Optical Transport Network Equipment Market Size 2026-2030

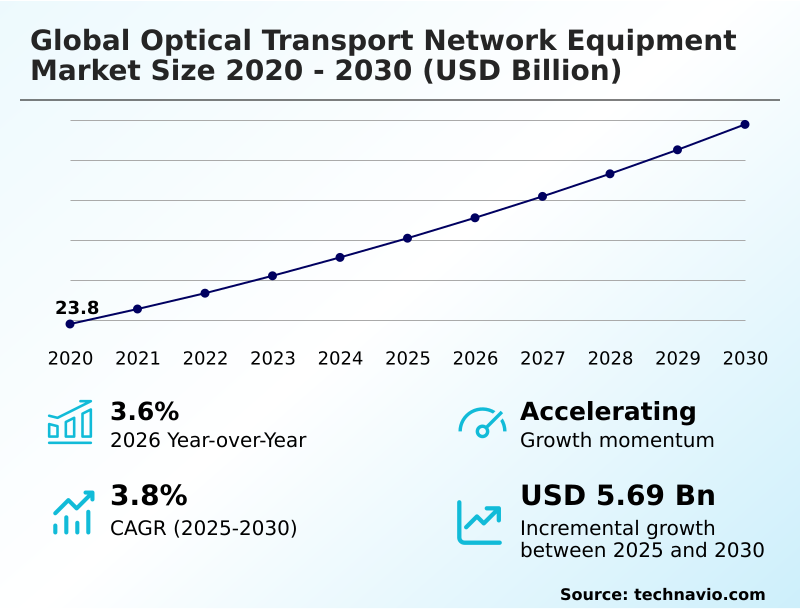

The optical transport network equipment market size is valued to increase by USD 5.69 billion, at a CAGR of 3.8% from 2025 to 2030. Exponential data traffic growth acceleration will drive the optical transport network equipment market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 35% growth during the forecast period.

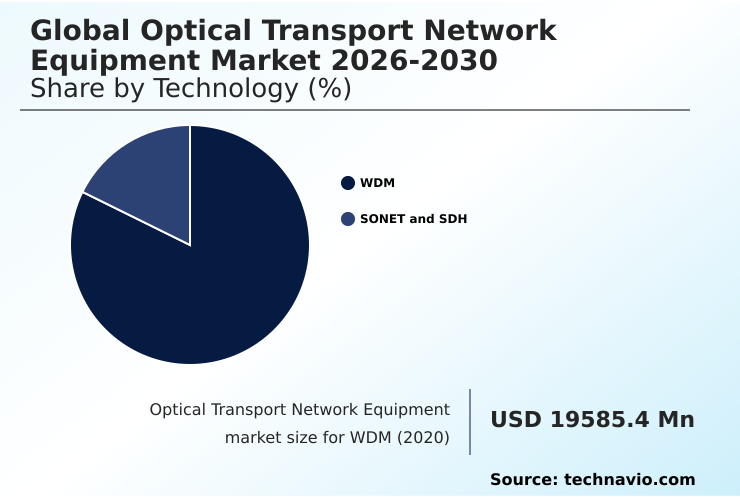

- By Technology - WDM segment was valued at USD 22.61 billion in 2024

- By End-user - Communication service providers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.98 billion

- Market Future Opportunities: USD 5.69 billion

- CAGR from 2025 to 2030 : 3.8%

Market Summary

- The optical transport network equipment market is the foundational layer of modern digital communication, enabling the high-capacity data transmission required by telecommunications carriers, cloud providers, and enterprises. This market revolves around specialized hardware and software, including systems for wavelength division multiplexing, which dramatically increases the capacity of fiber optic infrastructure.

- Key components like the optical transponder and reconfigurable optical add-drop multiplexer manage the flow of data, while advanced technologies such as terabit coherent optical technology and probabilistic constellation shaping push the boundaries of performance. The relentless growth in data traffic, fueled by bandwidth-intensive applications and the expansion of 5G, drives continuous innovation.

