Orthopedic Surgical Navigation Systems Market Size 2024-2028

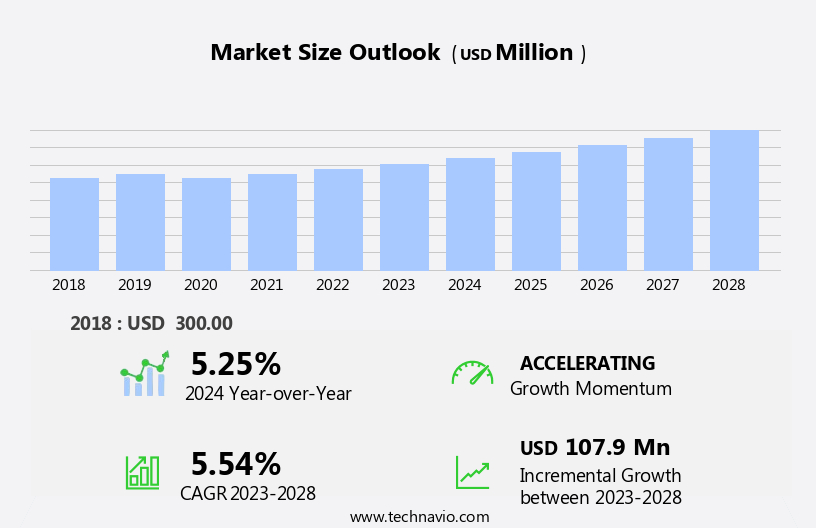

The orthopedic surgical navigation systems market size is forecast to increase by USD 107.9 million, at a CAGR of 5.54% between 2023 and 2028.

- The market is driven by the high prevalence of osteoporosis, a condition that increases the need for orthopedic surgical procedures. This trend is further fueled by the growing preference for minimally invasive surgeries, which rely on navigation systems for enhanced accuracy and precision. A significant shift from frame-based stereotaxic to frameless stereotaxic navigation systems is underway, offering advantages such as reduced invasiveness and improved patient comfort. However, the high cost of surgical navigation systems remains a notable challenge, potentially limiting market growth.

- Manufacturers must focus on developing cost-effective solutions while maintaining the necessary accuracy and precision to cater to the evolving demands of the market. Companies that successfully navigate these challenges and provide innovative, cost-effective navigation systems will be well-positioned to capitalize on the growing need for orthopedic surgical procedures.

What will be the Size of the Orthopedic Surgical Navigation Systems Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The orthopedic surgical navigation market continues to evolve, driven by advancements in technology and the increasing demand for more precise and efficient surgical procedures. Patient-specific instrumentation and implant placement accuracy are key benefits of these systems, enabling surgeons to tailor treatments to individual patients and improve surgical outcomes. Virtual reality simulation and 3D anatomical modeling offer surgeons the ability to plan procedures in detail before entering the operating room, reducing operative time and enhancing surgical workflow efficiency. Real-time feedback systems provide surgeons with critical information during procedures, allowing for adjustments to be made in real-time and reducing the risk of surgical errors.

Haptic feedback systems add a tactile dimension to these systems, enhancing the surgical experience and improving precision. Augmented reality overlay and optical tracking sensors provide surgeons with a clear view of the surgical site, enabling them to navigate complex anatomical structures with ease. Computer-assisted surgery and intraoperative guidance are becoming increasingly common in various sectors, including pediatric orthopedic surgery, spine surgery, joint replacement surgery, and trauma surgery. The integration of surgical robotics and advanced imaging techniques, such as image registration algorithms and image fusion, further enhances the capabilities of these systems. Soft tissue visualization and preoperative planning software are also gaining popularity, expanding the applications of orthopedic surgical navigation systems beyond bone procedures.

The ongoing development of these systems is expected to continue, with a focus on improving patient outcomes, reducing operative time, and enhancing surgical precision. The integration of artificial intelligence and machine learning algorithms is also expected to play a significant role in the future of orthopedic surgical navigation systems.

How is this Orthopedic Surgical Navigation Systems Industry segmented?

