-

USD 2.82 billion, at a CAGR of 38.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Vehicle Type (Robo taxis, Commercial vehicles, Passenger cars, and Others), Component (Hardware, Software, and Services), Propulsion (Electric, Hybrid, and Internal combustion engine) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Technological advancements in perception and artificial intelligence, Navigating labyrinth of regulatory and legal frameworks

-

-

Who are the major players in the Level 4 Autonomous Vehicles Market?

-

AB Volvo, Aptiv Plc, Aurora Innovation Inc., AutoX Inc., Baidu Inc., BMW AG, Ford Motor Co., Mercedes Benz Group AG, Mobileye Technologies Ltd., Motional Inc., Nuro Inc., Pony.ai, Toyota Motor Corp., Volkswagen AG, Waymo LLC, WeRide and ZF Friedrichshafen AG

-

Market Research Insights

- The market dynamics are shaped by a tense interplay between technological capability and external pressures like public perception and trust. For instance, while some data indicates higher accident rates for autonomous systems, this is often attributable to mandatory data sharing protocols for every minor incident, a standard not applied to most human-driven events.

- Economically, the drive for operational cost reduction is a powerful force, with autonomous trucking pilots demonstrating potential fuel savings of up to 14%. However, these benefits are weighed against complex regulatory frameworks and evolving legal liability standards. The effectiveness of commercial applications and the scalability of shared mobility services depend on resolving these tensions.

- Progress is contingent on managing infrastructure deficits and achieving a level of road safety enhancement that can overcome widespread consumer skepticism, which remains high in certain Western markets.

We can help! Our analysts can customize this level 4 autonomous vehicles market research report to meet your requirements.

RIA -

RIA -