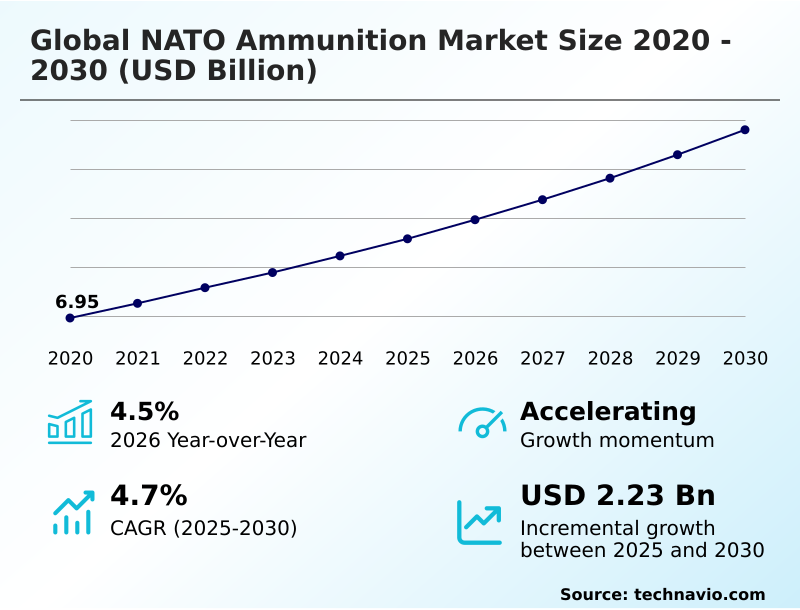

NATO Ammunition Market Size 2026-2030

The nato ammunition market size is valued to increase by USD 2.23 billion, at a CAGR of 4.7% from 2025 to 2030. Increasing in defense spending globally will drive the nato ammunition market.

Major Market Trends & Insights

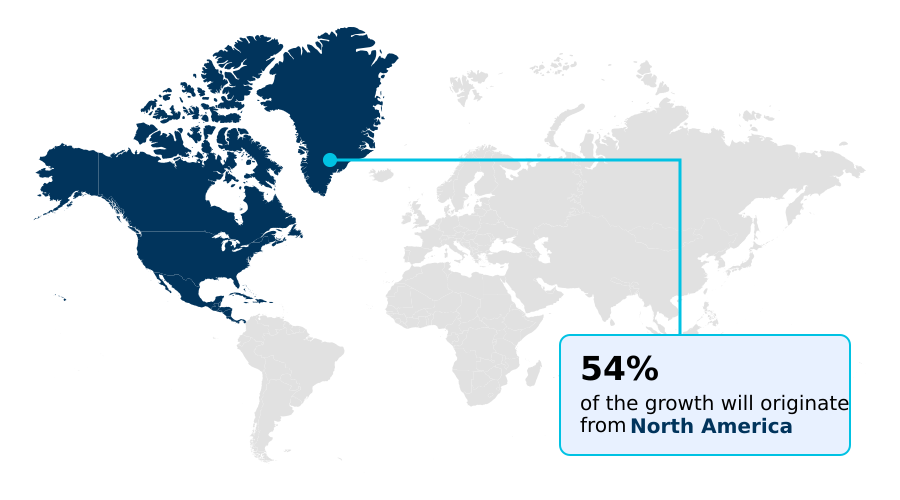

- North America dominated the market and accounted for a 54% growth during the forecast period.

