Low-cost Carrier (LCC) Market Size 2026-2030

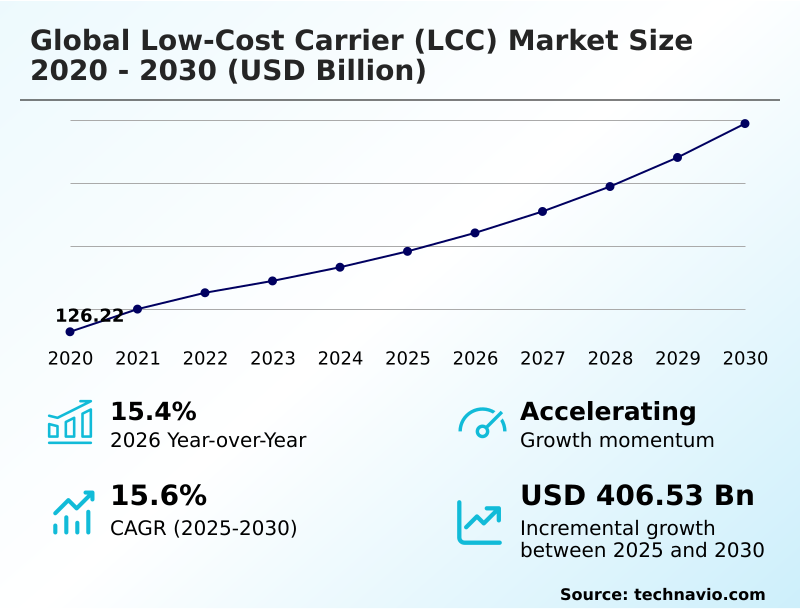

The low-cost carrier (lcc) market size is valued to increase by USD 406.53 billion, at a CAGR of 15.6% from 2025 to 2030. Strategic hybridization and premiumization of service models will drive the low-cost carrier (lcc) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 42.1% growth during the forecast period.

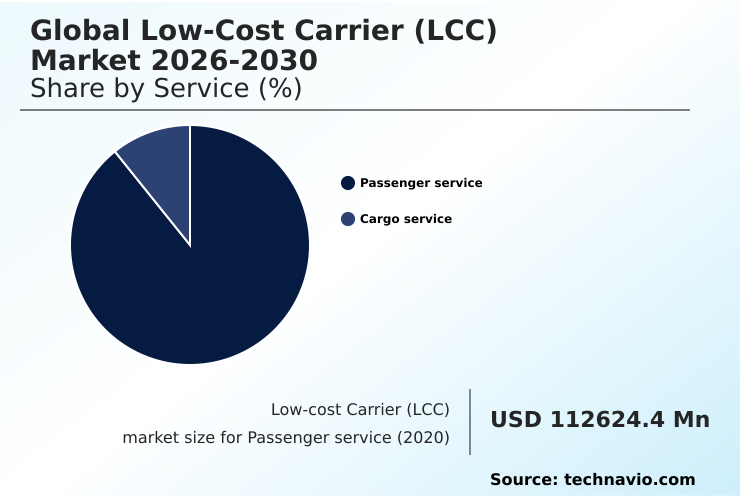

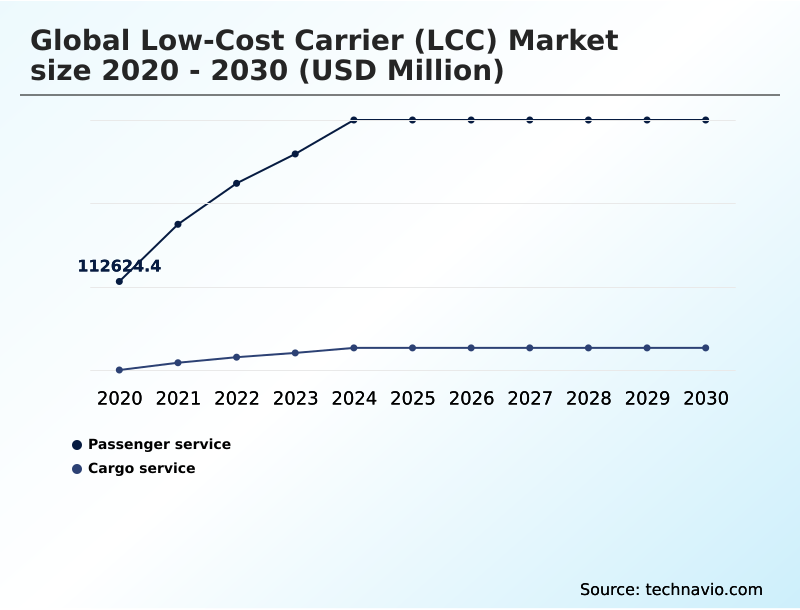

- By Service - Passenger service segment was valued at USD 293.24 billion in 2024

