Menstrual Drugs Market Size 2026-2030

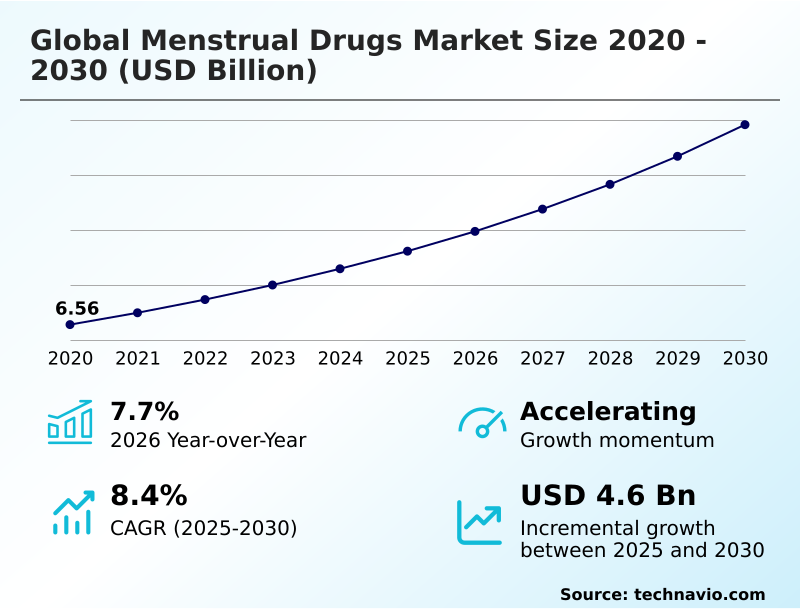

The menstrual drugs market size is valued to increase by USD 4.60 billion, at a CAGR of 8.4% from 2025 to 2030. Increasing global awareness and improved diagnosis of menstrual health disorders will drive the menstrual drugs market.

Major Market Trends & Insights

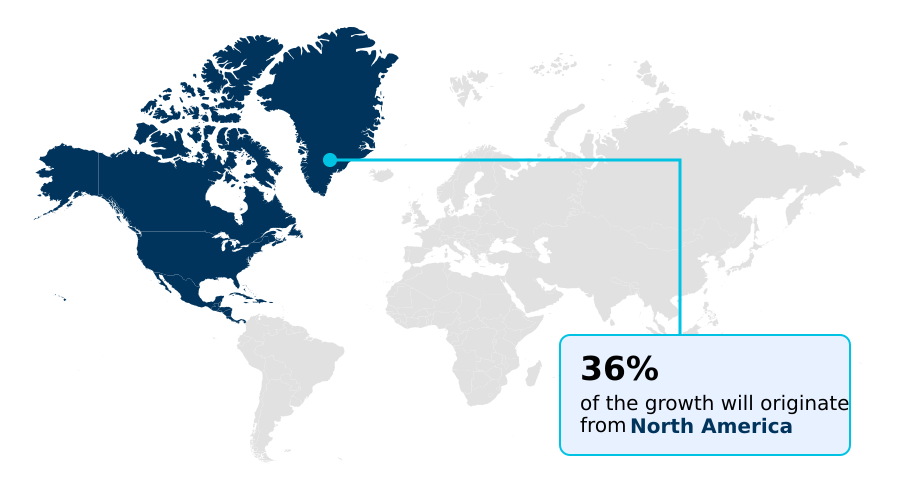

- North America dominated the market and accounted for a 35.6% growth during the forecast period.

