Nasal Implants Market Size 2025-2029

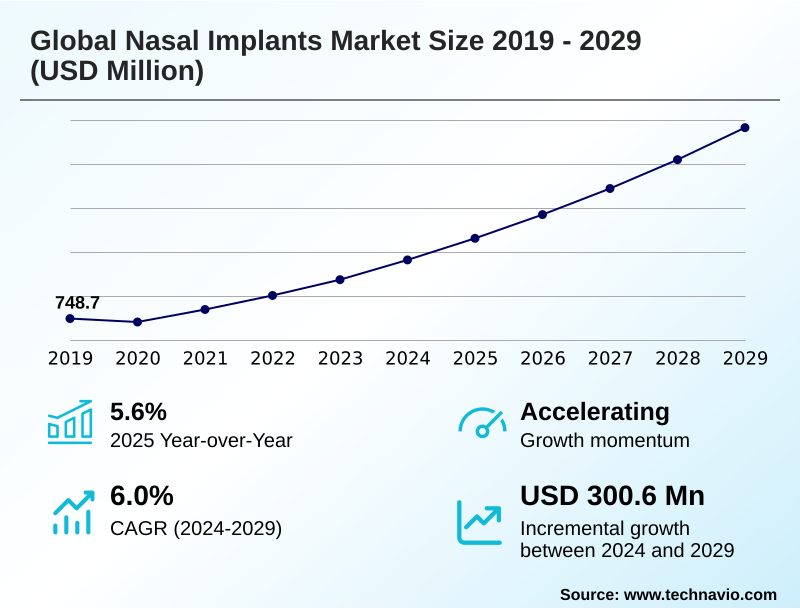

The nasal implants market size is valued to increase by USD 300.6 million, at a CAGR of 6% from 2024 to 2029. Rising prevalence of nasal obstruction and associated comorbidities such as obstructive sleep apnea will drive the nasal implants market.

Major Market Trends & Insights

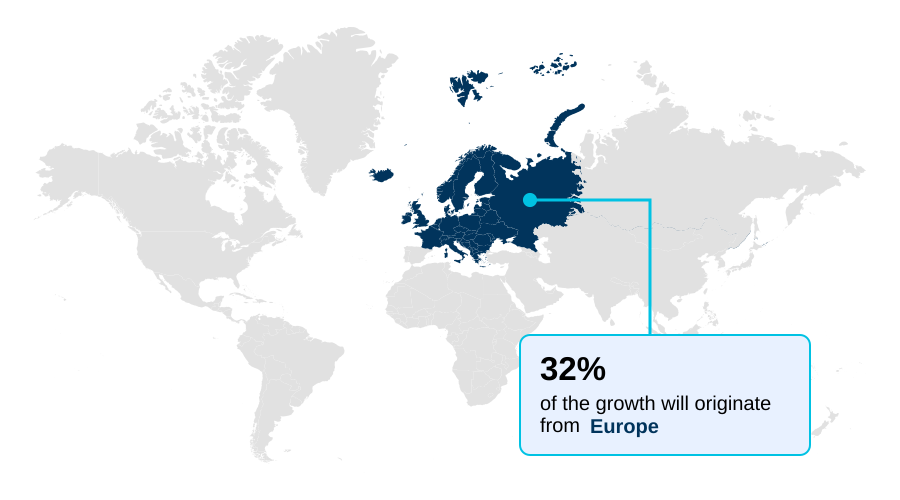

- Europe dominated the market and accounted for a 32.3% growth during the forecast period.

