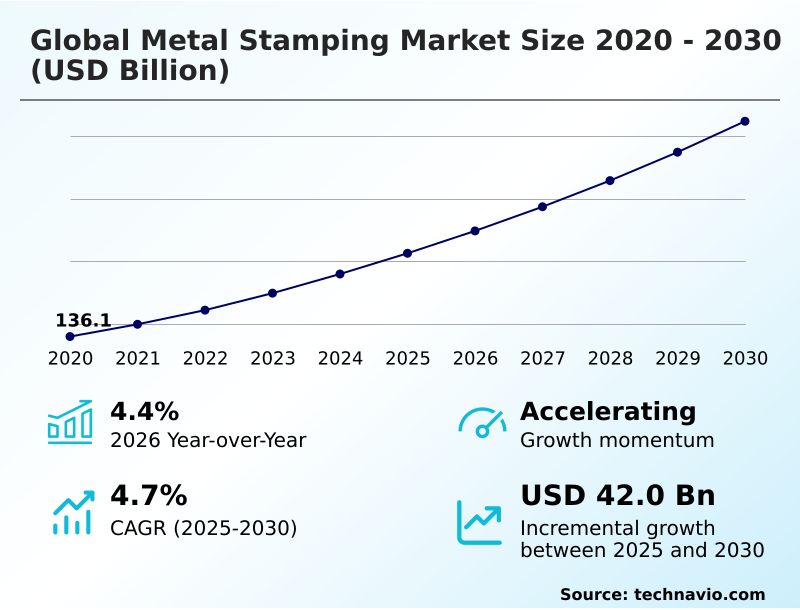

Metal Stamping Market Size 2026-2030

The metal stamping market size is valued to increase by USD 42.00 billion, at a CAGR of 4.7% from 2025 to 2030. Accelerated transition to EV manufacturing will drive the metal stamping market.

