Natural Language Generation Market Size 2025-2029

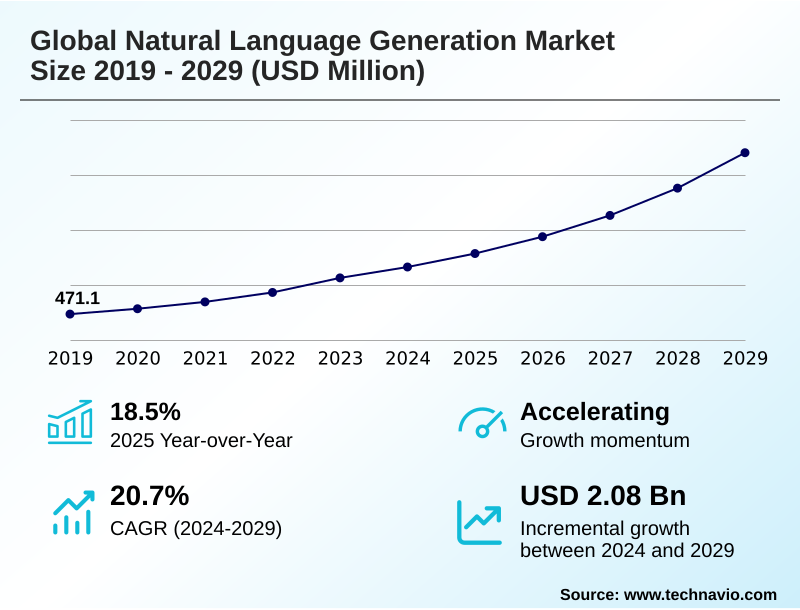

The natural language generation market size is valued to increase by USD 2.08 billion, at a CAGR of 20.7% from 2024 to 2029. Proliferation of advanced AI and LLM will drive the natural language generation market.

Major Market Trends & Insights

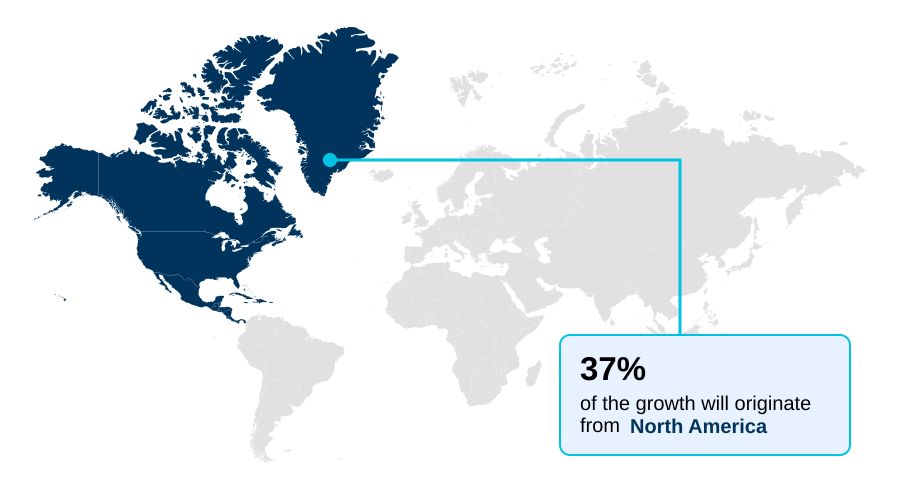

- North America dominated the market and accounted for a 36.8% growth during the forecast period.

