Paints Packaging Market Size 2024-2028

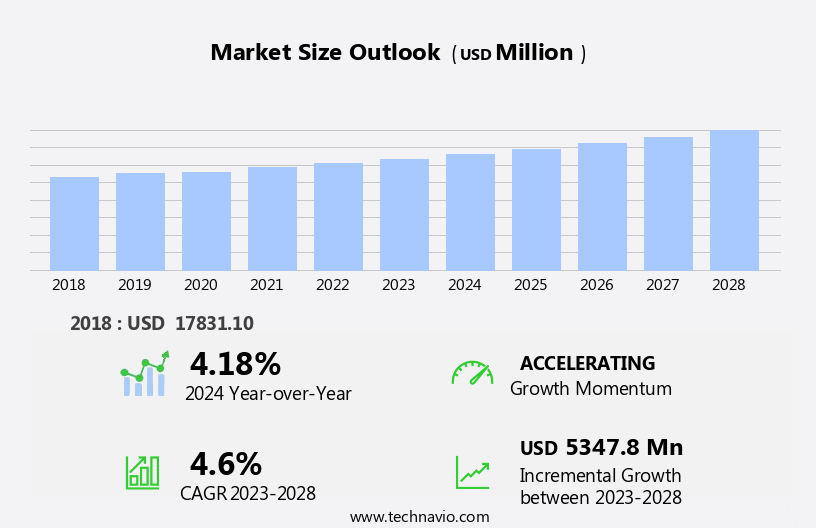

The paints packaging market size is forecast to increase by USD 5.35 billion, at a CAGR of 4.6% between 2023 and 2028.

- The market is driven by the surging demand for paints and their derivatives, fueled by the construction industry's expansion, particularly in the realm of skyscraper construction. This trend is expected to continue, providing ample opportunities for market participants. However, the market faces challenges as well. Fluctuating prices for raw materials, such as resins and pigments, used in paint packaging pose significant risks. These price volatilities can impact the overall cost structure of the industry and potentially disrupt supply chains. To navigate these challenges, market players must focus on implementing cost-effective production methods, exploring alternative raw materials, and fostering strong supplier relationships.

- By addressing these challenges and capitalizing on the growing demand, companies can effectively position themselves in the dynamic the market.

What will be the Size of the Paints Packaging Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The paint packaging market is characterized by its continuous evolution, with dynamic market trends shaping its various sectors. Roller coating, a popular application technique, is increasingly being adopted for its efficiency and cost optimization. Surface preparation plays a crucial role in ensuring the effectiveness of coatings, with pigment dispersion technology advancing to enhance color consistency. Cost optimization remains a significant focus, with logistics and distribution strategies being optimized to minimize transportation costs and improve delivery times. The use of plastic containers and paperboard packaging materials is growing due to their cost-effectiveness and environmental compliance. Safety data sheets and labeling and printing technologies are essential for ensuring regulatory compliance and consumer safety.

The ongoing development of resin technology and additives and fillers is driving innovation in protective coatings, epoxy coatings, and polyurethane coatings. The supply chain management of paint packaging involves intricate coordination between various stakeholders, from raw material suppliers to end-users. Inventory management and batch traceability are critical components of this process, ensuring product quality and customer satisfaction. Application techniques continue to evolve, with spray painting, dip coating, electrostatic painting, and brush painting each offering unique advantages. Curing processes, including drying time and UV resistance, are essential to ensure the durability and effectiveness of coatings. The paint packaging industry is subject to various regulations and standards, with environmental compliance being a significant concern.

Paint mixing equipment, paint cans, paint cartridges, and paint pouches are all designed to meet these requirements while optimizing performance and cost. The market for paint packaging is diverse, encompassing aerospace coatings, automotive coatings, marine coatings, architectural coatings, and industrial coatings, among others. Each sector presents unique challenges and opportunities, requiring ongoing innovation and adaptation. In conclusion, the paint packaging market is a dynamic and evolving industry, with continuous innovation and adaptation essential to meet the changing needs of various sectors. From cost optimization and surface preparation to application techniques and regulatory compliance, the market is characterized by its complexity and intricacy.

The ongoing development of paint packaging technology is essential to ensure the effectiveness, efficiency, and sustainability of coatings applications.