- Architectural shifts toward IP-optical convergence and open and disaggregated optical networking are transforming deployment models, offering greater flexibility. Concurrently, the integration of AI-driven network automation is becoming crucial for managing network complexity, optimizing end-to-end network performance, and enabling capabilities like predictive network maintenance.

- This evolution ensures that the underlying infrastructure can support future demands from both consumer and industrial applications, making it a critical area of investment for digital transformation.

What will be the Size of the Optical Transport Network Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Optical Transport Network Equipment Market Segmented?

The optical transport network equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

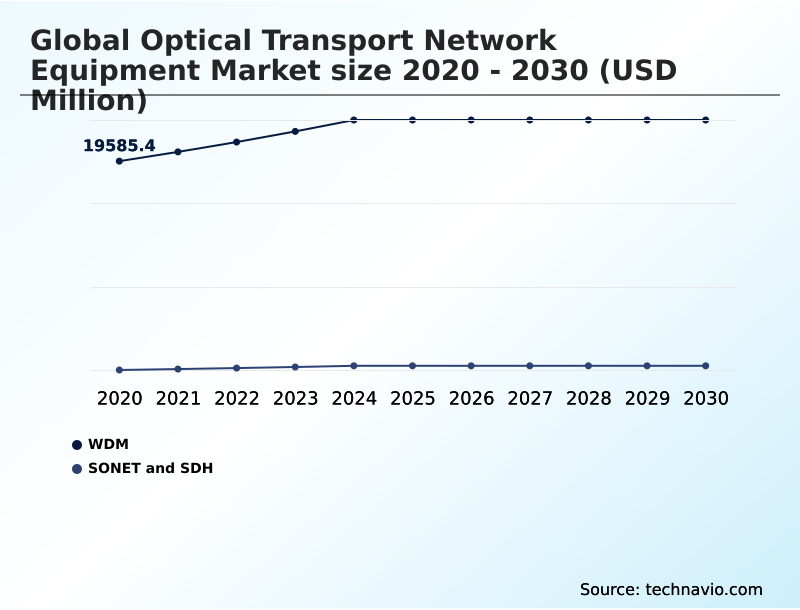

- Technology

- WDM

- SONET and SDH

- End-user

- Communication service providers

- Enterprises

- Public sector

- Others

- Component

- Hardware

- Services

- Software

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Technology Insights

The wdm segment is estimated to witness significant growth during the forecast period.

The optical transport network market is primarily defined by technology, with wavelength division multiplexing (WDM) being the dominant segment.

This technology, particularly dense wavelength division multiplexing, enables the transmission of multiple data streams over a single fiber using distinct optical wavelength assignments.

This method is essential for network capacity expansion to support growing IP traffic management needs from bandwidth-intensive applications and digital transformation initiatives.

Systems for optical channel monitoring are critical for managing these complex networks, ensuring low-latency data transmission across terrestrial fiber networks and long-haul backbone networks.

Advanced platforms now achieve superior spectral efficiency maximization, with industry reports showing that global internet bandwidth grew 23% in 2024, driving the need for continuous innovation in WDM for cloud service delivery.

The WDM segment was valued at USD 22.61 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Optical Transport Network Equipment Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the optical transport network market is diverse, with APAC leading as the largest region, contributing to 35% of incremental growth. North America remains a key market, driven by hyperscale data center expansion.

In Europe, a focus on energy-efficient networking and the modernization of legacy systems, including older SONET and SDH infrastructure, drives investment.

Across all regions, operators are deploying advanced hardware like the reconfigurable optical add-drop multiplexer and systems with sophisticated optical amplification using erbium-doped fiber amplifiers. Modern platforms use enhanced forward error correction and adaptive modulation algorithms for efficiency.

Geopolitical considerations and the need for quantum-safe encryption are increasingly influencing procurement decisions and strategies for intelligent capacity planning.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the optical transport network equipment market is increasingly nuanced, focusing on specific use cases and technological trade-offs. The debate over coherent pluggable optics vs transponders highlights a pivotal shift, with pluggables favored for their economic and operational benefits in metro networks.