The orthopedic surgical navigation systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

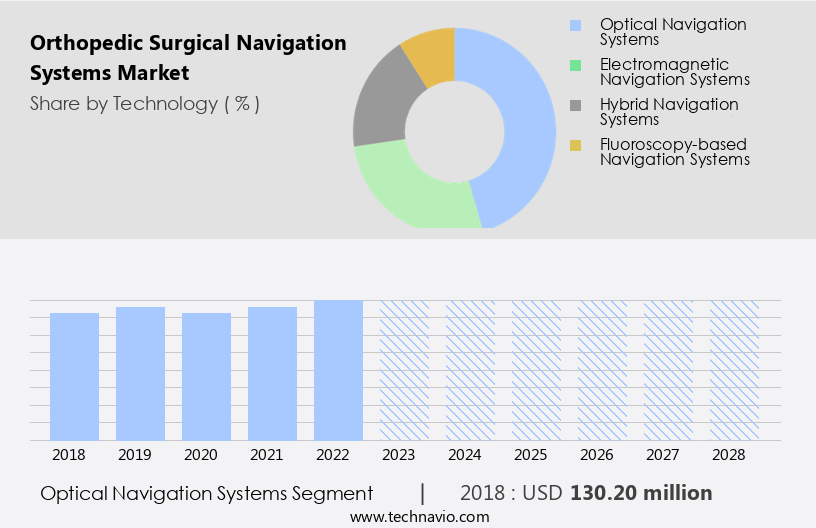

- Technology

- Optical navigation systems

- Electromagnetic navigation systems

- Hybrid navigation systems

- Fluoroscopy-based navigation systems

- End-user

- Hospitals

- ASCs

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- Rest of World (ROW)

- North America

By Technology Insights

The optical navigation systems segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant advancements, with optical navigation systems leading the technology landscape in 2023. This technology utilizes a 3D camera to provide real-time information to surgeons, ensuring precise orientation and minimizing postoperative complications. Optical tracking sensors play a crucial role in this system, enabling accurate instrument tracking and patient-specific instrumentation for implant placement. Pediatric orthopedic surgery and spine surgery navigation have also gained prominence, with augmented reality overlays and virtual reality simulation enhancing surgical accuracy and workflow efficiency. Haptic feedback systems offer improved surgical outcomes by providing tactile sensation during minimally invasive surgeries, while surgical robot integration streamlines complex procedures.

Intraoperative guidance and computer-assisted surgery enable real-time feedback systems, reducing operative time and surgical errors. Image registration algorithms and fusion techniques facilitate bone deformity correction and joint replacement surgery. Soft tissue visualization and preoperative planning software further optimize surgical workflows. Electromagnetic tracking and arthroscopic surgery guidance, along with sensor calibration methods, ensure surgical precision. Overall, the market continues to evolve, focusing on enhancing surgical accuracy, reducing operative time, and improving patient outcomes.

The Optical navigation systems segment was valued at USD 130.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

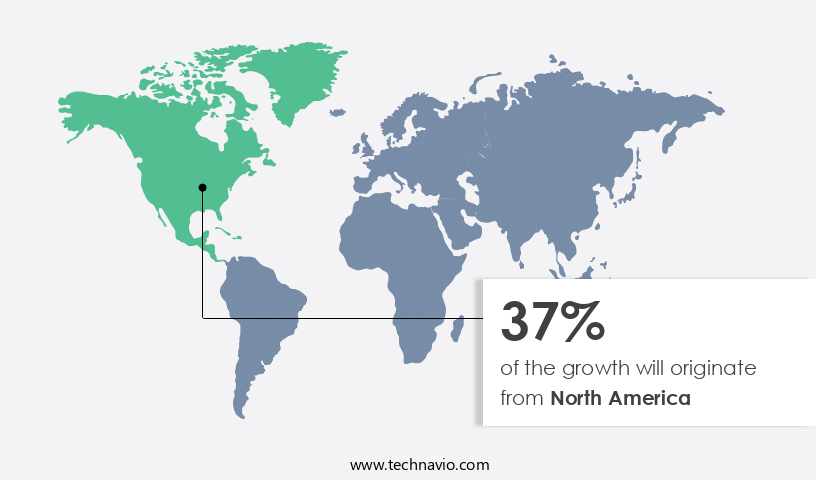

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America, with the US as the largest contributor, is experiencing significant growth due to the increasing volume of orthopedic surgeries. Advanced technology is driving the shift from frame-based stereotaxic navigation systems to frameless stereotaxic systems, offering benefits such as minimally invasive surgery, bone fracture reduction, haptic feedback systems, and pediatric orthopedic surgery. Augmented reality overlays, optical tracking sensors, and surgical navigation accuracy are essential components of these systems, ensuring improved surgical outcomes and real-time feedback. Intraoperative guidance systems, including computer-assisted surgery and spine surgery navigation, are essential for surgical workflow efficiency and soft tissue visualization.

Sensor calibration methods and image registration algorithms enable accurate implant placement and bone deformity correction. The integration of surgical robotics and arthroscopic surgery guidance further enhances the system's capabilities. Despite these advancements, the US Food and Drug Administration (FDA) has raised concerns regarding accuracy issues with frameless stereotaxic navigation systems and emphasizes the importance of continuous system accuracy assessments. However, FDA approvals for innovative surgical navigation technologies are fueling market growth, particularly in the US. Three-dimensional anatomical modeling, patient-specific instrumentation, and virtual reality simulation are transforming preoperative planning and postoperative recovery processes. Image fusion techniques and electromagnetic tracking methods further expand the system's capabilities, enabling surgeons to achieve surgical error reduction and optimal surgical outcomes.

