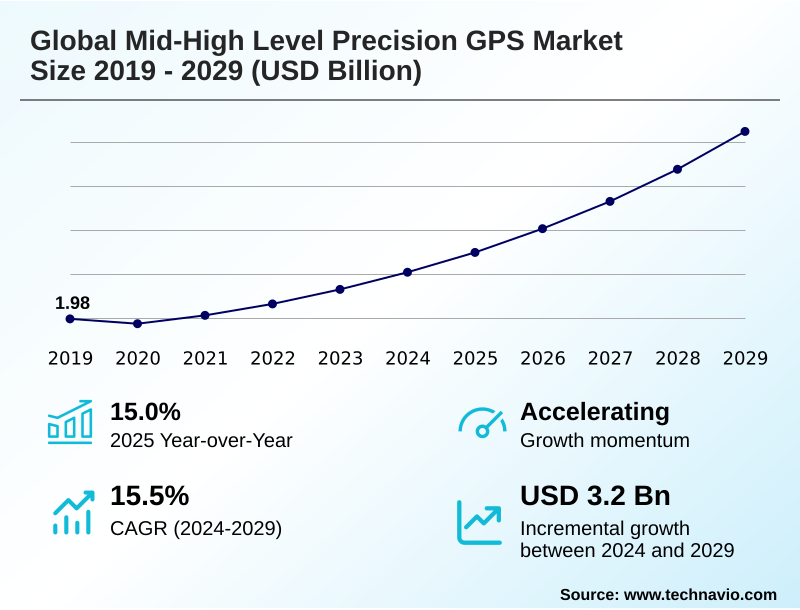

Mid-high Level Precision GPS Market Size 2025-2029

The mid-high level precision gps market size is valued to increase by USD 3.20 billion, at a CAGR of 15.5% from 2024 to 2029. Proliferation of automation and autonomous systems across key industries will drive the mid-high level precision gps market.

Major Market Trends & Insights

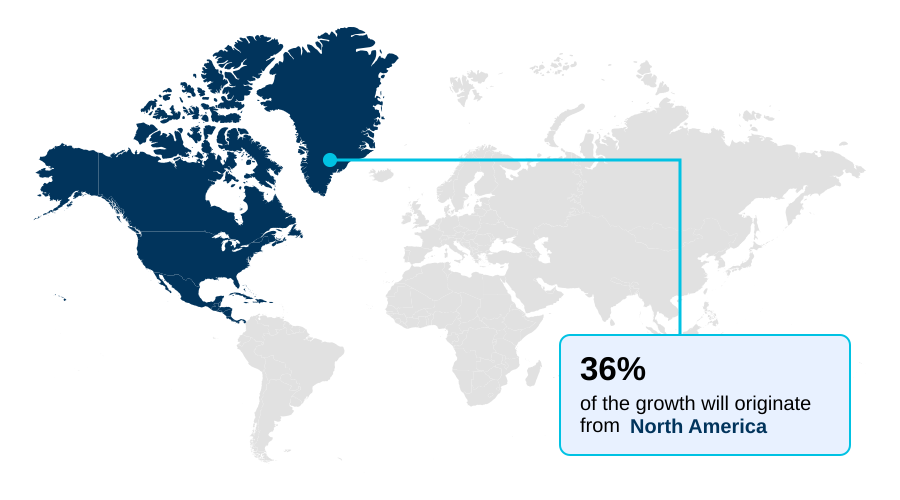

- North America dominated the market and accounted for a 36.3% growth during the forecast period.

