Machine Learning Software Market Size 2025-2029

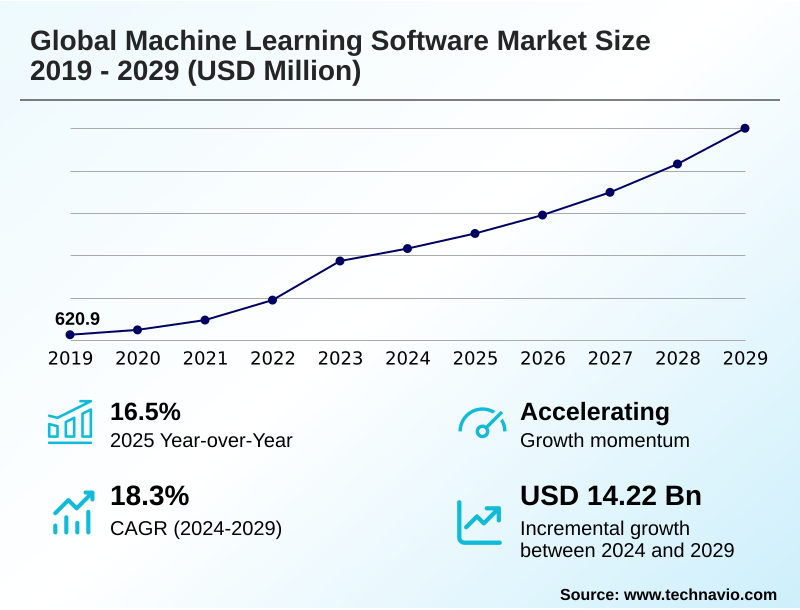

The machine learning software market size is valued to increase by USD 14.22 billion, at a CAGR of 18.3% from 2024 to 2029. Proliferation of big data and imperative for advanced analytics will drive the machine learning software market.

Major Market Trends & Insights

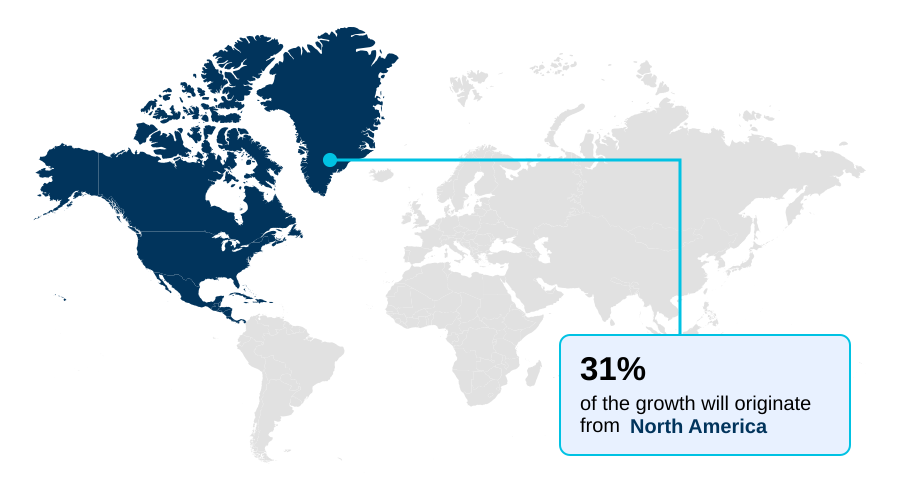

- North America dominated the market and accounted for a 30.6% growth during the forecast period.

