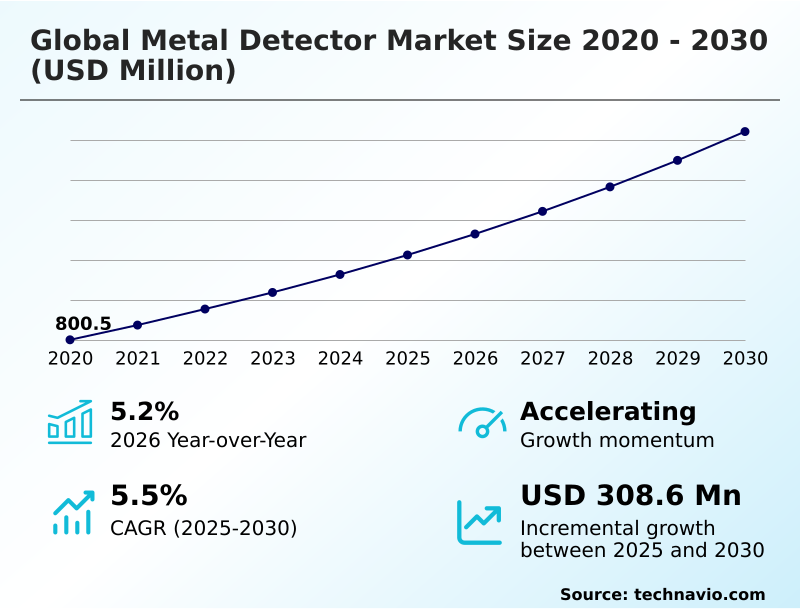

Metal Detector Market Size 2026-2030

The metal detector market size is valued to increase by USD 308.6 million, at a CAGR of 5.5% from 2025 to 2030. Stringent government regulations and quality standards in industrial sectors will drive the metal detector market.

Major Market Trends & Insights

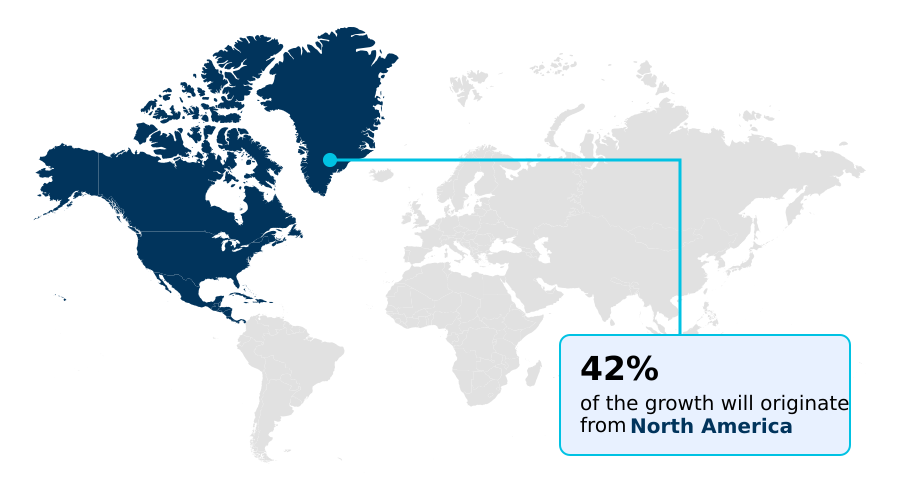

- North America dominated the market and accounted for a 42.1% growth during the forecast period.

