Oligonucleotide Therapeutics Market Size 2024-2028

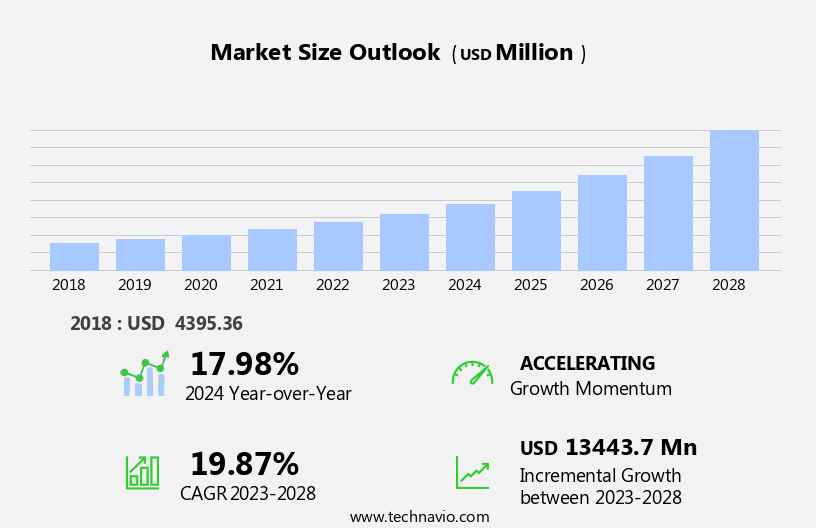

The oligonucleotide therapeutics market size is forecast to increase by USD 13.44 billion at a CAGR of 19.87% between 2023 and 2028.

What will be the Size of the Oligonucleotide Therapeutics Market During the Forecast Period?

How is this Oligonucleotide Therapeutics Industry segmented and which is the largest segment?

The oligonucleotide therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Antisense oligonucleotides

- RNA interference

- Aptamers and others

- Application

- Neurological

- Cancer

- Infectious diseases and others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- Japan

- Rest of World (ROW)

- North America

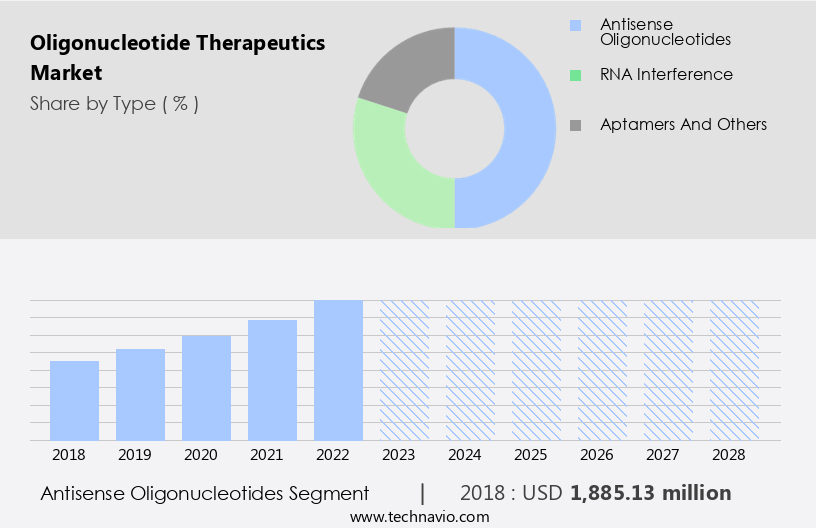

By Type Insights

- The antisense oligonucleotides segment is estimated to witness significant growth during the forecast period.

Oligonucleotide therapeutics, which include antisense RNA, RNAi, miRNA, aptamers, CpG/immunostimulatory, and RNA vaccines, have emerged as promising therapeutic agents for treating various diseases, such as genetic disorders, cancer, neurodegenerative disorders, cardiovascular diseases, and kidney diseases. The advancements in biomedical science and pharmaceutical research, particularly In the areas of gene expression and RNA targets, have fueled the growth of this market. The shift towards precision medicine and personalized therapies has further increased the demand for oligonucleotide therapeutics, as they offer the potential for targeted therapies with minimal off-target effects. The expanding pipeline of ASO-based drugs in clinical development, including those for treating ATTR, hepatic VOD, and cancer, is driving the demand for oligonucleotide therapeutics services.

The healthcare reforms and increasing healthcare expenditure are also contributing to the growth of this market. Oligonucleotide therapeutics offer a new approach to treating diseases by targeting specific genes and biological processes, making them an attractive option for pharmaceutical firms and researchers In the biotechnology industry.

Get a glance at the Oligonucleotide Therapeutics Industry report of share of various segments Request Free Sample

The Antisense oligonucleotides segment was valued at USD 1.89 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