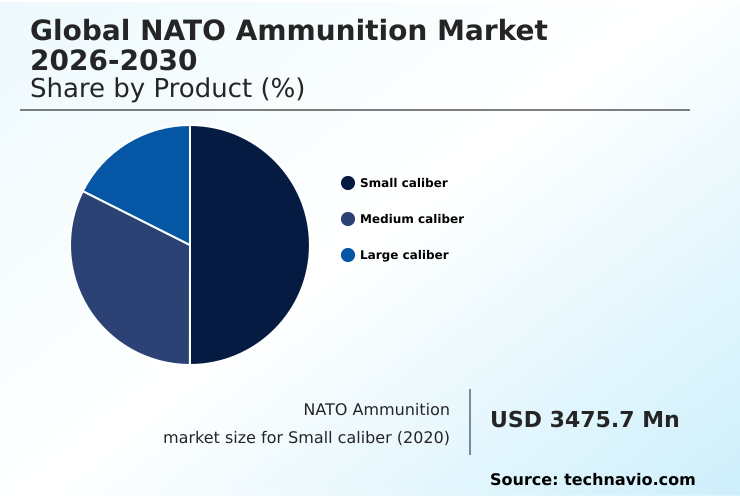

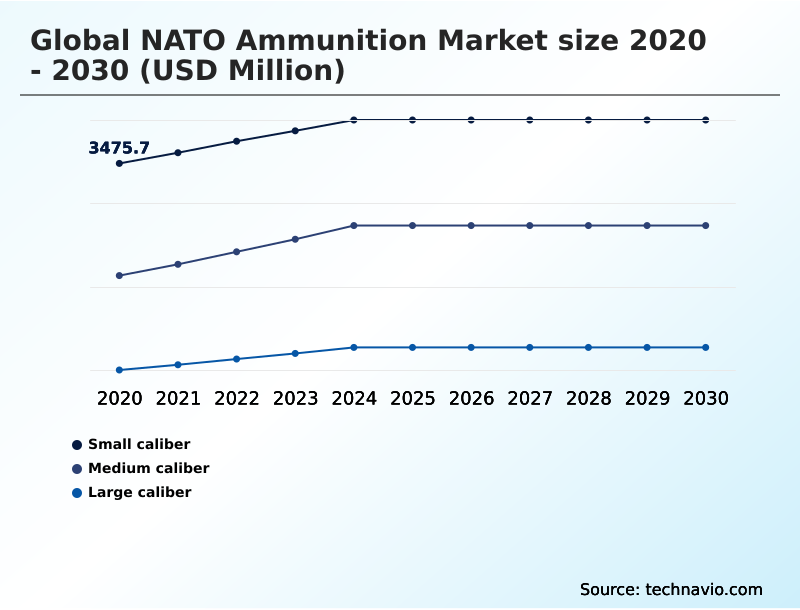

- By Product - Small caliber segment was valued at USD 3.95 billion in 2024

- By Type - Ground segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.85 billion

- Market Future Opportunities: USD 2.23 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The NATO ammunition market is undergoing a significant transformation, driven by heightened geopolitical tensions and a renewed focus on industrial readiness. Nations are moving beyond simple procurement to actively fostering sovereign production capabilities and enhancing ammunition supply chain resilience.

- This involves substantial investments in both expanding existing facilities and constructing new ones to ensure a steady supply of conventional munitions and advanced systems. Modernization efforts are a key aspect, with a clear shift towards developing and acquiring more effective ordnance.

- The development of precision guided artillery shells, extended range projectiles, and specialized armor piercing projectiles reflects a strategic imperative to gain a qualitative advantage.

- For defense planners, a key business challenge is balancing the urgent need for ammunition stockpile replenishment with long-term investments in next generation squad weapon ammunition technology, all while ensuring strict ITAR compliance and managing the complex logistics of critical raw material sourcing for materials like nitrocellulose.

What will be the Size of the NATO Ammunition Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the NATO Ammunition Market Segmented?

The nato ammunition industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Small caliber

- Medium caliber

- Large caliber

- Type

- Ground

- Aerial

- Naval

- End-user

- Military and defense forces

- Homeland security

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- South Korea

- Japan

- India

- Middle East and Africa

- Turkey

- Saudi Arabia

- UAE

- South America

- Brazil

- Colombia

- Rest of World (ROW)

- North America

By Product Insights

The small caliber segment is estimated to witness significant growth during the forecast period.

The small caliber ammunition segment is shaped by high-volume consumption for training and operations, with a strong focus on STANAG compliance for interoperability.

Current military modernization programs are driving demand for advanced rounds, including the new hybrid cased ammunition for the next generation squad weapon.