- By Type - Narrow body segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 662.40 billion

- Market Future Opportunities: USD 406.53 billion

- CAGR from 2025 to 2030 : 15.6%

Market Summary

- The Low-cost Carrier (LCC) Market is defined by a relentless focus on operational efficiency and cost minimization, traditionally achieved through unbundled services, high aircraft utilization, and point-to-point routes. However, the sector is undergoing a significant transformation.

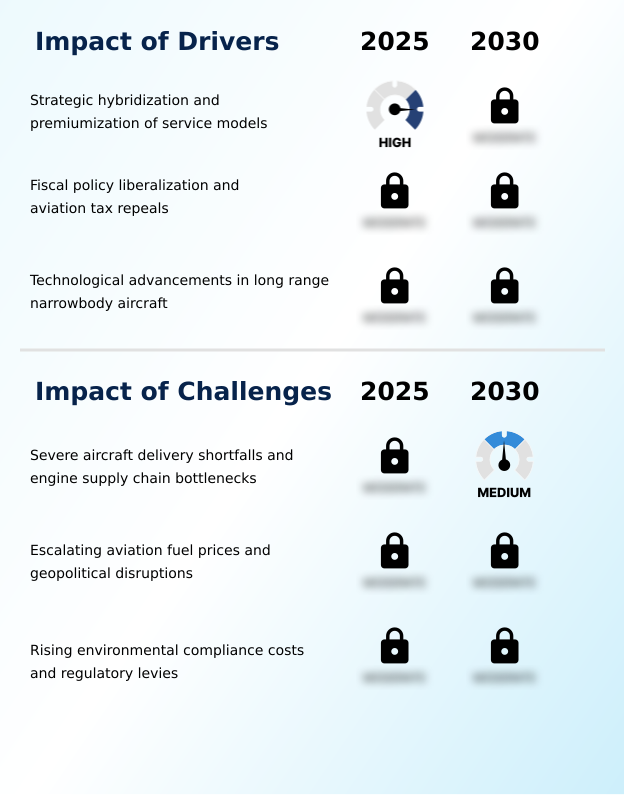

- A key driver is the strategic hybridization of service models, where carriers introduce premium elements like assigned seating and extra legroom to attract business travelers, moving away from the strict no-frills approach. This premiumization allows for diversified ancillary revenue models. Concurrently, technological advancements are reshaping the competitive landscape.

- The induction of long-range narrowbody aircraft enables LCCs to enter transcontinental routes, challenging legacy carriers. Digitalization is also critical, with carriers implementing AI-driven dynamic pricing and enhancing digital connectivity with satellite internet. This evolution occurs amid significant challenges, including severe aircraft delivery shortfalls and engine supply chain bottlenecks, which hinder fleet modernization and growth plans.

- For instance, a carrier's strategy to upgrade its fleet for better fuel efficiency might be disrupted by a two-year delay in aircraft deliveries, forcing it to extend leases on older, less efficient jets and impacting its cost structure and environmental targets. Geopolitical instability adds further pressure through volatile jet fuel prices.

What will be the Size of the Low-cost Carrier (LCC) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Low-cost Carrier (LCC) Market Segmented?

The low-cost carrier (lcc) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service

- Passenger service

- Cargo service

- Type

- Narrow body

- Wide body

- Application

- Individual

- Commercial

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Service Insights

The passenger service segment is estimated to witness significant growth during the forecast period.

The passenger service segment is evolving beyond its no-frills origins, driven by a strategic hybridization strategy and the premiumization of services. Operators are shifting from a purely transactional low-cost carrier business model to one focused on the digital passenger journey.

This includes the unbundling of services, allowing for customization through ancillary revenue models that offer priority boarding and extra legroom. This shift is designed to attract higher-yield travelers without compromising the core value proposition.

In some liberalized fiscal environments, carriers have achieved a 15% increase in annual passenger volume by rapidly expanding network rebalancing. This demonstrates a market where digital connectivity and enhanced cabin comfort are becoming standard expectations, even within the budget-focused framework.

The Passenger service segment was valued at USD 293.24 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Low-cost Carrier (LCC) Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the Low-cost Carrier (LCC) Market is diverse, shaped by regional connectivity demands and local economic factors.