Major Market Trends & Insights

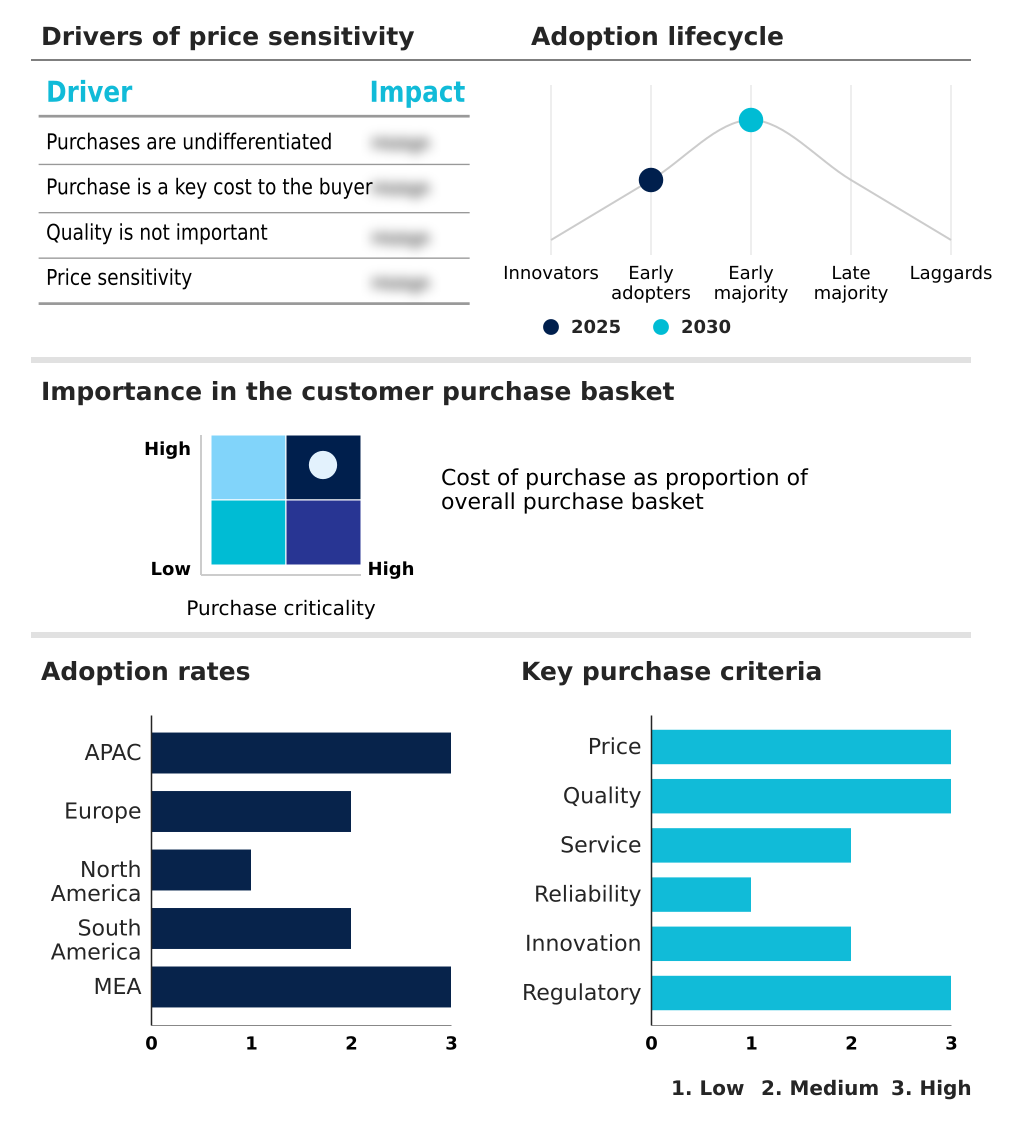

- APAC dominated the market and accounted for a 47.4% growth during the forecast period.

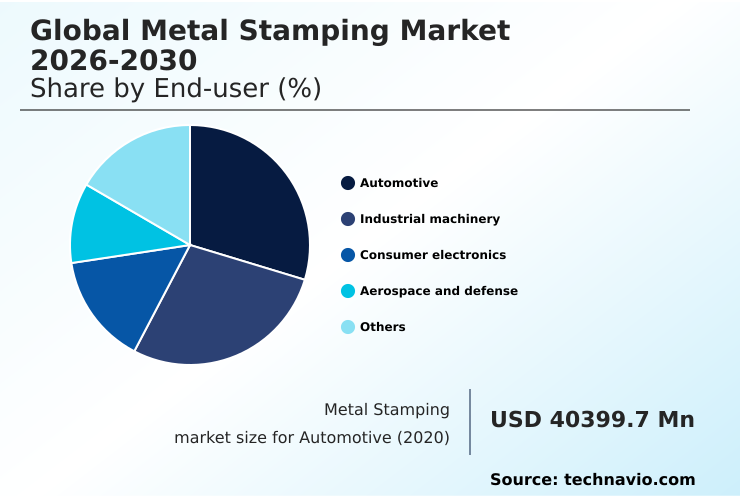

- By End-user - Automotive segment was valued at USD 46.79 billion in 2024

- By Material - Steel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 68.50 billion

- Market Future Opportunities: USD 42.00 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The metal stamping market is undergoing a significant transformation, driven by the dual pressures of technological innovation and evolving end-user demands. At its core, the industry provides essential components for sectors ranging from automotive to consumer electronics, utilizing processes that convert flat metal sheets into complex parts.

- Key drivers include the global transition to electric vehicles, which requires specialized components like battery enclosures and lightweight structural frames, and the continuous miniaturization in electronics, demanding high-precision parts with micron-level tolerances. A major trend reshaping the landscape is the adoption of Industry 4.0 technologies.

- For instance, a manufacturer might implement a digital twin for a new press line, allowing engineers to simulate die performance and material flow to optimize production and reduce physical trial-and-error waste by over 30% before a single component is stamped. This enhances efficiency and shortens lead times for new product introductions.

- However, the industry faces challenges, including volatile raw material prices for steel and aluminum and a widening skills gap, as experienced tool and die makers retire without a sufficient pipeline of new talent. This dynamic environment necessitates continuous investment in both technology and workforce training to maintain a competitive edge.

What will be the Size of the Metal Stamping Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metal Stamping Market Segmented?