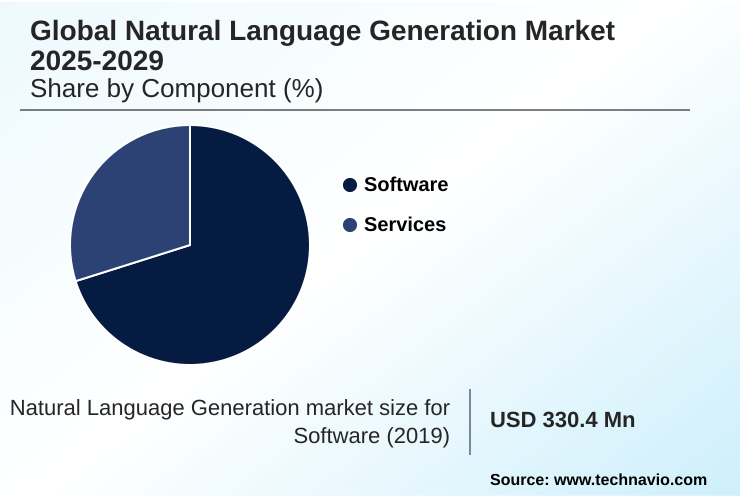

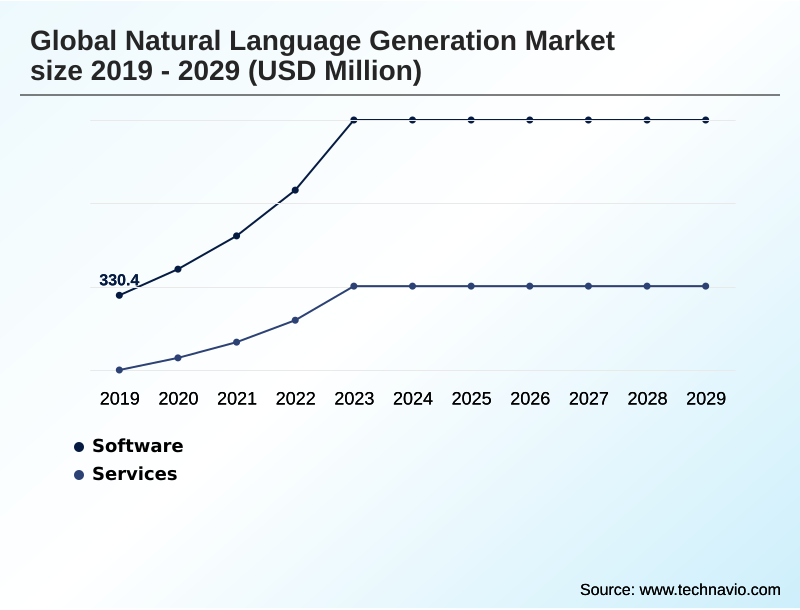

- By Component - Software segment was valued at USD 775.6 million in 2023

- By Deployment - Cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.93 billion

- Market Future Opportunities: USD 2.08 billion

- CAGR from 2024 to 2029 : 20.7%

Market Summary

- The natural language generation market is fundamentally transforming how businesses convert raw data into actionable intelligence. This technology leverages sophisticated algorithms to automate the creation of human-like text, turning complex datasets into coherent, readable narratives. Key drivers include the escalating demand for data-driven decision-making and the need for operational efficiency across industries.

- For example, in the financial sector, firms are deploying these systems to automate the generation of quarterly earnings reports and compliance documents, a process that was once manual and error-prone. This shift frees analysts to focus on strategic interpretation rather than repetitive writing.

- The market's trajectory is also shaped by advancements in deep learning and large language models, which are making the generated content more nuanced and contextually aware. However, the technology's dependence on high-quality, unbiased training data presents a notable challenge, as does the need to ensure the factual accuracy of the automated outputs.

- As the technology matures, its integration with business intelligence tools is democratizing data analysis, empowering a broader range of users to understand and act on complex information without requiring deep technical expertise. This evolution marks a significant step toward more intelligent and automated enterprise operations.

What will be the Size of the Natural Language Generation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Natural Language Generation Market Segmented?

The natural language generation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud

- On premise

- Application

- Risk and compliance management

- BFSI

- Healthcare

- Retail and e-commerce

- Media and entertainment

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is shifting from standalone platforms to embedded capabilities within enterprise applications. This evolution is driven by the need for seamless automated content creation and real-time data narratives directly within business workflows.

Innovations in transformer architectures are central to this change, enabling more sophisticated text summarization and prompt engineering.

The integration of NLG for compliance documentation and financial reporting automation is becoming standard, as firms using these tools report up to a 90% reduction in reporting errors.

This deep integration makes data-driven storytelling accessible to non-technical users, leveraging tokenization process and embedding models to turn complex data into clear insights, which enhances operational efficiency gains.

The Software segment was valued at USD 775.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Natural Language Generation Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which is projected to contribute over 36% of the market’s incremental growth, driven by early adoption and a high concentration of technology leaders.

The region's mature infrastructure supports advanced applications of generative AI and natural language understanding (NLU), particularly in its highly regulated financial and healthcare sectors.

Meanwhile, APAC is the fastest-growing region, fueled by rapid digitalization and a burgeoning e-commerce sector that demands multilingual content generation. The proliferation of AI model-as-a-service offerings is lowering entry barriers, fostering innovation in countries like India and China.