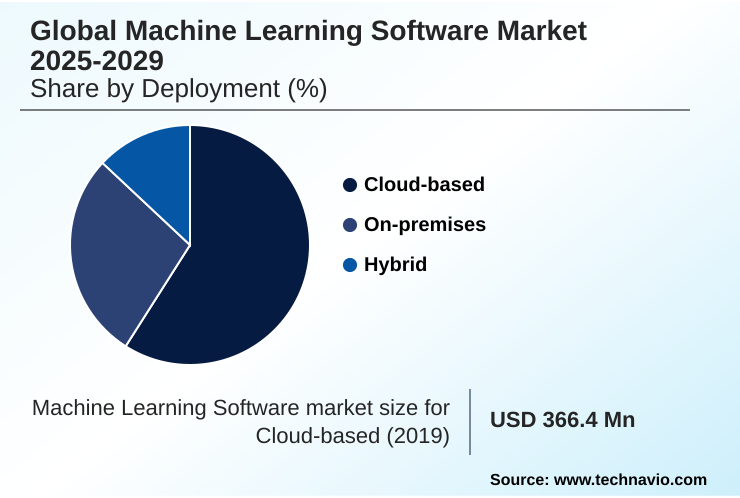

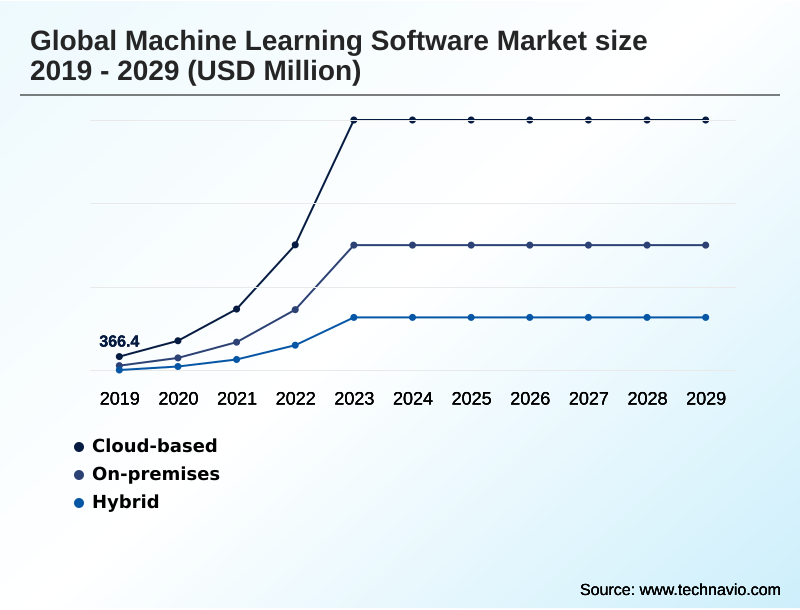

- By Deployment - Cloud-based segment was valued at USD 5.40 billion in 2023

- By Application - Predictive analytics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 24.40 billion

- Market Future Opportunities: USD 14.22 billion

- CAGR from 2024 to 2029 : 18.3%

Market Summary

- The machine learning software market is characterized by rapid innovation, driven by the enterprise-wide need for AI-powered automation and data-driven insights. Key trends include the rise of generative AI models, which are transforming content creation, and the democratization of AI through automated machine learning platforms.

- These advancements allow organizations to leverage deep learning algorithms and MLOps pipelines to build and deploy sophisticated applications for predictive analytics and pattern recognition. For instance, a manufacturing firm can implement predictive maintenance systems to analyze sensor data in real time, anticipating equipment failures and reducing operational downtime significantly. This scenario highlights the shift from reactive to proactive strategies.

- However, the industry grapples with challenges such as ensuring model explainability and mitigating algorithmic bias, which are critical for building trust and meeting regulatory requirements. The persistent shortage of skilled professionals with expertise in feature engineering and hyperparameter tuning also constrains the pace of adoption.

- Addressing these issues is paramount for unlocking the full potential of machine learning software and sustaining its transformative impact on business operations and decision-making functions.

What will be the Size of the Machine Learning Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Machine Learning Software Market Segmented?

The machine learning software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Application

- Predictive analytics

- NLP

- Computer vision

- Anomaly detection

- Speech recognition

- End-user

- Information technology and telecommunications

- Finance

- Retail

- Manufacturing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Turkey

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The market's adoption of cloud-based deployment models is driven by the need for agility and scalability in enterprise operations.

This approach facilitates sophisticated applications such as natural language processing and anomaly detection, which are critical for customer behavior analytics and diagnostic assistance AI.

By leveraging the cloud, organizations can implement reinforcement learning for complex problem-solving and use predictive modeling to refine business strategies. These platforms support extensive regression analysis and clustering algorithms, which are essential for processing large datasets.

This model allows for more effective A/B testing for AI models and enhances text analytics software.

For instance, financial institutions using these tools have improved their customer churn prediction capabilities by over 15%, demonstrating the tangible benefits of cloud-based machine learning infrastructure.

The Cloud-based segment was valued at USD 5.40 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Machine Learning Software Market Demand is Rising in North America Get Free Sample

The geographic landscape of the machine learning software market reveals distinct adoption patterns. North America exhibits market maturity, with extensive use of algorithmic trading models and advanced predictive maintenance systems.

