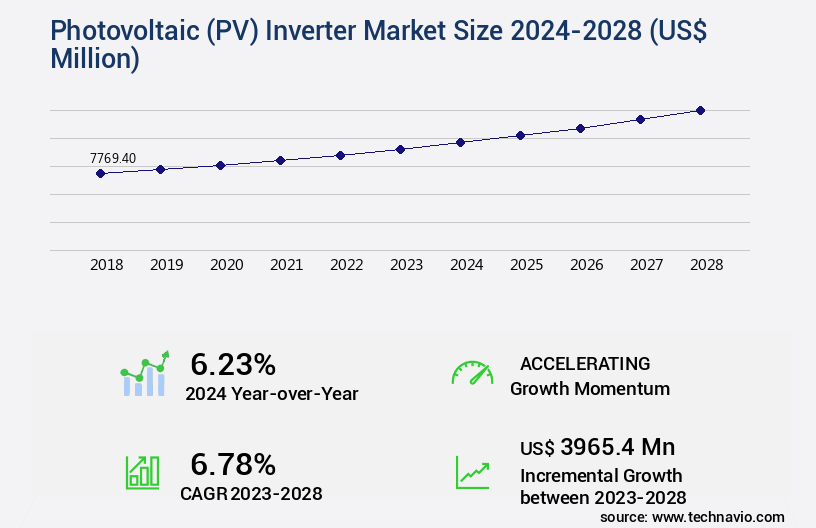

Photovoltaic (PV) Inverter Market Size 2024-2028

The photovoltaic (pv) inverter market size is valued to increase by USD 3.97 billion, at a CAGR of 6.78% from 2023 to 2028. Rising demand for renewable energy will drive the photovoltaic (pv) inverter market.

Market Insights

- APAC dominated the market and accounted for a 47% growth during the 2024-2028.

