Law Enforcement Software Market Size 2026-2030

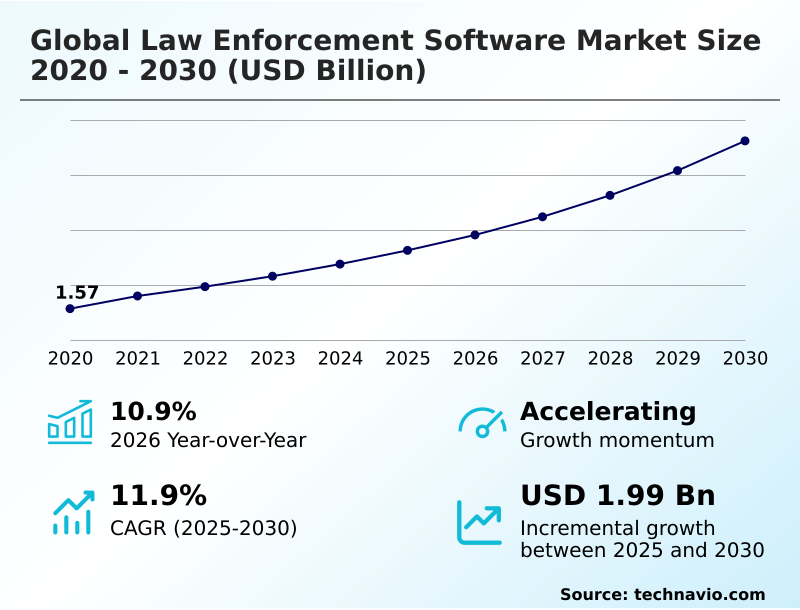

The law enforcement software market size is valued to increase by USD 1.99 billion, at a CAGR of 11.9% from 2025 to 2030. Increasing demand for analytics and data-driven policing will drive the law enforcement software market.

Major Market Trends & Insights

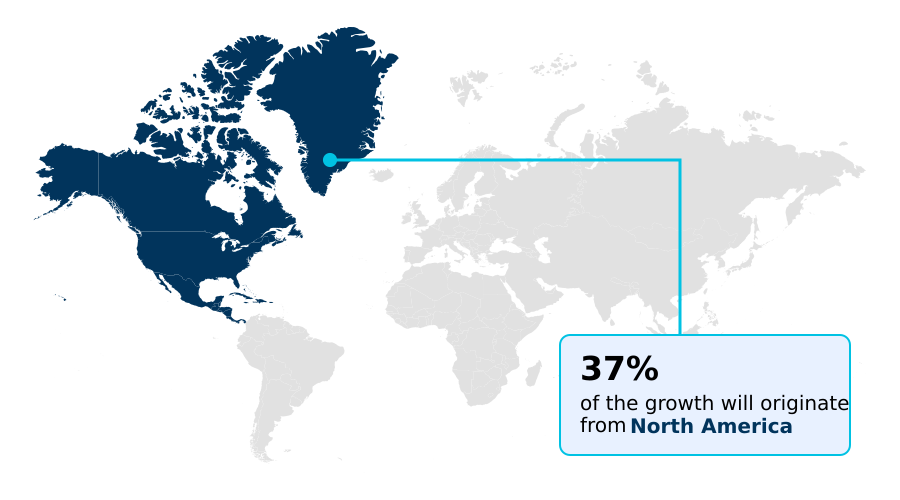

- North America dominated the market and accounted for a 37.2% growth during the forecast period.

