Military GNSS Devices Market Size 2025-2029

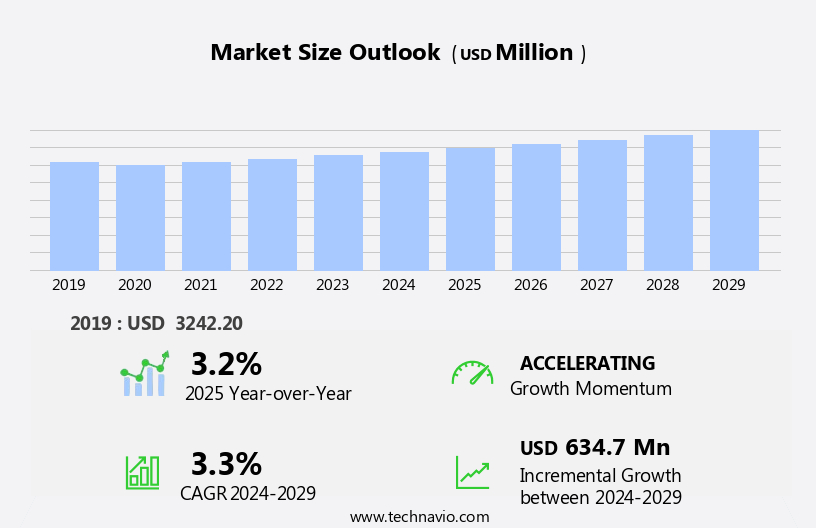

The military GNSS devices market size is forecast to increase by USD 634.7 million, at a CAGR of 3.3% between 2024 and 2029.

- The Military Global Navigation Satellite Systems (GNSS) Devices Market is driven by the growing demand for unmanned platforms in military applications. Unmanned aerial vehicles (UAVs), submarines, and ground vehicles are increasingly utilizing GNSS technology for navigation, positioning, and communication. Deep learning algorithms and AI-powered navigation enhance trajectory prediction and real-time decision-making. This trend is expected to continue as military forces seek to enhance operational capabilities and reduce risks to personnel. However, the market also faces significant challenges. The increasing focus on Network-Centric Warfare (NCW) necessitates robust and secure GNSS systems to ensure reliable communication and coordination among military assets.

- Technological limitations and other vulnerabilities, such as jamming and spoofing, pose significant threats to the integrity and availability of GNSS signals. Addressing these challenges will require continuous innovation and investment in advanced GNSS technologies and countermeasures. Companies in the market must stay abreast of these trends and challenges to effectively capitalize on market opportunities and navigate the strategic landscape. Sensor fusion and obstacle avoidance technologies enable autonomous navigation and battlefield visualization.

What will be the Size of the Military GNSS Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The Military Global Navigation Satellite System (GNSS) devices market is witnessing significant advancements, driven by the integration of sensor data and the fusion of multiple sources to enhance situational awareness. Geospatial intelligence and aerial reconnaissance play crucial roles in search and rescue operations and network centric warfare. Remote sensing and geodetic surveys contribute to precision agriculture and resource management. Secure communications protocols and interoperability standards ensure reliable data transmission in military environments.

- GNSS devices are essential for military data networks, enabling accurate positioning and tracking in various applications. Countermeasures against GPS spoofing and jamming are essential to maintain reliable positioning in contested environments. The integration of geospatial intelligence, remote sensing, and secure communications enhances military capabilities, providing a competitive edge on the battlefield. Military mapping and disaster response applications benefit from multi-constellation tracking and real-time data processing.

How is this Military GNSS Devices Industry segmented?

The military GNSS devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Airborne