- The growing adoption of 800G coherent pluggable optics applications, especially for optical transport for AI training clusters, underscores the demand for high-density, low-latency connectivity. Exploring the disaggregated optical networking cost benefits is now a standard practice for operators seeking to avoid vendor lock-in, though it raises challenges in managing multi-vendor optical networks and testing optical network interoperability.

- The role of AI in optical network fault prediction is transitioning from a concept to a core operational tool, crucial for maintaining service level agreements. For mobile infrastructure, designing effective optical transport for 5G fronthaul is critical for enabling advanced 5G services.

- In data centers, data center interconnect latency optimization and the implementation of IP-optical convergence network architecture are top priorities. Automation, particularly through software-defined optical network management and automating optical service provisioning workflows, is essential for operational efficiency. Operators are also addressing sustainability by analyzing the power consumption in optical networks and reinforcing security through optical network security best practices.

- For infrastructure planning, developing effective submarine cable capacity upgrade strategies and flexible grid WDM network design are key, alongside roadmaps for upgrading legacy SONET and SDH networks.

- These focused strategies demonstrate a market maturity where optimizing the ROI of open optical networking is a primary goal, with some disaggregated models showing a total cost of ownership reduction of over 20% compared to traditional architectures.

What are the key market drivers leading to the rise in the adoption of Optical Transport Network Equipment Industry?

- The exponential acceleration of data traffic, driven by bandwidth-intensive applications and cloud services, is a primary driver for market growth.

- Market drivers are centered on escalating bandwidth demand. The expansion of data center interconnection is a primary factor, with hyperscaler purchases increasing 45% in late 2024 to support cloud computing workloads and emerging generative AI workloads.

- The global deployment of 5G infrastructure is another critical driver, demanding robust optical backhaul solutions and high-capacity optical fronthaul connectivity for 5G radio access network support.

- This requires sophisticated packet optical transport systems across both metro optical infrastructure and submarine cable systems. The push for IP-optical convergence and network slicing enablement further fuels demand for advanced equipment that provides low-latency data transmission essential for next-generation services.

What are the market trends shaping the Optical Transport Network Equipment Industry?

- A primary trend influencing the market is the accelerating adoption of coherent pluggable optics. This architectural shift enables direct integration of advanced transmission capabilities into routing and switching equipment.

- Evolving architectural trends are reshaping the market, led by the adoption of coherent pluggable optics in compact formats like the QSFP-DD form factor. This shift toward 400ZR coherent modules and 800ZR coherent modules facilitates total cost of ownership reduction. Concurrently, open and disaggregated optical networking is gaining traction, promoting multi-vendor interoperability.

- The integration of AI-driven network automation enables advanced capabilities such as predictive network maintenance and automated service provisioning, with some deployments improving network utilization efficiency by 31%. Furthermore, software-defined optical networking and real-time traffic engineering allow for dynamic control, enhancing end-to-end network performance and reducing service provisioning times from days to hours.

What challenges does the Optical Transport Network Equipment Industry face during its growth?

- A key challenge affecting industry growth is the persistent constraints and dependencies within the component supply chain.

- The market faces significant headwinds, primarily from component supply chain constraints and pricing pressure dynamics. Critical subsystems relying on indium phosphide components and advanced photonic integrated circuit designs experienced lead times extending up to 52 weeks. The limited availability of the coherent digital signal processor and challenges in silicon photonics integration create bottlenecks.

- Concurrently, increasing technical complexity challenges and skills shortage obstacles hinder deployment and maintenance, complicating efforts toward mean time to repair reduction. While operators desire procurement flexibility, the need for specialized expertise for remote infrastructure management, network function virtualization, and cybersecurity threat detection adds to operational costs, with some estimates suggesting a need for 180,000 new technicians in the US alone.