In APAC, the unique archipelagic geography of nations like Indonesia makes air travel essential, driving robust domestic demand and fleet modernization.

North America is defined by a move toward a hybridization strategy, with carriers shifting away from open boarding to assigned seating to attract new customer segments.

Europe's market is characterized by intense fiscal migration, where network rebalancing occurs in direct response to aviation tax policies; a 50% hike in airport fees in one nation can trigger a base closure and reallocation of assets to a more favorable one.

This is part of a broader trend of service reliability and decarbonization mandates. The expansion into transcontinental routes is a global phenomenon, powered by long-range narrowbody aircraft with an 8,700-kilometer range, connecting secondary city pairs that were previously unviable.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global Low-cost Carrier (LCC) Market 2026-2030 is increasingly dictated by the sophisticated interplay between cost control and revenue diversification. The impact of ancillary revenue on airline profitability has become a central strategic pillar, moving far beyond simple baggage fees to include dynamic, multi-tiered fare structures.

- A key aspect of this transformation is how LCCs are using AI for dynamic pricing, enabling real-time adjustments that optimize load factors and yield. The comparison of narrowbody versus widebody LCC operations highlights another strategic frontier, as long-range narrowbody aircraft in low-cost models are enabling expansion into previously untenable transcontinental routes.

- This, however, brings into focus the challenges of engine supply chain for LCCs, which can ground aircraft and disrupt expansion plans. Concurrently, the LCC hybridization and its effect on market competition is blurring the lines with legacy carriers.

- As LCCs add premium features, they must manage the digital transformation in the LCC passenger experience to ensure it remains seamless and cost-effective. Low-cost carrier strategies for emerging markets are adapting to these global trends, balancing growth ambitions with local infrastructure constraints.

- Finally, sustainability challenges for the low-cost carrier sector, including emissions targets and the high cost of SAF, represent a long-term hurdle that will require significant investment and innovation to overcome. Carriers that successfully integrate these strategies have reported double-digit improvements in unit revenue compared to those with more static models.

What are the key market drivers leading to the rise in the adoption of Low-cost Carrier (LCC) Industry?

- The strategic hybridization and premiumization of service models represent a key driver for the market.

- The market's growth is propelled by several key drivers, most notably technological advancements in aircraft and the liberalization of fiscal policies.

- The induction of next-generation long-range narrowbody aircraft, with a range of up to 8,700 kilometers, is a primary catalyst, enabling carriers to launch direct transcontinental routes with significantly lower operational costs.

- This has been a critical factor in expanding the low-cost carrier business model into new international markets.

- Additionally, fiscal policy plays a crucial role; the abolition of a national aviation tax in one European country directly resulted in an 800 million USD investment and a 15% increase in passenger traffic, showcasing how tax repeals can unlock immediate growth.

- This market dynamism underscores the importance of both technological innovation and a favorable regulatory environment for sustained expansion.

What are the market trends shaping the Low-cost Carrier (LCC) Industry?

- A strategic pivot toward hybridization and premiumization is a significant upcoming market trend. This involves budget airlines incorporating premium service elements to attract high-yield travelers.

- Key trends are reshaping the Low-cost Carrier (LCC) Market, centered on a strategic pivot toward hybridization and advanced digitalization. The premiumization of services is a dominant theme, where carriers are moving beyond a no-frills model to offer tiered fare structures and priority boarding, enhancing the digital passenger journey. This approach has proven effective in attracting new customer segments.

- Concurrently, the integration of generative AI and AI-driven copilots is optimizing customer service and dynamic pricing, with some carriers reporting a 20% improvement in support ticket resolution times.

- The market is also defined by fiscal sensitivity and network rebalancing, as demonstrated when the removal of an aviation tax in one region led to an immediate 15% surge in passenger volume, prompting a strategic fiscal migration of assets. This highlights carriers' agility in response to government policies.

What challenges does the Low-cost Carrier (LCC) Industry face during its growth?

- Severe aircraft delivery shortfalls and engine supply chain bottlenecks present a key challenge affecting industry growth.

- The market faces significant operational and financial challenges that constrain growth. Severe aircraft delivery shortfalls and engine supply chain bottlenecks are a primary concern, with a global commercial aircraft backlog exceeding 5,300 units, forcing carriers to extend leases on older, less efficient jets. This directly impacts fleet modernization and operational costs.

- Volatile energy prices represent another major headwind; geopolitical instability recently contributed to an 18.2% year-on-year increase in jet fuel prices in some markets.