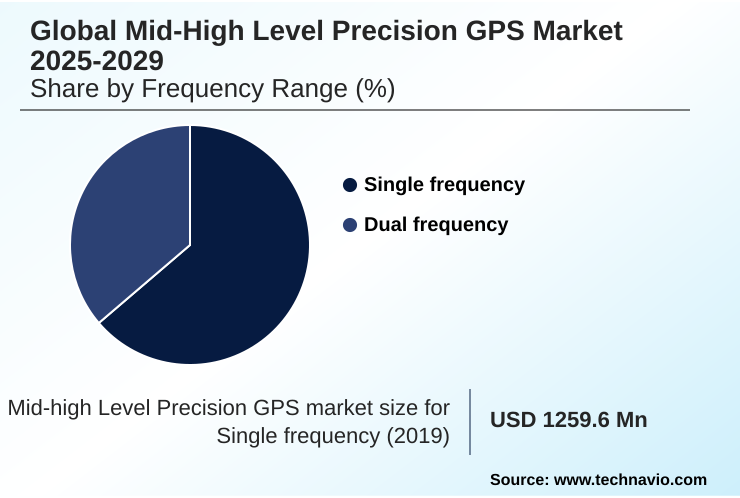

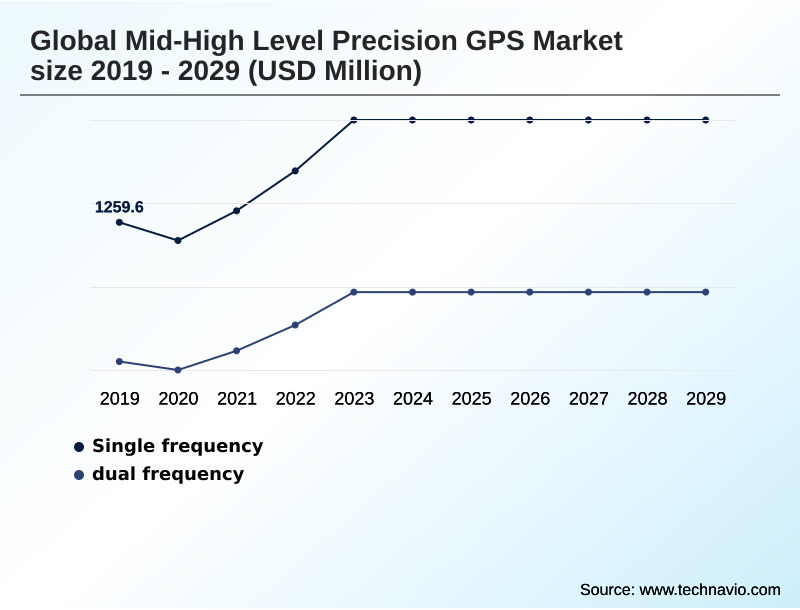

- By Frequency Range - Single frequency segment was valued at USD 1.66 billion in 2023

- By Type - Differential grade segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.26 billion

- Market Future Opportunities: USD 3.20 billion

- CAGR from 2024 to 2029 : 15.5%

Market Summary

- The mid-high level precision GPS market is defined by hardware, software, and services engineered for sub-meter to centimeter-level accuracy. This is achieved using advanced multi-constellation GNSS and multi-frequency receivers that process signals from multiple satellite systems.

- The core of this market is the use of augmentation techniques like Real Time Kinematic (RTK) and Precise Point Positioning (PPP), which correct for atmospheric and other signal errors. This technology is critical for professional sectors where precise location is non-negotiable.

- For instance, in a large-scale construction project, machine control systems on earthmoving equipment use this precision to grade sites according to digital plans, ensuring accuracy and reducing rework. The expansion of automation, the push for industrial digitalization through digital twins, and the constant modernization of satellite infrastructure are key drivers.

- However, challenges such as signal vulnerability in obstructed environments and the high total cost of ownership persist, shaping the competitive landscape for applications in surveying, agriculture, and autonomous mobility.

What will be the Size of the Mid-high Level Precision GPS Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Mid-high Level Precision GPS Market Segmented?

The mid-high level precision gps industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Frequency range

- Single frequency

- Dual frequency

- Type

- Differential grade

- Survey grade

- End-user

- Agriculture

- Construction

- Oil and gas

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Frequency Range Insights

The single frequency segment is estimated to witness significant growth during the forecast period.

The mid-high level precision GPS market is segmented by offerings, including a foundational category that leverages single-frequency bands.

These solutions are defined by lower cost and power consumption, but their reliance on a single band makes them susceptible to ionospheric scintillation, a significant source of positional error. Performance can be compromised in environments prone to multipath interference.

Despite these limitations, advancements in processing and the use of a satellite based augmentation system (sbas) are improving performance. For applications in autonomous systems navigation, where meter-level precision is adequate, these systems provide a cost-effective solution.

The ongoing focus on optimizing system on chip (soc) design and providing georeferenced data for less demanding fleet management optimization ensures this segment's continued relevance, reducing data acquisition errors by up to 30% compared to uncorrected devices.

The Single frequency segment was valued at USD 1.66 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Mid-high Level Precision GPS Market Demand is Rising in North America Get Free Sample

The geographic landscape of the mid-high level precision GPS market is diverse, with regional dynamics shaped by distinct industrial priorities.

North America leads in developing autonomous systems, while Europe's market is driven by its advanced automotive sector and the Galileo satellite system, which offers a high-accuracy service enabling 20-centimeter precision.