Exclusive Technavio Analysis on Customer Landscape

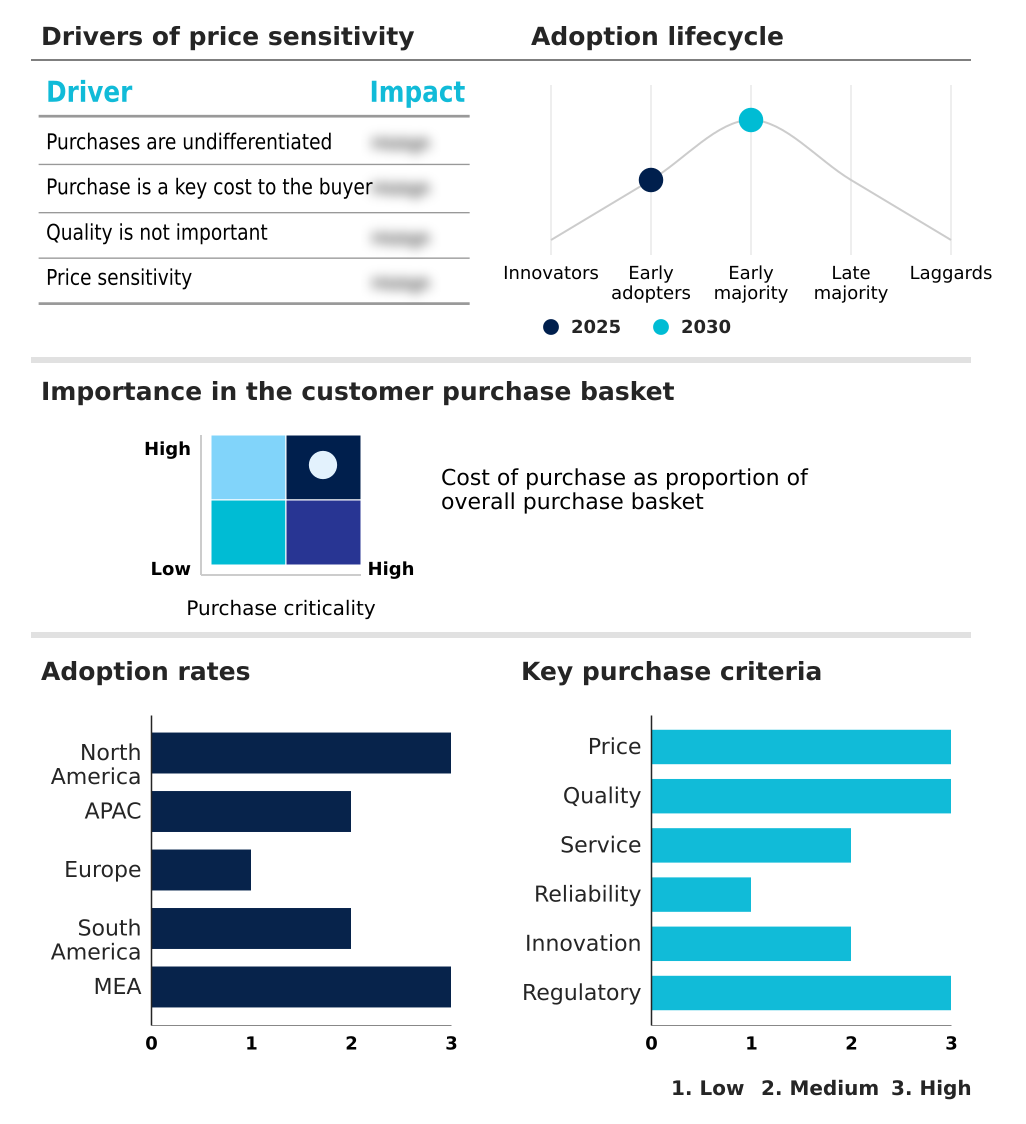

The optical transport network equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the optical transport network equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Optical Transport Network Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, optical transport network equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adtran Holdings Inc. - Key offerings include high-capacity optical transmission hardware, advanced network management software, and integrated systems designed to scale modern digital infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adtran Holdings Inc.

- Aliathon Technology

- Ciena Corp.

- Cisco Systems Inc.

- Deutsche Telekom AG

- Ekinops SA

- FiberHome

- Fujitsu Ltd.

- Huawei Technologies Co. Ltd.

- Infinera Corp.

- Juniper Networks Inc.

- Mitsubishi Electric Corp.

- NEC Corp.

- Padtec Holding S.A.

- Ribbon Communications Inc.

