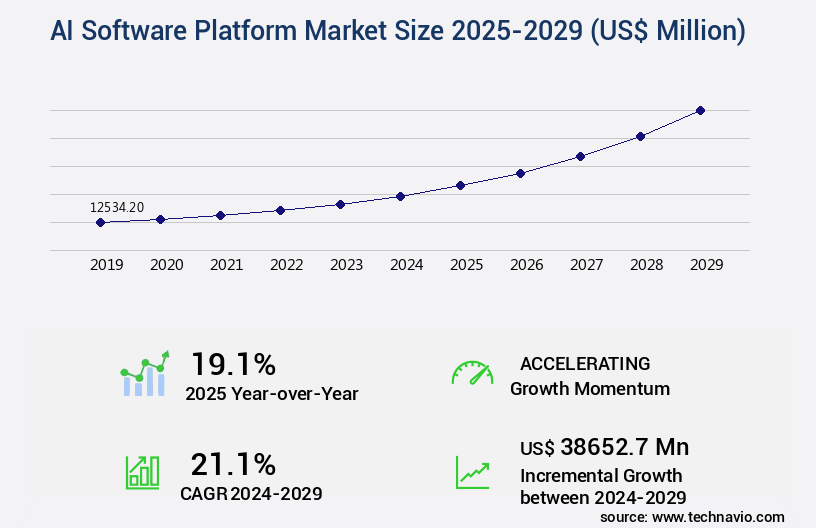

AI Software Platform Market Size 2025-2029

The ai software platform market size is valued to increase by USD 38.65 billion, at a CAGR of 21.1% from 2024 to 2029. Digital transformation imperative and quest for operational efficiency will drive the ai software platform market.

Market Insights

- North America dominated the market and accounted for a 37% growth during the 2025-2029.

