Office Coffee Service Market Size 2026-2030

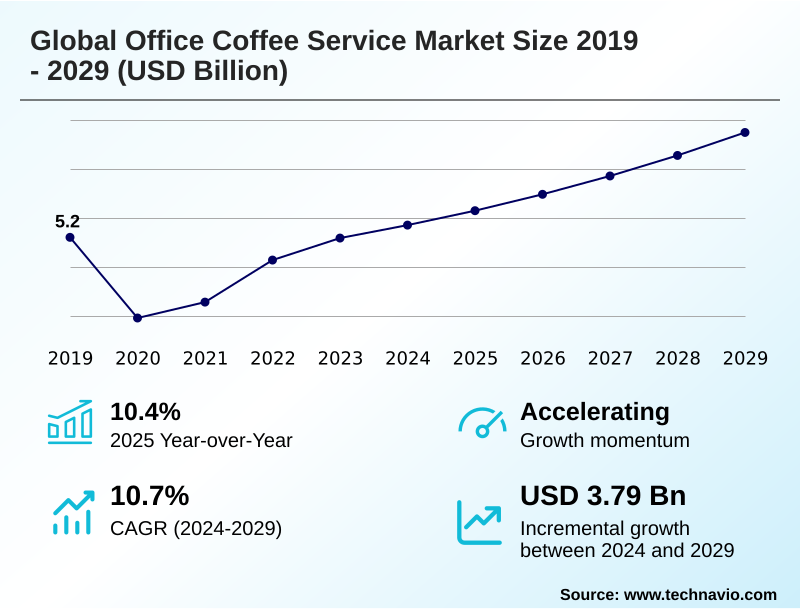

The office coffee service market size is valued to increase by USD 4.94 billion, at a CAGR of 12.3% from 2025 to 2030. Increasing corporate emphasis on employee retention and workplace well-being will drive the office coffee service market.

Major Market Trends & Insights

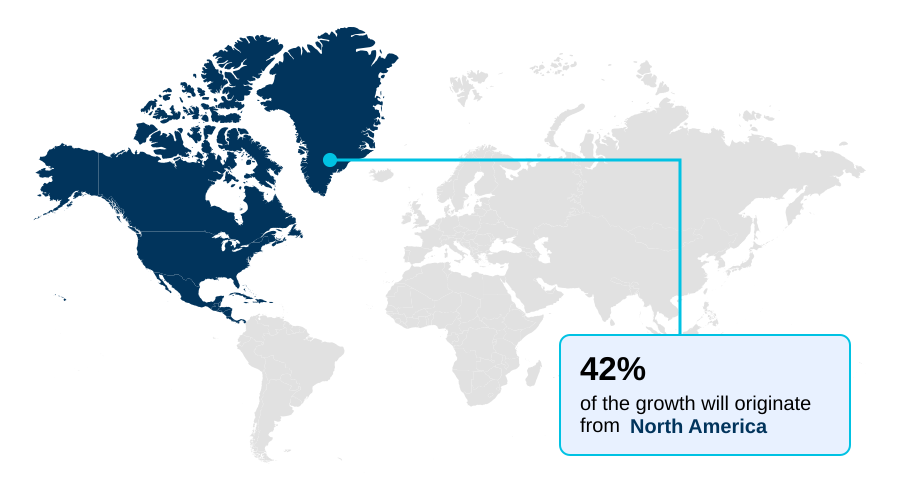

- North America dominated the market and accounted for a 42.7% growth during the forecast period.