APAC is the fastest-growing region, fueled by China's massive infrastructure projects and the BeiDou Navigation Satellite System (BDS). The adoption of reality capture technology is pivotal for these large-scale developments.

In South America, demand is concentrated in large-scale agriculture and mining, where precision is essential for operational efficiency. The use of differential grade systems in these sectors boosts productivity by over 25%.

Even in emerging markets in the Middle East and Africa, giga-projects are creating unprecedented demand for survey grade equipment and associated services like remote asset inspection.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the mid-high level precision GPS market are increasingly influenced by detailed performance evaluations, such as the RTK vs PPP accuracy comparison, which dictates investment choices for specific applications.

- The trend toward GNSS IMU integration for robotics is critical for ensuring operational continuity in signal-denied environments like warehouses, where navigation errors can be reduced by over 60% compared to systems without it. This addresses a major challenge of GNSS in urban canyons and other obstructed areas.

- The benefits of multi-band GNSS in agriculture are now well-documented, directly impacting yield through precise machinery guidance. Similarly, the growing adoption of high precision GPS for drone surveying is transforming land management and construction workflows by enabling rapid, accurate data collection.

- This is central to using GNSS for infrastructure digital twins, where the fidelity of the virtual model depends on the accuracy of the initial geospatial data. As a result, the cost of ownership for survey grade GPS is being weighed against the significant efficiency gains and risk mitigation it provides.

- The evolution of sensor fusion in autonomous vehicle navigation continues to be a primary area of R&D, as it is fundamental to achieving the required safety and reliability for mass-market deployment.

What are the key market drivers leading to the rise in the adoption of Mid-high Level Precision GPS Industry?

- The proliferation of automation and autonomous systems across key industries is a primary driver for market growth.

- Market growth is fundamentally driven by the pervasive trend of industrial digitalization and automation. The demand for high-fidelity geospatial data is surging as industries from agriculture to construction adopt data-driven optimization strategies.

- For example, the use of precision agriculture applications powered by high-accuracy GNSS has increased crop yields by up to 15% while reducing input costs.

- Furthermore, the continuous modernization of satellite infrastructure, including the deployment of new constellations and L-band correction signals, enhances signal availability and integrity.

- This improved infrastructure underpins the expansion of autonomous systems navigation, where reliable centimeter-level accuracy is a prerequisite for safe operation. This technological advancement enables a 20% increase in the operational efficiency of automated machinery in sectors like mining and logistics.

What are the market trends shaping the Mid-high Level Precision GPS Industry?

- A defining market trend is the convergence of Global Navigation Satellite System (GNSS) technology with sensor fusion. This integration provides more robust and reliable positioning for mission-critical applications.

- Key trends are reshaping the market, moving beyond standalone hardware to comprehensive positioning engines. The convergence of GNSS with sensor fusion algorithms is critical, creating solutions that provide continuous and reliable navigation. This approach is becoming standard for dynamic positioning systems, where uptime is paramount.

- By tightly coupling data from multiple sensors, these systems can bridge GNSS signal outages, reducing positioning interruptions by over 80% in obstructed environments like urban canyons. Concurrently, the shift toward positioning as a service (PaaS) and cloud-based platforms is making high precision technology more accessible, converting large capital expenditures into manageable operational costs.

- This model is accelerating the creation of digital twins and improving site surveying automation, where data can be processed and shared in near-real-time, enhancing collaboration.

What challenges does the Mid-high Level Precision GPS Industry face during its growth?

- The high total cost of ownership and the complexity of system integration present a key challenge to industry growth.

- Despite technological advancements, significant challenges constrain broader market adoption. The high total cost of ownership, which includes hardware, software, and recurring subscriptions for correction services, remains a barrier for smaller enterprises. Integrating systems is also complex, often requiring specialized expertise that can increase initial project costs by up to 25%.

- Furthermore, the inherent vulnerability of GNSS signals to environmental and man-made interference poses a persistent reliability risk. Signal disruption in dense urban canyons can lead to positioning errors or complete loss of service in over 40% of operational time for un-augmented systems.

- Navigating complex regulatory landscapes and addressing data security risks associated with sensitive geospatial data add further layers of operational complexity, impacting everything from structural health monitoring to pipeline integrity management and smart city infrastructure.