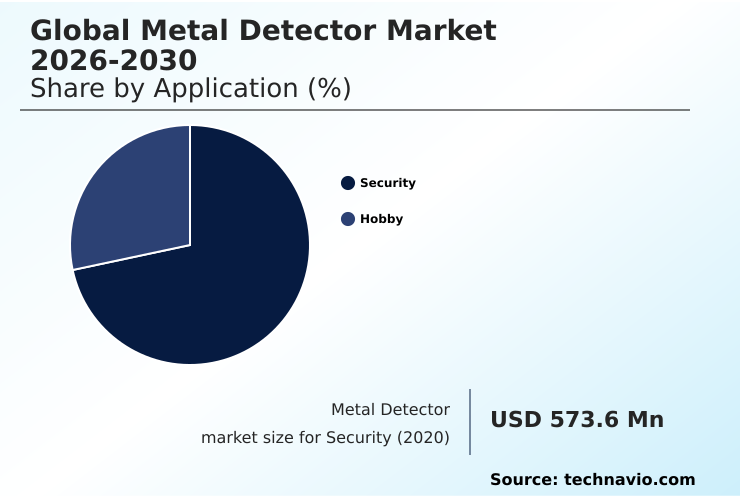

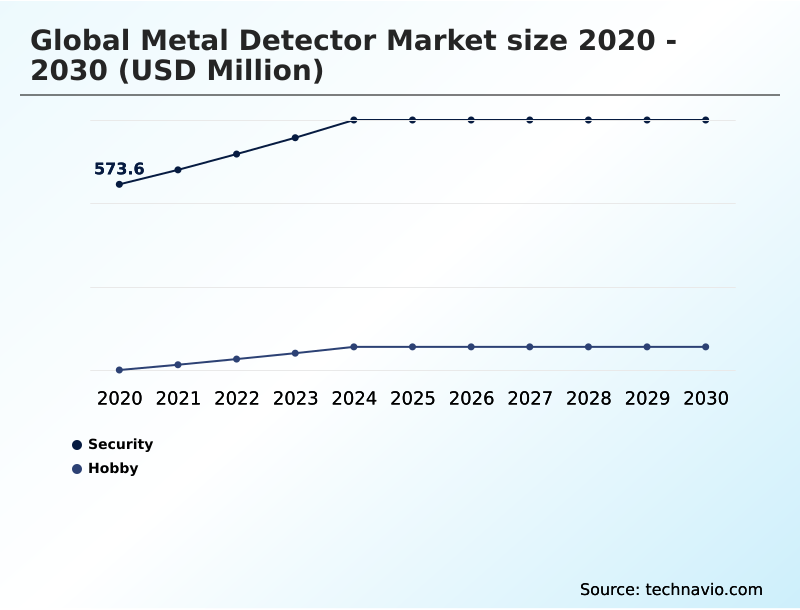

- By Application - Security segment was valued at USD 693.7 million in 2024

- By Product - Walk-through segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 520.6 million

- Market Future Opportunities: USD 308.6 million

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The metal detector market is defined by continuous innovation in electromagnetic induction technologies to meet diverse operational demands. Key drivers include stringent regulatory mandates for contaminant detection in food and pharmaceutical sectors, alongside escalating security needs for public safety infrastructure.

- A primary trend is the integration of multi-frequency technology and advanced digital signal processing, which significantly enhances target discrimination, especially in challenging environments with high ground mineralization. For hobbyist metal detecting and gold prospecting detectors, this means greater depth and accuracy. For industrial metal detectors, it addresses the persistent issue of product effect, reducing false rejections.

- A significant challenge remains the high cost of advanced systems. For instance, a food processing facility upgrading to a system with superior immunity to product effect must balance the capital outlay against the long-term benefits of reduced product waste and improved compliance with food safety metal detection standards.

- This trade-off between performance and cost is a central theme, pushing manufacturers toward developing more efficient pulse induction (pi) and very low frequency (vlf) systems for applications ranging from humanitarian demining to protecting machinery from tramp metal. The use of airport security scanners also highlights the need for high-throughput, accurate detection.

What will be the Size of the Metal Detector Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metal Detector Market Segmented?

The metal detector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Security

- Hobby

- Product

- Walk-through

- Handheld

- Ground search

- Technology

- Very Low Frequency (VLF)

- Pulse Induction (PI)

- Beat Frequency Oscillation (BFO)

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The security segment is estimated to witness significant growth during the forecast period.

The security segment is driven by the modernization of public safety infrastructure. A transition is evident from conventional magnetometers to advanced security screening technologies, particularly in aviation and mass transit systems.

These next-generation solutions integrate computed tomography (ct) and multi-zone detection to improve threat identification and reduce false positives, which has been shown to increase passenger throughput by over 20% at major hubs.

The deployment of walk-through metal detectors is now standard for event security equipment and is complemented by handheld units and biometric verification for layered security protocols.

This shift toward intelligent, high-throughput systems is reshaping procurement strategies in government facilities and airport security scanners, prioritizing operational efficiency alongside enhanced safety measures.