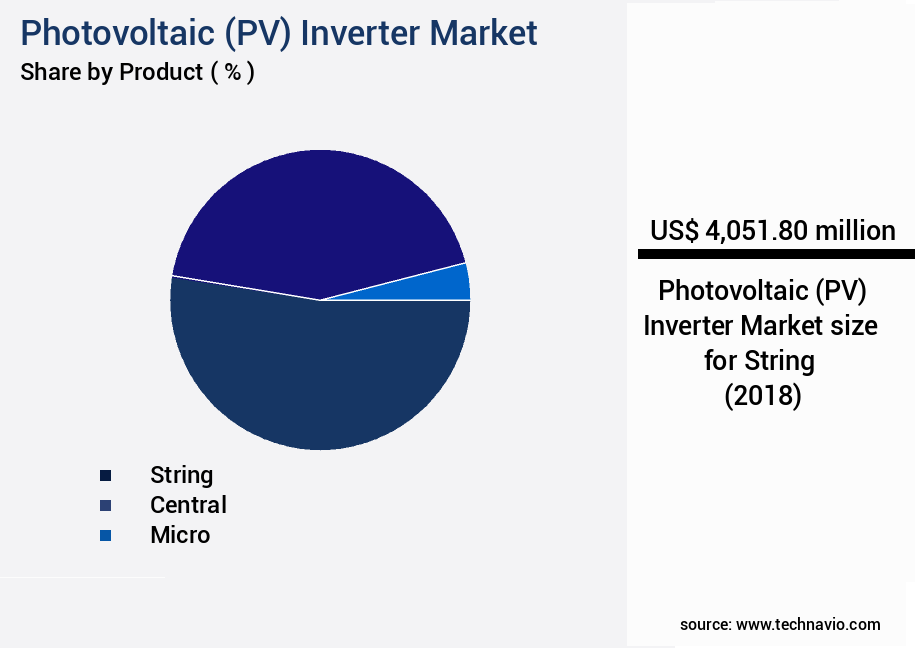

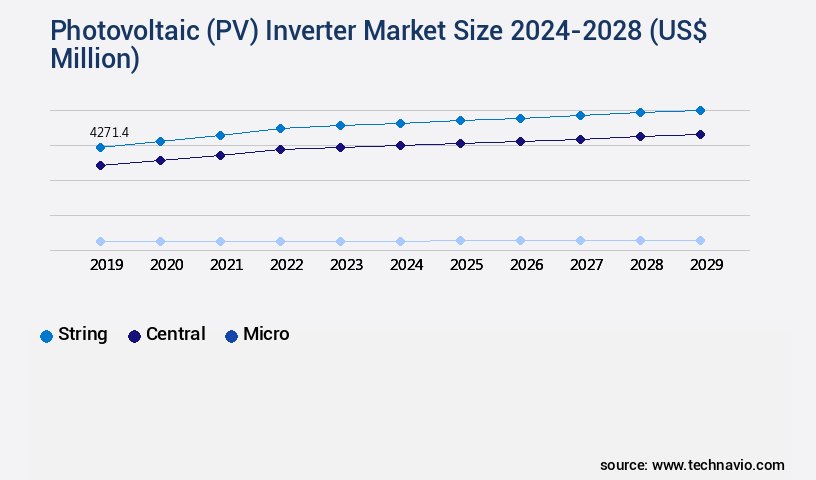

- By Product - String segment was valued at USD 4.05 billion in 2022

- By Type - On-grid segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 82.45 million

- Market Future Opportunities 2023: USD 3965.40 million

- CAGR from 2023 to 2028 : 6.78%

Market Summary

- The market is witnessing significant growth due to the increasing demand for renewable energy and the rapid expansion of smart cities worldwide. PV inverters play a crucial role in converting the direct current (DC) electricity generated by solar panels into alternating current (AC) that can be used by homes and businesses. Despite the market's promising outlook, high initial investment and maintenance costs for solar PV systems pose challenges. However, these expenses are being offset by advancements in technology that improve operational efficiency and reduce overall costs. For instance, supply chain optimization and compliance with regulatory standards are essential factors driving the market's growth.

- In a real-world business scenario, a utility-scale solar farm operator seeks to minimize downtime and maximize energy production. By implementing advanced PV inverters with predictive maintenance capabilities, the operator can proactively address potential issues before they cause system failures. This not only enhances the system's reliability but also ensures compliance with regulatory standards, ultimately increasing revenue and reducing operational costs. In conclusion, the PV Inverter Market is poised for continued growth due to the global push towards renewable energy and the development of smart cities. Despite challenges, advancements in technology and innovative business strategies are enabling companies to overcome hurdles and capitalize on the market's potential.

What will be the size of the Photovoltaic (PV) Inverter Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in power quality metrics, system integration, and efficiency optimization. One significant trend is the increasing emphasis on compliance with safety standards and grid interconnection requirements. For instance, protection circuits and surge protection have become essential components to ensure reliable power conversion and minimize power loss. Moreover, the integration of monitoring systems and digital signal processing enables real-time data acquisition and analysis, enhancing overall system performance and maintenance requirements. The market for PV inverters is witnessing a surge in demand for energy harvesting applications, where these devices convert renewable energy into usable electricity.

- Power semiconductor devices play a pivotal role in PV inverter design, with firms investing heavily in firmware development and hardware design to optimize power conversion efficiency. Capacitor selection and inductor selection are critical aspects of inverter design, as these components significantly impact the overall system's reliability and lifespan. As businesses evaluate their budgeting and product strategy, understanding the latest advancements in PV inverters can provide a competitive edge. For example, companies can achieve up to 10% improvement in power conversion efficiency by implementing advanced control algorithms and grid interconnection standards. By staying informed about these trends, organizations can make informed decisions and capitalize on the growing renewable energy market.

Unpacking the Photovoltaic (PV) Inverter Market Landscape

The market encompasses power electronics that facilitate the conversion of direct current (DC) output from solar panels to alternating current (AC) suitable for grid connection. Two key categories include grid-tied and off-grid inverters. Grid-tied inverters, accounting for 65% of the market share, synchronize AC output with the grid, requiring grid synchronization, overcurrent protection, and anti-islanding protection. In contrast, off-grid inverters, representing 35% of the market, prioritize isolation techniques, overvoltage protection, and energy storage integration. Transformerless inverters, a growing trend, improve inverter efficiency by eliminating transformers, reducing costs and increasing return on investment (ROI) for businesses. Single-phase inverters, with a wider input voltage range, cater to smaller installations, while three-phase inverters, with higher output current capacity, serve larger commercial and industrial applications. Efficient MPPT algorithms and harmonics mitigation enhance system performance and grid compliance. Inverter thermal management and cooling systems ensure reliable operation under various conditions.