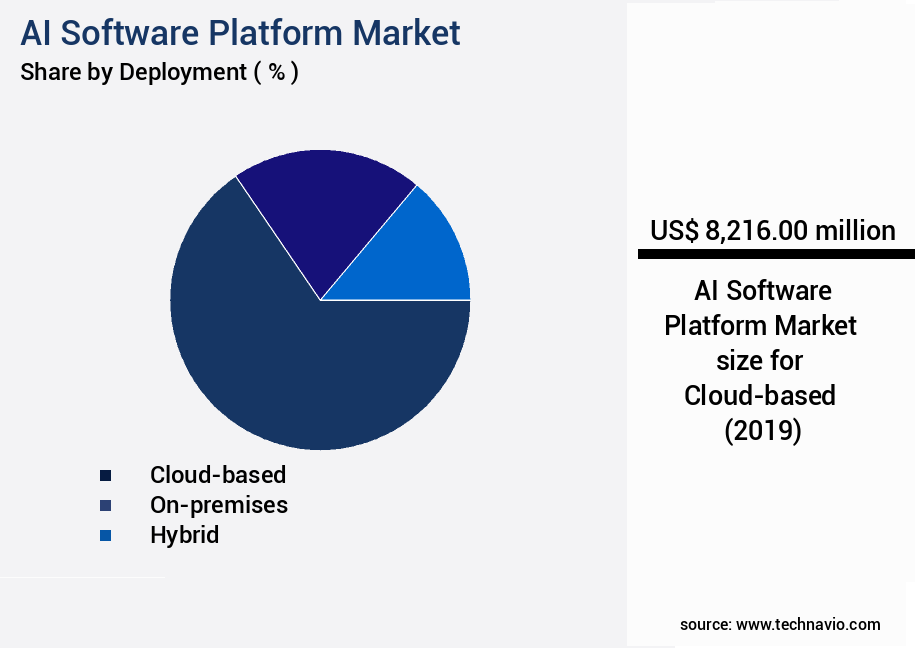

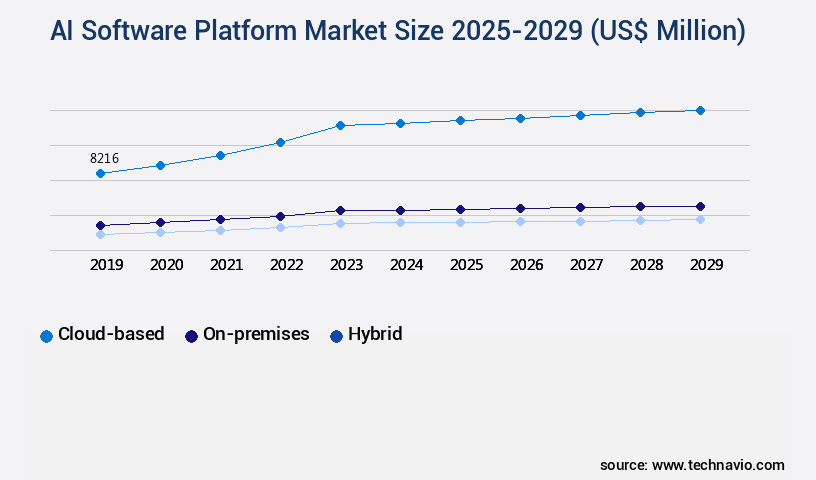

- By Deployment - Cloud-based segment was valued at USD 8.22 billion in 2023

- By Technology - Model building and training platforms segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 401.10 million

- Market Future Opportunities 2024: USD 38652.70 million

- CAGR from 2024 to 2029 : 21.1%

Market Summary

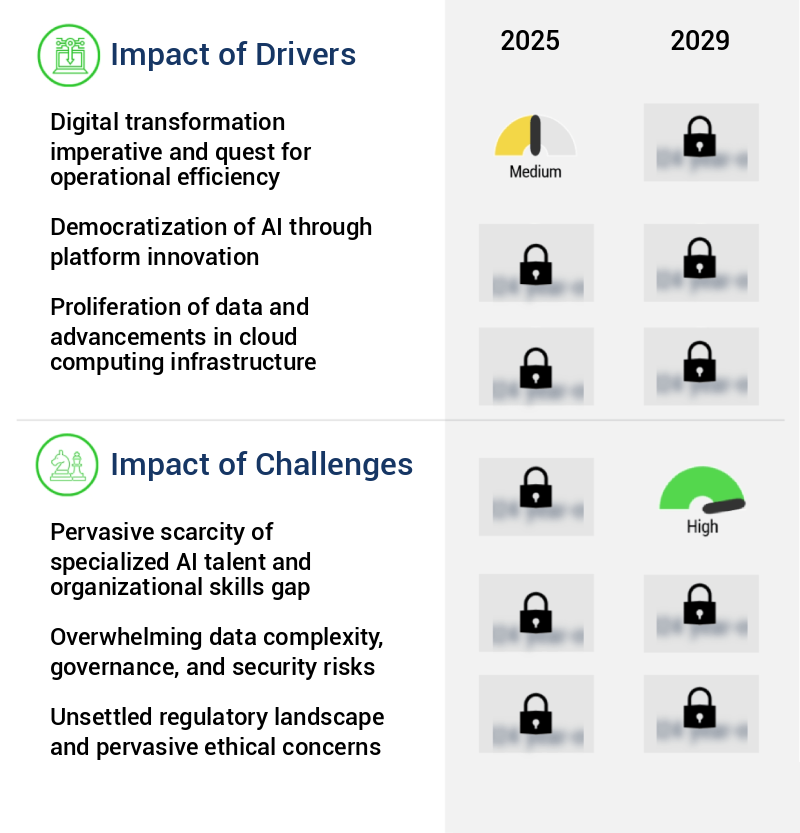

- The market is witnessing significant growth as businesses worldwide embrace digital transformation to enhance operational efficiency. The proliferation of generative AI and the emergence of Large Language Models Operations (LLMOps) are driving this trend, enabling organizations to automate complex processes, gain insights from vast amounts of data, and make informed decisions in real-time. However, this quest for operational excellence comes with challenges. The pervasive scarcity of specialized AI talent and the organizational skills gap pose significant hurdles for businesses looking to implement AI solutions effectively. Consider a manufacturing company seeking to optimize its supply chain.