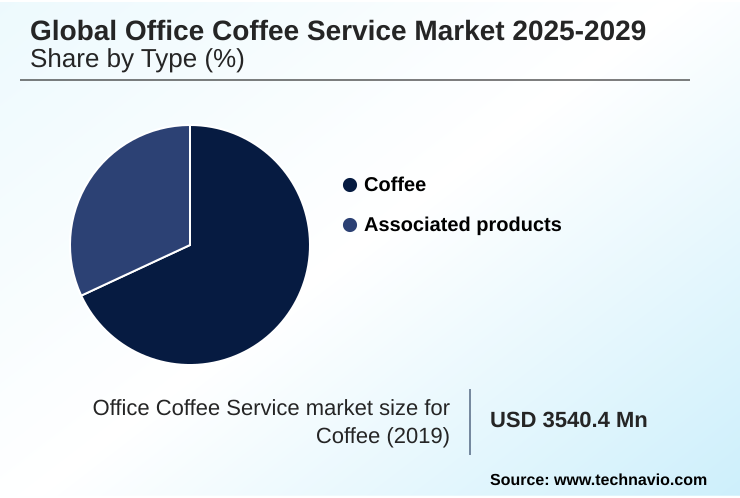

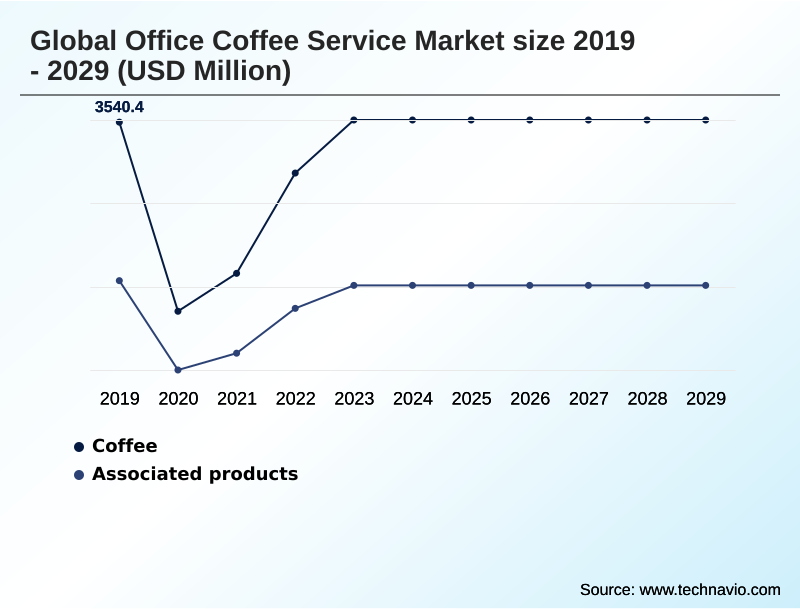

- By Type - Coffee segment was valued at USD 3.94 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.34 billion

- Market Future Opportunities: USD 4.94 billion

- CAGR from 2025 to 2030 : 12.3%

Market Summary

- The office coffee service market is undergoing a profound transformation, moving beyond simple beverage provision to become a strategic tool for corporate entities. As organizations focus on creating engaging workplaces to attract and retain talent, the breakroom has evolved into a central hub for collaboration and morale.

- This shift is fueled by a demand for premium, cafe-quality experiences, compelling providers to offer sophisticated bean-to-cup systems and artisanal roasts. A key business scenario involves optimizing supply chains using data-driven logistics, where telemetry capabilities on smart brewing systems predict consumption patterns.

- This allows for preventative maintenance and ensures inventory management is aligned with fluctuating office attendance, reducing waste and operational costs. Concurrently, sustainability has become a non-negotiable aspect, with corporate clients demanding ethical sourcing, fair trade certifications, and compostable packaging.

- Navigating the high capital expenditure for commercial-grade machines and the operational costs of managed service contracts remains a challenge, pushing the industry toward flexible equipment leasing programs and subscription frameworks to meet diverse client needs.

What will be the Size of the Office Coffee Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Office Coffee Service Market Segmented?

The office coffee service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Coffee

- Associated products

- End-user

- Large enterprises

- SMEs

- Service type

- Subscription based

- One time purchase

- Managed services

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The coffee segment is estimated to witness significant growth during the forecast period.

The coffee segment is the foundational pillar of the global office coffee service market 2026-2030, driven by its role in corporate wellness initiatives and enhancing corporate culture.

The trend of premiumization has shifted demand toward custom artisanal roasts and high-quality workplace beverage programs that require commercial-grade machines.

This evolution toward on-demand beverage quality reflects a strategic move to improve employee satisfaction, with North America alone poised to contribute over 42% of the market's incremental growth.

To meet this demand for premium beverage offerings, providers are deploying high-volume dispense units and automated brewing systems that mirror the experience of workplace cafe solutions.

Ethical sourcing and the provision of customized beverage profiles are now standard expectations in procurement.

The Coffee segment was valued at USD 3.94 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Office Coffee Service Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global office coffee service market 2026-2030 is led by North America, which accounts for over 42% of the incremental growth, driven by a mature corporate culture that prioritizes hybrid work model amenities and employee engagement platforms.

In contrast, Europe's market, contributing over 28% of growth, is characterized by a strong emphasis on a sustainable coffee supply chain. Providers are leveraging subscription frameworks and managed service contracts to offer flexible solutions globally.