Joint replacement surgery and trauma surgery navigation are significant applications of these advanced systems.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing adoption of advanced technologies that enhance surgical precision and improve patient outcomes. Orthopedic navigation systems utilize image registration, haptic feedback, and 3D modeling software to provide real-time guidance during orthopedic procedures. Image registration technology ensures accurate alignment of pre-operative images with the patient's anatomy, while haptic feedback provides tactile sensation to the surgeon, enhancing surgical precision. 3D modeling software finds extensive applications in orthopedic surgery, enabling surgeons to plan and execute complex procedures with greater accuracy. Computer-assisted surgery workflows have become more efficient with the integration of minimally invasive orthopedic navigation systems, which allow for smaller incisions and reduced trauma to the patient. Surgical robots have also been integrated into orthopedic procedures, providing enhanced precision and accuracy, especially during joint replacement surgeries. Virtual reality simulation and augmented reality overlay technologies offer orthopedic trainees an immersive learning experience, enabling them to gain expertise in complex procedures. Patient-specific instrumentation is another key application of orthopedic navigation systems, allowing for customized implant placement and improved surgical outcomes. Navigation systems have shown effectiveness in various orthopedic surgeries, including spine, trauma, pediatric, arthroscopic, and bone deformity correction procedures. Image fusion techniques and real-time feedback systems further enhance the capabilities of orthopedic navigation systems, providing surgeons with a comprehensive view of the surgical site and enabling them to make informed decisions in real-time. The adoption of these advanced technologies is expected to continue driving growth in the market.

What are the key market drivers leading to the rise in the adoption of Orthopedic Surgical Navigation Systems Industry?

- The high prevalence of osteoporosis serves as the primary market driver, given its significant impact on healthcare expenditures and the growing demand for effective treatments.

- Osteoporosis, a disease characterized by the gradual loss of bone density, affects millions of adults in the US each year, resulting in an estimated 1-3 million osteoporosis-related fractures annually. These fractures, most commonly occurring in the spine, hip, and wrist, can lead to significant pain, disability, and increased healthcare costs. To address the challenges of treating osteoporosis-related fractures, orthopedic surgical navigation systems have emerged as a promising solution. These advanced systems utilize technologies such as minimally invasive surgery, haptic feedback systems, augmented reality overlay, optical tracking sensors, and instrument tracking systems to enhance surgical navigation accuracy. Minimally invasive surgery reduces trauma to the body, while haptic feedback systems provide tactile sensations to surgeons, allowing for precise bone fracture reduction.

- Pediatric orthopedic surgery also benefits from these systems due to their ability to ensure accurate alignment and positioning during procedures. The integration of these technologies results in a more immersive, harmonious surgical experience, emphasizing the importance of precision and accuracy in the treatment of osteoporosis-related fractures.

What are the market trends shaping the Orthopedic Surgical Navigation Systems Industry?

- The transition from frame-based to frameless stereotaxic navigation is an emerging trend in the orthopedic surgery market. This advanced navigation system offers several benefits, including greater precision and flexibility, reduced invasiveness, and improved patient outcomes.

- Stereotaxic navigation systems play a crucial role in orthopedic surgeries, particularly in procedures that require precise implant placement. These systems utilize patient-specific imaging, such as CT and MRI, to guide surgeons in real-time during the surgical intervention. The integration of virtual reality simulation and 3D anatomical modeling enhances the accuracy and harmonious execution of implant placement. The implementation of stereotaxic navigation systems in orthopedic surgeries leads to several benefits, including operative time reduction, improved surgical outcomes, and surgical error reduction. The systems provide real-time feedback systems that allow surgeons to adjust their approach as needed, ensuring optimal implant positioning.

- During the surgical procedure, surgeons use specialized instruments, such as drivers, needles, and cut guides, in conjunction with electromagnetic and optical tracking methods to navigate the targeted site accurately. The use of stereotaxic navigation systems in orthopedic surgeries results in a more immersive and harmonious surgical experience, ultimately leading to better patient outcomes.

What challenges does the Orthopedic Surgical Navigation Systems Industry face during its growth?

- The high cost of surgical navigation systems poses a significant challenge to the growth of the industry. These advanced technologies, which enable precise and accurate surgical interventions, come with a hefty price tag that limits their accessibility and adoption, thereby hindering the expansion of the market.