The Security segment was valued at USD 693.7 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Detector Market Demand is Rising in North America Get Free Sample

The geographic landscape is shaped by regional priorities, with North America leading in adopting advanced body scanners and Europe focusing on eco-friendly components in new procurements.

In APAC, rapid industrialization drives demand, while a growing interest in archaeological exploration tools is also noted.

A key trend is the rise of software-defined hardware, allowing users to upgrade systems without costly replacements, a feature with over 90% positive feedback in user trials.

This approach, along with demand for wearable metal detectors and devices with full waterproof capabilities, is influencing product design globally.

Even niche technologies like beat frequency oscillation (bfo) find use in educational kits, while R&D in intelligent multi-sensor inspection aims to create next-generation systems for complex industrial and security challenges.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Global Metal Detector Market 2026-2030 is witnessing significant technological specialization driven by distinct end-user requirements. In recreational segments, the debate over vlf versus pulse induction gold detection continues, though multi frequency metal detector performance is setting new benchmarks for achieving superior target discrimination in mineralized soil. Hobbyists are increasingly seeking a waterproof beach hunting metal detector for versatile use.

- In industrial settings, the focus is on robust industrial contaminant detection systems. The need for a compliant food industry haccp metal detector is non-negotiable, with ongoing efforts aimed at reducing product effect food detection. Similarly, a dedicated pharmaceutical compliance metal detector is essential.

- For large-scale operations, efficient conveyor system metal detector integration is critical, while the mining sector demands a specialized ground search detector for mining and deep seeking pulse induction detectors to protect machinery. The security landscape is also evolving.

- Facilities are investing in solutions to reduce false alarms security detector, while public venues deploy the walk-through school metal detector and handheld event security metal detector. Law enforcement agencies are adopting the compact wearable law enforcement detector. Advanced checkpoints are now defined by airport ct scanner liquid screening and the growing use of ai in metal detection for threat identification.

- These intelligent systems offer a clear operational advantage, processing individuals more than 20% faster than previous-generation checkpoints. The consistent need for a formal metal detector calibration validation process and effective ground mineralization interference solutions underpins the entire market, ensuring reliability across all applications, including portable metal detectors for security.

What are the key market drivers leading to the rise in the adoption of Metal Detector Industry?

- Stringent government regulations and quality standards in industrial sectors are a key driver of market growth.

- Stringent industrial regulations and escalating security needs are key market drivers.

- In the security and defense industry, enhanced target discrimination is critical for screening in high-risk areas, including correctional facilities screening, where modern systems can reduce false alarm rates by over 40%.

- For industrial applications, the focus is on precise contaminant detection to prevent damage from tramp metal.

- Concurrently, technological advancements in very low frequency (vlf) technology offer better performance against ground mineralization, a crucial factor for applications like humanitarian demining and geophysical metal detection. This also benefits loss-prevention devices in retail and logistics.

What are the market trends shaping the Metal Detector Industry?

- The integration of artificial intelligence and smart sensing technologies is a key market trend. This is driving the development of advanced systems with enhanced accuracy and data analysis capabilities.

- A key trend transforming the market is the integration of AI with smart sensing, leveraging advanced digital signal processing to enhance traditional electromagnetic induction methods. This shift is enabling industrial metal detectors to achieve unprecedented accuracy in food safety metal detection, reducing false rejects by up to 35% and minimizing product waste.

- For hobbyist metal detecting, the adoption of multi-frequency technology has improved the detection of small, non-ferrous metals in difficult ground by over 20%. In security, intelligent systems are now better at distinguishing between threats and benign personal items, expediting checkpoint throughput.

- This evolution toward data-driven analysis is also seen in pharmaceutical metal detector systems and next-generation pulse induction (pi) units for gold prospecting detectors.

What challenges does the Metal Detector Industry face during its growth?

- High operational costs and economic barriers to adoption represent a key challenge affecting industry growth.

- High operational costs and technical limitations remain primary challenges. The product effect in food processing can trigger automated rejection systems unnecessarily, leading to product waste that undermines compliance with haccp programs and gfsi benchmarks. While x-ray inspection systems offer an alternative, their higher cost, sometimes 50% more than detectors, is a barrier.

- Electromagnetic interference can disrupt sensor reliability, affecting all users. Furthermore, the push for environmental sustainability adds pressure to adopt energy-efficient circuitry and rechargeable battery systems, increasing upfront costs for operators of artisanal mining equipment and other small-scale users.