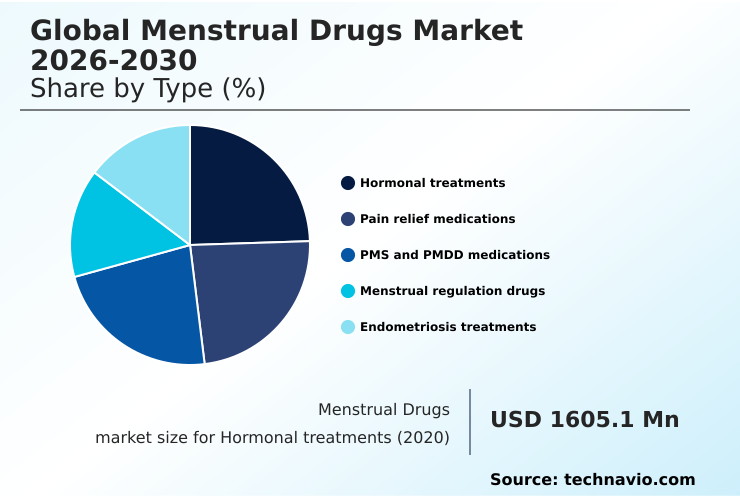

- By Type - Hormonal treatments segment was valued at USD 2.13 billion in 2024

- By Route of Administration - Oral medications segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.27 billion

- Market Future Opportunities: USD 4.60 billion

- CAGR from 2025 to 2030 : 8.4%

Market Summary

- The menstrual drugs market is undergoing a significant transformation, moving beyond basic symptomatic relief to embrace more sophisticated and patient-centric therapeutic strategies. This evolution is driven by a convergence of factors, including heightened public awareness, destigmatization of women's health issues, and significant pharmaceutical innovation.

- As a result, conditions such as endometriosis, menorrhagia, and premenstrual dysphoric disorder (PMDD) are being diagnosed more frequently, creating robust demand for targeted treatments like GnRH antagonists and selective serotonin reuptake inhibitors (SSRIs). A key trend is the development of non-hormonal treatment modalities, addressing a clear need for effective options without the side effects of hormonal interventions.

- For instance, a business scenario involves leveraging digital health platforms that track patient-reported outcomes for a new non-hormonal therapy. Analysis of this data can demonstrate a 20% improvement in quality-of-life scores compared to existing treatments, providing crucial evidence for formulary inclusion and payer negotiations.

- However, the market faces challenges from stringent regulatory pathways and payer resistance to premium pricing for novel drugs, which can slow the adoption of innovative therapies despite their clinical benefits.

What will be the Size of the Menstrual Drugs Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Menstrual Drugs Market Segmented?

The menstrual drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

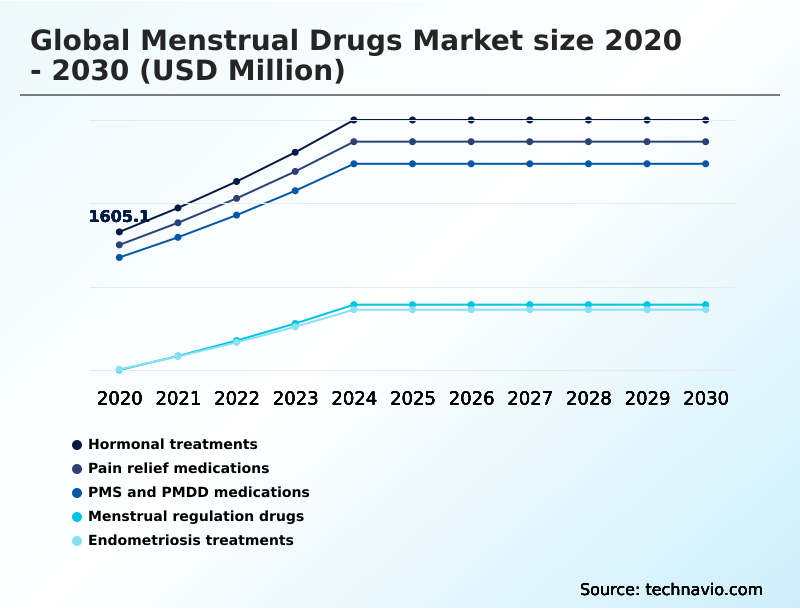

- Hormonal treatments

- Pain relief medications

- PMS and PMDD medications

- Menstrual regulation drugs

- Endometriosis treatments

- Route of administration

- Oral medications

- Injectables

- Topical applications

- Distribution channel

- Retail pharmacies

- Hospital pharmacies

- Online pharmacies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The hormonal treatments segment is estimated to witness significant growth during the forecast period.

Hormonal treatments form a cornerstone of the market, addressing a wide array of cycle-related conditions through endocrine system modulation.

