Surgical Navigation Systems Market Size 2024-2028

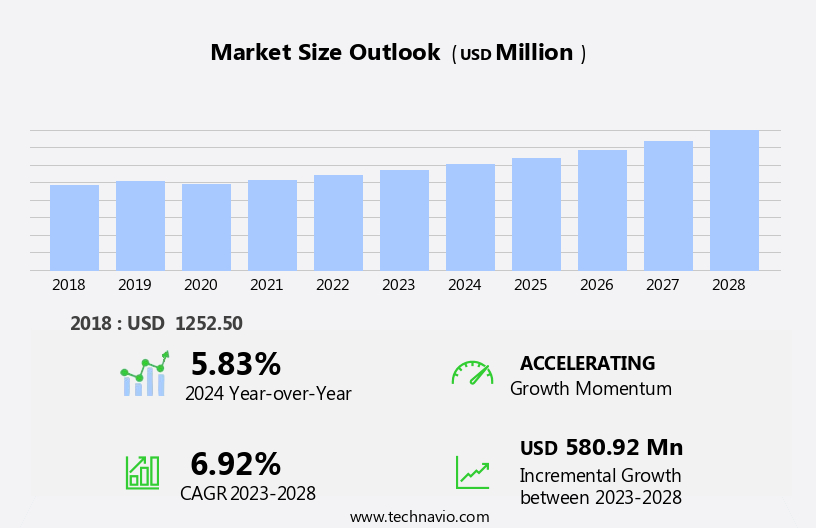

The surgical navigation systems market size is forecast to increase by USD 580.92 million, at a CAGR of 6.92% between 2023 and 2028.

- The market is driven by the high prevalence of cardiovascular diseases (CVD) and ongoing technological advancements. The increasing incidence of CVDs necessitates the use of advanced surgical navigation systems to enhance precision and improve patient outcomes. These systems enable surgeons to visualize and navigate complex anatomies, leading to reduced invasiveness and faster recovery times. However, the high initial cost for acquiring surgical navigation systems poses a significant challenge for market growth. The substantial investment required for purchasing and implementing these systems may deter some healthcare providers, particularly smaller facilities, from adopting them.

- Despite this obstacle, companies can capitalize on the market's potential by focusing on cost-effective solutions, collaborating with healthcare providers to offer flexible financing options, and demonstrating the long-term cost savings and improved patient outcomes associated with surgical navigation systems.

What will be the Size of the Surgical Navigation Systems Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and the increasing demand for precision and minimally invasive procedures. Anatomical modeling and image fusion algorithms play a crucial role in preoperative planning, enabling surgeons to visualize and plan complex surgeries with greater accuracy. Computer-assisted surgery, including neurosurgical navigation and electrode placement guidance, benefits from these tools, ensuring bone registration accuracy and reducing calibration procedures. Surgical workflow efficiency is enhanced through the integration of ultrasound, depth perception enhancement, and computed tomography guidance. Augmented reality overlay and laser guidance systems provide real-time visualization, while intraoperative imaging and instrument tracking offer precise navigation during surgery.

Surgical robotics and virtual reality simulation are gaining popularity, leveraging sensor fusion techniques, fluorescence guidance, and real-time tracking for enhanced precision. Intraoperative imaging and data integration platforms facilitate surgical trajectory planning and error reduction, further improving surgical outcomes. The market dynamics remain continuous and evolving, with ongoing research and development in areas such as tissue deformation compensation, radiation therapy integration, and haptic feedback. These advancements contribute to the growing adoption of surgical navigation systems across various sectors, including orthopedic and neurosurgery.

How is this Surgical Navigation Systems Industry segmented?