How is this Paints Packaging Industry segmented?

The paints packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

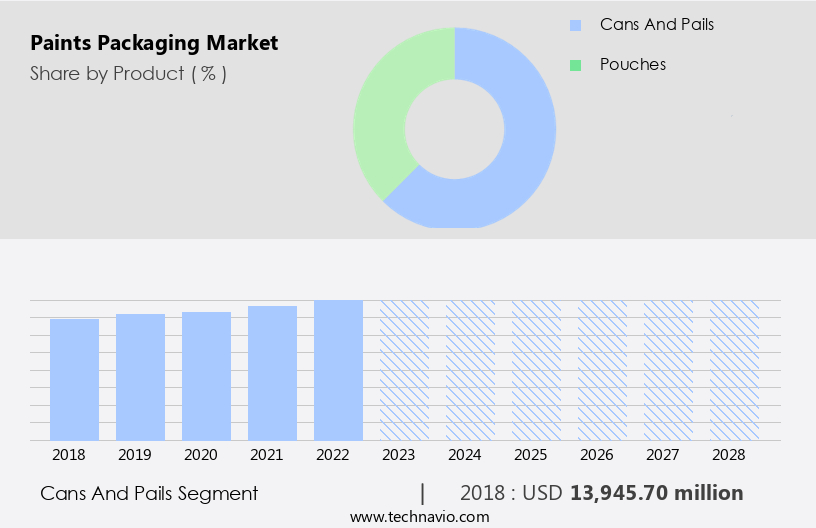

- Cans and pails

- Pouches

- Material

- Rigid plastic

- Metal

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The cans and pails segment is estimated to witness significant growth during the forecast period.

In the dynamic world of paints packaging, traditional containers such as cans and pails continue to play a significant role. Metal cans, primarily made from steel or aluminum, have been a mainstay in the industry due to their durability, resistance to external elements, and preservation capabilities. These containers come in various sizes, including quart, gallon, and larger volumes, catering to both DIY painters and professionals. Beyond metal containers, the market also embraces other packaging solutions. Water-based and solvent-based coatings require specific packaging to maintain their properties. For instance, water-based coatings often utilize paperboard containers, while solvent-based coatings may rely on metal or plastic containers for optimal preservation.

Aerospace coatings, protective coatings, industrial coatings, and marine coatings all have unique packaging requirements. Regulations and standards, such as batch traceability, environmental compliance, and safety data sheets, influence the design and production of paint packaging. Pigment dispersion, surface preparation, and application techniques are crucial factors in the curing processes of various coatings. Paint packaging machinery, roller coating, spray painting, and electrostatic painting are essential techniques used in the industry. Supply chain management, inventory management, logistics and distribution, and cost optimization are key aspects of the market. Advanced packaging technologies, such as paint pouches, paint cartridges, and paint dispensing systems, are increasingly popular due to their convenience and cost-effectiveness.

Resin technology, additives and fillers, and labeling and printing are integral components of the packaging design process. Corrosion resistance, chemical resistance, and weather resistance are essential properties that packaging must possess to ensure the longevity and effectiveness of the coating products. In conclusion, the market is a complex ecosystem that requires a deep understanding of various factors, from the properties of coatings to the logistical challenges of distribution. By focusing on innovation, sustainability, and regulatory compliance, market players can stay competitive and meet the evolving needs of their customers.

The Cans and pails segment was valued at USD 13.95 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