- Land

- Naval

- Type

- Portable

- Integrated

- Product Type

- Navigation

- Surveillance

- Target acquisition

- Command and control

- Search and rescue

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Russia

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

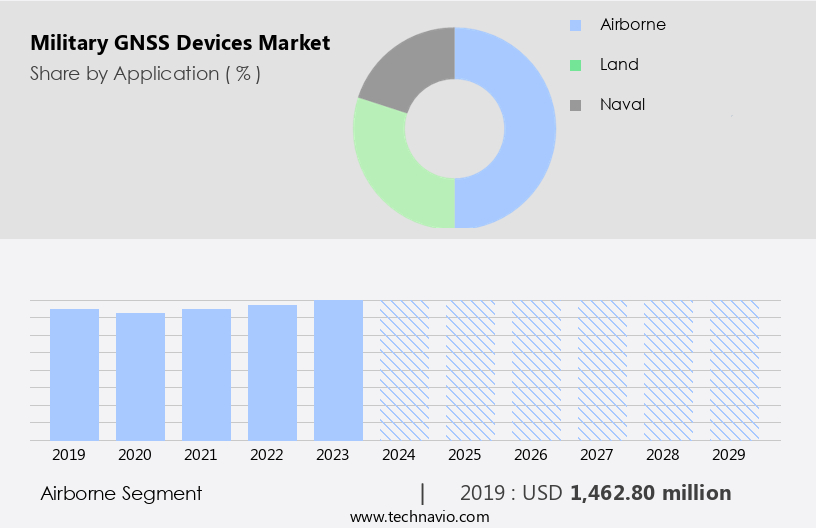

By Application Insights

The airborne segment is estimated to witness significant growth during the forecast period. Airborne vehicles, including those used for airdrops, helicopter lifts, gliders, and air landings, rely on Global Navigation Satellite System (GNSS) devices for real-time positional and navigational information. Prior to the integration of GNSS, the aviation industry faced challenges in identifying fuel-efficient routes and navigating complex terrain at low altitudes. With the implementation of military-grade GNSS devices, airborne units can now achieve accurate and continuous positioning, enhancing situational awareness during transportation and enabling precise drop zone supervision, even during nighttime operations. Military GNSS devices are integral to airborne applications, providing navigation software and real-time kinematic (RTK) capabilities for GPS-guided receivers.

These receivers issue steering commands to guide payloads to their intended drop zones. In addition, GNSS devices play a crucial role in mission planning, differential corrections, and time synchronization for electronic warfare systems and target tracking. Land-based military operations also benefit from the use of GNSS devices. They ensure precise positioning for force protection, surveillance systems, and command and control, as well as time synchronization for communication networks and logistics management. Furthermore, GNSS devices are essential for unmanned systems, enabling autonomous vehicle navigation and target tracking. Emerging technologies, such as multi-frequency operation, advanced filtering techniques, and high-sensitivity antennas, enhance the performance and reliability of GNSS devices in various military applications.

Military standards for environmental resistance, data security, and military-grade encryption ensure the devices' robustness and longevity in the field. Government procurement and certification requirements drive the demand for GNSS devices in the defense industry. Regular maintenance, software updates, and performance testing are essential to maintain the devices' operational readiness. In summary, the integration of GNSS devices into military applications, particularly airborne units, has revolutionized situational awareness, precision, and operational efficiency.

The Airborne segment was valued at USD 1.46 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

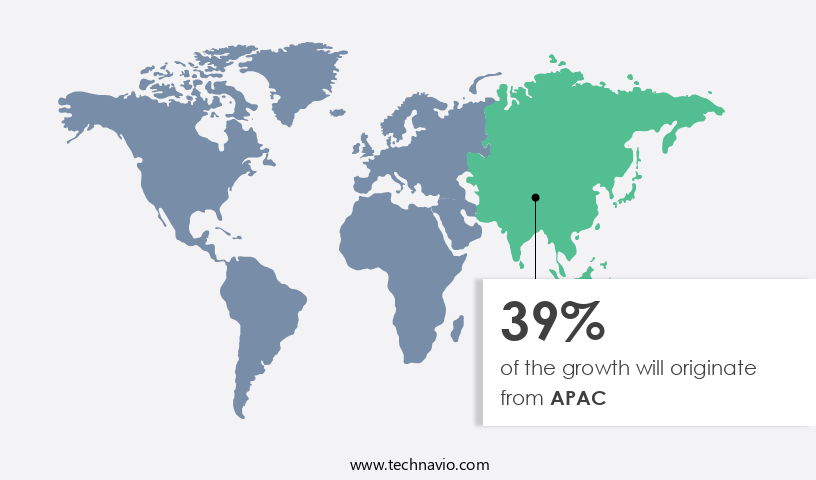

APAC is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The global military Global Navigation Satellite System (GNSS) devices market is experiencing significant growth due to the increasing demand for advanced tactical communications, positioning accuracy, and situational awareness in combat operations. Satellite constellations, such as GPS, GLONASS, Galileo, and BeiDou, play a crucial role in providing accurate location information for various military applications, including airborne, land-based, and maritime operations. Military standards for signal integrity and anti-jamming technology are essential for force protection and mission planning in electronic warfare environments. Autonomous vehicles and unmanned systems are increasingly being integrated into military operations, necessitating high-performance GNSS devices. Emerging technologies, such as multi-frequency operation, advanced filtering techniques, and real-time kinematic (RTK) GNSS data processing, are enhancing the capabilities of military GPS receivers and navigation software.