The surgical navigation systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Neurology

- Orthopedic

- ENT

- Dental

- Spinal

- Cardiac

- Urology

- Oncology

- Others

- Technology

- Electromagnetic

- Optical

- Hybrid

- Fluoroscopy-Based

- CT-Based

- Imageless

- Others

- End-User

- Hospitals

- ASCs

- Clinics

- Research Institutes

- Component

- Hardware

- Software

- Services

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- UAE

- APAC

- China

- South America

- Brazil

- Rest of World (ROW)

- North America

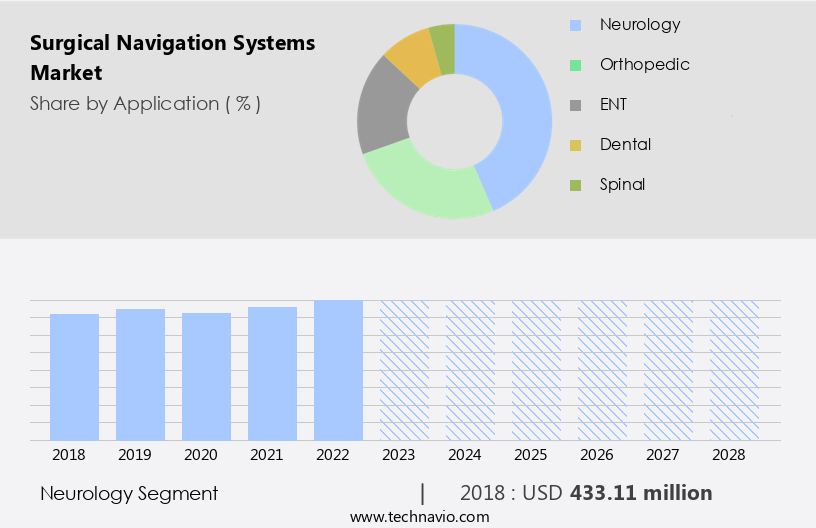

By Application Insights

The neurology segment is estimated to witness significant growth during the forecast period.

In the medical field, surgical navigation systems have gained significant traction, particularly in the neurology segment. These advanced technologies offer real-time imaging and navigation guidance during intricate neurosurgical procedures, ensuring high precision and accuracy. Neurosurgeons rely on surgical navigation systems to map out tumor locations, delicate nerve pathways, and intricate brain structures, enabling minimally invasive interventions. For instance, during neurosurgical tumor resections, these systems help identify and avoid critical brain regions, thereby minimizing neurological deficits post-surgery. Moreover, surgical navigation systems are indispensable in procedures like deep brain stimulation (DBS) for Parkinson's disease and essential tremor. Image fusion algorithms, preoperative planning, patient positioning systems, and 3D visualization are integral components of these systems, enhancing surgical workflow efficiency and depth perception.

In addition, real-time tracking, instrument tracking, and sensor fusion techniques contribute to navigation accuracy. Surgical planning software, ultrasound integration, and computed tomography guidance further expand the capabilities of surgical navigation systems. Furthermore, radiation therapy integration and haptic feedback offer enhanced capabilities for neurosurgical procedures. Surgical robotics, virtual reality simulation, and laser guidance systems are also integral parts of these advanced systems, offering minimally invasive and precise surgical interventions. Overall, surgical navigation systems are revolutionizing neurosurgery by providing critical guidance during complex procedures, ensuring optimal patient outcomes.

The Neurology segment was valued at USD 433.11 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

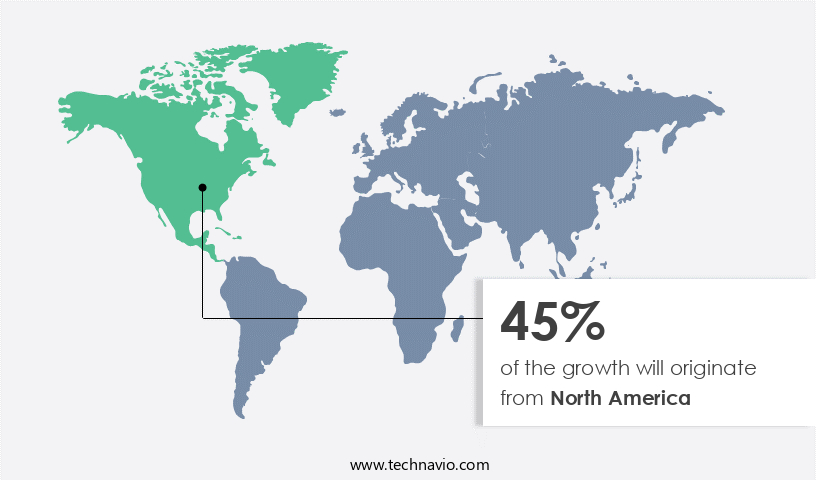

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth due to the integration of advanced technologies such as anatomical modeling, image fusion algorithms, and preoperative planning in precision surgery. Minimally invasive procedures are becoming increasingly popular, leading to a demand for surgical navigation systems that enhance workflow efficiency and provide real-time tracking of instruments. Haptic feedback and computer-assisted surgery enable surgeons to perform neurosurgical procedures with greater accuracy, while electrode placement guidance and bone registration accuracy ensure optimal results. Image-guided surgery and patient positioning systems offer 3D visualization and tissue deformation compensation, allowing for more effective radiation therapy integration.