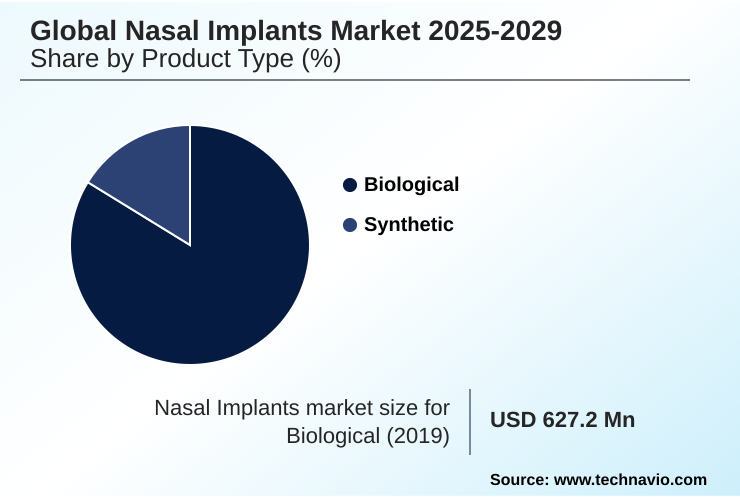

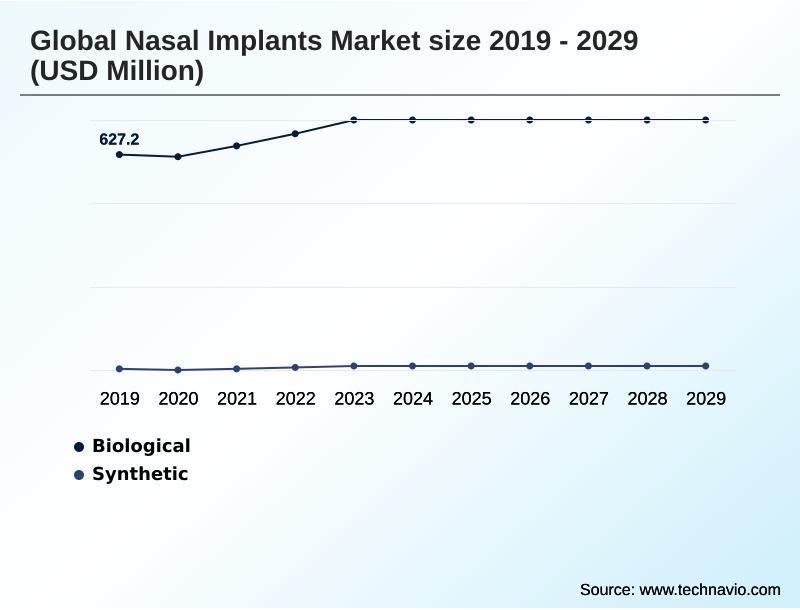

- By Product Type - Biological segment was valued at USD 708.8 million in 2023

- By End-user - Hospitals and clinics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 433.9 million

- Market Future Opportunities: USD 300.6 million

- CAGR from 2024 to 2029 : 6%

Market Summary

- The nasal implants market is evolving, driven by innovations in materials and a growing patient population seeking both functional and aesthetic improvements. A major driver is the increasing diagnosis of conditions such as nasal valve collapse, which significantly impacts quality of life.

- The market is shifting toward minimally invasive procedures that can be performed in outpatient settings, reducing recovery times and healthcare costs. For instance, the adoption of bioabsorbable polymers is transforming procedural risk profiles by eliminating the need for secondary removal surgeries. Concurrently, the development of 3D-printed, patient-specific implants represents a significant leap in personalization, offering superior anatomical fit.

- This addresses a critical operational challenge for surgical centers, where using custom implants can streamline inventory management by reducing the need to stock a wide range of standard sizes, thereby optimizing supply chain efficiency. However, navigating complex reimbursement landscapes and overcoming procedural inertia among clinicians remain significant hurdles.

- The competitive environment is further shaped by established pharmaceutical and alternative surgical options, requiring implant manufacturers to provide robust clinical evidence to demonstrate value.

What will be the Size of the Nasal Implants Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Nasal Implants Market Segmented?

The nasal implants industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product type

- Biological

- Synthetic

- End-user

- Hospitals and clinics

- Ambulatory surgical centers

- Type

- Open rhinoplasty

- Close rhinoplasty

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Product Type Insights

The biological segment is estimated to witness significant growth during the forecast period.

The biological implants segment is integral to the market, valued for inherent biocompatibility and host tissue integration.

This category, encompassing autologous cartilage grafts and processed allograft tissue processing, is the standard for complex procedures like revision rhinoplasty procedures and post-traumatic nasal reconstruction. Innovation is now targeting the limitations of traditional grafts, such as donor site morbidity.