Maintenance and support, performance testing, and certification requirements are critical aspects of ensuring the reliability and effectiveness of these systems. The defense industry is investing heavily in logistics management, ruggedized design, and military grade encryption to improve force protection and data security. In land-based operations, GNSS devices are used for surveillance systems, intelligence gathering, and environmental resistance. High-sensitivity antennas and software updates are essential for maintaining optimal performance in challenging environments. The market for military GNSS devices is expected to continue growing due to the increasing need for accurate navigation and positioning in various military applications.

The US, with its significant defense expenditure and focus on upgrading military capabilities, holds a significant share of the global market. Collaboration between countries and the transfer of technology are driving innovation and advancing the capabilities of military GNSS devices. Maintenance and support, as well as performance testing, are essential to ensure the reliability and accuracy of these devices. The integration of military GPS receivers and navigation software is essential in network-centric warfare to ensure effective information gathering, analysis, and decision-making. These devices provide precise location information for unmanned systems and enable shared awareness about the battlespace for forces. Maintenance, support, and performance testing are necessary to ensure their reliability and accuracy, while emerging technologies continue to enhance their capabilities.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Military GNSS Devices market drivers leading to the rise in the adoption of Industry?

- The increasing need for unmanned platforms is the primary market driver, fueled by the growing demand for automation and remote operation in various industries. The Military Global Navigation Satellite Systems (GNSS) Devices Market is witnessing significant growth due to the increasing demand for advanced tactical communications and positioning accuracy in combat operations. The integration of satellite constellations into military systems enhances situational awareness, enabling force protection and effective anti-jamming technology.

- The market is expected to continue its growth trajectory as countries invest in advanced weapon systems to maintain their military superiority. The development of military standards for airborne applications is driving the market, particularly in the use of Unmanned Combat Aerial Vehicles (UCAVs) for surveillance and preemptive attacks. Improved signal integrity is crucial for the successful deployment of these systems, ensuring the reliability and cost-effectiveness of military assets. The integration of autonomous vehicles in military applications is also expected to boost market growth.

What are the Military GNSS Devices market trends shaping the Industry?

- The growing emphasis on Nanotechnology, Chemistry, and Materials Science (NCW) is a significant market trend that cannot be ignored. NCW is a multidisciplinary field that combines advanced knowledge in nanotechnology, chemistry, and materials science to develop new products and technologies. The potential applications of NCW are vast, ranging from healthcare and energy to electronics and manufacturing. Staying informed about the latest NCW research and developments is essential for businesses and individuals looking to remain competitive in today's rapidly evolving market.

- Military GPS receivers and navigation software play a crucial role in network-centric warfare (NCW) by providing precise location information for unmanned systems and field operations. NCW is a mode of warfare that links warfighting assets to achieve situational awareness and synchronization in a fast-paced environment. Effective information gathering, analysis, and decision-making are essential in NCW, making the integration of precise navigation sensors a necessity. These sensors help triangulate the position of drones or unmanned vehicles, enabling shared awareness about the battlespace for forces. Military GPS receivers are integral to land-based operations and electronic warfare, as they provide accurate positioning data for mission planning and differential corrections.

How does Military GNSS Devices market faces challenges during its growth?

- The expansion of the industry faces significant challenges due to technological limitations and other vulnerabilities. These factors pose a substantial impediment to growth. Military Global Navigation Satellite Systems (GNSS) devices play a crucial role in defense applications, including training and simulation, precision attack capability, command and control, time synchronization, target tracking, and maritime navigation. With heightened national security concerns, there is a growing demand for advanced Military GNSS devices that can operate in challenging environments and provide reliable and accurate data. Technological advancements have led to the development of multi-frequency operation and advanced filtering techniques to mitigate interference and improve signal accuracy.