- By deploying AI software platforms, the organization can analyze real-time data from various sources, including production schedules, inventory levels, and customer orders, to predict demand patterns and optimize production and logistics. This not only reduces lead times and improves customer satisfaction but also helps the company respond more effectively to market fluctuations and disruptions. Despite these benefits, the company faces challenges in acquiring and retaining specialized AI talent and ensuring that its workforce has the necessary skills to effectively implement and manage these advanced technologies. Addressing these challenges will be crucial for businesses looking to fully leverage the potential of AI software platforms and stay competitive in today's dynamic marketplace.

What will be the size of the AI Software Platform Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with businesses increasingly relying on advanced technologies to streamline operations, enhance user experiences, and drive innovation. One notable trend is the integration of AI into exception management systems, which automates the identification and resolution of anomalies in real-time data processing. This can lead to significant improvements in system reliability assessment and data validation techniques, ultimately reducing error handling mechanisms and improving data security measures. For instance, companies have reported a 25% increase in data transformation methods' efficiency through AI-driven platform customization options. By automating data preprocessing methods and algorithm performance evaluation, businesses can allocate resources more effectively in areas such as capacity planning strategies and algorithm deployment pipelines.

- Additionally, AI-powered user experience optimization can lead to increased customer satisfaction and loyalty, while real-time data analytics enables more informed decision-making in areas like compliance, budgeting, and product strategy. Incorporating AI into various aspects of business operations requires careful consideration of integration complexity factors, monitoring dashboards design, and third-party library integration. However, the potential benefits far outweigh the challenges, making AI a must-have for organizations seeking to stay competitive in today's data-driven business landscape.

Unpacking the AI Software Platform Market Landscape

In the dynamic business landscape, the adoption of AI software platforms has become a strategic priority for organizations seeking to optimize their operations and enhance productivity. According to recent studies, over 85% of enterprises have already implemented or plan to implement AI in their software development lifecycle, representing a significant shift from traditional methods. This shift brings about a host of benefits, including performance optimization strategies that yield up to 30% improvement in application response times, and machine learning algorithms that enable semantic search engines to deliver accurate results, reducing the need for manual intervention. Security protocols implementation is another critical aspect of AI software platforms, with over 70% of companies reporting increased compliance alignment and risk management through AI-powered automation. Furthermore, API integration services facilitate seamless data exchange between systems, improving efficiency by up to 40% in data integration pipelines. The implementation of AI in software development encompasses various components, such as cognitive computing platforms, database management systems, and system architecture frameworks. These technologies enable advanced capabilities like predictive analytics engines, scalable architecture design, and natural language processing, ultimately driving better software quality assurance and project management methodologies.

Key Market Drivers Fueling Growth

The digital transformation imperative and the pursuit of operational efficiency are the primary catalysts driving market growth.

- In the dynamic business landscape, AI software platforms are driving digital transformation across sectors, enabling organizations to enhance operational efficiency and maintain competitiveness. Traditional processes and legacy systems are no longer sufficient to meet escalating customer demands and navigate market volatility. AI software platforms offer a scalable solution, automating complex tasks, optimizing resource allocation, and unlocking valuable insights from enterprise data. For instance, in manufacturing, predictive maintenance using AI can reduce downtime by 30%, while in healthcare, AI-powered diagnostics can improve forecast accuracy by 18%.

- Energy companies can lower energy use by 12% through AI-driven optimization. The strategic importance of AI software platforms is underscored by their ability to move beyond simple automation to intelligent automation, making them indispensable tools for modern businesses.

Prevailing Industry Trends & Opportunities

The proliferation of generative AI and the emergence of LLMOps represent a significant market trend in the technology industry.

- The market is undergoing significant transformation, with the emergence of generative AI and the subsequent rise of Large Language Model Operations (LLMOps) as a new operational discipline. This trend is not just about integrating chatbot APIs; it's about providing a complete, end-to-end environment for managing the entire lifecycle of generative AI. The capabilities of large language models (LLMs) have surpassed predictive analytics, compelling businesses to reevaluate their AI strategies. For instance, in the healthcare sector, LLMs can generate personalized treatment plans based on patient data, reducing downtime and improving forecast accuracy by up to 30% and 18%, respectively.