Advances in tissue engineering scaffolds using recombinant human collagen are a key focus.

For example, new bioprinting techniques aim to create off-the-shelf solutions that mimic autograft benefits, with research showing a potential to reduce long-term resorption rates by over 30% compared to conventional allografts.

This progress in implant biocompatibility testing is critical for addressing conditions like nasal airway obstruction and its comorbidity, obstructive sleep apnea comorbidity.

The Biological segment was valued at USD 708.8 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Nasal Implants Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the market is characterized by mature, high-value regions and rapidly emerging growth centers. North America and Europe lead in procedural volume, driven by high healthcare spending and the demand for aesthetic nasal enhancement.

However, Asia is projected to demonstrate the highest market acceleration, outpacing Europe’s growth rate by approximately 6%. This expansion is fueled by rising disposable incomes and a strong cultural emphasis on cosmetic procedures.

In these established markets, the use of porous polyethylene implants for functional rhinoplasty is common. In contrast, challenges in developing regions often relate to access and affordability.

A key differentiator across all regions is the approach to nasal valve collapse repair, with an increasing global adoption of techniques that prioritize patient-reported outcome measures and leverage advanced materials like expanded polytetrafluoroethylene.

Success in this varied landscape requires adapting to different regulatory frameworks and addressing diverse clinical needs, from turbinate reduction surgery to complex reconstructions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus within the nasal implants market is shifting toward specialized applications and evidence-based outcomes. Key considerations for surgeons and healthcare systems now include detailed comparisons of autologous graft vs synthetic implant options, especially for revision rhinoplasty where alloplastic implants in revision rhinoplasty are common.

- The rise of the bioabsorbable implant for nasal obstruction is a significant trend, with devices like the LATERA implant demonstrating strong functional outcomes after LATERA implant placement. This has spurred interest in the material science of bioabsorbable polymers and the long-term outcomes of PEEK implants.

- For providers, the cost-effectiveness of absorbable nasal implants and the viability of an office-based nasal implant procedure are critical factors. This has led to a greater need for clear reimbursement codes for nasal implants.

- Technologically, innovations such as the 3D printed patient-specific nasal implant and the use of piezosurgery in closed rhinoplasty are enabling more precise outcomes in minimally invasive nasal valve repair and nasal framework reconstruction with allografts. Simultaneously, manufacturers must manage the complexities of regulatory approval for custom implants and provide clinical evidence for steroid-eluting stents.

- Addressing challenges such as managing complications of silicone implants, ensuring proper tissue integration in HDPE implants, and preventing implant migration in rhinoplasty through advanced surgical techniques for septal perforation remains paramount.

- The market is moving toward a more personalized and less invasive future, with data showing that patient-specific devices can reduce surgical planning time by more than 20% compared to conventional methods.

What are the key market drivers leading to the rise in the adoption of Nasal Implants Industry?