- Tejas Network Ltd.

- Telefonaktiebolaget Ericsson

- Yokogawa Electric Corp.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Optical transport network equipment market

- In November 2024, Nokia announced the integration of Infinera's coherent pluggable technologies into its portfolio, demonstrating a unified roadmap targeting 1.6 terabit solutions post-acquisition.

- In January 2025, Ciena Corp. reported new deployments of its coherent pluggable optics with neoscaler companies, which are leveraging the technology to build high-capacity optical links for AI infrastructure connecting distributed GPU clusters.

- In March 2025, Alibaba Cloud announced a significant expansion of its infrastructure in Southeast Asia, deploying new availability zones that rely on high-capacity optical transport for integration into its global network.

- In May 2025, IBM Cloud revealed enhancements to its hybrid cloud offerings, introducing advanced connectivity options that utilize high-bandwidth optical networking to ensure seamless interconnection between on-premises and cloud data centers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Optical Transport Network Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 339 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.8% |

| Market growth 2026-2030 | USD 5687.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.6% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The optical transport network equipment market is undergoing a significant architectural evolution driven by insatiable bandwidth demand. Core technologies like wavelength division multiplexing and its high-capacity variant, dense wavelength division multiplexing, remain fundamental to scaling fiber optic infrastructure.

- The innovation focus has shifted to the component level, with coherent pluggable optics in QSFP-DD form factor and OSFP configurations revolutionizing data center interconnection. These modules, leveraging advanced photonic integrated circuit designs with silicon photonics integration and indium phosphide components, are displacing traditional optical transponder systems.

- Inside, the coherent digital signal processor enables complex techniques like probabilistic constellation shaping and robust forward error correction. For network management, software-defined optical networking and IP-optical convergence are key, supported by hardware such as the reconfigurable optical add-drop multiplexer and optical switching matrix.

- This ecosystem, which includes the optical line system, ensures efficient optical amplification and management of each optical wavelength. This transition facilitates new deployment models like packet optical transport and robust optical backhaul solutions for 5G, while also managing the migration from legacy SONET and SDH systems.

- Some carriers have leveraged these advancements to reduce service provisioning times from days to mere hours.

What are the Key Data Covered in this Optical Transport Network Equipment Market Research and Growth Report?

-

What is the expected growth of the Optical Transport Network Equipment Market between 2026 and 2030?

-

USD 5.69 billion, at a CAGR of 3.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (WDM, and SONET and SDH), End-user (Communication service providers, Enterprises, Public sector, and Others), Component (Hardware, Services, and Software) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential data traffic growth acceleration, Component supply chain constraints and dependencies

-

-

Who are the major players in the Optical Transport Network Equipment Market?

-

Adtran Holdings Inc., Aliathon Technology, Ciena Corp., Cisco Systems Inc., Deutsche Telekom AG, Ekinops SA, FiberHome, Fujitsu Ltd., Huawei Technologies Co. Ltd., Infinera Corp., Juniper Networks Inc., Mitsubishi Electric Corp., NEC Corp., Padtec Holding S.A., Ribbon Communications Inc., Tejas Network Ltd., Telefonaktiebolaget Ericsson, Yokogawa Electric Corp. and ZTE Corp.

-

Market Research Insights

- Market dynamics are shaped by a confluence of technological innovation and operational imperatives. The shift toward AI-driven network automation and predictive network maintenance is paramount, with some operators achieving a 31% improvement in network utilization. The adoption of open and disaggregated optical networking enhances multi-vendor interoperability, while data center interconnection demands optimized low-latency data transmission to support cloud computing workloads.

- Advanced multi-layer network orchestration enables automated service provisioning and real-time traffic engineering for network slicing enablement. This focus on efficiency drives total cost of ownership reduction and supports network capacity expansion for 5G radio access network support.

- As digital transformation initiatives accelerate, the emphasis on cybersecurity threat detection, energy-efficient networking, and quantum-safe encryption is intensifying, influencing both technology and investment strategies.

We can help! Our analysts can customize this optical transport network equipment market research report to meet your requirements.

RIA -

RIA -