Surgical planning software, ultrasound integration, and depth perception enhancement are essential components of the market, providing surgeons with valuable data for informed decision-making. Computed tomography guidance, augmented reality overlay, and laser guidance systems offer enhanced precision and accuracy during procedures. Intraoperative imaging and instrument tracking enable real-time monitoring, while surgical robotics and virtual reality simulation provide immersive and harmonious surgical experiences. Sensor fusion techniques, fluorescence guidance, and real-time tracking further improve navigation accuracy. The data integration platform and surgical trajectory planning facilitate seamless data exchange and reduce surgical errors, making surgical navigation systems an indispensable tool in modern healthcare.

Orthopedic navigation and optical tracking systems cater to the unique needs of orthopedic procedures, further expanding the market's scope. The integration of these advanced technologies is driving the market, with North America holding a significant share due to the high prevalence of chronic disorders such as diabetes and cardiovascular diseases.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Surgical Navigation Systems Industry?

- The high prevalence of cardiovascular diseases (CVD) serves as the primary driver for the market's growth.

- Cardiovascular diseases (CVD) are a significant global health concern, accounting for approximately one-third of annual worldwide deaths, according to the World Health Organization. In the US, as reported by the Centers for Disease Control and Prevention (CDC), heart disease claims around 610,000 lives each year, with about 790,000 Americans experiencing a heart attack, of which nearly 580,000 are first-time occurrences and 210,000 are recurrent. To enhance precision in surgical procedures for treating CVD, advanced technologies like surgical navigation systems are increasingly being adopted.

- These systems utilize anatomical modeling, image fusion algorithms, and preoperative planning to facilitate minimally invasive surgeries, improving surgical workflow efficiency and accuracy. Additionally, haptic feedback and computer-assisted surgery technologies further refine the surgical experience, ensuring harmonious interaction between the surgeon and the system. Neurosurgical navigation systems are a prime application of these advanced technologies, enabling surgeons to navigate complex anatomical structures with greater accuracy and confidence.

What are the market trends shaping the Surgical Navigation Systems Industry?

- Surgical navigation systems are experiencing significant technological advancements, which is currently a prominent trend in the medical industry. These innovative systems enhance the precision and effectiveness of surgical procedures.

- Surgical navigation systems are revolutionizing the medical field with advanced technologies that enhance precision and optimize surgical procedures. These systems leverage electrode placement guidance, bone registration accuracy, and calibration procedures to ensure accurate and efficient surgical interventions. The integration of surgical simulation, image-guided surgery, patient positioning systems, 3D visualization, tissue deformation compensation, and radiation therapy integration is transforming the landscape of various medical specialties. One significant technological advancement is the incorporation of augmented reality (AR) and virtual reality (VR) capabilities into surgical navigation systems. AR technology provides surgeons with real-time imaging data overlay, offering enhanced spatial orientation and precise anatomical guidance during procedures.

- In orthopedic surgeries, AR-assisted navigation systems enable detailed visualization of bone structures and implant positioning, reducing the risk of postoperative complications and improving the accuracy of joint replacement procedures. Moreover, ongoing advancements in surgical navigation systems are driving innovation and improving patient outcomes across multiple medical specialties. The market is expected to continue growing, as healthcare providers seek to provide the most advanced and precise surgical interventions possible. With the integration of advanced technologies, surgical navigation systems are becoming an essential tool in modern healthcare, transforming the way surgeons approach complex procedures and ultimately improving patient care.

What challenges does the Surgical Navigation Systems Industry face during its growth?

- The significant upfront expense associated with procuring surgical navigation systems poses a substantial challenge to the industry's growth trajectory.