The metal stamping industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

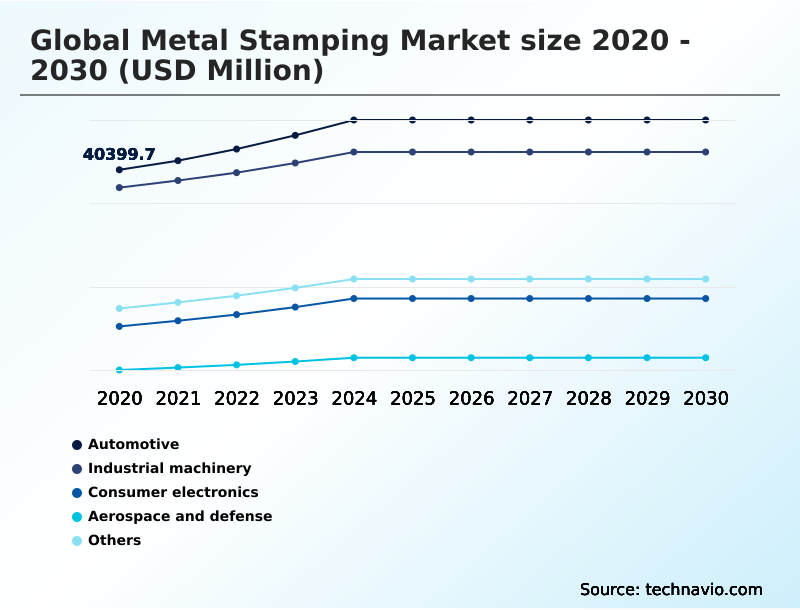

- End-user

- Automotive

- Industrial machinery

- Consumer electronics

- Aerospace and defense

- Others

- Material

- Steel

- Aluminum

- Copper

- Others

- Type

- Progressive die stamping

- Transfer die stamping

- Deep draw stamping

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- Italy

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive sector remains the primary end-user, with a pronounced shift toward electric mobility reshaping component demand.

The imperative for component lightweighting strategies to extend vehicle range drives the adoption of advanced materials, necessitating specialized high-strength steel forming and aluminum processing.

This transition demands significant investment in technologies like the hot stamping process and advanced tool and die design to produce complex electric vehicle battery enclosures and automotive body-in-white structures.

Effective die maintenance programs have become critical for managing the complex tooling, with some operators achieving a 15% reduction in unplanned downtime.

Processes such as progressive die stamping for connectors and transfer die stamping for large panels are essential for high-volume production runs supporting just-in-time delivery systems, ensuring robust structural integrity analysis standards are met.

This evolution underscores the need for continuous precision tooling manufacturing innovation.

The Automotive segment was valued at USD 46.79 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Stamping Market Demand is Rising in APAC Get Free Sample

The geographic landscape is undergoing a strategic realignment. While APAC remains the epicenter for high-volume production runs, particularly for EMI shielding components using micro stamping processes, North America and Europe are experiencing a resurgence driven by reshoring initiatives.

In these regions, the focus is on specialized applications like industrial machinery housing and tight tolerance manufacturing, where investments in energy-efficient stamping can yield operational savings of up to 12%.

Advanced techniques such as fine blanking technology and multi-slide stamping are gaining traction for complex parts. Firms are adopting robotic welding integration post-stamping, which has been shown to improve throughput by 20%.

The adoption of circular economy principles is also influencing facility design. Meanwhile, short-run stamping process specialists cater to niche markets, focusing on superior surface finish control after sheet metal blanking.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global metal stamping market's evolution is clearly visible in its specialized applications, where process optimization and material science converge. The use of progressive die stamping for electrical connectors and micro stamping for electronic lead frames is fundamental to the miniaturization of consumer electronics.

- Similarly, precision stamping for EMI shielding cans and high-speed stamping of consumer electronics frames address the dual needs of performance and aesthetics in high-tech devices. In the automotive sector, the transition to electric mobility is driving demand for metal stamping for EV battery enclosures and deep draw stamping for battery casings.

- Safety and lightweighting are addressed through hot stamping of advanced high-strength steel for structural reinforcements and aluminum stamping for lightweight body panels and aluminum stamping for heat exchanger fins. Large structural components are efficiently produced via transfer die stamping of automotive cross members, while high-strength steel stamping for chassis parts ensures durability.

- The efficiency of these operations is enhanced by servo press technology for improved formability and verified by automated quality control in stamping lines. Specialized sectors rely on precision metal stamping for medical devices and custom metal stamping for aerospace parts.

- The use of tool and die design for complex geometries enables the creation of parts for sheet metal forming for industrial enclosures. Industrial practices are also advancing with fine blanking for tight tolerance components and multi-slide stamping for complex small parts, while sheet metal fabrication for custom prototypes accelerates development cycles.

- Firms that successfully integrate these advanced processes often report a parts-per-million defect rate that is more than 50% lower than those using conventional methods, a critical metric for supply chain planning in high-reliability sectors.

What are the key market drivers leading to the rise in the adoption of Metal Stamping Industry?