- Orthopedic surgical navigation systems, which utilize computer-assisted technology for intraoperative guidance during spine surgery and other orthopedic procedures, are currently experiencing significant advancements. These systems incorporate image registration algorithms and fusion techniques to provide surgeons with real-time, three-dimensional visualization of the surgical site. This immersive and harmonious environment enhances accuracy and precision, leading to improved patient outcomes and reduced postoperative recovery time. Despite these benefits, the high purchasing and installation costs associated with these technologically advanced systems pose a significant challenge to market growth. Manufacturers continue to invest heavily in research and development to create devices compatible with the latest technologies, contributing to the high costs.

- Furthermore, the low reimbursement rates for orthopedic surgeries performed using surgical navigation systems hinder market expansion, particularly in developing countries. In conclusion, while the adoption of computer-assisted surgical navigation systems in orthopedics offers numerous advantages, the high costs and limited reimbursement rates present significant barriers to market growth. To address these challenges, ongoing research and development efforts aim to create more cost-effective solutions while maintaining the accuracy and precision that these systems provide.

Exclusive Customer Landscape

The orthopedic surgical navigation systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the orthopedic surgical navigation systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, orthopedic surgical navigation systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amplitude SAS - Aesculap Inc., a subsidiary of the global medical technology leader, provides orthopedic surgical navigation systems. These advanced technologies enhance surgical precision and accuracy during procedures, contributing significantly to improved patient outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amplitude SAS

- B.Braun SE

- Brainlab AG

- Exactech Inc.

- Globus Medical Inc.

- Intellijoint Surgical Inc.

- Johnson and Johnson Services Inc.

- joimax GmbH

- Kinamed Inc.

- Medtronic Plc

- MicroPort Scientific Corp.

- OrthAlign Corp.

- OrthoGrid Systems Inc.

- Orthokey Italia SRL

- Siemens Healthineers AG

- Smith and Nephew plc

- Stryker Corp.

- Toshbro Medicals Pvt. Ltd.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Orthopedic Surgical Navigation Systems Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the U.S. Food and Drug Administration (FDA) clearance for its Mazor X Stealth Edition surgical navigation system. This advanced system combines robotics, imaging, and navigation technology to enhance the precision and accuracy of orthopedic procedures (Medtronic Press Release, 2024).

- In March 2024, Stryker Corporation, a leading medical technology company, entered into a strategic partnership with Brainlab AG, a German medical technology firm, to develop and commercialize advanced orthopedic surgical navigation systems. The collaboration aims to improve surgical outcomes and patient care by integrating Stryker's orthopedic implants with Brainlab's navigation technology (Stryker Press Release, 2024).

- In April 2025, Zimmer Biomet Holdings, Inc., a global leader in musculoskeletal healthcare, completed the acquisition of Medacta International, a European orthopedic implant and instrument manufacturer. The acquisition significantly expanded Zimmer Biomet's orthopedic portfolio and strengthened its position in the European market (Zimmer Biomet Press Release, 2025).

- In May 2025, Smith & Nephew plc, a global medical technology business, received FDA clearance for its Navio Surgical System, an intelligent robotic-assisted navigation platform for total knee arthroplasty. The system uses real-time data to create a personalized surgical plan for each patient, enabling more accurate and efficient procedures (Smith & Nephew Press Release, 2025).

Research Analyst Overview

- Orthopedic surgical navigation systems have gained significant traction in the healthcare industry due to their ability to enhance surgical precision and safety. These systems employ advanced technologies such as virtual reality training, surgical simulation tools, and augmented reality guidance to improve surgical planning and execution. The market is driven by the need for minimally invasive approaches, spine deformity correction, and trauma surgery planning. Surgical complication reduction and recovery time improvement are key benefits, making these systems increasingly popular. Navigation system calibration ensures bone alignment accuracy using sensor data processing and optical tracking technology. Robotic surgical assistance and real-time data analysis further boost surgical precision metrics.

- Pediatric orthopedic care and joint reconstruction also benefit from these innovations. Image-guided surgery and 3D anatomical reconstruction offer enhanced surgical safety, while soft tissue modeling and bone modeling techniques refine surgical workflow optimization. Overall, the market for orthopedic surgical navigation systems continues to evolve, driven by technological advancements and the growing demand for superior patient care.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Orthopedic Surgical Navigation Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.54% |

|

Market growth 2024-2028 |

USD 107.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.25 |

|

Key countries |

US, Germany, UK, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Orthopedic Surgical Navigation Systems Market Research and Growth Report?

- CAGR of the Orthopedic Surgical Navigation Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the orthopedic surgical navigation systems market growth of industry companies

We can help! Our analysts can customize this orthopedic surgical navigation systems market research report to meet your requirements.

RIA -

RIA -