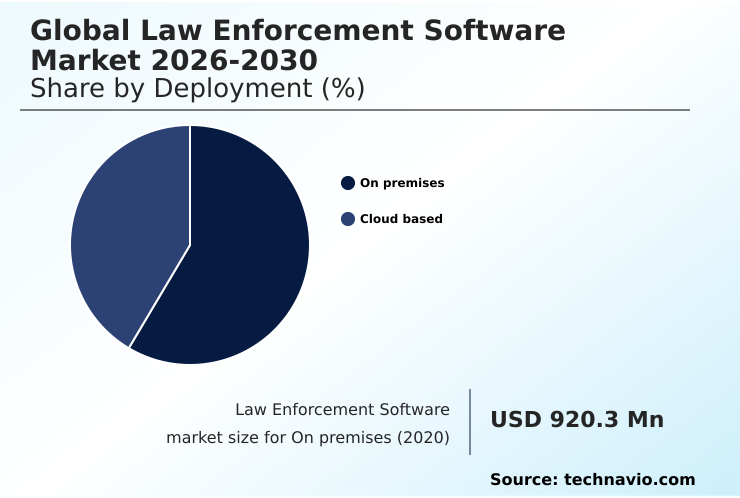

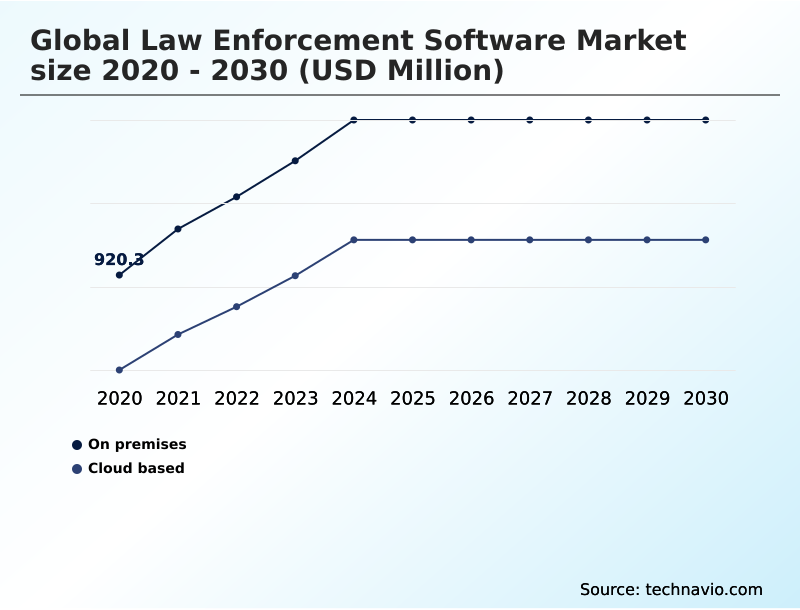

- By Deployment - On premises segment was valued at USD 1.36 billion in 2024

- By Type - Software segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.05 billion

- Market Future Opportunities: USD 1.99 billion

- CAGR from 2025 to 2030 : 11.9%

Market Summary

- The law enforcement software market is undergoing a significant transformation as agencies shift from legacy systems to integrated digital ecosystems. This evolution is driven by the need to improve operational efficiency, enhance officer safety, and foster greater public trust through transparency.

- Key trends include the accelerated migration to cloud-based platforms, which offer superior scalability and accessibility, and the integration of artificial intelligence for advanced analytics. For instance, a metropolitan police department can leverage a unified public safety platform to analyze historical crime data, traffic patterns, and public event schedules.

- This allows for proactive resource allocation, optimizing patrol routes to improve response times by 15% and placing officers where they are most needed. However, this progress is met with challenges, including significant budgetary constraints for modernizing infrastructure and intense public scrutiny over data privacy and the potential for algorithmic bias in predictive policing tools.

- Successfully navigating this landscape requires a balanced approach that embraces technological innovation while upholding stringent ethical standards and regulatory compliance.

What will be the Size of the Law Enforcement Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Law Enforcement Software Market Segmented?

The law enforcement software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On premises

- Cloud based

- Type

- Software

- Services

- End-user

- Police departments

- Municipalities

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The on premises segment is estimated to witness significant growth during the forecast period.

The on-premises segment of the law enforcement software market involves agencies housing their own servers, providing direct control over sensitive information.

This model is critical for organizations governed by strict data sovereignty rules, where maintaining full ownership of hardware and security protocols is paramount.

While the broader digital transformation in policing favors cloud adoption, many agencies continue to invest in on-premises police software. The rationale often involves the deep integration of legacy records management systems and computer-aided dispatch platforms into existing workflows.

Modernizing this infrastructure with new enterprise-level software platforms is complex. Therefore, organizations prioritize system stability and control, ensuring over 99.9% uptime for their integrated public safety solutions rather than pursuing a complete migration to a different deployment model.