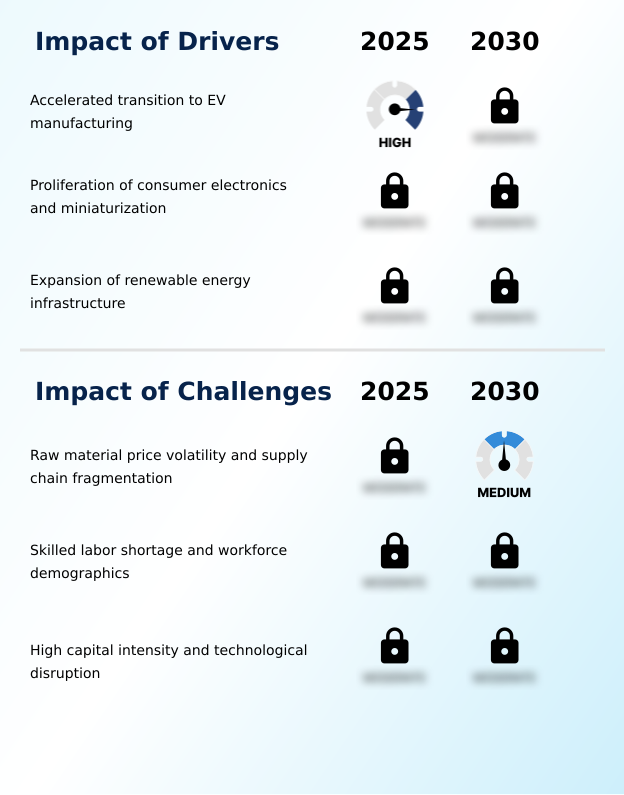

- A primary driver for the market is the accelerated global transition toward electric vehicle manufacturing, which creates substantial demand for new, specialized stamped metal components.

- The transition to electric vehicles and the proliferation of compact electronics are major market drivers.

- Demand for lightweight material stamping is surging, with aluminum alloy stamping used extensively to reduce vehicle weight and improve battery range, with some new vehicle platforms achieving a 15% mass reduction through its use.

- Concurrently, the consumer electronics sector requires high-volume precision metal stamping for items like consumer electronics chassis and thermal management solutions. Techniques such as deep draw stamping and cold forming technology are essential for complex geometry fabrication.

- A strategic push for supply chain localization is leading to new investments in regional coil-fed stamping operations. This focus on regional production improves logistics efficiency by up to 20%.

- The aerospace sector also contributes, requiring advanced sheet metal forming for aerospace structural components using sustainable material sourcing.

What are the market trends shaping the Metal Stamping Industry?

- The accelerated adoption of Industry 4.0 and smart manufacturing principles is a significant trend, reshaping production economics and quality control standards across the industry.

- The accelerated industry 4.0 integration is reshaping manufacturing, with automated stamping lines and robotic transfer systems becoming standard. Advanced metal forming simulation and digital twin simulation enable engineers to optimize processes before production, reducing trial-and-error waste by up to 25%. The use of in-die sensor technology allows for real-time monitoring, which supports predictive maintenance scheduling and improves production line efficiency.

- Furthermore, the deployment of servo press technology provides greater control over the forming process, which is critical for zero-defect quality control. AI-powered automated quality inspection systems can detect microscopic flaws, increasing defect detection rates by over 40% compared to manual methods. These innovations drive cost-per-part optimization and support effective scrap reduction methods.

What challenges does the Metal Stamping Industry face during its growth?

- Significant challenges affecting industry growth include persistent raw material price volatility and increasing supply chain fragmentation, which impact operational costs and planning.

- Key market challenges include raw material price volatility and a persistent skilled labor gap, which can increase operational costs by 10-15% annually. The industry's shift toward processing advanced high-strength steel and ultra-high-strength steel requires substantial capital investment in high-tonnage press operations and specialized techniques like the press hardening process.

- Proper material formability analysis and advanced stamping lubrication technology are now critical for achieving micron-level precision without defects. This technological shift intensifies the need for workforce skill development programs. Small and medium-sized enterprises, particularly those in custom metal fabrication, struggle to finance these upgrades, impacting their ability to compete on projects requiring short lead times, such as medical device implants.

- These firms find that inadequate access to rapid prototyping methods can extend project timelines by over 30%, hindering their ability to improve material utilization rate and achieve reduced tooling lead times.

Exclusive Technavio Analysis on Customer Landscape

The metal stamping market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal stamping market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Stamping Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal stamping market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAPICO Hitech Public Co. Ltd. - Offerings include precision-stamped automotive body components, structural assemblies, and other formed metal parts tailored for vehicle manufacturing and assembly operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAPICO Hitech Public Co. Ltd.