- Furthermore, rising environmental compliance costs, including the phasing out of free carbon emission allowances and mandates for expensive Sustainable Aviation Fuel (SAF), are adding significant financial pressure, particularly in regions with aggressive decarbonization mandates that challenge the viability of the ultra-low-cost model.

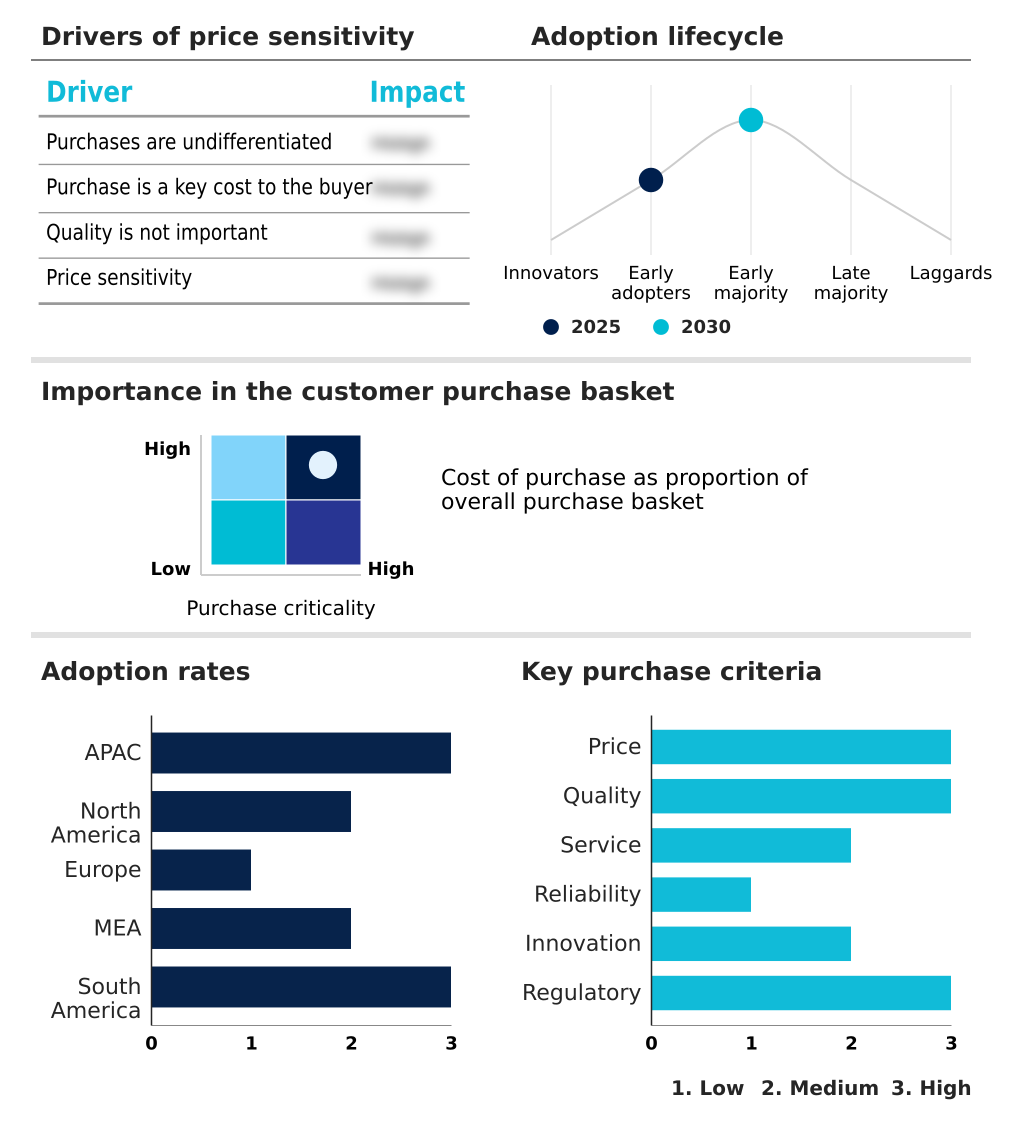

Exclusive Technavio Analysis on Customer Landscape

The low-cost carrier (lcc) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the low-cost carrier (lcc) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Low-cost Carrier (LCC) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, low-cost carrier (lcc) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aeroenlaces Nacionales SA de CV - Analysis indicates a focus on point-to-point air travel services, leveraging an ultra-low-cost pricing structure to target price-sensitive passenger segments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aeroenlaces Nacionales SA de CV

- Air Arabia PJSC

- Cebu Pacific

- Dubai Aviation Corp.