Exclusive Technavio Analysis on Customer Landscape

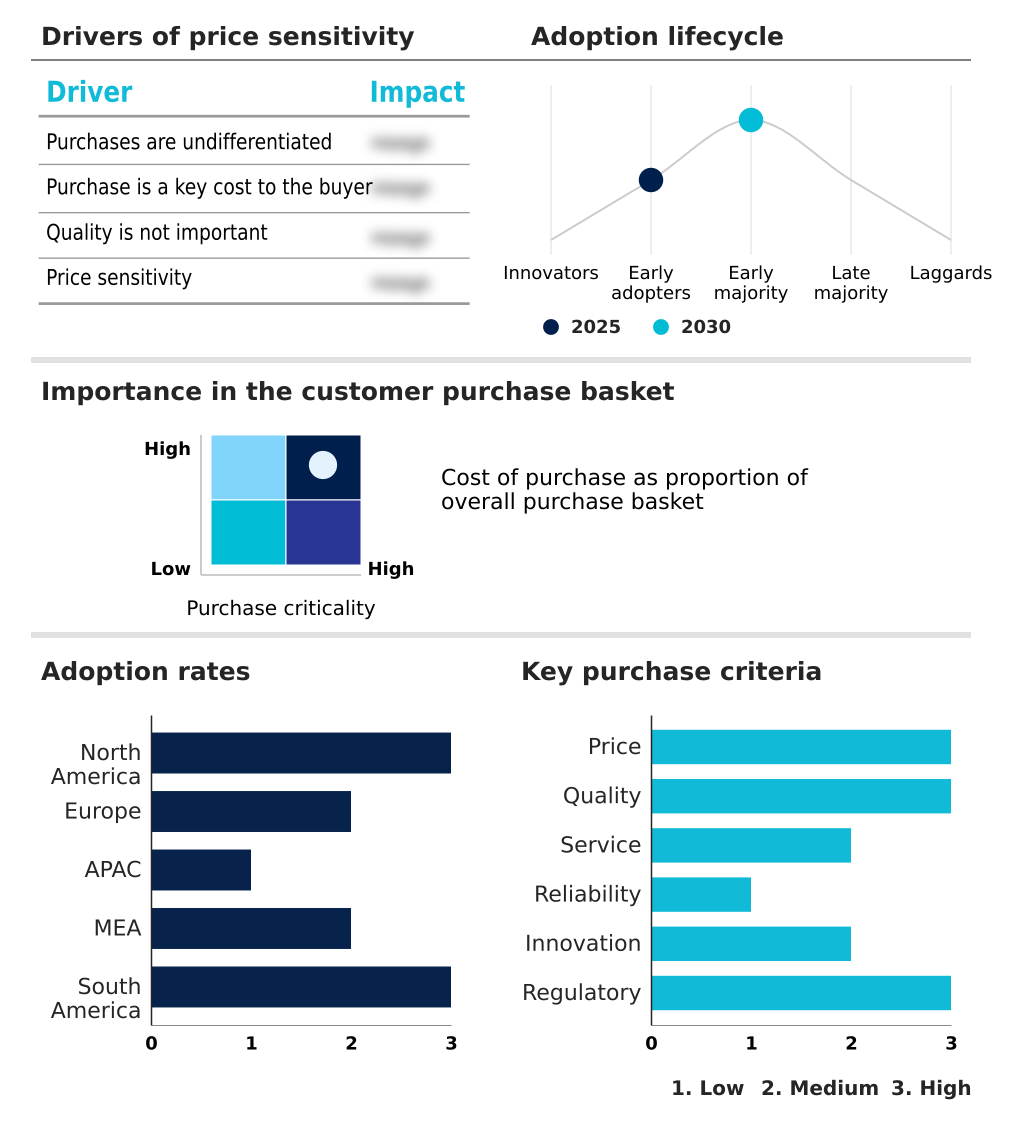

The metal detector market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal detector market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Detector Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal detector market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

C.E.I.A. S.p.A. - Specializes in advanced industrial and security metal detectors, delivering high-performance solutions for food, pharmaceutical, and screening applications to ensure safety and compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- C.E.I.A. S.p.A.