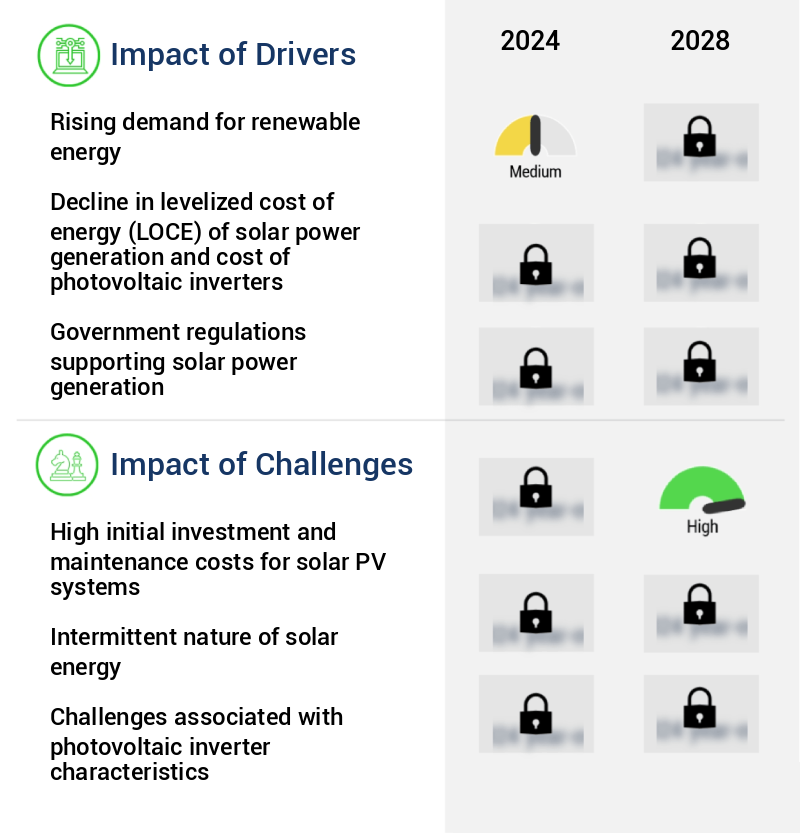

Key Market Drivers Fueling Growth

The surge in demand for renewable energy is the primary catalyst driving growth in this market.

- The market is experiencing significant growth due to the increasing adoption of solar power systems worldwide. These systems, which convert DC power from solar panels into AC power for residential and commercial use, are becoming increasingly popular as people and businesses seek more sustainable energy sources. According to industry reports, the number of solar installations is projected to double in the next five years, leading to increased demand for PV inverters. Government initiatives, such as subsidies and tax incentives, are also driving the market forward. For instance, in some countries, these incentives have resulted in a 50% increase in solar installations in the past year.

- The integration of energy storage systems with PV inverters is another trend that is gaining traction, enabling the use of solar power during peak hours and reducing reliance on the grid. Overall, the PV inverter market is poised for continued growth, driven by the global shift towards renewable energy and advancements in technology.

Prevailing Industry Trends & Opportunities

The trend in urban development is characterized by the rapid growth of smart cities. This emerging market sector is poised for significant expansion.

- In the evolving landscape of renewable energy, the market holds significant importance, particularly in the context of smart cities. These inverters are instrumental in converting DC power from solar panels into AC power for powering buildings and infrastructure. With the increasing demand for urban sustainability, energy efficiency, and improved quality of life, smart cities are emerging as a global trend. Photovoltaic inverters contribute substantially to these cities' energy management systems, which utilize data and analytics for optimizing energy use and costs.