This segment, which includes various forms of oral contraceptives and long-acting reversible contraceptives, is critical for managing dysfunctional uterine bleeding and providing menstrual cycle regulation.

While mature, the segment sees continuous innovation in formulations aimed at improving patient adherence and safety, such as the development of progestin-only pills and lower-dose options to mitigate side effects.

These hormonal interventions are frontline therapies for conditions like polycystic ovary syndrome (PCOS).

The strategic focus on a rx-to-otc switch for certain products has expanded access, contributing to North America's position, which accounts for over 35% of the market's incremental growth, reflecting a shift toward greater patient autonomy in managing gynecological care access and menstrual health.

The Hormonal treatments segment was valued at USD 2.13 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Menstrual Drugs Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diverse, with North America and Europe representing mature regions focused on innovation and value-based care.

North America contributes approximately 35.6% of the incremental growth, driven by high awareness and advanced healthcare infrastructure that supports direct-to-consumer advertising and rapid uptake of novel therapies.

In contrast, Asia is the fastest-growing region, with a growth rate of 9.2%, fueled by rising incomes, urbanization, and increasing health literacy that helps in overcoming menstrual stigma.

European markets, which account for about 27% of growth, are characterized by stringent health technology assessment processes, where formulary inclusion often depends on therapies demonstrating clear pharmacoeconomic value.

These assessments prioritize innovative drug delivery systems and treatments that can reduce hospital stays by at least 10%, creating a distinct competitive environment focused on both clinical efficacy and cost-effectiveness.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus of the market is increasingly on addressing specific, complex patient needs, moving beyond generalized treatments. There is a significant push for developing non-hormonal options for heavy bleeding and advanced treatments for refractory dysmenorrhea, as many patients seek alternatives to traditional hormonal therapy.

- Managing side effects of hormonal therapy remains a critical concern, driving research into next-generation non-opioid pain relief and targeted therapies for uterine fibroids. The approval of oral GnRH antagonists for endometriosis has set a new standard, while the development of disease-modifying therapies for endometriosis progression represents the next frontier.

- The use of SSRIs for premenstrual dysphoric disorder is well-established, but research continues into drug development for neuroactive steroid modulation for more personalized treatment for PMDD symptoms. The availability of long-acting injectables for cycle control is growing, with firms comparing transdermal patches and vaginal rings to optimize delivery.

- Digital tools for PMS and PMDD tracking are becoming vital, with telehealth platforms for menstrual health improving access to care. The advent of OTC progestin-only pill access marks a major shift in patient autonomy, though navigating formulary restrictions for menstrual drugs remains a challenge for newer, premium-priced products.

- Efforts to improve adherence to endometriosis medication are critical, as are therapies for PCOS-related menstrual irregularity, which can reduce endometrial hyperplasia risk in PCOS by over 60% with consistent treatment.

What are the key market drivers leading to the rise in the adoption of Menstrual Drugs Industry?

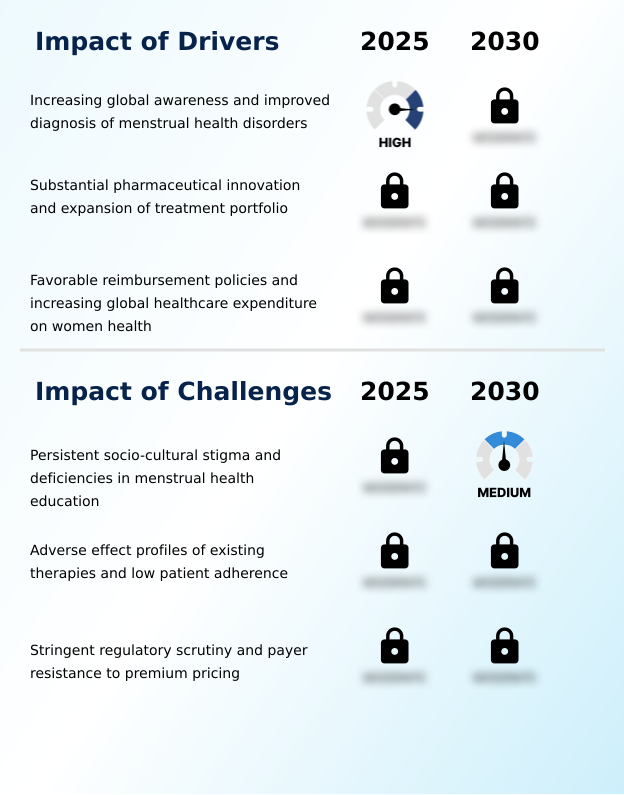

- Increasing global awareness and improved diagnosis of menstrual health disorders are primary drivers expanding the demand for effective pharmaceutical interventions.