Telemetry capabilities and data-driven logistics are crucial for optimizing operations, with smart, energy-efficient equipment enabling preventative maintenance and efficient breakroom management.

The adoption of integrated facility services and equipment leasing programs allows for scalable, single-source procurement, meeting the complex needs of multinational clients.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the contemporary office coffee service market requires a deep dive into several interconnected factors. The impact of hybrid work on office coffee consumption is a primary consideration, forcing a re-evaluation of traditional service models.

- This leads to a cost-benefit analysis of managed coffee services versus direct ownership, where IoT integration in commercial coffee machines for smart coffee machine maintenance and diagnostics plays a pivotal role.

- The ROI of premium office coffee amenities is now directly linked to employee well-being programs and corporate brand image, which is why the importance of ethical sourcing for corporate brand image cannot be understated. Technology advancements in automated coffee vending and touchless brewing technology for workplace safety are also critical.

- Businesses are comparing bean-to-cup vs pod systems for offices, considering factors like single-serve coffee waste reduction solutions. For smaller companies, finding the best office coffee solutions for small businesses often involves flexible office coffee subscription models. The larger trend involves office micro-market integration strategies and managing coffee service for fluctuating office attendance.

- Premiumization trends in corporate beverage offerings and the rise of plant-based milk trends in workplace coffee are reshaping supply chains, with some managed services showing over 15% higher adoption in enterprises focused on employee wellness. Ultimately, navigating the challenges of office coffee service logistics while using data analytics for optimizing office coffee supply defines success.

What are the key market drivers leading to the rise in the adoption of Office Coffee Service Industry?

- The increasing corporate emphasis on employee retention and workplace well-being serves as a key driver for the growth of the office coffee service market.

- The primary driver is the strategic use of corporate refreshment solutions as workplace satisfaction tools and employee retention amenities. The adoption of advanced smart brewing systems and bean-to-cup systems is central to delivering the barista-level experiences modern employees expect.

- These systems, often featuring touchless interfaces and mobile application ordering, cater to the demand for hygiene and convenience, with firms seeing a 15% increase in breakroom utilization after upgrading.

- The integration of technology for inventory management provides real-time data, improving restocking efficiency by over 20% compared to manual methods.

- This focus on premium, accessible employee beverage programs, including options like cold brew on tap and nitro infusions, is a direct response to the need to make the physical office an attractive destination.

What are the market trends shaping the Office Coffee Service Industry?

- A defining market trend is the stringent emphasis on sustainability, which increasingly shapes ethical supply chains and corporate procurement decisions for workplace amenities.

- A defining trend is the push for sustainability through fair trade certifications and circular economy principles, which is reshaping office pantry services. The adoption of biodegradable capsules and compostable packaging is becoming standard, with some providers reporting a 30% reduction in plastic waste for clients. This movement complements the rise of integrated pantry solutions and micro-market solutions within corporate environments.

- These unattended retail solutions, featuring self-checkout retail, offer a holistic workplace refreshment experience. This convergence, driven by a desire for turn-key breakroom operations and corporate dining programs, has led to a notable efficiency gain, with some integrated models reducing procurement administration time by up to 25% compared to managing separate vendors.

- Advanced extraction technology further enhances the quality of offerings within these consolidated systems.

What challenges does the Office Coffee Service Industry face during its growth?

- Distribution vulnerabilities within the global agricultural supply chain and significant volatility in raw material pricing present a key challenge affecting industry growth and profitability.

- A significant challenge is the high cost of asset management, particularly for sophisticated hardware like commercial coffee brewers, office espresso machines, and dual milk frothing units. The capital outlay for these systems, coupled with ongoing maintenance for features like automated cleaning cycles, puts pressure on providers.

- Many clients are shifting to pay-per-consumption billing to manage fluctuating office attendance, which can destabilize revenue for providers. This model requires precise tracking, a burden that increases operational costs by an estimated 10% to 15%. Furthermore, the demand for a wide array of options, including single-serve espresso systems and diverse plant-based dairy alternatives, complicates beverage distribution services.

- These complexities, typical of commercial hospitality sectors, require providers to function more like managers of diverse commercial kitchen appliances than simple suppliers, creating a barrier for smaller operators.