- Surgical navigation systems, which incorporate advanced technologies such as surgical planning software, ultrasound integration, depth perception enhancement, computed tomography guidance, augmented reality overlay, laser guidance systems, intraoperative imaging, and instrument tracking, have gained significant attention in the healthcare industry due to their potential to enhance surgical precision and improve patient outcomes. However, the high cost of acquiring and implementing these systems remains a significant barrier to widespread adoption. The substantial investment required for hardware, software, training, and infrastructure upgrades can strain the financial resources of hospitals and surgical facilities.

- Furthermore, the integration of technologies like ultrasound and computed tomography guidance, as well as the implementation of immersive and harmonious surgical robotics, can add to the overall cost. Despite these challenges, the potential benefits of surgical navigation systems, including improved accuracy, reduced operative time, and enhanced patient safety, continue to drive demand for these advanced technologies in healthcare settings.

Exclusive Customer Landscape

The surgical navigation systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the surgical navigation systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, surgical navigation systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

B.Braun SE - The company specializes in providing surgical navigation systems, including the AMPLIVISION system, which enables surgeons to perform procedures efficiently and accurately with customized preferences. This technology enhances surgical precision and reliability, contributing significantly to the medical field.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- B.Braun SE

- Brainlab AG

- CASCINATION AG

- Corin Group Plc

- Fiagon GmbH

- General Electric Co.

- Johnson and Johnson

- KARL STORZ SE and Co. KG

- Lexmark International Inc.

- Medacta International SA

- Medtronic Plc

- Navigate Surgical Technologies Inc.

- OrthAlign Corp.

- Orthofix Medical Inc.

- Samsung Electronics Co. Ltd.

- Siemens AG

- Smith and Nephew plc

- Stryker Corp.

- Zimmer Biomet Holdings Inc.

- Amplitude Surgical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Surgical Navigation Systems Market

- In January 2024, Medtronic plc, a leading medical technology, services, and solutions company, announced the U.S. Food and Drug Administration (FDA) clearance for its StealthStation S7 System, an advanced surgical navigation platform designed to enhance precision in spine procedures (Medtronic Press Release, 2024).

- In March 2024, Stryker Corporation, a global medical technology company, entered into a strategic partnership with Brainlab AG, a leading provider of medical technology solutions, to expand its surgical navigation offerings and enhance its neuro and spine portfolios (Stryker Press Release, 2024).

- In May 2024, Intuitive Surgical, Inc., a pioneer in robotic-assisted surgery, received FDA clearance for the Ion EndoWrist Stapler, an addition to its da Vinci surgical system, enabling more precise and efficient surgical procedures (Intuitive Surgical Press Release, 2024).

- In April 2025, Zimmer Biomet Holdings, Inc., a global leader in musculoskeletal healthcare, completed the acquisition of Medtech Surgical, a privately-held company specializing in image-guided surgery and surgical navigation systems, to strengthen its portfolio and expand its presence in the growing image-guided surgery market (Zimmer Biomet Press Release, 2025).

Research Analyst Overview

- In the market, image registration metrics play a crucial role in ensuring accurate and effective navigation during complex procedures. User interface design is another significant factor, as intuitive interfaces streamline clinical workflow optimization and enhance surgical technique optimization. Performance benchmarking is essential for assessing system capabilities, while sensor data fusion and error detection mechanisms improve overall system reliability. Preoperative image acquisition requires data privacy safeguards, and training simulation modules enable usability testing and regulatory compliance. Surgical navigation software and hardware components must integrate seamlessly, with safety features and system security prioritized. Intraoperative image analysis and postoperative image review rely on medical image processing and data visualization tools.

- Registration algorithms and 3D reconstruction algorithms utilize optical tracking technology and computer vision techniques to enhance accuracy. System calibration methods and system maintenance protocols ensure consistent performance, while system integration challenges persist as new technologies emerge. Motion tracking sensors and system integration are key areas of focus for market growth.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Surgical Navigation Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.92% |

|

Market growth 2024-2028 |

USD 580.92 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.83 |

|

Key countries |

US, Germany, France, UK, China, Canada, Italy, UAE, Brazil, and Rest of World(ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Surgical Navigation Systems Market Research and Growth Report?

- CAGR of the Surgical Navigation Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the surgical navigation systems market growth of industry companies

We can help! Our analysts can customize this surgical navigation systems market research report to meet your requirements.

RIA -

RIA -