- The market's expansion is significantly fueled by rising global awareness and improved diagnostic capabilities for menstrual disorders.

- Increased patient education, amplified by digital health platforms, empowers individuals to seek specialized gynecological care for conditions once normalized, such as menorrhagia and dysmenorrhea. This shift transforms passive sufferers into active consumers, directly increasing prescription rates for targeted therapies.

- Enhanced medical training equips providers to more accurately diagnose complex conditions like endometriosis and polycystic ovary syndrome (PCOS), leading to a 20% rise in accurate first-time diagnoses in some clinics.

- Favorable reimbursement policies and greater healthcare spending on women's health further drive growth, making innovative treatments more accessible. This supportive ecosystem, built on destigmatization and improved access, is a foundational driver for sustained market growth and women's healthcare innovation.

What are the market trends shaping the Menstrual Drugs Industry?

- A defining market trend is the strategic ascendancy of non-hormonal treatment modalities. This shift addresses growing patient demand for therapies with more favorable side-effect profiles.

- A defining trend is the strategic pivot towards non-hormonal treatment modalities, driven by patient demand for symptom control without the hormonal burden. This shift addresses the needs of individuals with contraindications or preferences against hormonal interventions like oral contraceptives.

- Pharmaceutical R&D is exploring novel targets for visceral pain management, independent of the endocrine system, to treat conditions such as endometriosis-associated pain and refractory menstrual pain. The development of new neurokinin 3 receptor antagonist drugs is a prime example of this innovation.

- This pursuit of personalized medicine in gynecology is supported by advancements in female technology (femtech) integration, where digital platforms improve clinical trial endpoint selection, leading to a 15% faster data validation process. These targeted drug delivery systems promise greater efficacy and tolerability, reshaping the competitive landscape for managing chronic gynecological conditions.

What challenges does the Menstrual Drugs Industry face during its growth?

- Persistent socio-cultural stigma and inadequate menstrual health education remain significant challenges, fundamentally suppressing market potential by hindering diagnosis and treatment-seeking behaviors.

- A primary challenge is the stringent regulatory scrutiny and payer resistance to premium pricing for innovative therapies, which can stifle women's healthcare innovation. The high bar for approval, requiring extensive clinical trials with subjective endpoints like pain reduction, presents a significant investment risk.

- Post-approval, new therapies face intense pharmacoeconomic value assessment, with payers often favoring cheaper, generic nonsteroidal anti-inflammatory drugs (NSAIDs). Gaining favorable reimbursement requires demonstrating substantial clinical advantage, a difficult task that can limit market access. For example, some new treatments achieve formulary inclusion in less than 40% of targeted health plans in their first year.

- This pressure has a chilling effect on R&D for PMDD therapeutic agents and other novel treatments, as companies weigh the risk of low returns on investment, ultimately constraining the options available to patients.