Exclusive Technavio Analysis on Customer Landscape

The office coffee service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the office coffee service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Office Coffee Service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, office coffee service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Dining Creations - Key offerings include comprehensive workplace refreshment solutions, integrating premium beverage programs with breakroom management and customized corporate pantry services to enhance employee satisfaction and productivity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Dining Creations

- Aramark

- AVS Companies

- Bodecker

- Bunn O Matic Corp.

- Compass Group

- Evoca S.p.A.

- Farmer Bros Co.

- Hamilton Beach Brands Holding

- JACOBS DOUWE EGBERTS B.V.

- Keurig Green Mountain Inc.

- Luigi Lavazza SPA.

- Nestle SA

- Royal Cup Inc.

- Selecta Group BV

- Sodexo SA

- Starbucks Corp.

- Strauss Coffee BV

- Westrock Coffee Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Office coffee service market

- In August 2024, Keurig Dr Pepper announced the acquisition of JDE Peets, a transformative move designed to consolidate operations and expand its geographic reach across North America and international territories.

- In October 2024, Franke Coffee Systems launched a fully automatic coffee machine featuring advanced extraction technology and an integrated milk foam system, designed specifically for high-volume commercial environments and office spaces.

- In December 2024, Sodexo expanded its Aspretto signature coffee concept across corporate dining and pantry programs in India, responding to the rising demand for premium workplace brews in the rapidly growing Asia Pacific market.

- In February 2025, the Saudi Coffee Company formed a strategic partnership with Shahia Food Company to integrate specialized training academy programs into commercial networks, aiming to elevate barista standards across corporate settings in the Middle East.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Office Coffee Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.3% |

| Market growth 2026-2030 | USD 4940.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global office coffee service market 2026-2030 is characterized by a significant shift toward premiumization and integrated corporate wellness initiatives. The deployment of sophisticated commercial-grade machines, including bean-to-cup systems and high-volume dispense units, is now standard as employers seek to replicate high-street cafe experiences.

- This evolution is supported by flexible equipment leasing programs and managed service contracts that incorporate preventative maintenance and data-driven logistics. A critical boardroom-level consideration is aligning with sustainability mandates through ethical sourcing, fair trade certifications, and circular economy principles using biodegradable capsules and compostable packaging.

- In fact, the market for coffee itself is forecasted to be more than double the size of associated products by 2025, underscoring the focus on the core beverage.

- Success hinges on leveraging smart brewing systems with telemetry capabilities for efficient inventory management and offering diverse options like cold brew on tap, nitro infusions, and plant-based dairy alternatives through integrated pantry and micro-market solutions that utilize self-checkout retail and subscription frameworks, often with touchless interfaces and mobile application ordering and automated cleaning cycles on commercial coffee brewers, office espresso machines and dual milk frothing units.

What are the Key Data Covered in this Office Coffee Service Market Research and Growth Report?

-

What is the expected growth of the Office Coffee Service Market between 2026 and 2030?

-

USD 4.94 billion, at a CAGR of 12.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Coffee, and Associated products), End-user (Large enterprises, and SMEs), Service Type (Subscription based, One time purchase, Managed services, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing corporate emphasis on employee retention and workplace well-being, Distribution vulnerabilities and agricultural volatility

-

-

Who are the major players in the Office Coffee Service Market?

-

American Dining Creations, Aramark, AVS Companies, Bodecker, Bunn O Matic Corp., Compass Group, Evoca S.p.A., Farmer Bros Co., Hamilton Beach Brands Holding, JACOBS DOUWE EGBERTS B.V., Keurig Green Mountain Inc., Luigi Lavazza SPA., Nestle SA, Royal Cup Inc., Selecta Group BV, Sodexo SA, Starbucks Corp., Strauss Coffee BV and Westrock Coffee Co.

-

Market Research Insights

- The market's dynamic nature is shaped by the demand for sophisticated workplace beverage programs and corporate refreshment solutions that serve as critical employee retention amenities. Providers offering integrated facility services are gaining traction over single-source procurement models, as clients seek holistic breakroom management.

- Adoption of these comprehensive services is growing, with regions like North America showing a year-over-year growth rate of 12.7%, notably higher than the 11.7% seen in APAC. This indicates a stronger push for premiumization in mature markets.

- Furthermore, the emphasis on hybrid work model amenities is compelling operators to deliver on-demand beverage quality, with technology like touchless coffee dispensing becoming a key differentiator. The ability to enhance corporate culture through superior amenities is a core value proposition driving investment in this sector.

We can help! Our analysts can customize this office coffee service market research report to meet your requirements.

RIA -

RIA -