These innovations aim to improve infantry operational stamina and battlefield logistics efficiency by significantly reducing combat load, with some lightweight designs achieving up to a 30% reduction in carried weight.

The segment's evolution is closely tied to ammunition stockpile replenishment strategies and the integration of advanced rounds with digital battle management systems, ensuring forces maintain a decisive edge.

The Small caliber segment was valued at USD 3.95 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 54% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How NATO Ammunition Market Demand is Rising in North America Request Free Sample

The geographic landscape is dominated by North America, which commands over 50% of the market share, driven by large-scale modernization and ammunition stockpile replenishment programs.

However, Europe is exhibiting a higher growth rate of 5.2%, spurred by efforts to enhance sovereign production capability for high-intensity conflict readiness. This includes expanding facilities for medium caliber systems and precision guided artillery shells.

Across all regions, NATO ammunition interoperability is a critical requirement, influencing everything from C4ISR systems integration to foreign military sales.

This standardization ensures that allied forces can seamlessly support each other during joint tactical ISR missions and electronic warfare systems operations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus across the industry is currently on improving 155mm artillery shell production to meet the demands of modern attrition-based warfare. This has highlighted significant challenges in the nitrocellulose supply chain, prompting a re-evaluation of sourcing and domestic manufacturing capabilities.

- In parallel, there is a strong push toward technological advancement in smaller calibers, particularly concerning the standardization of 5.56x45mm rounds for greater interoperability. A key area of innovation is the next generation squad weapon ammunition technology, which explores novel materials and designs to enhance performance.

- The impact of polymer casings on ammunition weight is a critical consideration in this field, as it directly influences soldier mobility and logistical footprints. Logistical analysis shows that adopting such lightweight designs can reduce transportation and handling costs by up to 15% for an equivalent number of rounds.

- Furthermore, the cost-benefit of precision guided artillery shells continues to be a central topic for procurement decision-makers, who must balance the higher upfront expense against the significant increase in first-round accuracy and effectiveness.

What are the key market drivers leading to the rise in the adoption of NATO Ammunition Industry?

- The primary market driver is the significant global increase in defense spending among NATO member nations.

- A primary driver for the market is a significant shift in national defense policies, leading to increased defense budget allocation for weapon systems modernization. Many nations have raised defense spending by over 18% to support collective defense strategies.

- This funding directly fuels defense industrial base expansion, with munitions procurement strategies now prioritizing large caliber artillery.

- There is an unprecedented focus on increasing the output of the 155mm artillery projectile, with some facilities aiming to raise production by 200% to meet new stockpile targets.

- Similarly, investments are flowing into the manufacturing of rocket artillery components to bolster long-range strike capabilities.

What are the market trends shaping the NATO Ammunition Industry?

- A prominent modernization trend centers on reducing ammunition weight. This strategic shift is driven by the operational need for improved soldier mobility and greater logistical efficiency.

- Evolving geopolitical security imperatives are accelerating trends in the market, moving beyond conventional munitions. The focus is on adopting polymer casings and advanced composite materials through lightweight ammunition development, which can reduce a soldier's load by over 15% while contributing to combat readiness enhancement.

- Another key trend involves developing extended range projectiles that can increase artillery reach by more than 25% without requiring new launch platforms. These advancements, however, introduce challenges in critical raw material sourcing for specialized components, compelling a re-evaluation of supply chain dependencies to sustain momentum.

What challenges does the NATO Ammunition Industry face during its growth?

- The proliferation of illicit ammunition manufacturing and trafficking presents a significant challenge to market stability and global security.

- A major market challenge is ensuring ammunition supply chain resilience against the threats of illicit ammunition trafficking and state-sponsored diversion. With over 80% of global ammunition trade remaining outside official data, arms embargo monitoring becomes exceedingly difficult. The scarcity of critical materials like nitrocellulose and gun cotton adds another layer of complexity.

- Furthermore, stringent ITAR compliance and the high capital cost of certified explosive handling facilities create significant barriers. Poorly managed national stockpiles, accounting for an estimated 12% of weapons diversion, undermine security and highlight the urgent need for improved accountability.