The On premises segment was valued at USD 1.36 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Law Enforcement Software Market Demand is Rising in North America Get Free Sample

The geographic landscape for law enforcement software is diverse, with mature markets focusing on sophisticated integrations and emerging regions prioritizing foundational modernization.

North America represents over 37% of the incremental opportunity, with agencies adopting advanced public safety analytics and smart city policing technology.

In contrast, the market in APAC is expanding at the fastest regional pace, approximately 1 percentage point higher than in Europe, driven by large-scale public safety projects.

These initiatives often involve deploying video surveillance analytics and geospatial intelligence for proactive crime prevention. Key investments are being made in digital forensics platform capabilities and threat intelligence platforms to support multi-agency coordination through a national data-sharing initiative.

The adoption of incident reporting software and emergency management software is becoming standard, creating a more connected security ecosystem globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic adoption within the global law enforcement software market 2026-2030 requires careful planning, beginning with decisions on core infrastructure like cloud based cad rms integration. The evaluation of ai predictive policing software accuracy is critical, as is selecting the right digital evidence management for bodycams to ensure evidence integrity.

- Empowering field personnel through a mobile policing app real-time access is a key objective, which often shows a doubling of report filing efficiency compared to station-based processes. Concurrently, improving police community engagement platforms builds public trust. Agencies face significant law enforcement software interoperability challenges and must budget for the high cost of modernizing legacy police systems.

- Navigating data privacy in facial recognition and leveraging geospatial crime mapping analysis tools are key operational considerations. The integrated public safety platform benefits are clear, but achieving them depends on successful records management system data migration and establishing effective cross-jurisdiction data sharing solutions. Agencies must also factor in gunshot detection system implementation costs and acquire advanced cybercrime investigation software features.

- A robust command center software for emergencies is essential for large-scale events. Ultimately, success hinges on managing digital evidence chain of custody, utilizing software for officer accountability reporting, applying analytics for resource allocation optimization, providing real-time intelligence for patrol officers, and reducing administrative tasks with software.

What are the key market drivers leading to the rise in the adoption of Law Enforcement Software Industry?

- An increasing demand for analytics and data-driven policing strategies serves as a key driver for market growth.

- Market growth is driven by the imperative to adopt intelligence-led policing and enhance transparency through technology.

- The demand for robust digital evidence management systems is surging, as these platforms are critical for chain of custody tracking and are considered essential officer accountability tools. Agencies implementing these systems report a 40% reduction in evidence processing time.

- Another major driver is modernizing legacy infrastructure with a unified public safety platform, which provides a unified operational picture and enhances decision-making in command center platforms.

- These integrated public safety solutions facilitate real-time data analysis and empower officers with mobile policing solutions.

- The shift to end-to-end public safety solutions, combining dispatch, records, and case management systems, streamlines workflows and improves inter-agency collaboration, which is a key goal for most departments.

What are the market trends shaping the Law Enforcement Software Industry?

- The proliferation of artificial intelligence and predictive analytics is emerging as a significant market trend, reshaping traditional policing models toward more proactive, data-informed strategies.

- Key market trends are centered on the integration of artificial intelligence and the migration to cloud-based law enforcement solutions. The adoption of data-driven policing strategies for proactive crime prevention is powered by predictive policing algorithms and AI-powered video analytics, which have improved crime forecast accuracy by over 25% in some urban areas.

- AI-enhanced records management systems use natural language processing to analyze reports, accelerating intelligence extraction. The use of criminal intelligence software for automated data analysis and tools like facial recognition systems is growing, though it is accompanied by ethical debates. This technological shift enables real-time situational awareness and more efficient operations.

- Furthermore, the standardization of biometric data exchange protocols is improving how agencies collaborate on complex investigations, reducing suspect identification time significantly.

What challenges does the Law Enforcement Software Industry face during its growth?

- Heightened scrutiny over data privacy and the potential for algorithmic bias presents a key challenge affecting industry growth.

- Significant challenges constrain market growth, led by heightened scrutiny over data privacy and algorithmic bias in investigative analytics. The complexity of cross-border data sharing and the lack of standardized interoperability protocols for public safety software create technical hurdles, with integration projects often exceeding budgets by over 15%.