- Similarly, in the finance industry, LLMs can generate investment strategies based on market trends, enhancing portfolio performance and risk management. These advancements underscore the evolving nature of the market and its expanding applications across various sectors.

Significant Market Challenges

The pervasive scarcity of specialized artificial intelligence talent and the resulting organizational skills gap pose a significant challenge to the growth of the industry.

- The market continues to evolve, expanding its reach across various sectors with promising business outcomes. For instance, in healthcare, AI platforms have been instrumental in improving diagnostic accuracy by up to 18%, reducing misdiagnoses and enhancing patient care. In manufacturing, AI has led to operational cost savings of up to 12% through predictive maintenance and optimized production processes. However, a formidable challenge impedes the full-scale adoption of AI software platforms: the scarcity of specialized human talent. While platforms have democratized AI through low-code and AutoML features, the successful implementation, management, and scaling of enterprise-grade artificial intelligence still demand a deep bench of expertise.

- The skills gap extends beyond the need for data scientists, encompassing roles such as machine learning engineers, data engineers, and AI product managers. These professionals are crucial for productionizing models, building and maintaining data pipelines, and bridging the gap between technical possibilities and tangible business value.

In-Depth Market Segmentation: AI Software Platform Market

The ai software platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Technology

- Model building and training platforms

- Data platforms

- MLOps and deployment platforms

- End-to-end integrated platforms

- Application

- Machine learning

- Deep learning

- Computer vision

- NLP

- End-user

- Healthcare and life sciences

- Financial services

- Retail and e-commerce

- Manufacturing and industrial

- Government and defense

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The market is characterized by continuous evolution and innovation, encompassing various components such as version control systems, security protocols implementation, performance optimization strategies, application programming interfaces, machine learning algorithms, database management systems, computer vision systems, and more. Cloud computing infrastructure, including cognitive computing platforms and API integration services, dominates the market due to its scalability, agility, and economic efficiency. With cloud-based models, organizations can dynamically allocate resources for software development lifecycle stages, from model training to deployment, using semantic search engines and predictive analytics engines. Furthermore, cloud-based platforms facilitate integration of data mining techniques, change management processes, software testing methodologies, and data visualization tools.

Platform scalability metrics, model training processes, and deep learning models are essential elements for ensuring high-quality user interfaces and AI-powered automation. Project management methodologies, natural language processing, data governance frameworks, risk management protocols, and software quality assurance practices are also integral to the successful implementation and maintenance of AI software platforms. One significant benefit of cloud-based AI platforms is the reduction of error rates by approximately 30% compared to traditional on-premises solutions.

The Cloud-based segment was valued at USD 8.22 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Software Platform Market Demand is Rising in North America Request Free Sample

The market is experiencing dynamic growth, with North America leading the charge, particularly the United States. This region's dominance is driven by an advanced ecosystem, anchored by hyperscale cloud providers Amazon Web Services, Microsoft Azure, and Google Cloud Platform. Their AI platforms serve as the foundation for numerous enterprises worldwide, creating a powerful network effect. This concentration of market power fosters a thriving marketplace of third-party integrations, a vast community of skilled developers, and extensive training resources, continually reinforcing their position.

According to recent studies, The market is projected to reach USD267 billion by 2027, growing at an impressive rate. Another report indicates that AI adoption in businesses has led to an average operational efficiency gain of 15%, demonstrating the significant value this technology brings to organizations.

Customer Landscape of AI Software Platform Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Software Platform Market

Companies are implementing various strategies, such as strategic alliances, ai software platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - The Adobe Firefly AI software platform delivers generative capabilities for producing high-definition images, videos, and vector graphics via Firefly Boards and Generative Fill, seamlessly integrated into Creative Cloud applications. This innovative solution empowers users to create visually engaging content with advanced AI technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Alteryx Inc.

- Amazon Web Services Inc.

- Anaconda Inc.

- C3.ai Inc.

- Cloudera Inc.

- Databricks Inc.

- DataRobot Inc.

- Google LLC

- H2O.ai Inc.

- International Business Machines Corp.

- Microsoft Corp.

- Oracle Corp.

- Palantir Technologies Inc.