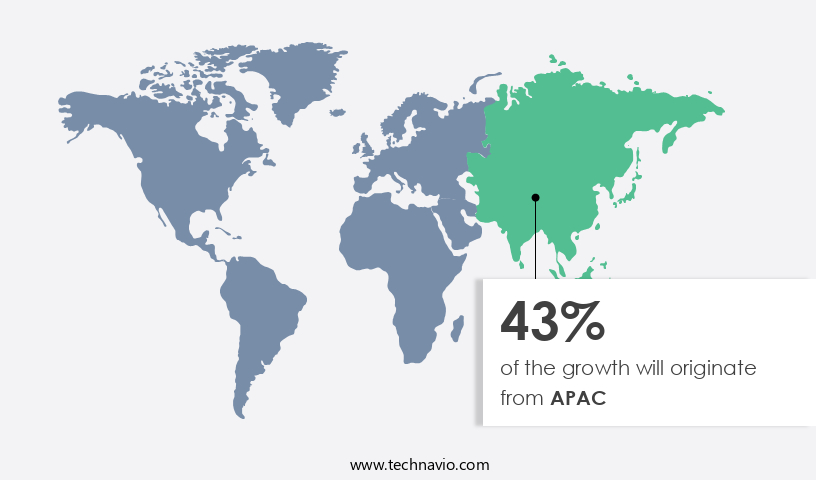

APAC is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC) is experiencing significant growth due to the increasing demand for paints in the region, driven by population growth, urbanization, and the construction industry. China, India, South Korea, Australia, and Japan are expected to dominate the market during the forecast period. China's low manufacturing costs, primarily due to low labor costs, make it a major supplier in the market. Regulations and standards, such as environmental compliance and safety data sheets, are essential considerations in the industry. Paint packaging solutions include various types, such as solvent-based coatings, water-based coatings, aerospace coatings, protective coatings, industrial coatings, and marine coatings.

Paint packaging formats include paint cans, paint buckets, paint cartridges, paint pouches, and paint aerosols. Supply chain management, inventory management, logistics and distribution, and application techniques are critical aspects of the industry. Paint packaging machinery, such as paint mixing equipment, paint packaging machinery, and roller coating, are essential for efficient production. Resin technology, pigment dispersion, and curing processes are also crucial in the production of high-quality paints. Chemical resistance, corrosion resistance, weather resistance, and UV resistance are essential properties of paint packaging materials. Additives and fillers, such as acrylic coatings, epoxy coatings, polyurethane coatings, and powder coatings, enhance the performance and durability of paints.

Labeling and printing, cost optimization, and surface preparation are other essential factors influencing the market. The paints packaging industry is subject to various regulations, including batch traceability and environmental compliance. The industry also requires quality control and packaging design to ensure customer satisfaction and brand reputation. The market is expected to continue growing during the forecast period, driven by the increasing demand for paints and the need for efficient and effective paint packaging solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Paints Packaging Industry?

- The significant increase in demand for paints and their derivatives serves as the primary market driver.

- The paints market encompasses a range of products, catering to diverse applications and end-user needs. These include solvent-based coatings such as varnishes, lacquers, and enamels, as well as water-based alternatives like acrylic paints and latex. The construction sector, driven by the demand for new and refurbished buildings, is a significant market for paints and their derivatives. Each building typically undergoes repainting every 3-5 years, with the frequency depending on the paint type and building material. Existing structures represent a substantial market share and will fuel the growth of the paints market during the forecast period.

- This trend is expected to boost the demand for paint packaging solutions, particularly for protective, industrial, and aerospace coatings, which require robust supply chain management for chemical resistance and batch traceability. Epoxy and dip coatings are other notable segments that will contribute to the market expansion due to their superior performance in various industries.

What are the market trends shaping the Paints Packaging Industry?

- Skyscraper construction is currently experiencing a significant uptick, representing the latest market trend. This growth is driven by various factors, including urbanization, technological advancements, and increasing demand for commercial and residential space.

- The market is driven by several factors, including environmental compliance, advancements in resin technology, and the growing demand for various coatings such as polyurethane and marine. Environmental regulations have led to the adoption of eco-friendly packaging solutions, such as metal containers with corrosion resistance and paperboard containers, which are increasingly being used to meet these requirements. Paint mixing equipment and labeling and printing technologies have also advanced, enabling more precise and efficient production processes. Additionally, the use of additives and fillers has improved paint quality and performance. Spray painting technology has gained popularity due to its convenience and speed, leading to an increase in demand for paint packaging machinery.

- The market for marine coatings is also expected to grow due to the rising demand for durable and protective coatings for ships and boats. Overall, the market is expected to continue its growth trajectory, driven by these trends and advancements in technology.

What challenges does the Paints Packaging Industry face during its growth?

- The paint industry faces significant growth challenges due to the volatile pricing of raw materials utilized in packaging, a key component of production costs.