- American Axle Manufacturing

- American Industrial Co.

- Caparo Group

- CIE Automotive SA

- Clow Stamping Co.

- D and H Industries Inc.

- Gestamp Automocion SA

- Goshen Stamping Co.

- Harvey Vogel Manufacturing Co.

- Kenmode Inc.

- Klesk Metal Stamping Co.

- KOBAKIN J Co. Ltd.

- Magna International Inc.

- Manor Tool and Manufacturing

- Metrican Stamping Co.

- Nelson Miller

- Tempco Manufacturing Co. Inc.

- thyssenkrupp AG

- Wiegel Tool Works Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal stamping market

- In October, 2024, Tata Advanced Systems commenced full-scale assembly operations at its final assembly line for the C295 military transport aircraft, driving demand for locally stamped aerostructure components.

- In February, 2025, Toyota Battery Manufacturing North Carolina officially began commercial shipments of lithium-ion batteries, utilizing large-scale metal stamping to fabricate metallic cases and module frames.

- In April, 2025, Gestamp implemented a comprehensive digital twin and smart sensor pilot program across its production lines to capture real-time data and enhance precision in automotive components.

- In May, 2025, The Boeing Co. reported operational delays linked to a shortage of specialized machinists and metal forming professionals, highlighting a critical labor challenge affecting the aerospace supply chain.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Stamping Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 42003.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, Germany, France, Italy, UK, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The metal stamping market is advancing beyond traditional manufacturing through the integration of sophisticated technologies. Core processes like progressive die stamping, transfer die stamping, and deep draw stamping are being refined with innovations such as servo press technology and automated stamping lines.

- A critical trend influencing boardroom strategy is the adoption of metal forming simulation, which allows for material formability analysis before capital-intensive tool and die design begins, significantly de-risking new product launches.

- The industry’s ability to work with advanced high-strength steel and ultra-high-strength steel using methods like the hot stamping process and press hardening process is pivotal for the automotive sector's lightweighting goals. Companies are leveraging in-die sensor technology and robotic transfer systems to achieve zero-defect quality control, with some achieving a 99.9% success rate on critical components.

- This evolution requires robust die maintenance programs and advanced stamping lubrication technology.

- The market also includes specialized techniques such as fine blanking technology, multi-slide stamping, cold forming technology, micro stamping processes, and short-run stamping process for niche applications, supported by precision tooling manufacturing, robotic welding integration, scrap reduction methods, superior surface finish control, sheet metal blanking, and high-tonnage press operations for custom metal fabrication and lightweight material stamping through coil-fed stamping operations.

What are the Key Data Covered in this Metal Stamping Market Research and Growth Report?

-

What is the expected growth of the Metal Stamping Market between 2026 and 2030?

-

USD 42.00 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Automotive, Industrial machinery, Consumer electronics, Aerospace and defense, and Others), Material (Steel, Aluminum, Copper, and Others), Type (Progressive die stamping, Transfer die stamping, and Deep draw stamping) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated transition to EV manufacturing, Raw material price volatility and supply chain fragmentation

-

-

Who are the major players in the Metal Stamping Market?

-

AAPICO Hitech Public Co. Ltd., American Axle Manufacturing, American Industrial Co., Caparo Group, CIE Automotive SA, Clow Stamping Co., D and H Industries Inc., Gestamp Automocion SA, Goshen Stamping Co., Harvey Vogel Manufacturing Co., Kenmode Inc., Klesk Metal Stamping Co., KOBAKIN J Co. Ltd., Magna International Inc., Manor Tool and Manufacturing, Metrican Stamping Co., Nelson Miller, Tempco Manufacturing Co. Inc., thyssenkrupp AG and Wiegel Tool Works Inc.

-

Market Research Insights

- The metal stamping market is characterized by dynamic shifts driven by technological adoption and supply chain realignment. The integration of industry 4.0 integration and digital twin simulation is improving production line efficiency, with some operators reporting a 15% increase in output from existing press lines.

- A strategic emphasis on supply chain localization is shortening just-in-time delivery systems, reducing logistics-related costs by up to 20% in certain automotive corridors. This is particularly crucial for manufacturing electric vehicle battery enclosures and automotive body-in-white components.

- Furthermore, the push for sustainable material sourcing and circular economy principles is influencing procurement, improving material utilization rate and creating new value from recycled metals. These dynamics are compelling firms to invest in workforce skill development to manage more sophisticated automated systems.

We can help! Our analysts can customize this metal stamping market research report to meet your requirements.

RIA -

RIA -