Market Analysis APAC, North America, Europe, Middle East and Africa, South America - US, China, Japan, India, UK - Size and Forecast 2024-2028")

Enjoy complimentary customisation on priority with our Enterprise License!

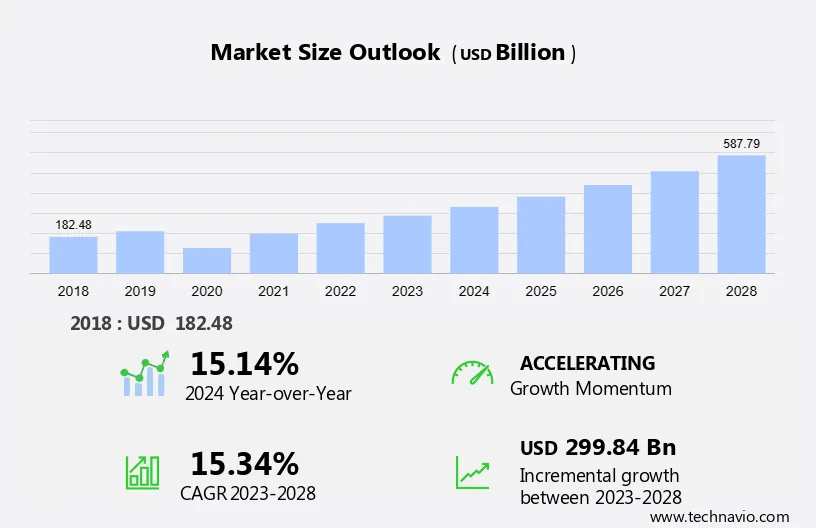

The low-cost carrier market size is forecast to increase by USD 299.84 billion, at a CAGR of 15.34% between 2023 and 2028.

The rapid urban commoditization has led to a surge in demand for affordable air travel and air passenger traffic, fueling the expansion of low-cost carriers (LCC). While these carriers offer competitive fare structures and discounts, they often operate on slim profit margins, facing occasional losses due to factors like seasonal demand and downtime. However, their extensive star network and hub connections ensure a steady flow of direct demand from passengers seeking reduced fares and different air passenger classes.

Market Forecast 2024-2028

To learn more about this report, Request Free Sample

The cost airlines market is thriving with fierce competition and steady growth. Airlines in this sector prioritize budget-friendly fares, expanding routes, and accessible destinations to meet the rising demand for affordable travel. Capturing a larger market share, these carriers offer affordable tickets and cater to expanding travel needs. Amidst intense competition, airlines focus on innovation to attract passengers with competitive fares and services. As the industry continues to evolve, low-cost carriers play a significant role in shaping the airline market, providing accessible travel options for passengers worldwide. Our researchers studied the market research and growth data for years, with 2023 as the base year and 2024 as the estimated year, and presented the key drivers, trends, and challenges for the market.

LCCs are continually exploring innovative ways to enhance their revenue streams. This involves expanding their services to new routes to tap into previously unexplored markets. Airlines commonly employ aviation market intelligence tools to analyze comprehensive data, including passenger flows, timing, and connectivity options, to assess potential routes. The introduction of new routes not only strengthens the overall aviation infrastructure but also stimulates activity in various sectors. This includes acquiring new aircraft and retrofitting existing fleets, as well as encouraging regional component manufacturers to participate in both scheduled and unscheduled maintenance tasks. The increased frequency of flights also fosters the establishment of aircraft repair facilities nearby, which can source necessary components from certified local vendors to minimize operational expenses.

For instance, in November 2022, Air Arabia, the Middle East and North Africa's leading LCC operator inaugurated a new route from Sharjah to Namangan in Uzbekistan. The introduction of such new service routes promises to unlock fresh revenue streams for LCCs, enabling them to provide economically feasible services to passengers. This, in turn, is poised to propel the market's growth trajectory during the forecast period.

The US, China, France, Indonesia, Japan, and India are among the countries that have increased the demand for air travel. LCCs in these countries constantly monitor and adapt to consumer expectations to provide cost-efficient service as a part of the luxury air travel package. With growing affluence, individuals are increasing their spending on unique experiences rather than accumulating material goods. It is becoming highly challenging for LCCs to cater to the demand for luxurious air travel from some customers while remaining economical. Aircraft interior designers are experimenting with modern systems.

Moreover, as several air passengers seek the material aspects of luxury travel, mature markets such as the US and China are demanding a new, evolved type of luxury air travel. Thus, offering luxury customers a relevant, personal, and exclusive experience has become crucial. LCCs remain committed to surpassing passenger expectations in terms of the level of comfort offered at a certain price point. The incorporation of luxury air travel at economical prices will offer growth opportunities to many LCCs across regions, which will positively impact the market during the forecast period.