- easyJet plc

- Eurowings GmbH

- Flynas LCC

- Frontier Group Holdings Inc.

- Hong Kong Express Airways Ltd.

- InterGlobe Aviation Ltd.

- Move Travel Sdn Bhd

- Norwegian Air Shuttle ASA

- Pegasus Hava Tasimaciligi A.S.

- Ryanair Holdings plc

- Scoot Pte. Ltd.

- Southwest Airlines Co.

- Volaris

- Volotea S.A.

- Wizz Air Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Low-cost carrier (lcc) market

- In December, 2024, Volaris and Viva Aerobus announced a definitive merger agreement to form a new holding company, Grupo Mas Vuelos, aiming to create a dominant regional player with a combined fleet of over 250 aircraft.

- In January, 2025, Southwest Airlines officially began its transition to a standardized assigned seating system, introducing a tiered fare structure and extra legroom options to attract a larger share of the corporate travel segment.

- In February, 2025, Zipair operated the first commercial passenger flight in Asia equipped with high-speed Starlink satellite internet, signaling a strategic push towards enhancing the digital experience on long-haul budget routes.

- In March, 2025, Ryanair announced its largest-ever summer schedule for Sweden, an USD 800 million investment, in response to the Swedish government's decision to abolish the national aviation tax.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Low-cost Carrier (LCC) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 281 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.6% |

| Market growth 2026-2030 | USD 406530.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.4% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Egypt, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Low-cost Carrier (LCC) Market is fundamentally built on point-to-point routes and unbundled services, but it is now undergoing a critical evolution driven by fleet modernization and strategic repositioning. Carriers are aggressively replacing older fleets with next-generation narrowbody aircraft and, increasingly, widebody aircraft to enhance fuel efficiency and open new long-range markets.

- This transition is crucial, as some new airframes offer up to a 16% reduction in fuel burn, a vital metric given the volatility of jet fuel prices. The operational model is also changing, with a notable shift from open boarding to assigned seating and tiered fare structures, designed to attract higher-yield passengers.

- Digital connectivity, including satellite internet, is becoming a key differentiator. However, this growth is constrained by significant headwinds. The engine supply chain is a primary concern, with maintenance backlogs causing widespread groundings. Geopolitical instability and fiscal policy shifts, such as fluctuating aviation tax, create an unpredictable operating environment.

- Furthermore, environmental pressures are mounting, with mandates for Sustainable Aviation Fuel (SAF) and carbon emission allowances increasing operational costs, forcing carriers to balance expansion with decarbonization mandates.

What are the Key Data Covered in this Low-cost Carrier (LCC) Market Research and Growth Report?

-

What is the expected growth of the Low-cost Carrier (LCC) Market between 2026 and 2030?

-

USD 406.53 billion, at a CAGR of 15.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (Passenger service, and Cargo service), Type (Narrow body, and Wide body), Application (Individual, and Commercial) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Strategic hybridization and premiumization of service models, Severe aircraft delivery shortfalls and engine supply chain bottlenecks

-

-

Who are the major players in the Low-cost Carrier (LCC) Market?

-

Aeroenlaces Nacionales SA de CV, Air Arabia PJSC, Cebu Pacific, Dubai Aviation Corp., easyJet plc, Eurowings GmbH, Flynas LCC, Frontier Group Holdings Inc., Hong Kong Express Airways Ltd., InterGlobe Aviation Ltd., Move Travel Sdn Bhd, Norwegian Air Shuttle ASA, Pegasus Hava Tasimaciligi A.S., Ryanair Holdings plc, Scoot Pte. Ltd., Southwest Airlines Co., Volaris, Volotea S.A. and Wizz Air Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the high price sensitivity of consumers, which results in low brand switching costs and intense competition. Airlines are responding by adopting sophisticated ancillary revenue models and pursuing greater operational efficiency. The strategic shift toward a hybridization strategy is evident, as carriers that enhance service reliability can capture higher-yield segments.

- This has led to measurable outcomes; for instance, some operators have seen ancillary revenue contribute up to 40% of total revenue. Concurrently, network rebalancing is common, with carriers demonstrating fiscal migration by shifting capacity away from regions with high airport fees, where costs have increased by as much as 50%, toward more favorable tax environments.

- This agility is crucial for survival in a market with low entry barriers for niche routes but significant economies of scale protecting incumbents.

We can help! Our analysts can customize this low-cost carrier (lcc) market research report to meet your requirements.

RIA -

RIA -