Europe's growth is propelled by a strong focus on AI governance frameworks and ethical AI deployment, which builds trust and encourages enterprise adoption for applications such as clinical documentation improvement.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly evaluating the strategic benefits of natural language generation, often starting by comparing on-premise vs. cloud NLG solutions to align with security and scalability needs. A key adoption pathway involves NLG integration with CRM platforms, which transforms customer data into actionable insights and enhances communication.

- For instance, firms are now improving customer service with conversational AI that delivers nuanced and personalized support. In parallel, the technology is revolutionizing content-centric operations, demonstrated by the use of NLG for personalized e-commerce descriptions, which can significantly lift conversion rates. The application of NLG for automated technical documentation streamlines knowledge management and reduces manual effort.

- In finance, automating financial reports with NLG is becoming standard practice, with some firms reducing report generation times from days to minutes, an efficiency gain nearly double that of other automated business processes. Success in these areas depends on addressing the core data quality requirements for NLG systems.

- As organizations scale, many are fine-tuning language models for specific industries to improve accuracy and relevance, whether for creating personalized travel itineraries with NLG or for use of NLG in media and entertainment.

- These targeted applications underscore the technology's versatility, from reducing compliance risk with NLG to optimizing supply chain reports using NLG, which are critical for modernizing how NLG improves business process automation.

What are the key market drivers leading to the rise in the adoption of Natural Language Generation Industry?

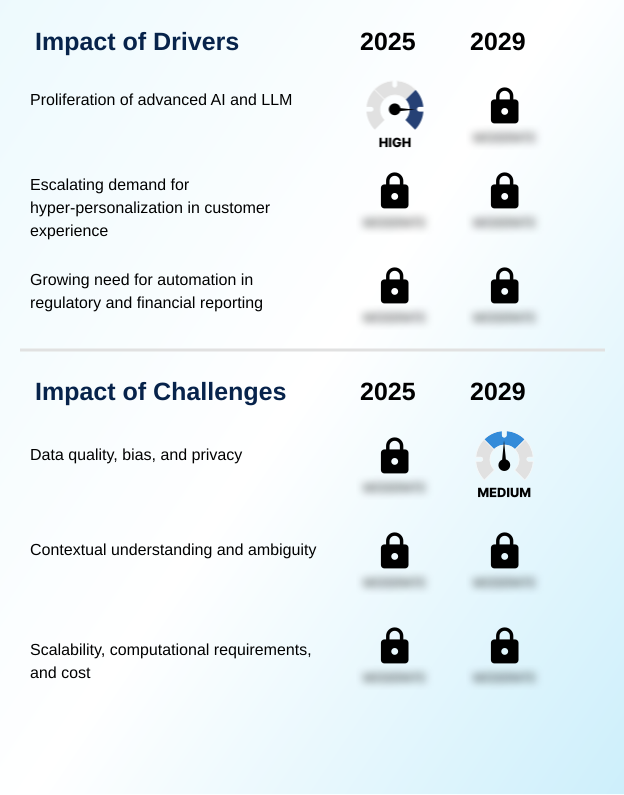

- The proliferation of advanced AI, particularly large language models, is the fundamental driver accelerating growth and innovation within the Natural Language Generation market.

- The market is significantly driven by the enterprise push for hyper-personalization at scale and the need for regulatory reporting automation.

- The use of large language models for customer experience personalization allows companies to craft unique messages, with some reporting up to a 45% increase in customer engagement.

- This capability is powered by deep neural networks that analyze user data to generate highly relevant content. Simultaneously, the demand for automation in creating financial portfolio summaries and other compliance-related documents is intensifying.

- Businesses using natural language generation for these tasks have reduced manual reporting efforts by over 80%. This dual focus on enhancing customer interactions through conversational AI and streamlining back-office functions through report automation is fueling widespread adoption across industries.

What are the market trends shaping the Natural Language Generation Industry?

- The Natural Language Generation market is witnessing a significant shift toward multimodal platforms that integrate text with other data formats. Concurrently, there is a growing demand for explainable AI to ensure transparency and trust in automated outputs.

- A primary trend is the shift toward multimodal platforms and the increasing demand for explainable AI. These advanced systems are moving beyond simple text summarization to integrate visual data, enabling the generation of richer, context-aware content. The use of retrieval-augmented generation enhances factual accuracy, a critical factor for enterprise adoption where user trust is paramount.