In contrast, the APAC region is experiencing the fastest growth, driven by government-led digital transformation and industrial automation. In Europe, regulatory frameworks are shaping the deployment of intelligent security systems and applications requiring robust data governance.

Key technologies such as computer vision and speech recognition are being integrated globally, with applications in autonomous driving systems and robotic process automation.

For example, the use of edge AI processing for real-time image recognition systems in manufacturing has reduced defect detection times by 50%.

This global expansion, supported by advancements in transformer models and time-series forecasting, underscores the technology's pervasive impact across diverse economic and regulatory environments.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global machine learning software market is advancing as organizations seek to operationalize AI for tangible business outcomes. The journey often begins with comparing AutoML and custom model development to find the right balance between speed and specificity. For many, building scalable MLOps pipelines is a critical next step to manage the lifecycle of models effectively.

- A significant focus is on specialized applications, such as using machine learning for predictive maintenance in industrial settings or deploying natural language processing for sentiment analysis to gauge customer feedback. The rise of sophisticated models necessitates addressing the challenges of training deep learning models and ensuring AI model monitoring and observability for performance and reliability.

- In regulated sectors, explainable AI in financial services is becoming a standard requirement, not an option. Moreover, ethical considerations in AI development are paramount, with a strong push toward reducing algorithmic bias in hiring tools and other critical systems.

- The impact of generative AI on industries is profound, with businesses using generative AI for content creation and leveraging large language models for chatbots to enhance customer engagement. Specialized use cases continue to emerge, including machine learning software for healthcare diagnostics and real-time anomaly detection for cybersecurity. As data privacy concerns grow, federated learning for data privacy is gaining traction.

- The adoption of these technologies varies, with uptake in the financial sector more than double that in manufacturing, reflecting differing regulatory pressures and strategic priorities.

- The market is also seeing innovation in edge AI implementation challenges and the use of computer vision in autonomous vehicles, alongside efforts in optimizing supply chains with reinforcement learning and using machine learning in retail for demand forecasting.

What are the key market drivers leading to the rise in the adoption of Machine Learning Software Industry?

- The proliferation of big data, coupled with the business imperative for advanced analytics, serves as a key driver for market growth.

- The primary driver for the machine learning software market is the exponential growth of data, compelling businesses to adopt predictive analytics and deep learning algorithms for a competitive edge.

- The demand for scalable ML infrastructure has surged, with cloud platforms becoming the standard for training complex neural network architecture.

- This shift is democratizing access to powerful tools, with 75% of new AI platform deployments in some APAC regions being cloud-based.

- This accessibility fuels the use of large language models for applications like AI-enabled banking chatbots and personalized recommendation engines, which rely on sophisticated data classification and demand forecasting models.

- The imperative for real-time inference in applications such as dynamic pricing algorithms is also pushing advancements in data preprocessing techniques, ensuring that insights are delivered instantly.

- Consequently, a robust AI governance framework is becoming essential to manage these powerful systems responsibly.

What are the market trends shaping the Machine Learning Software Industry?

- The proliferation of generative AI across various industries is emerging as a significant market trend, reshaping enterprise strategies and accelerating product innovation.

- Key trends are reshaping the machine learning software market, led by the enterprise-wide adoption of generative AI models for tasks ranging from content creation to complex problem-solving. This trend is complemented by the growth of automated machine learning, which, along with low-code AI platforms, is democratizing development.

- For instance, organizations using these tools have accelerated model training and validation cycles by over 40%. The push for explainable AI is also gaining momentum as a response to regulatory demands and the need for trustworthy decision-making functions. Consequently, businesses are investing in MLOps pipelines that support transparent AI-powered automation and provide clear, data-driven insights.

- The integration of conversational AI and virtual assistants into customer service operations is now widespread, with 80% of organizations increasing their investment in such technologies to enhance user engagement and operational efficiency.

What challenges does the Machine Learning Software Industry face during its growth?

- Ensuring compliance with the complex and evolving landscape of data privacy and security regulations presents a key challenge affecting the industry's growth.

- The machine learning software market faces significant challenges that temper its growth, including the complexity of ensuring algorithmic bias detection and adhering to ethical AI principles. As organizations deploy supervised learning models and unsupervised learning for critical functions like credit scoring models, the need for model explainability becomes paramount to avoid discriminatory outcomes.