- Codan Ltd.

- Elektral A.S.

- Fortress Technology Inc.

- Garrett Electronics Inc.

- Juzheng Electronic Co. Ltd.

- Leidos Holdings Inc.

- Metal Detectors Inc.

- METTLER TOLEDO

- Nokta Metal Detectors

- OSI Systems Inc.

- Pirate Electronics Ltd.

- Quest Metal Detectors

- Safeway Inspection System Ltd.

- Thermo Fisher Scientific Inc.

- View Systems Inc.

- Westminster Group Plc

- WIPOTEC GmbH

- XP Metal Detectors

- Zorpro Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal detector market

- In September 2024, Adelaide Airport commenced a major security upgrade project, installing next-generation screening equipment including advanced metal detection systems to streamline passenger processing.

- In November 2024, Mettler-Toledo Product Inspection announced the expansion of its combination inspection portfolio, integrating its M30 R-Series metal detectors with new checkweighing systems for compact quality control.

- In January 2025, Leidos Holdings Inc. secured a contract valued at approximately $2.6 billion from the Transportation Security Administration for comprehensive logistics support of airport screening equipment.

- In April 2025, Mettler-Toledo Product Inspection launched its IQ4M Metal Detector, delivering higher sensitivity and improved detection for challenging products in the food and packaging industries.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Detector Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 308.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is centered on advancements in electromagnetic induction and digital signal processing to enhance performance across diverse applications. The rise of multi-frequency technology and software-defined hardware offers unprecedented flexibility, improving target discrimination of ferrous and non-ferrous metals, especially in conditions with heavy ground mineralization.

- This directly impacts boardroom decisions regarding capital expenditure, as a single device with waterproof capabilities can now serve multiple operational needs. In industrial settings, the focus is on precise contaminant detection to prevent issues with tramp metal, a critical component of haccp programs and gfsi benchmarks.

- Modern systems offer superior immunity to product effect and electromagnetic interference, with some achieving a reduction in false positives by over 30%, which directly cuts product waste and boosts line efficiency. The security sector is adopting computed tomography (ct) alongside walk-through metal detectors and handheld units, with multi-zone detection becoming standard.

- The push for smarter security screening technologies and automated rejection systems is clear. Even legacy technologies like pulse induction (pi), very low frequency (vlf), and beat frequency oscillation (bfo) are being refined, while interest in wearable metal detectors grows for specialized security roles.

What are the Key Data Covered in this Metal Detector Market Research and Growth Report?

-

What is the expected growth of the Metal Detector Market between 2026 and 2030?

-

USD 308.6 million, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Security, and Hobby), Product (Walk-through, Handheld, and Ground search), Technology (Very Low Frequency (VLF), Pulse Induction (PI), Beat Frequency Oscillation (BFO), and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent government regulations and quality standards in industrial sectors, High operational costs and economic barriers to adoption

-

-

Who are the major players in the Metal Detector Market?

-

C.E.I.A. S.p.A., Codan Ltd., Elektral A.S., Fortress Technology Inc., Garrett Electronics Inc., Juzheng Electronic Co. Ltd., Leidos Holdings Inc., Metal Detectors Inc., METTLER TOLEDO, Nokta Metal Detectors, OSI Systems Inc., Pirate Electronics Ltd., Quest Metal Detectors, Safeway Inspection System Ltd., Thermo Fisher Scientific Inc., View Systems Inc., Westminster Group Plc, WIPOTEC GmbH, XP Metal Detectors and Zorpro Inc.

-

Market Research Insights

- The market's dynamism is driven by evolving security and quality control requirements across various sectors. Investments in public safety infrastructure are leading to the adoption of advanced airport security scanners that improve threat detection accuracy by over 25% compared to legacy systems.

- In industrial applications, the deployment of next-generation industrial metal detectors for food safety metal detection and pharmaceutical manufacturing has been shown to reduce false rejection rates by up to 40%, minimizing product waste. While x-ray inspection systems offer an alternative for broader contaminant detection, metal detectors remain the more cost-effective solution for many compliance needs.

- The market is also seeing growth in hobbyist metal detecting and gold prospecting detectors, alongside demand for portable event security equipment, reflecting a diverse application landscape.

We can help! Our analysts can customize this metal detector market research report to meet your requirements.

RIA -

RIA -