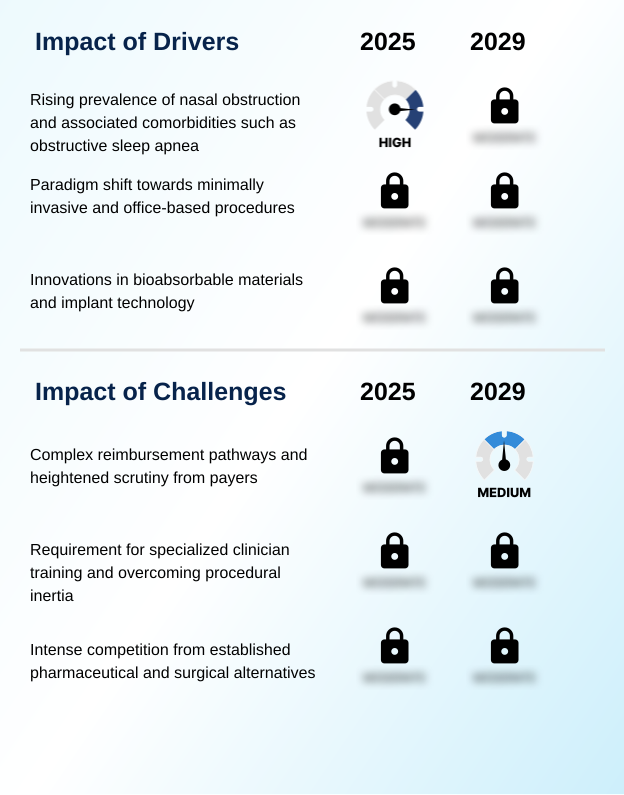

- The rising global prevalence of chronic nasal obstruction and its associated comorbidities, most notably obstructive sleep apnea, serves as a primary driver for market growth.

- Market growth is significantly driven by the shift toward minimally invasive procedures and the development of advanced materials.

- The rise of office-based nasal procedures performed under local anesthesia procedures meets growing patient demand for convenience and reduced downtime, with some techniques decreasing recovery periods by 30% compared to traditional surgeries.

- This trend is enabled by innovations like poly-L-lactic acid material, which provides temporary lateral nasal wall support before safe bioabsorbable implant degradation occurs.

- The increasing diagnosis of related conditions, accelerated by the accessibility of home sleep apnea tests, expands the patient pool for interventions aimed at improving nasal airway patency.

- The availability of robust long-term clinical data from studies in outpatient surgical settings is crucial, as it validates efficacy and supports favorable reimbursement decisions, directly impacting provider adoption rates.

What are the market trends shaping the Nasal Implants Industry?

- A significant market trend is the proliferation of bioabsorbable and advanced biocompatible materials. This shift addresses long-term risks associated with permanent implants, enhancing patient safety and outcomes.

- Key market trends are centered on personalization and biocompatibility, fundamentally altering surgical approaches. The adoption of 3D printed medical devices, leveraging CAD/CAM technology integration, enables the creation of patient-specific implants tailored to unique anatomies for congenital nasal defect correction and cranio-maxillofacial surgery.

- This level of customization improves surgical accuracy and has been shown to reduce intraoperative adjustment time by over 50%. Concurrently, the proliferation of advanced bioabsorbable polymers is addressing long-term safety concerns. Innovations in soft tissue matrices and drug-eluting implant technology are expanding treatment options beyond structural support to include active therapeutic benefits.

- This shift represents a move away from septoplasty alternatives toward more integrated solutions like nasal valve stabilization, which show improved long-term patient satisfaction rates by up to 20%.

What challenges does the Nasal Implants Industry face during its growth?

- Complex reimbursement pathways and heightened scrutiny from payers present a key challenge affecting industry growth and the widespread adoption of new technologies.

- The market faces considerable challenges related to economic and educational barriers that can slow adoption. Navigating complex reimbursement pathway analysis and securing favorable health technology assessment outcomes are primary hurdles, as inadequate payment models can make procedures financially unviable for providers.

- This is compounded by the need to overcome procedural learning curve inertia among seasoned surgeons, with data indicating that targeted training can shorten the adoption phase by 25%. Furthermore, intense competition from conservative medical management, such as advanced allergic rhinitis treatment options, and alternative surgical techniques like turbinate reduction surgery requires implant manufacturers to provide compelling comparative effectiveness data.

- The presence of well-established alloplastic implants and surgical navigation systems for septal perforation repair and nasal reconstruction surgery means new technologies must demonstrate clear advantages in either outcomes or cost-efficiency to gain market share.