- Systems incorporating explainability features report up to 20% higher user acceptance rates. Concurrently, the development of domain-specific NLG models for industries like finance and healthcare is accelerating, as these models offer superior performance on specialized tasks.

- This focus on both multimodal capabilities and model explainability is crucial for building reliable AI-powered systems that can handle complex, real-world applications in business intelligence integration and beyond.

What challenges does the Natural Language Generation Industry face during its growth?

- Significant challenges surrounding data quality, inherent bias in training datasets, and complex privacy regulations restrain the seamless growth and adoption of Natural Language Generation technologies.

- Key challenges center on data quality, model bias, and the high computational cost of scaling systems. The performance of any linguistic realization process is directly tied to its training data, and biased datasets can lead to skewed outcomes in over 30% of deployments, creating significant reputational risk.

- Issues with data privacy in NLG are compounded by complex, evolving AI governance frameworks. Furthermore, the cost of training state-of-the-art models has increased exponentially, creating barriers for smaller organizations.

- The significant computational requirements for both training and inference demand scalable AI infrastructure that remains expensive to acquire and maintain, hampering the broader democratization of advanced NLG capabilities and prompting a focus on computational cost reduction.

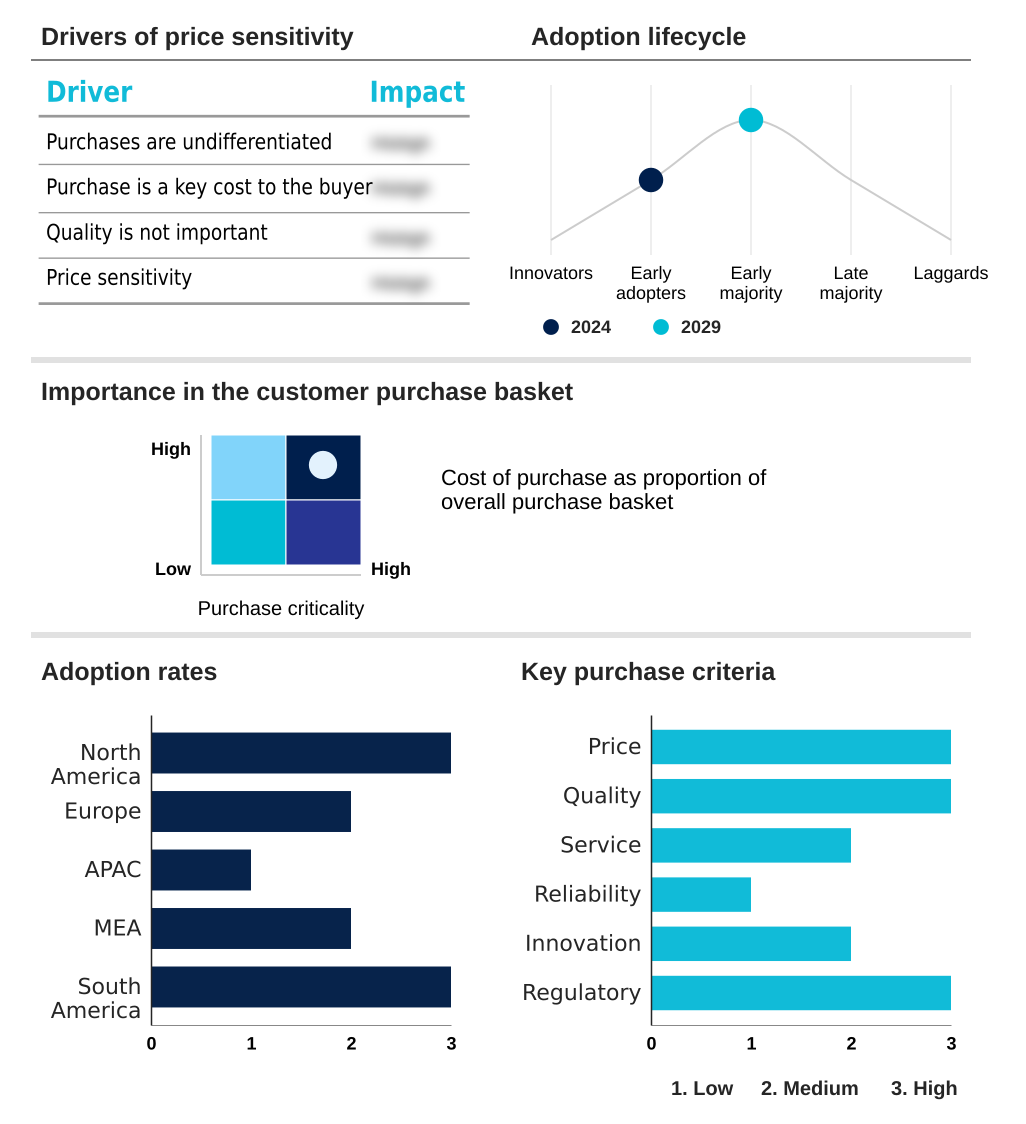

Exclusive Technavio Analysis on Customer Landscape

The natural language generation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the natural language generation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Natural Language Generation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, natural language generation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Provides a scalable, cloud-based natural language generation platform, enabling code generation, advanced summarization, and conversational AI for enterprise applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Apple Inc.

- ARRIA NLG Ltd.

- AX Semantics GmbH

- Baidu Inc.

- Dolbey Systems Inc.

- Google LLC

- Hewlett Packard

- Interactions LLC

- IBM Corp.

- Lexalytics Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- Nuance Communications Inc.

- SAP SE

- SAS Institute Inc.

- Verint Systems Inc.

- YSEOP

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Natural language generation market

- In September 2024, Yseop launched an advanced digital assistant, leveraging generative AI to automate the creation of complex clinical trial documentation for the biopharmaceutical industry.

- In October 2024, CoRover.ai, in collaboration with a major cloud provider, introduced a generative AI platform with a focus on Indian languages to deliver more inclusive and multilingual NLG solutions.

- In November 2024, Salesforce announced the integration of its generative AI technology into its CRM platform, enabling the automatic generation of sales emails, case summaries, and marketing content.

- In January 2025, SAP revealed plans to embed generative AI capabilities across its entire application suite, including S/4HANA Cloud, to automate tasks like job description creation and sales order completion.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Natural Language Generation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.7% |