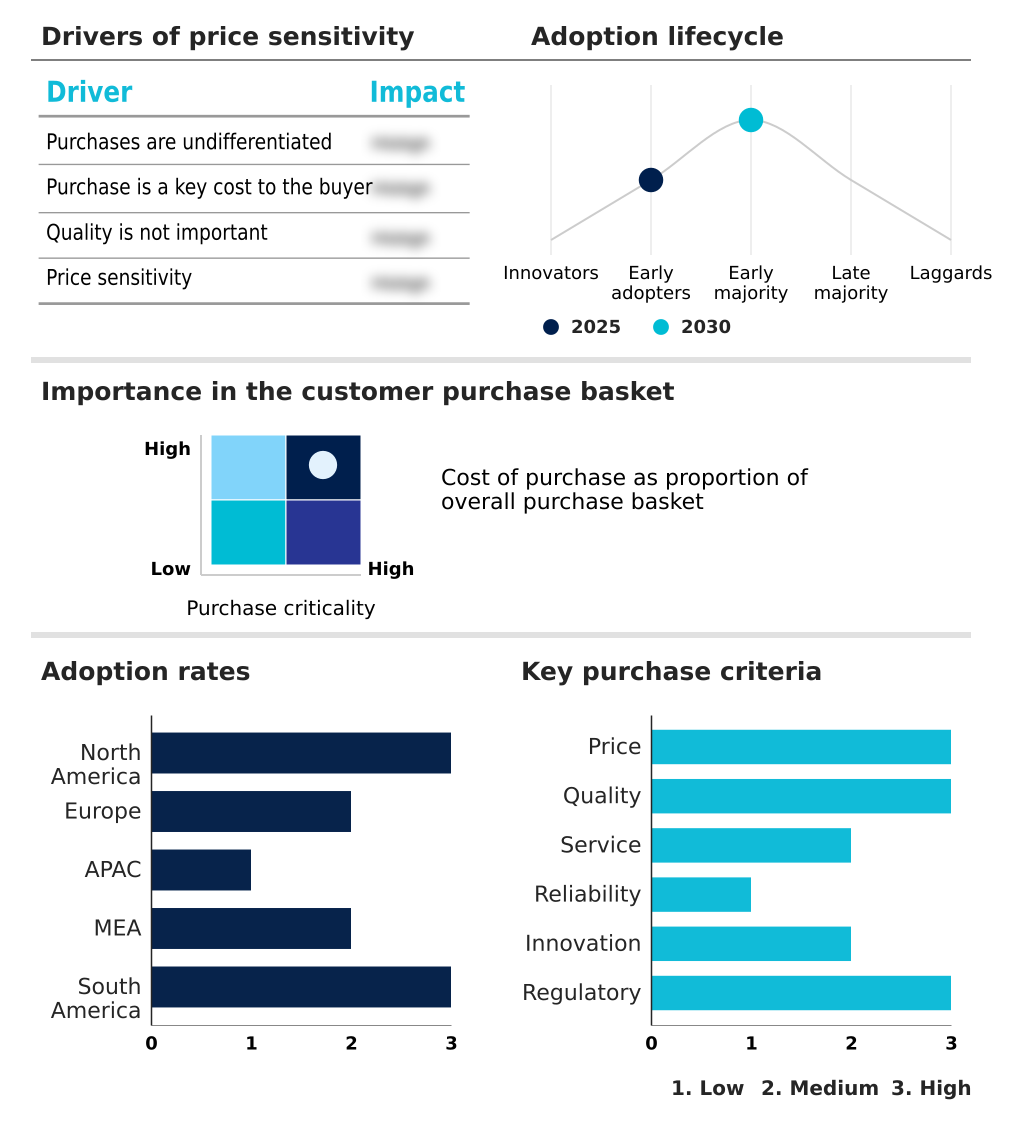

Exclusive Technavio Analysis on Customer Landscape

The nato ammunition market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the nato ammunition market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of NATO Ammunition Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, nato ammunition market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ARSENAL JS Co. - Offers a diverse portfolio of NATO-compliant ammunition for military and commercial defense, leveraging multiple specialized product lines for broad market coverage.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ARSENAL JS Co.