- Constellations of geo-location satellites with automated trajectory correction are essential to maintain on-orbit formations and ensure consistent readings, even in the presence of intense jamming environments. Recent research highlights the importance of Military GNSS devices in defense applications. Their capabilities, such as precision attack, command and control, target tracking, and time synchronization, are vital to maintaining national security. Technological advancements, including multi-frequency operation, advanced filtering techniques, and automated trajectory correction, are essential to improving their performance and reliability. These devices also offer surveillance systems for situational awareness and data security measures to protect sensitive information.

Exclusive Customer Landscape

The military GNSS devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military GNSS devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, military gnss devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accord Software and Systems Pvt. Ltd. - The company specializes in providing advanced Global Navigation Satellite System (GNSS) devices for defense applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accord Software and Systems Pvt. Ltd.

- BAE Systems Plc

- Broadcom Inc.

- Cobham Ltd.

- Collins Aerospace

- Elbit Systems Ltd.

- Garmin Ltd.

- General Dynamics Corp.

- Hertz Systems Ltd. Sp. z.o.o

- Honeywell International Inc.

- JAVAD GNSS Inc.

- L3Harris Technologies Inc.

- Mayflower Communications Co. Inc.

- Novatel Inc.

- Qualcomm Inc.

- Safran SA

- Septentrio NV

- Thales Group

- Topcon Positioning Systems Inc.

- Trimble Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military GNSS Devices Market

- In March 2023, Lockheed Martin Corporation announced the successful integration of Advanced Navigation's Lite-Nav GNSS receiver into their Sniper Advanced Targeting Pod (ATP). This collaboration enhances the Sniper ATP's capabilities, providing more accurate and reliable positioning data for military aircraft (Lockheed Martin Press Release, 2023).

- In June 2024, Thales Alenia Space and the European Space Agency (ESA) signed a contract worth â¬1.3 billion (USD1.4 billion) to develop the next-generation Galileo satellite constellation, which will significantly improve the accuracy and availability of Global Navigation Satellite System (GNSS) signals for military applications (ESA Press Release, 2024).

- In October 2024, Honeywell International launched their Mini-UAV Navigator GNSS receiver, designed for small unmanned aerial vehicles (UAVs) used in military applications. This compact and lightweight receiver offers improved accuracy and reliability, expanding the capabilities of small UAVs in military operations (Honeywell Press Release, 2024).

- In January 2025, the U.S. Department of Defense (DoD) issued a request for proposals for a new satellite-based Positioning, Navigation, and Timing (PNT) system, aiming to reduce reliance on foreign GNSS systems and enhance military autonomy (DoD Solicitation, 2025). This initiative represents a significant shift towards self-sufficient military PNT capabilities.

Research Analyst Overview

The Military Global Navigation Satellite System (GNSS) devices market is characterized by continuous evolution and dynamic market activities. These advanced technologies play a pivotal role in various military sectors, including tactical communications, combat operations, and force protection. The integration of satellite constellations enables positioning accuracy for situational awareness, autonomous vehicles, and airborne applications. Military standards demand signal integrity and anti-jamming technology for uninterrupted operations. GNSS devices are essential for mission planning, real-time kinematic (RTK) positioning, and differential corrections in land-based and field operations. Command and control, time synchronization, and target tracking are crucial applications, necessitating deployment strategies that ensure optimal performance.

Multi-frequency operation and advanced filtering techniques enhance the reliability and accuracy of these systems. Surveillance systems and data security are integral components, ensuring the protection of sensitive information during intelligence gathering and maritime navigation. The defense industry continues to invest in emerging technologies, such as electronic warfare, precision attack capability, and unmanned systems. Maintenance and support, certification requirements, software updates, and military-grade encryption are essential for ensuring the longevity and effectiveness of these systems. GNSS devices are subjected to rigorous testing and certification processes to meet the demanding requirements of military applications. Environmental resistance, ruggedized design, and logistics management are critical considerations for the deployment and sustainability of these systems.

In the ever-evolving landscape of military technology, GNSS devices continue to play a vital role, enabling mission success and enhancing operational effectiveness. Emerging technologies, such as augmented reality and artificial intelligence, are enhancing the capabilities of military GPS receivers and navigation software.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military GNSS Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.3% |

|

Market growth 2025-2029 |

USD 634.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.2 |

|

Key countries |

US, China, India, Canada, Russia, Mexico, UK, Japan, France, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Military GNSS Devices Market Research and Growth Report?

- CAGR of the Military GNSS Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the military gnss devices market growth of industry companies

We can help! Our analysts can customize this military gnss devices market research report to meet your requirements.

RIA -

RIA -