| Market growth 2025-2029 | USD 2077.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 18.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, UAE, Saudi Arabia, Israel, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by rapid advancements in large language models and transformer architectures, which are elevating the sophistication of data-to-text conversion. Core processes such as semantic analysis, syntactic parsing, and the tokenization process are becoming highly automated through advanced neural network models and new embedding models.

- This facilitates more effective prompt engineering and fine-tuning models for specific use cases like report automation and question answering systems. Enterprises leveraging these technologies for compliance documentation have demonstrated a 90% reduction in reporting errors, a metric that drives boardroom-level decisions on technology investment.

- The focus is shifting toward practical applications, including dialogue generation for customer service, real-time data narratives for operational oversight, and personalized marketing copy. As capabilities in text summarization and automated content creation mature, the technology is becoming integral to functions ranging from financial reporting automation to clinical trial reporting and product description generation.

What are the Key Data Covered in this Natural Language Generation Market Research and Growth Report?

-

What is the expected growth of the Natural Language Generation Market between 2025 and 2029?

-

USD 2.08 billion, at a CAGR of 20.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services), Deployment (Cloud, On premise), Application (Risk and compliance management, BFSI, Healthcare, Retail and e-commerce, Media and entertainment) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of advanced AI and LLM, Data quality, bias, and privacy

-

-

Who are the major players in the Natural Language Generation Market?

-

Amazon Web Services Inc., Apple Inc., ARRIA NLG Ltd., AX Semantics GmbH, Baidu Inc., Dolbey Systems Inc., Google LLC, Hewlett Packard, Interactions LLC, IBM Corp., Lexalytics Inc., Meta Platforms Inc., Microsoft Corp., Nuance Communications Inc., SAP SE, SAS Institute Inc., Verint Systems Inc. and YSEOP

-

Market Research Insights

- Market dynamics are defined by the pursuit of hyper-personalization at scale, driven by customer experience personalization and the need for more contextually aware responses in service interactions. Augmented analytics platforms now integrate natural language generation, with some achieving a 40% reduction in time-to-insight. This business intelligence integration allows for more effective data-driven storytelling.

- The demand for regulatory reporting automation is also a major factor, as companies aim for flawless compliance. In customer service, the use of virtual assistant responses powered by sophisticated models has improved first-contact resolution rates by over 25%.

- This push for efficiency and personalization is creating a competitive landscape where scalable AI infrastructure and effective AI governance frameworks are critical for success.

We can help! Our analysts can customize this natural language generation market research report to meet your requirements.

RIA -

RIA -