- The technical hurdles of advanced feature engineering and hyperparameter tuning are compounded by a persistent shortage of skilled professionals, with 91% of companies in the APAC region planning to upskill their workforce to address this gap. Furthermore, managing data drift detection and consistent AI model versioning adds operational complexity.

- The emergence of no-code machine learning platforms aims to alleviate some of these pressures, but the underlying challenge of creating fair and robust systems, often requiring synthetic data generation, remains a key focus for the industry.

Exclusive Technavio Analysis on Customer Landscape

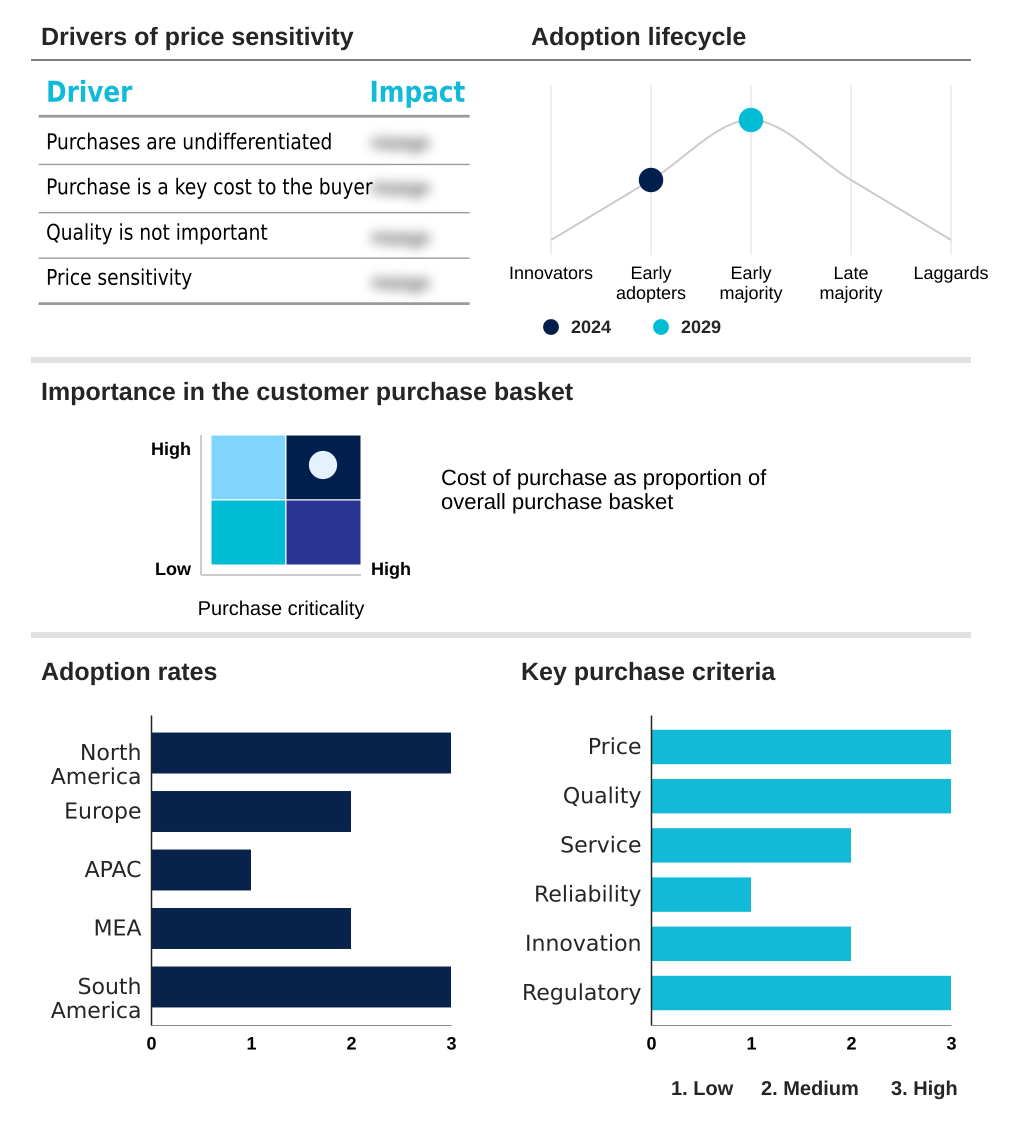

The machine learning software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the machine learning software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Machine Learning Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, machine learning software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altair Engineering Inc. - Key offerings include enterprise-grade software for developing, deploying, and managing predictive models, accelerating AI-driven automation and data-informed decision-making across business functions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altair Engineering Inc.