- While there is a push for transparency through public-facing dashboards and community engagement platforms, agencies face budgetary constraints when attempting to modernize. The high cost of deploying specialized tools like a gunshot detection system or advanced traffic management software can be prohibitive.

- Furthermore, achieving end-to-end digital justice and security is complicated by the need to ensure data from various systems is compatible with judicial tools such as e-discovery platforms and courtroom presentation software, a critical but often overlooked expense.

Exclusive Technavio Analysis on Customer Landscape

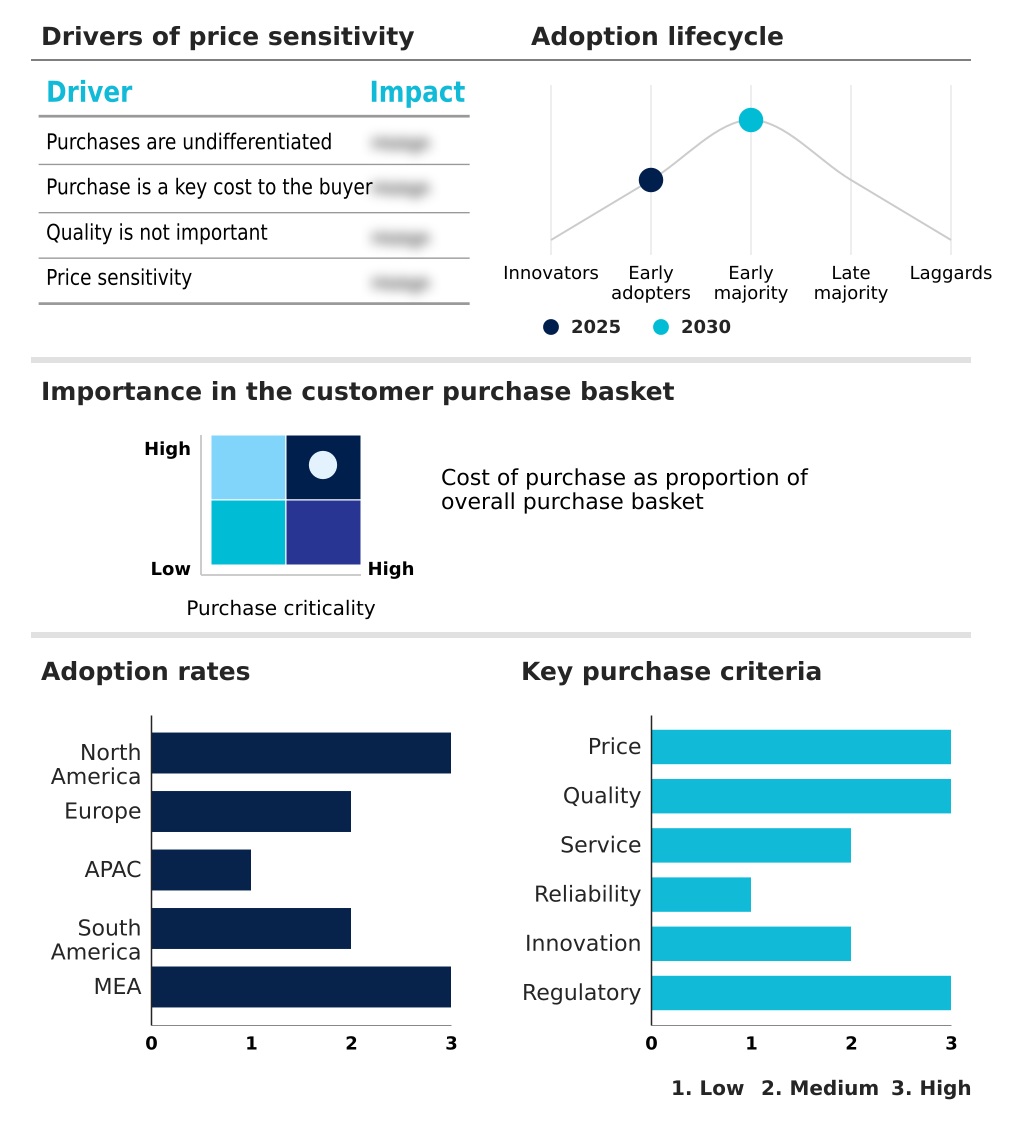

The law enforcement software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the law enforcement software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Law Enforcement Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, law enforcement software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - Harnessing data science, cloud computing, and AI, its integrated public safety platforms are designed to foster safer communities through advanced, connected software solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Axon Enterprise Inc.