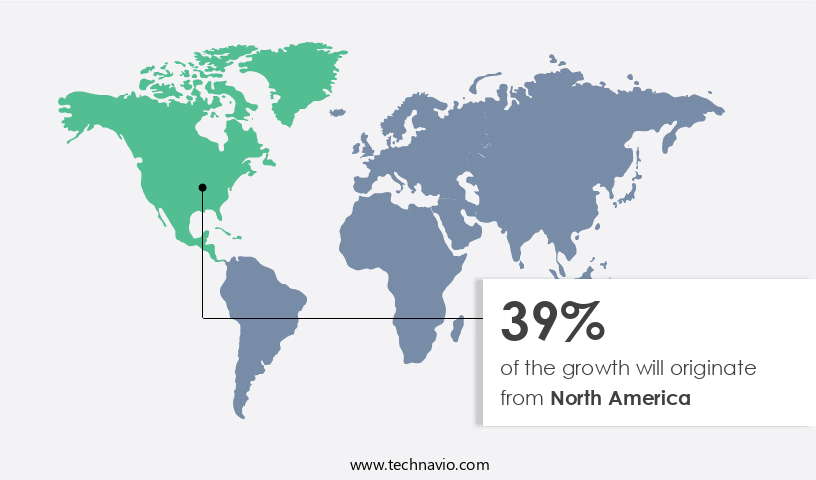

- North America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for oligonucleotide therapeutics is expected to lead due to advanced healthcare systems In the US and Canada, accommodating a significant disease burden. The region's dominance is primarily driven by substantial investments in healthcare research and testing, with key contributors being the National Institute of Health and other funding agencies In the US. Oligonucleotide therapeutics, including Antisense RNA, RNAi treatments, miRNA, CpG/Immunostimulatory, and RNA vaccines, are revolutionizing biomedical science by targeting specific genes and biological processes related to various disorders such as Infectious Diseases, Oncology, Neurodegenerative Disorders, Cardiovascular Diseases, and Kidney Diseases. These therapies offer precision medicine approaches to treat disorders at their root cause.

Key applications include detecting minor antibodies and addressing rare genetic disorders like ATTR and Hepatic VOD. Pharmaceutical firms are increasingly investing in RNA-based therapeutic techniques, such as CRISPR-Cas9, to expand their portfolios and cater to the growing demand.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Oligonucleotide Therapeutics Industry?

Increasing incidence of cancer boosts demand for novel diagnostics is the key driver of the market.

What are the market trends shaping the Oligonucleotide Therapeutics Industry?

Advances in DNA sequencing increasing adoption of microfluidic techniques is the upcoming market trend.

What challenges does the Oligonucleotide Therapeutics Industry face during its growth?

Inherent issues associated with oligonucleotide therapies is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The oligonucleotide therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the oligonucleotide therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, oligonucleotide therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Agilent Technologies Inc. - The Agilent synthetic oligonucleotides platform provides access to a range of oligonucleotide therapeutics, including antisense oligonucleotides (ASOs) and small interfering RNAs (siRNAs). These therapeutics leverage the specificity of nucleic acid sequences to modulate gene expression or RNA function, offering potential treatments for various diseases. Agilent's platform ensures the highest quality and accuracy in oligonucleotide synthesis, enabling effective digital analysis for therapeutic applications. By harnessing the power of oligonucleotide technology, the company is at the forefront of advancing innovative therapeutic solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies Inc.

- Alnylam Pharmaceuticals Inc.

- Biogen Inc.

- CSL Ltd.

- GlaxoSmithKline Plc

- Ionis Pharmaceuticals Inc.

- Maravai LifeSciences Holdings Inc.

- Merck KGaA

- Nippon Shinyaku Co. Ltd.

- Novartis AG

- Pfizer Inc.

- Sarepta Therapeutics Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Oligonucleotide therapeutics represent a burgeoning field In the realm of pharmaceutical research, offering innovative solutions for addressing various disorders and diseases. These therapeutics, which include antisense RNA, RNAi treatments, aptamers, and RNA-based vaccines, harness the power of nucleotides to manipulate gene expression and biological processes. Antisense RNA and RNAi treatments represent two primary classes of oligonucleotide therapeutics. Antisense RNA functions by binding to specific mRNA sequences, thereby inhibiting their translation into proteins. RNAi treatments, on the other hand, utilize small RNA molecules to degrade specific mRNAs. Both approaches offer potential for treating a range of disorders, including infectious diseases, neurodegenerative disorders, oncology, cardiovascular diseases, and kidney diseases.

Another class of oligonucleotide therapeutics includes aptamers, which are short, single-stranded RNA or DNA molecules that can bind to specific targets with high affinity and specificity. Aptamers have shown promise in detecting minor antibodies and can be used as therapeutic agents in various applications. MicroRNAs (miRNAs) represent another category of RNA-based therapeutic techniques. MiRNAs are small non-coding RNAs that regulate gene expression by binding to specific mRNAs. MiRNAs have been implicated in various biological processes and offer potential for treating a range of disorders, including cancer, neurological diseases, and cardiovascular diseases. The development of oligonucleotide therapeutics is driven by advancements in biomedical science and biotechnology.

Pharmaceutical firms are investing heavily in research and development of these therapeutics, driven by the potential for precision medicine and the ability to target specific genetic disorders. The application of CRISPR-Cas9 technology, a revolutionary gene-editing tool, has further expanded the potential of oligonucleotide therapeutics. This technology allows for precise modification of DNA sequences, offering potential for treating a wide range of genetic disorders. Despite the promising potential of oligonucleotide therapeutics, there are challenges to their development and commercialization. These challenges include the high cost of production, the need for specific delivery systems, and the potential for off-target effects.

In conclusion, oligonucleotide therapeutics represent a promising field in pharmaceutical research, offering innovative solutions for addressing various disorders and diseases. These therapeutics, which include antisense RNA, RNAi treatments, aptamers, and RNA-based vaccines, harness the power of nucleotides to manipulate gene expression and biological processes. The development of these therapeutics is driven by advancements in biomedical science and biotechnology, and offers potential for precision medicine and the treatment of a wide range of disorders. However, challenges remain, including the high cost of production, the need for specific delivery systems, and the potential for off-target effects.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 19.87% |

|

Market growth 2024-2028 |

USD 13443.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.98 |

|

Key countries |

US, Canada, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Oligonucleotide Therapeutics Market Research and Growth Report?

- CAGR of the Oligonucleotide Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the oligonucleotide therapeutics market growth of industry companies

We can help! Our analysts can customize this oligonucleotide therapeutics market research report to meet your requirements.

RIA -

RIA -