- The market is influenced by several factors, with raw material costs being a significant determinant. Rigid materials, primarily plastic and metals, are commonly used for paint packaging. Price fluctuations in these raw materials can significantly impact the cost of paints packaging during the forecast period. The increasing demand-supply gap in recent years has led to a surge in raw material prices, which may reduce manufacturers' profit margins. Various types of plastics, such as polyethylene, polypropylene, and polyvinyl carbonates, are utilized for manufacturing paint packages. The selection of plastic type depends on factors like cost optimization, surface preparation, pigment dispersion, application techniques, curing processes, and shelf life.

- Logistics and distribution are also crucial aspects of the market. Ensuring efficient and safe transportation and storage of paints is essential to maintain product quality and safety. Proper product labeling, including safety data sheets, is necessary for regulatory compliance and consumer information. Powder coatings, an alternative to traditional liquid paints, are gaining popularity due to their environmental benefits and cost-effectiveness. However, the packaging requirements for powder coatings differ significantly from those of liquid paints, necessitating specialized packaging solutions. In conclusion, the market is driven by various factors, including raw material costs, product requirements, and regulatory compliance.

- Manufacturers must address these challenges to ensure cost-effective, efficient, and safe packaging solutions for paints and coatings.

Exclusive Customer Landscape

The paints packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the paints packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, paints packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - This company specializes in innovative paint packaging solutions, catering to various industries including furniture and construction.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Ardagh Group SA

- BABA GROUP OF COMPANIES

- Berlin Packaging LLC

- Berry Global Inc.

- BWAY Corp.

- Can One Berhad

- Dow Inc.

- Envases Group

- Greif Inc.

- Inno Pak Inc.

- Involvement Ltd

- Mangla Metal Pvt. Ltd.

- Mold Tek Packaging Ltd.

- Mondi Plc

- MUTHA PLASTIC INDUSTRIES

- National Can Industries Pty Ltd.

- Reliance Plastic Containers

- Silgan Holdings Inc.

- Sun Packaging

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Paints Packaging Market

- In January 2024, PPG Industries, a leading paints and coatings company, announced the launch of its new line of eco-friendly paint cans made from 100% recycled materials. This innovation marked a significant stride in the market towards sustainable solutions (PPG Industries press release).

- In March 2024, AkzoNobel, a global paints and coatings company, entered into a strategic partnership with Würth, the global leader in the fastening and assembly materials industry. This collaboration aimed to co-create innovative packaging solutions for the paints and coatings sector (AkzoNobel press release).

- In May 2024, Axalta Coating Systems, a leading global coatings company, completed the acquisition of the European decorative coatings business of Sika AG. This acquisition expanded Axalta's presence in Europe and strengthened its position in the market (Axalta Coating Systems press release).

- In February 2025, BASF SE, the world's largest chemical producer, received regulatory approval from the European Commission for its new packaging solution for paints, which uses renewable raw materials. This approval marked a significant step forward in the adoption of eco-friendly packaging in the paints industry (BASF SE press release).

Research Analyst Overview

- In the dynamic packaging market, trends lean towards sustainable and high-performance solutions. Flexographic printing and digital printing dominate the scene, ensuring vibrant brand identity on various packaging formats. Tamper-evident seals and child-resistant packaging enhance product safety, while circular economy principles drive the adoption of recycled content and bio-based packaging. Oxygen and moisture barriers, UV protection, and climate testing are crucial for extended shelf life. Sustainability certifications, such as those for compostable and recycled content, are increasingly sought after. Packaging automation streamlines production, reducing waste and improving efficiency. Leak-proof packaging, vacuum packaging, and bag-in-box solutions cater to diverse industry needs.

- High-barrier packaging, including those with UV protection and moisture barriers, protect sensitive products. Packaging line integration and label design are key considerations for seamless production and brand differentiation. Vibration and drop testing ensure product durability throughout the supply chain. The market continues to evolve, with an emphasis on sustainable, functional, and cost-effective solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Paints Packaging Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2024-2028 |

USD 5347.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.18 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Paints Packaging Market Research and Growth Report?

- CAGR of the Paints Packaging industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the paints packaging market growth of industry companies

We can help! Our analysts can customize this paints packaging market research report to meet your requirements.

RIA -

RIA -