Exclusive Technavio Analysis on Customer Landscape

The mid-high level precision gps market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mid-high level precision gps market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Mid-high Level Precision GPS Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mid-high level precision gps market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAA Taranis Visual Ltd. - Engineered GNSS systems with proprietary engines, tilt compensation, and versatile correction services deliver high-integrity positioning for professional applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAA Taranis Visual Ltd.

- Ag Leader Technology

- AGCO Corp.

- AgEagle Aerial Systems

- Bayer AG

- CropMetrics LLC

- CropX Technologies Ltd.

- Deere and Co.

- Digital Agri Solutions

- Farmers Edge Inc.

- GEA Group AG

- Madison One Holdings LLC

- Precision Planting

- Raven Industries Inc.

- Tetra Laval SA

- Topcon Positioning Systems Inc.

- Trimble Inc.

- Valmont Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mid-high level precision gps market

- In September, 2024, Trimble Inc. launched a new line of compact, low-power multi-frequency receivers designed for mass-market deployment in autonomous lawnmowers and delivery robots, aiming to democratize centimeter-level accuracy.

- In November, 2024, Hexagon AB announced a strategic partnership with a leading automotive Tier 1 supplier to integrate its Precise Point Positioning (PPP) correction services directly into next-generation vehicle infotainment platforms, enabling lane-level navigation as a standard feature.

- In February, 2025, Deere and Co. acquired a European startup specializing in AI-driven sensor fusion algorithms, a move intended to enhance the performance of its autonomous tractors in environments with frequent GNSS signal outages.

- In April, 2025, the European Union Agency for the Space Programme (EUSPA) declared the initial operational capability of a new Galileo authentication service, providing a verifiable layer of trust for safety-critical applications like unmanned aerial vehicle (UAV) guidance in controlled airspace.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mid-high Level Precision GPS Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.5% |

| Market growth 2025-2029 | USD 3201.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 15.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The mid-high level precision GPS market is evolving beyond hardware-centric sales into an integrated ecosystem where data and services are paramount. At the core of this transformation are advanced technologies like multi-constellation GNSS and multi-frequency receivers, which are becoming standard.

- The use of carrier phase measurement techniques, including real time kinematic (RTK) and precise point positioning (PPP), delivers the centimeter-level accuracy required by professional applications. For boardroom consideration, the decision to invest in survey grade equipment versus less precise differential grade systems now hinges on the total cost of ownership versus the ROI from operational efficiency.

- For instance, adopting systems with advanced multipath mitigation and anti-jamming capabilities, often coupled with inertial measurement units (IMUs) using dead reckoning technology, ensures uptime in challenging environments, achieving a 30% reduction in field survey times.

- This reliability is critical for geodetic surveying, machine control systems, and preventing gnss signal outages, making technology selection a key strategic decision impacting long-term capital expenditure and project viability.

What are the Key Data Covered in this Mid-high Level Precision GPS Market Research and Growth Report?

-

What is the expected growth of the Mid-high Level Precision GPS Market between 2025 and 2029?

-

USD 3.20 billion, at a CAGR of 15.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Frequency Range (Single frequency, and dual frequency), Type (Differential grade, and Survey grade), End-user (Agriculture, Construction, Oil and gas, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of automation and autonomous systems across key industries, High total cost of ownership and complex system integration

-

-

Who are the major players in the Mid-high Level Precision GPS Market?

-

AAA Taranis Visual Ltd., Ag Leader Technology, AGCO Corp., AgEagle Aerial Systems, Bayer AG, CropMetrics LLC, CropX Technologies Ltd., Deere and Co., Digital Agri Solutions, Farmers Edge Inc., GEA Group AG, Madison One Holdings LLC, Precision Planting, Raven Industries Inc., Tetra Laval SA, Topcon Positioning Systems Inc., Trimble Inc. and Valmont Industries Inc.

-

Market Research Insights

- The market's momentum is driven by the demand for high-fidelity geospatial data across industries. The adoption of positioning as a service (PaaS) is lowering entry barriers, enabling more businesses to access advanced capabilities. For example, using this model for as-built verification improves accuracy by over 40% compared to traditional methods.

- Furthermore, the integration of this technology in the construction project lifecycle has demonstrated a 15% reduction in project timelines by minimizing rework. The push for lane-level positioning in advanced driver assistance systems (ADAS) and the need for precision in variable rate technology (VRT) for agriculture are expanding application frontiers.

- This shift toward service-based, high-accuracy solutions is reshaping operational standards and creating new value streams.

We can help! Our analysts can customize this mid-high level precision gps market research report to meet your requirements.

RIA -

RIA -