Rising fuel prices and increasing labor costs are increasing the overall operating expense (OPEX) of LCCs. The surge in fuel prices is attributable to geopolitical events such as US sanctions on Iran's oil exports and production cuts in the Organization of the Petroleum Exporting Countries (OPEC). Further, factors such as a significant increase in the number of LCCs and several consolidation deals are making the market very competitive. Online travel agencies (OTAs) and other intermediaries are investing in technology solutions to establish their digital presence and market penetration, which are challenges for the LCC market. LCCs may incur additional costs to keep up with digitization and remain competitive.

Therefore, increasing competition and rising OPEX are eroding the profit margins of LCCs and forcing them to implement strategies such as competitive ticket pricing, which is not a feasible long-term solution. Thus, increasing fuel prices and labor costs, coupled with growing competition, may hinder revenue generation by LCCs. This will challenge the growth of the market during the forecast period.

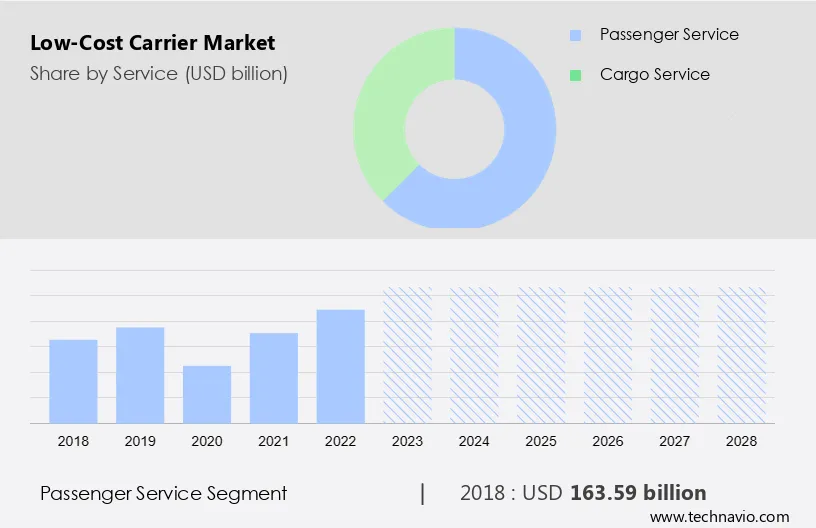

The market has witnessed significant growth in recent years, attracting budget-conscious travelers and stimulating competition within the industry. The market report includes a comprehensive outlook on the market offering forecasts for the industry segmented by Service, which comprises passenger service and cargo service. Additionally, it categorizes Type into narrow body and wide body and covers Region, including North America, APAC, Europe, Middle East and Africa, and South America. The report provides market size, historical data spanning from 2018 to 2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

The market share growth by the passenger service segment will be significant during the forecast period. In 2022, global passenger footfall stood at 5 billion, which was a 4% increase over the previous year's value. This figure is anticipated to double in the next 15 years, primarily because of the rapid growth in air travel in APAC. Most LCCs are trying to modernize the existing fleet to exploit new market opportunities in the market.

Customised Report as per your requirements!

The passenger service segment was valued at USD 163.59 billion in 2018. Fuel costs drastically affect the profit margins of LCCs, as these carriers already charge less than other carriers per flight. Vendors continue to focus on using fuel-efficient aircraft to control operational expenditure. Aircraft OEMs are constantly improving their product offerings to cater to a wider segment of a booming market. Such developments are expected to improve the efficiency of the commercial aircraft and help LCCs increase their profit margins during the forecast period. Also, LCC service providers are expanding their service offerings. For instance, Tulum will now be served by JetBlue, the airlines fourth Mexican destination. JetBlue began operating flights to Tulum in December 2023. On June 13, 2024, John F. Kennedy International Airport (JFK) in New York will start offering daily nonstop service to Felipe Carrillo Puerto Tulum International Airport (TQO). This in turn will drive the segment and market in focus during the forecast period.

Based on the type, the market has been segmented into a narrow body and a wide body. The narrow body?segment will account for the largest share of this segment.?Narrow-body or single-aisle aircraft are referred to as aircraft having a single aisle in the cabin with passenger seating arrangement divided into axial groups. Further, airlines focus on point-to-point flying routes instead of opting for a non-stop flight to the destination, which allows operators to achieve superior flexibility over wide-body airlines while enhancing their networks. LCCs are key contributors to the growing demand for this aircraft type, as operational efficiency and overall profitability remain the prime concern for LCCs. Fluctuating fuel costs, strict regulations on noise and CO2 emissions, and increasing competition among LCCs are forcing LCCs to optimize their operational efficiency. One of the ways is to use fuel-efficient aircraft while providing attractive service, safety, and comfort to attract passengers. This is driving the adoption of narrow-body aircraft among LCCs, thus augmenting the growth of the market.

For more insights on the market share of various regions Download Sample PDF now!