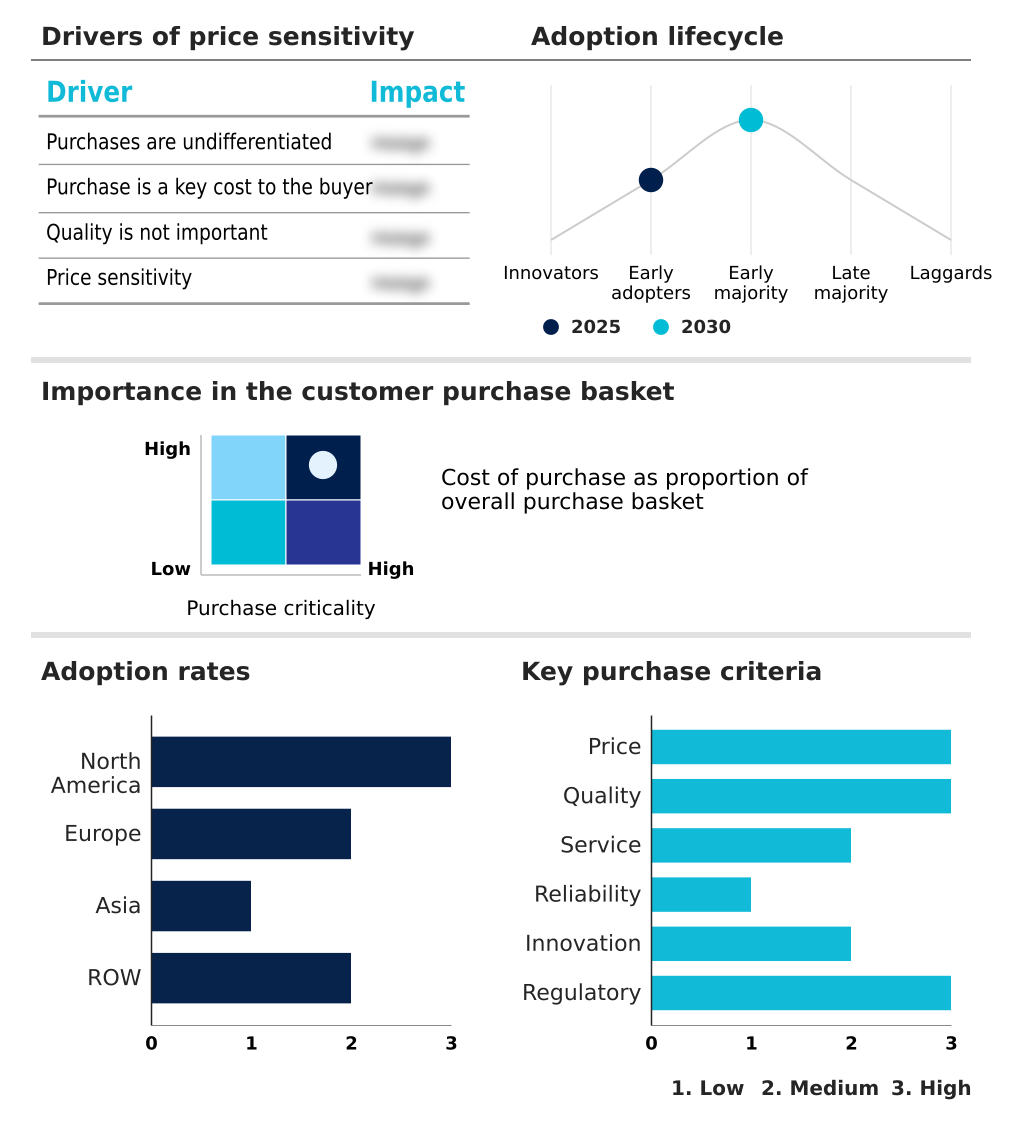

Exclusive Technavio Analysis on Customer Landscape

The menstrual drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the menstrual drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Menstrual Drugs Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, menstrual drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Highlights include an FDA-approved oral medication for heavy menstrual bleeding, underscoring innovation in targeted therapies for specific and underserved gynecological conditions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Adorefem

- Bayer AG

- Cipla Inc.

- Dr Reddys Laboratories Ltd.

- GlaxoSmithKline Plc

- Haleon Plc

- Johnson and Johnson Services

- Leeford Healthcare Ltd.

- Mallinckrodt Plc

- Maxwellia Ltd.

- Perrigo Co. Plc

- Pfizer Inc.

- Reckitt Benckiser Group Plc

- Sanofi SA

- Sumitomo Chemical Co. Ltd.

- Teva Pharmaceutical Ltd.

- The Himalaya Drug Co.

- Walgreens Boots Alliance Inc.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Menstrual drugs market

- In October 2024, Bayer AG announced the FDA granted Fast Track designation for its novel non-hormonal investigational drug for the treatment of pain associated with endometriosis, based on promising Phase II data.