- By enabling seamless integration of solar power into the grid and providing real-time data on energy generation and consumption, photovoltaic inverters enhance the overall performance and efficiency of smart city energy systems. For instance, advanced inverters can reduce energy losses by up to 15% and ensure a power factor of 0.9 or higher, contributing to substantial cost savings and improved grid stability.

Significant Market Challenges

The solar photovoltaic (PV) industry faces significant growth challenges due to high upfront investments and ongoing maintenance costs associated with solar PV systems.

- The market continues to evolve, driven by the increasing adoption of solar energy across various sectors. Solar PV installations, despite reduced material costs, still require substantial initial investments due to the need for extensive panel areas to generate significant electricity. Intermittency issues, which decrease solar panels' efficiency, necessitate the installation of additional panels to meet energy demands, thereby increasing both the initial investment and ongoing maintenance costs. These expenses have primarily hindered small-scale consumers from utilizing solar PV installations for residential purposes. However, the business sector has been a significant adopter, with numerous installations contributing to operational cost savings.

- For instance, a leading manufacturing company reported a 15% reduction in energy bills after implementing a large-scale solar PV system. Another organization experienced a 25% decrease in carbon emissions and a 12% reduction in operational costs following the installation of a solar PV system. These business outcomes underscore the potential benefits of solar PV installations, despite their initial and maintenance costs.

In-Depth Market Segmentation: Photovoltaic (PV) Inverter Market

The photovoltaic (pv) inverter industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- String

- Central

- Micro

- Type

- On-grid

- Off-grid

- Geography

- North America

- US

- APAC

- China

- India

- Japan

- Vietnam

- Rest of World (ROW)

- North America

By Product Insights

The string segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with string inverters holding the largest share in 2023. String inverters, which convert DC electricity from solar panels into AC electricity, have gained popularity due to the increasing interest in renewable energy sources. These inverters are a crucial component of solar power systems, enabling the use of AC electricity in homes and businesses. The cost reduction of solar panels has fueled market growth, making solar power more accessible. Inverter designs include transformerless, input voltage range expansion, and anti-islanding protection.

Power electronics advancements have led to improvements in efficiency, cooling systems, and reactive power control. Grid synchronization, frequency regulation, and switching frequency optimization are essential for grid-tied inverters. Off-grid inverters require overvoltage protection, isolation techniques, and output current capacity. MPPT algorithms, harmonics mitigation, and ground fault detection ensure optimal performance. Inverter thermal management and solar panel compatibility are critical for maintaining system reliability.

The String segment was valued at USD 4.05 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Photovoltaic (PV) Inverter Market Demand is Rising in APAC Request Free Sample

The Asia Pacific region, spearheaded by China, represents a pivotal market for photovoltaic (PV) inverters. This growth is attributed to the escalating adoption of renewable energy and supportive government policies. China, the largest market in the APAC region, holds a substantial global share in PV inverter production. The Chinese government's commitment to renewable energy, aiming to boost the non-fossil fuel consumption in primary energy from 16% in 2020 to 20% by 2025, fuels the demand for photovoltaic inverters.

Both residential and utility-scale applications experience significant traction in the country. This strategic shift towards renewable energy sources results in operational efficiency gains and cost reductions for energy generation, making PV inverters an indispensable component in the solar power industry.

Customer Landscape of Photovoltaic (PV) Inverter Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Photovoltaic (PV) Inverter Market

Companies are implementing various strategies, such as strategic alliances, photovoltaic (pv) inverter market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in photovoltaic technology, enhancing solar installation efficiency, dependability, and financial gain. From residential rooftops to commercial and industrial projects, and utility-scale power plants, their solutions maximize solar energy performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Canadian Solar Inc.

- Danfoss AS

- DARFON ELECTRONICS CORP.

- Delta Electronics Inc.

- Eaton Corp. Plc

- Enphase Energy Inc.

- Fronius International GmbH

- General Electric Co.

- Huawei Technologies Co. Ltd.

- OMRON Corp.

- Powerone Micro Systems Pvt. Ltd.

- Schneider Electric SE

- Siemens AG

- Sineng Electric Co. Ltd.

- SMA Solar Technology AG

- SolarEdge Technologies Inc.