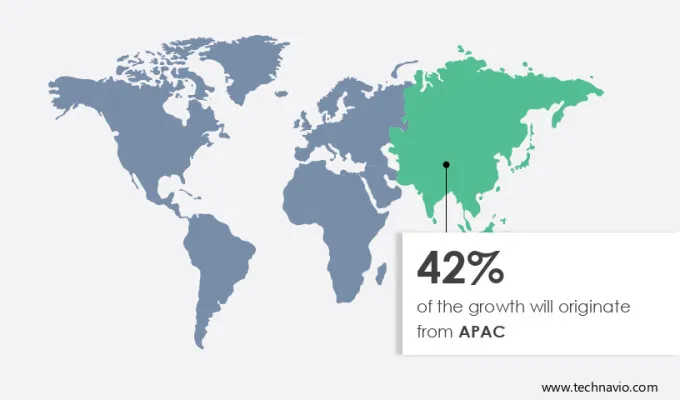

APAC is estimated to contribute 42% to the growth by 2028. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. A steady increase in passenger traffic in APAC is providing growth opportunities market companies in the region. Growth in passenger traffic in the region has attracted investments in the construction of new airports and the upgrade of existing ones. China, Japan, India, South Korea, Singapore, and Australia are contributing significantly to the growth of the LCC market in the region. The fast growth of the regional market can be primarily attributed to increased air passenger transportation in the region. APAC, with about half of the global population, is a high-growth market for LCCs, with an increasing number of middle-class households. The region contributed to more than 37% of the global GDP in 2021.

In addition, commercial airline companies, including LCCs, across APAC, are focusing on expanding their operational fleet, owing to the increasing number of passengers in the region. Domestic and international airlines in India, Singapore, Malaysia, Indonesia, and Australia, among other countries, are procuring new-generation aircraft and associated components. Thus, the growth outlook for the market in APAC will be positive during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Air Arabia PJSC: The company offers low-cost carrier services with free inflight streaming service, snacks and meals at affordable prices through their Sky Café.

Additionally, we also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including Air Arabia PJSC, Air Canada, Capital A Berhad, Cebu Pacific, easyJet plc, Fly LEVEL SL, FLYPOP Ltd., Frontier Group Holdings Inc., InterGlobe Aviation Ltd., JetBlue Airways Corp., Lion Air, Norwegian Air Shuttle ASA, Qantas Airways Ltd., Ryanair Holdings plc, Singapore Airlines Ltd., Southwest Airlines Co., SpiceJet Ltd., Spirit Airlines Inc., Vueling Airlines SA, and WestJet Encore Ltd.

Technavio market market forecast the an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

Low-cost airline companies revolutionize air travel with budget-friendly fares and narrowbody aircraft type like the Airbus A321 and Boeing B737. LCCs (Low-Cost Carriers) prioritize operational responsiveness, serving small airports in crowded cities to enhance ease of travel and boost the tourism industry. Low-cost carriers typically offer no-frills services, charging extra for amenities such as checked baggage and in-flight meals.They focus on cost-saving measures, simplified operations, and efficient turnaround times. With a point-to-point model, they optimize routes and reduce fares, appealing to a wide range of passenger trips. Despite challenges such as travel restrictions and uncertainty, LCCs remain competitive through fleet expansion and leveraging technical advancements.

The market is characterized by its commitment to providing affordable air travel options while maintaining high standards of service. Traditional services like priority boarding, seat assignment, and baggage handling are offered alongside discounted tickets to appeal to consumer preferences. These carriers optimize their operating cost structure to achieve cost savings and ensure quick turnaround times between flights. Maintenance costs are kept low through efficient ground operations and partnerships with reliable maintenance providers. Despite facing intense competition, LCCs generate secondary revenue through initiatives like pre-sale seats and in-flight snacks. They cater to a diverse clientele, including business travelers and those seeking last-minute bookings. With a focus on internet-based delivery and other non-aviation services, these carriers remain at the forefront of the industry, adapting to changing lifestyles and economic activities while contributing to the growth of air passenger travel worldwide.

The market has become a dominant force in the aviation industry, catering to consumers seeking affordable air transportation options. Indigo and other low-cost carriers have revolutionized travel by offering lower ticket prices compared to traditional airlines. With a focus on budget carriers and cost flights, these airline industry have expanded their scheduling networks and locations, providing convenient and accessible travel opportunities. In addition to competitive pricing, LCCs prioritize efficient operations, streamlined services, and minimal amenities like inflight food and entertainment, allowing for ticketless travel and reduced checked baggage fees. Despite challenges such as crew training and deregulation, LCCs continue to thrive, with their aircraft models and LCC fleets earning recognition at prestigious events like the World Travel Awards.

The market analysis and report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and market growth analysis opportunities from 2018 to 2028.

|

Low-Cost Carrier Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.34% |

|

Market Growth 2024-2028 |

USD 299.84 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.14 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

US, China, Japan, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Air Arabia PJSC, Air Canada, Capital A Berhad, Cebu Pacific, easyJet plc, Fly LEVEL SL, FLYPOP Ltd., Frontier Group Holdings Inc., InterGlobe Aviation Ltd., JetBlue Airways Corp., Lion Air, Norwegian Air Shuttle ASA, Qantas Airways Ltd., Ryanair Holdings plc, Singapore Airlines Ltd., Southwest Airlines Co., SpiceJet Ltd., Spirit Airlines Inc., Vueling Airlines SA, and WestJet Encore Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Service

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.