- In January 2025, Pfizer Inc. entered a strategic partnership with a leading digital health platform to integrate its menstrual cycle tracking data into clinical trials for a new PMDD therapy, aiming to improve endpoint accuracy and patient-reported outcomes.

- In March 2025, Organon & Co. launched its new long-acting subcutaneous injectable contraceptive, offering a six-month dosing interval, in several key European markets, expanding options for long-term menstrual cycle management.

- In April 2025, AbbVie Inc. completed its acquisition of a clinical-stage biotechnology firm for approximately $1.2 billion, gaining control of a promising portfolio of first-in-class disease-modifying therapies for endometriosis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Menstrual Drugs Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.4% |

| Market growth 2026-2030 | USD 4597.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, UAE, Brazil, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The menstrual drugs market is advancing beyond symptomatic treatment towards precision-based care, driven by a deeper understanding of underlying pathologies. Key developments center on non-hormonal treatment modalities and disease-modifying therapies, particularly for chronic conditions like endometriosis and uterine fibroids.

- The introduction of oral gonadotropin releasing hormone (GnRH) antagonists, such as elagolix and relugolix combination therapy, marks a significant milestone, offering targeted management of endometriosis-associated pain. Concurrently, there is a strong pipeline for therapies addressing premenstrual dysphoric disorder (PMDD), including selective serotonin reuptake inhibitors (SSRIs) and novel approaches involving allopregnanolone modulation and GABA-A receptor interaction.

- For boardroom consideration, the trend of Rx-to-OTC switch strategies is critical; successfully transitioning a product can expand the addressable market by over 30%, but it requires careful navigation of regulatory pathways.

- The market is also defined by innovation in delivery systems, including transdermal contraceptive patches, intravaginal rings, and long-acting subcutaneous formulations, which aim to improve adherence by avoiding first-pass hepatic metabolism. This push for innovation is balanced by the need to demonstrate value through health technology assessments to secure favorable formulary inclusion and navigate clinical practice guidelines.

What are the Key Data Covered in this Menstrual Drugs Market Research and Growth Report?

-

What is the expected growth of the Menstrual Drugs Market between 2026 and 2030?

-

USD 4.60 billion, at a CAGR of 8.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Hormonal treatments, Pain relief medications, PMS and PMDD medications, Menstrual regulation drugs, and Endometriosis treatments), Route of Administration (Oral medications, Injectables, and Topical applications), Distribution Channel (Retail pharmacies, Hospital pharmacies, and Online pharmacies) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing global awareness and improved diagnosis of menstrual health disorders, Persistent socio-cultural stigma and deficiencies in menstrual health education

-

-

Who are the major players in the Menstrual Drugs Market?

-

AbbVie Inc., Adorefem, Bayer AG, Cipla Inc., Dr Reddys Laboratories Ltd., GlaxoSmithKline Plc, Haleon Plc, Johnson and Johnson Services, Leeford Healthcare Ltd., Mallinckrodt Plc, Maxwellia Ltd., Perrigo Co. Plc, Pfizer Inc., Reckitt Benckiser Group Plc, Sanofi SA, Sumitomo Chemical Co. Ltd., Teva Pharmaceutical Ltd., The Himalaya Drug Co., Walgreens Boots Alliance Inc. and Zydus Lifesciences Ltd.

-

Market Research Insights

- The market's dynamism is driven by a strategic pivot towards addressing unmet needs in women's healthcare innovation. Advances in personalized medicine in gynecology are enabling more effective long-term endometriosis management and treatments for refractory menstrual pain. The integration of female technology (femtech) is improving patient adherence, with some digital platforms demonstrating a 15% increase in compliance rates for chronic therapies.

- This focus on improving patient quality of life is evident as companies explore non-hormonal options for PCOS and other neuroendocrine disorder treatments. The transition of certain prescription drugs to over-the-counter status has broadened access, increasing the user base for some therapies by over 25% in initial launch regions.

- This shift, combined with targeted drug delivery systems, is reshaping the landscape for chronic pain management solutions and specialized gynecological care.

We can help! Our analysts can customize this menstrual drugs market research report to meet your requirements.

RIA -

RIA -