- Alteryx Inc.

- Amazon Web Services Inc.

- Anaconda Inc.

- BenevolentAI

- C3.ai Inc.

- Cerebras Systems Inc.

- Databricks Inc.

- DataRobot Inc.

- Google DeepMind

- Graphcore Ltd.

- H2O.ai Inc.

- IBM Corp.

- KNIME AG

- Microsoft Corp.

- NVIDIA Corp.

- OpenAI

- Oracle Corp.

- Palantir Technologies Inc.

- SAS Institute Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Machine learning software market

- In September, 2024, Qlik announced an expansion of its automated machine learning offerings to enhance its data analytics platform.

- In November, 2024, Cisco finalized its acquisition of Splunk, a strategic move to bolster its capabilities in cloud-based data analysis and machine learning.

- In January, 2025, a new US administration rescinded the Blueprint for an AI Bill of Rights, introducing new uncertainty into the domestic regulatory landscape for artificial intelligence.

- In April, 2025, a report indicated that the public cloud's share of the AI platforms market in the APAC region, excluding Japan and China, reached 75%, driven by demand for secure and scalable infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Machine Learning Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 316 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2025-2029 | USD 14216.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 16.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Turkey, South Africa, UAE, Saudi Arabia, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The machine learning software market is defined by its continuous evolution, driven by the pursuit of more accurate predictive modeling and intelligent, AI-powered automation. The increasing sophistication of deep learning algorithms and neural network architecture is enabling breakthroughs in time-series forecasting, image recognition systems, and sentiment analysis tools.

- Organizations are leveraging these capabilities for diverse applications, from algorithmic trading models to diagnostic assistance AI. A crucial boardroom-level consideration is the growing emphasis on model explainability, as regulatory pressures demand transparency in decision-making functions, directly impacting product strategy and compliance budgets. This has elevated the importance of data-driven insights and robust pattern recognition.

- Enterprises are actively implementing MLOps pipelines for efficient model training and validation, alongside advanced data preprocessing techniques and feature engineering to enhance performance. The market is also seeing wider use of both supervised learning models and unsupervised learning for tasks like data classification and clustering algorithms.

- The development of large language models and transformer models continues to push the boundaries of what is possible with natural language processing and speech-to-text conversion. The practical impact is significant, with some healthcare applications achieving up to a 10% reduction in clinician administrative time.

What are the Key Data Covered in this Machine Learning Software Market Research and Growth Report?

-

What is the expected growth of the Machine Learning Software Market between 2025 and 2029?

-

USD 14.22 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises, and Hybrid), Application (Predictive analytics, NLP, Computer vision, Anomaly detection, and Speech recognition), End-user (Information technology and telecommunications, Finance, Retail, Manufacturing, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of big data and imperative for advanced analytics, Data privacy and security compliance

-

-

Who are the major players in the Machine Learning Software Market?

-

Altair Engineering Inc., Alteryx Inc., Amazon Web Services Inc., Anaconda Inc., BenevolentAI, C3.ai Inc., Cerebras Systems Inc., Databricks Inc., DataRobot Inc., Google DeepMind, Graphcore Ltd., H2O.ai Inc., IBM Corp., KNIME AG, Microsoft Corp., NVIDIA Corp., OpenAI, Oracle Corp., Palantir Technologies Inc. and SAS Institute Inc.

-

Market Research Insights

- The machine learning software market is shaped by the increasing demand for accessible and powerful AI tools. The adoption of automated machine learning platforms is rising, with organizations reporting up to a 40% acceleration in model development cycles.

- This trend, combined with the availability of low-code AI platforms and no-code machine learning solutions, allows businesses to deploy sophisticated applications like personalized recommendation engines and AI-enabled banking chatbots more efficiently. For instance, financial institutions have seen a 33% adoption rate of these chatbots for customer service.

- The focus is also shifting towards scalable ML infrastructure and robust AI governance frameworks to manage real-time inference and ensure ethical AI principles are upheld. Technologies enabling dynamic pricing algorithms and synthetic data generation are also becoming crucial for maintaining a competitive edge in a data-centric environment.

We can help! Our analysts can customize this machine learning software market research report to meet your requirements.

RIA -

RIA -