- BAE Systems Plc

- CBC Global Ammunition

- Diehl Stiftung and Co. KG

- FN Herstal SA

- General Dynamics Corp.

- Global Ordnance LLC

- KNDS N.V.

- Nammo AS

- Northrop Grumman Corp.

- Olin Corp.

- Polska Grupa Zbrojeniowa SA

- Poongsan Corp.

- Rheinmetall AG

- Thales Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Nato ammunition market

- In September 2024, Sig Sauer entered into a joint venture agreement with an Indian defense manufacturing facility to bolster India military capabilities amid rising global defense expenditures.

- In November 2024, Rheinmetall AG announced the completion of its capacity expansion project at the Varpalota facility in Hungary, significantly boosting the production of 155mm artillery projectiles for NATO partners.

- In March 2025, the German government, in partnership with Rheinmetall AG, announced a landmark initiative to construct a new, state-of-the-art small caliber ammunition plant in Lower Saxony to ensure sovereign production capability.

- In May 2025, Nammo AS announced a strategic partnership with a consortium of Nordic chemical suppliers to domesticate the production of nitrocellulose, aiming to reduce dependency on non-NATO raw material sources.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled NATO Ammunition Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 285 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 2226.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Poland, Spain, South Korea, Japan, India, Australia, Indonesia, Thailand, Turkey, Saudi Arabia, UAE, Egypt, Algeria, Brazil, Colombia and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The NATO ammunition market is experiencing a period of intense strategic realignment, forcing a reconsideration of long-held production and procurement models. A core boardroom-level decision revolves around weapon systems modernization, specifically balancing investment in advanced platforms like loitering munitions and hypersonic weapons against the urgent need to mass-produce conventional munitions.

- The adoption of new technologies, such as polymer casings and advanced composite materials for small caliber ammunition and medium caliber systems, requires significant capital expenditure in new explosive handling facilities. Executives must weigh the long-term benefits of lightweight ammunition, including enhanced soldier effectiveness and reduced logistical strain, against the high costs of retooling.

- This is particularly relevant as procurement analysis indicates that while price remains a key factor, mission-critical attributes like the effectiveness of armor piercing projectiles and extended range projectiles now account for over 40% of the decision-making criteria, signaling a shift from cost-centric to capability-focused acquisition strategies that align with modern C4ISR systems and battle management systems.

What are the Key Data Covered in this NATO Ammunition Market Research and Growth Report?

-

What is the expected growth of the NATO Ammunition Market between 2026 and 2030?

-

USD 2.23 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Small caliber, Medium caliber, and Large caliber), Type (Ground, Aerial, and Naval), End-user (Military and defense forces, Homeland security, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing in defense spending globally, Proliferation of illicit ammunition manufacturers

-

-

Who are the major players in the NATO Ammunition Market?

-

ARSENAL JS Co., BAE Systems Plc, CBC Global Ammunition, Diehl Stiftung and Co. KG, FN Herstal SA, General Dynamics Corp., Global Ordnance LLC, KNDS N.V., Nammo AS, Northrop Grumman Corp., Olin Corp., Polska Grupa Zbrojeniowa SA, Poongsan Corp., Rheinmetall AG and Thales Group

-

Market Research Insights

- Market dynamics are increasingly shaped by geopolitical security imperatives that are accelerating munitions procurement strategies and driving defense industrial base expansion. Strategic investments in sovereign production capability have already led to a 20% reduction in reliance on foreign sourcing for certain critical components.

- Simultaneously, the focus on combat readiness enhancement is fueling lightweight ammunition development, which has been shown to improve infantry operational stamina by over 15% during extended missions. These shifts reflect new national defense policies that prioritize high-intensity conflict readiness and battlefield logistics efficiency.

- As a result, long-term contracts are being awarded to ensure ammunition stockpile replenishment and support sustained military modernization programs.

We can help! Our analysts can customize this nato ammunition market research report to meet your requirements.