- Capterra Inc.

- CentralSquare

- CODY Computer Serv Inc.

- Esri Global Inc.

- Genetec Inc.

- Guardian Alliance Tech Inc.

- Hexagon AB

- LexisNexis Risk Solutions.

- Matrix Pointe Software

- Motorola Solutions Inc.

- NiCE Ltd.

- Omnigo Software

- Palantir Technologies Inc.

- Tyler Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Law enforcement software market

- In January 2025, The Dallas Police Department initiated an upgrade to a hybrid cloud case management platform from IBM to enhance data accessibility and predictive policing capabilities.

- In February 2025, The European Commission issued new implementing regulations for the Prum II framework, which mandates standardized technical protocols for the automated exchange of biometric data among member states.

- In March 2025, Motorola Solutions deployed an AI-enhanced records management system for the New York Police Department, designed to accelerate crime analysis and improve interdepartmental coordination.

- In May 2025, a consortium of mid-sized municipal police departments awarded a multi-year managed services contract to a technology provider for the end-to-end management of their shared cloud-based digital evidence system.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Law Enforcement Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.9% |

| Market growth 2026-2030 | USD 1991.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The law enforcement software market is defined by a suite of interconnected technologies. Core operations rely on computer-aided dispatch and records management systems, while investigations are enhanced by case management systems, investigative analytics, digital forensics platform tools, and e-discovery platforms.

- A boardroom-level focus on cloud migration is driven by the need to integrate these with modern digital evidence management solutions, essential for chain of custody tracking and managing data from bodycams and video surveillance analytics.

- The adoption of AI-enhanced records management and predictive policing algorithms utilizing natural language processing and automated data analysis can improve case clearance rates by up to 10%. Public safety is further augmented by specialized tools like gunshot detection system tech, gunshot detection and analysis, facial recognition systems, cryptocurrency transaction analysis, and dark web monitoring software.

- A unified public safety platform integrates these with incident reporting software, geospatial intelligence, and crime mapping to provide a complete operational picture.

- This is crucial for command center platforms, emergency management software, traffic management software, and global security operations center operations, which depend on mobile policing solutions, interoperability protocols, real-time data analysis, a digital docket system, guard tour management, courtroom presentation software and threat intelligence platforms to function effectively.

What are the Key Data Covered in this Law Enforcement Software Market Research and Growth Report?

-

What is the expected growth of the Law Enforcement Software Market between 2026 and 2030?

-

USD 1.99 billion, at a CAGR of 11.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On premises, and Cloud based), Type (Software, and Services), End-user (Police departments, Municipalities, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for analytics and data-driven policing, Heightened scrutiny over data privacy and algorithmic bias

-

-

Who are the major players in the Law Enforcement Software Market?

-

Accenture PLC, Axon Enterprise Inc., Capterra Inc., CentralSquare, CODY Computer Serv Inc., Esri Global Inc., Genetec Inc., Guardian Alliance Tech Inc., Hexagon AB, LexisNexis Risk Solutions., Matrix Pointe Software, Motorola Solutions Inc., NiCE Ltd., Omnigo Software, Palantir Technologies Inc. and Tyler Technologies Inc.

-

Market Research Insights

- Market dynamics are shaped by the dual pressures of technological advancement and regulatory oversight. Agencies are adopting data-driven policing strategies to improve outcomes, with integrated public safety solutions demonstrating a 20% improvement in cross-agency case collaboration. The shift toward cloud-based law enforcement solutions is driven by cost-efficiency, reducing infrastructure overhead by up to 30% compared to on-premise systems.

- As part of a broader digital transformation in policing, community engagement platforms are being deployed to enhance transparency. However, the implementation of these technologies is moderated by the complexities of modernizing legacy infrastructure and ensuring compliance with evolving data privacy laws.

We can help! Our analysts can customize this law enforcement software market research report to meet your requirements.

RIA -

RIA -