Exclusive Technavio Analysis on Customer Landscape

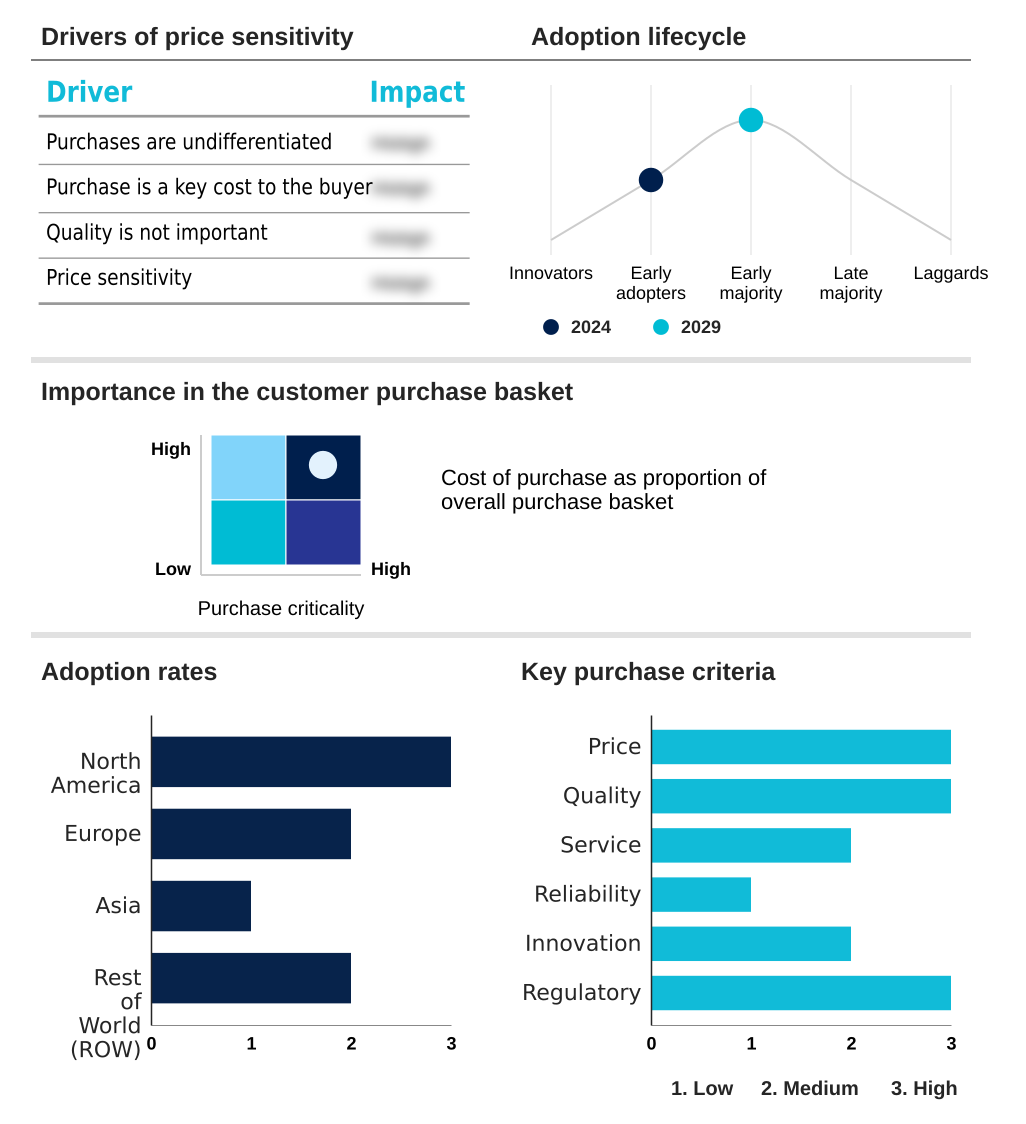

The nasal implants market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the nasal implants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Nasal Implants Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, nasal implants market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allergan Aesthetics - Offerings range from alloplastic implants for aesthetic enhancement to advanced bioabsorbable devices for functional reconstruction, addressing diverse surgical needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allergan Aesthetics

- B.Braun SE

- Gebruder Martin GmbH and Co.

- Global Consolidated Aesthetics Ltd.

- Implantech Associates Inc.

- Integra LifeSciences Corp.

- Johnson and Johnson Services

- KARL STORZ SE and Co. KG

- Matrix Surgical USA

- Medtronic Plc

- Olympus Corp.

- Silimed Industria de Implantes Ltd.

- Smith and Nephew plc

- Stryker Corp.

- Surgiform Technologies Ltd.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Nasal implants market

- In May 2025, a leading medical device firm launched a next-generation temperature-controlled radiofrequency device for turbinate reduction, promising faster procedures and improved patient outcomes.