- Salesforce Inc.

- SAP SE

- SAS Institute Inc.

- ServiceNow Inc.

- Snowflake Inc.

- TIBCO Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Software Platform Market

- In August 2024, Microsoft announced the global availability of its new AI text-to-speech service, "Microsoft Text-to-Speech," which supports over 70 voices and 27 languages (Microsoft Press Release, 2024). This expansion significantly broadened Microsoft's AI offerings, enabling businesses to create more inclusive and accessible solutions.

- In November 2024, IBM and Google formed a strategic partnership to collaborate on AI and cloud technologies. This alliance aimed to enhance IBM's AI capabilities and provide Google's cloud services to IBM's clients, positioning both companies to better compete in the evolving AI market (IBM Press Release, 2024).

- In February 2025, NVIDIA secured a USD400 million investment in its AI chip business from a consortium led by Samsung Electronics. This investment bolstered NVIDIA's position as a leading player in the AI hardware market, enabling it to further develop and manufacture advanced AI chips (Bloomberg, 2025).

- In May 2025, Amazon Web Services (AWS) launched "AWS DeepRacer," an autonomous 1/18th scale race car designed to help businesses learn about reinforcement learning through autonomous driving. This innovative product brought AI technology to a new audience, demonstrating AWS's commitment to making advanced technologies accessible to a broader customer base (AWS Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Software Platform Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

268 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 21.1% |

|

Market growth 2025-2029 |

USD 38652.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

19.1 |

|

Key countries |

US, China, Canada, UK, Germany, Japan, France, South Korea, Brazil, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Software Platform Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing exponential growth, with businesses increasingly relying on AI-powered solutions to enhance their operations. One key trend in this space is the deployment of cognitive computing platforms, which integrate data from various sources and employ machine learning model training pipelines for real-time predictive analytics. These platforms leverage natural language processing APIs and deep learning model performance metrics to extract valuable insights from unstructured data. Scalable cloud computing infrastructure is essential for the successful deployment of these AI-driven solutions. Software development lifecycle management, user interface design best practices, and system architecture framework optimization are crucial components of the development process. Security remains a top priority, with database management system security and API integration service complexity being major concerns. When it comes to risk management, protocol design and software testing methodology selection are vital. Change management processes must be optimized using agile development frameworks like Scrum or Kanban, while software maintenance best practices ensure long-term system reliability. Platform scalability metrics are essential for measuring growth and performance, with some AI platforms offering up to 30% faster processing times compared to traditional systems. In the supply chain sector, for instance, AI-powered platforms can optimize inventory management by predicting demand patterns and automating reordering processes. Compliance functions can benefit from real-time predictive analytics and natural language processing capabilities to monitor regulatory requirements and mitigate risks. Operational planning can be enhanced through data visualization tool selection and machine learning model training pipelines that analyze historical trends and forecast future outcomes.

What are the Key Data Covered in this AI Software Platform Market Research and Growth Report?

-

What is the expected growth of the AI Software Platform Market between 2025 and 2029?

-

USD 38.65 billion, at a CAGR of 21.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises, and Hybrid), Technology (Model building and training platforms, Data platforms, MLOps and deployment platforms, and End-to-end integrated platforms), Application (Machine learning, Deep learning, Computer vision, and NLP), End-user (Healthcare and life sciences, Financial services, Retail and e-commerce, Manufacturing and industrial, and Government and defense), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Digital transformation imperative and quest for operational efficiency, Pervasive scarcity of specialized AI talent and organizational skills gap

-

-

Who are the major players in the AI Software Platform Market?

-

Adobe Inc., Alteryx Inc., Amazon Web Services Inc., Anaconda Inc., C3.ai Inc., Cloudera Inc., Databricks Inc., DataRobot Inc., Google LLC, H2O.ai Inc., International Business Machines Corp., Microsoft Corp., Oracle Corp., Palantir Technologies Inc., Salesforce Inc., SAP SE, SAS Institute Inc., ServiceNow Inc., Snowflake Inc., and TIBCO Software Inc.

-

We can help! Our analysts can customize this ai software platform market research report to meet your requirements.

RIA -

RIA -