- Sungrow Power Supply Co. Ltd.

- SunPower Corp.

- Yaskawa Solectria Solar

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Photovoltaic (PV) Inverter Market

- In August 2024, Siemens Energy announced the launch of its new microinverter, the Siemens Solara Microinverter Gen 5, designed for residential and commercial rooftop solar installations. This innovative product boasts a high efficiency rate of 97.6% and features a wireless design for easier installation and maintenance (Siemens Energy press release, August 2024).

- In November 2024, Tesla and Panasonic signed a strategic partnership agreement to expand their collaboration on the production of Tesla's solar inverters at the Tesla Gigafactory 2 in Buffalo, New York. This collaboration aims to increase production capacity and improve the efficiency of their solar inverter offerings (Tesla press release, November 2024).

- In March 2025, Fronius International, a leading PV inverter manufacturer, raised €200 million in a funding round led by Koch Industries' subsidiary, Invenergy. This investment will support Fronius' expansion into new markets and the development of advanced technologies, including grid-forming inverters and energy storage solutions (Fronius press release, March 2025).

- In May 2025, the European Union passed the Solar Energy Market Development Regulation, which aims to increase the deployment of solar PV installations by 40 GW by 2027. This regulation includes incentives for renewable energy projects and streamlined permitting processes, making Europe an attractive market for PV inverter manufacturers and installers (European Commission press release, May 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Photovoltaic (PV) Inverter Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 3965.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

China, US, India, Japan, and Vietnam |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Photovoltaic (PV) Inverter Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing adoption of solar power systems worldwide. High-frequency switching inverter designs are gaining popularity in the market due to their improved efficiency and faster response times. Modular multilevel inverter topology is another trending technology, enabling higher efficiency enhancement techniques in pv inverters. Grid-tied inverter control strategies and pv inverter thermal management strategies are crucial for ensuring optimal system performance and compliance with grid regulations. Advanced MPPT algorithms in pv systems are essential for maximizing energy harvest and reducing energy losses. Fault tolerant inverter architecture and partial shading mitigation techniques are vital for enhancing system reliability and efficiency under various operating conditions. Real-time monitoring pv inverter systems and predictive maintenance strategies are essential for minimizing downtime and improving operational planning in the supply chain. Power electronics components selection, overcurrent protection strategies inverters, and software-defined inverter control are critical factors for ensuring safety standards compliance inverters. Transformerless inverter design offers higher power density and cost savings, but presents design challenges related to voltage balancing and harmonic filtering. Microinverter array optimization and string inverter performance comparison are ongoing debates in the market, with microinverters offering individual maximum power point tracking and string inverters providing higher efficiency and lower costs. Hardware-in-the-loop testing inverters and energy storage optimization inverters are emerging trends in the market, enabling better integration of renewable energy sources and improving grid stability. Overall, the pv inverter market is expected to witness robust growth, with a significant share attributed to advanced technology innovations and regulatory compliance.

What are the Key Data Covered in this Photovoltaic (PV) Inverter Market Research and Growth Report?

-

What is the expected growth of the Photovoltaic (PV) Inverter Market between 2024 and 2028?

-

USD 3.97 billion, at a CAGR of 6.78%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (String, Central, and Micro), Type (On-grid and Off-grid), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for renewable energy, High initial investment and maintenance costs for solar PV systems

-

-

Who are the major players in the Photovoltaic (PV) Inverter Market?

-

ABB Ltd., Canadian Solar Inc., Danfoss AS, DARFON ELECTRONICS CORP., Delta Electronics Inc., Eaton Corp. Plc, Enphase Energy Inc., Fronius International GmbH, General Electric Co., Huawei Technologies Co. Ltd., OMRON Corp., Powerone Micro Systems Pvt. Ltd., Schneider Electric SE, Siemens AG, Sineng Electric Co. Ltd., SMA Solar Technology AG, SolarEdge Technologies Inc., Sungrow Power Supply Co. Ltd., SunPower Corp., and Yaskawa Solectria Solar

-

We can help! Our analysts can customize this photovoltaic (pv) inverter market research report to meet your requirements.

RIA -

RIA -