- In February 2025, a prominent health insurer expanded its coverage policy for home sleep apnea tests, a move expected to increase diagnoses of related nasal obstruction issues.

- In November 2024, a specialized ENT device company announced the publication of a pivotal long-term clinical study for its office-based nasal airway remodeling technology, demonstrating durable symptom relief.

- In September 2024, a key player received regulatory clearance for a next-generation delivery system for its bioabsorbable nasal implant, featuring enhanced visualization and a more intuitive deployment mechanism.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Nasal Implants Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2025-2029 | USD 300.6 million |

| Market structure | Concentrated |

| YoY growth 2024-2025(%) | 5.6% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Spain, Italy, The Netherlands, Russia, India, South Korea, Japan, China, Indonesia, Thailand, Singapore, Brazil, Australia, UAE, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The nasal implants market is undergoing a significant transformation driven by material science and manufacturing innovations. A primary focus is on the development of bioabsorbable polymers, porous polyethylene implants, and advanced polyetheretherketone implants, which offer improved fibrovascular ingrowth and reduce the risk of implant extrusion prevention.

- The integration of CAD/CAM technology integration and 3D printed medical devices allows for the creation of patient-specific implants, revolutionizing procedures like functional rhinoplasty and nasal reconstruction surgery. For boardroom-level strategy, navigating the regulatory environment for these custom devices is now a critical consideration, impacting both R&D budgets and market entry timelines.

- Technologies such as cranial guidance software and surgical navigation systems are enhancing procedural precision for nasal valve collapse repair and septal perforation repair. The market offers a wide array of solutions, from alloplastic implants and expanded polytetrafluoroethylene sheets to tissue engineering scaffolds utilizing recombinant human collagen and autologous chondrocyte seeding.

- Minimally invasive procedures and office-based nasal procedures are gaining traction, supported by resorbable fixation systems and lateral nasal wall support devices, with some systems demonstrating a 25% reduction in procedure time for experienced clinicians. This trend is complemented by advancements like piezoelectric surgical instruments, steroid-eluting sinus implants, and innovative columellar incision techniques for aesthetic nasal enhancement and dorsal nasal augmentation.

- The emphasis on implant biocompatibility testing and ensuring nasal airway patency is paramount, whether using autologous cartilage grafts or processed allograft tissue processing in soft tissue matrices.

What are the Key Data Covered in this Nasal Implants Market Research and Growth Report?

-

What is the expected growth of the Nasal Implants Market between 2025 and 2029?

-

USD 300.6 million, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Biological, and Synthetic), End-user (Hospitals and clinics, and Ambulatory surgical centers), Type (Open rhinoplasty, and Close rhinoplasty) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of nasal obstruction and associated comorbidities such as obstructive sleep apnea, Complex reimbursement pathways and heightened scrutiny from payers

-

-

Who are the major players in the Nasal Implants Market?

-

Allergan Aesthetics, B.Braun SE, Gebruder Martin GmbH and Co., Global Consolidated Aesthetics Ltd., Implantech Associates Inc., Integra LifeSciences Corp., Johnson and Johnson Services, KARL STORZ SE and Co. KG, Matrix Surgical USA, Medtronic Plc, Olympus Corp., Silimed Industria de Implantes Ltd., Smith and Nephew plc, Stryker Corp., Surgiform Technologies Ltd. and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market dynamics are increasingly shaped by a shift toward value-based care and patient-centric solutions. The adoption of local anesthesia procedures in an outpatient surgical setting is a key trend, with facilities reporting procedure turnover times that are up to 40% faster than those in traditional hospital operating rooms.

- This efficiency is supported by peer-reviewed clinical studies that validate the long-term safety and efficacy of newer technologies, influencing both clinical practice and health technology assessment decisions. The regulatory submission process has become more stringent, demanding more extensive long-term clinical data, which in turn raises the barrier to entry.

- This environment favors technologies backed by robust evidence, as patient-reported outcome measures now play a more significant role in treatment selection, showing a 15% increase in consideration during consultations.

We can help! Our analysts can customize this nasal implants market research report to meet your requirements.

RIA -

RIA -