Plastic Caps And Closures Market Size 2024-2028

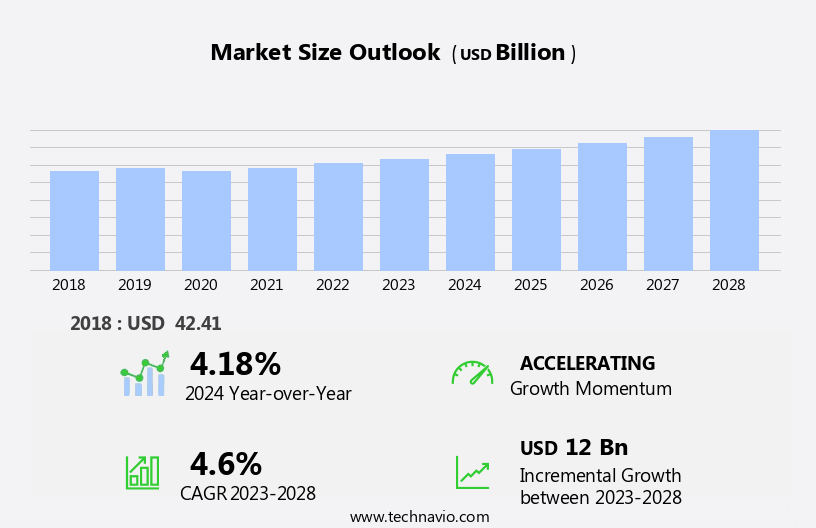

The plastic caps and closures market size is forecast to increase by USD 12 billion at a CAGR of 4.6% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the increasing demand for packaged beverages. This trend is particularly prominent in regions with a high consumption of bottled water and soft drinks. Another key factor fueling market expansion is the rise in mergers and acquisitions (M&A) among market players, as companies seek to expand their product portfolios and geographical reach. However, the market is not without challenges. Competition from closure-less packaging, such as pouch packaging and cartons, is intensifying, putting pressure on market participants to innovate and differentiate their offerings.

- To capitalize on opportunities and navigate challenges effectively, companies must stay abreast of consumer preferences and emerging technologies, while also focusing on cost optimization and sustainable manufacturing practices. By doing so, they can position themselves for long-term success in this dynamic and competitive market.

What will be the Size of the Plastic Caps And Closures Market during the forecast period?

- The market in the United States is a dynamic and significant segment of the beverage packaging sector, driven by the rising consumption of fruit beverages, bottled water, and ready-to-drink beverages. This market encompasses various materials, including thermoplastics such as polypropylene, high-density polyethylene (HDPE), and low-density polyethylene (LDPE), as well as elastomers, thermosets, metal, glass, wood, and paperboard. Tamper-evident caps and closures, including child-resistant designs, are essential for ensuring product safety and consumer confidence. FMCG companies continue to invest in innovative solutions, such as lighter-weight and more sustainable materials, to address environmental concerns and reduce packaging waste.

- Growth in the market is fueled by the increasing popularity of sports drinks, diet beverages, and other non-alcoholic beverages, as well as the ongoing shift from traditional glass and metal containers to plastic alternatives.

How is this Plastic Caps And Closures Industry segmented?

The plastic caps and closures industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Food and beverages

- Cosmetics and personal care products

- Pharmaceuticals

- Others

- Type

- Polypropylene

- Polyethylene

- Others

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- Russia

- Middle East and Africa

- South America

- APAC

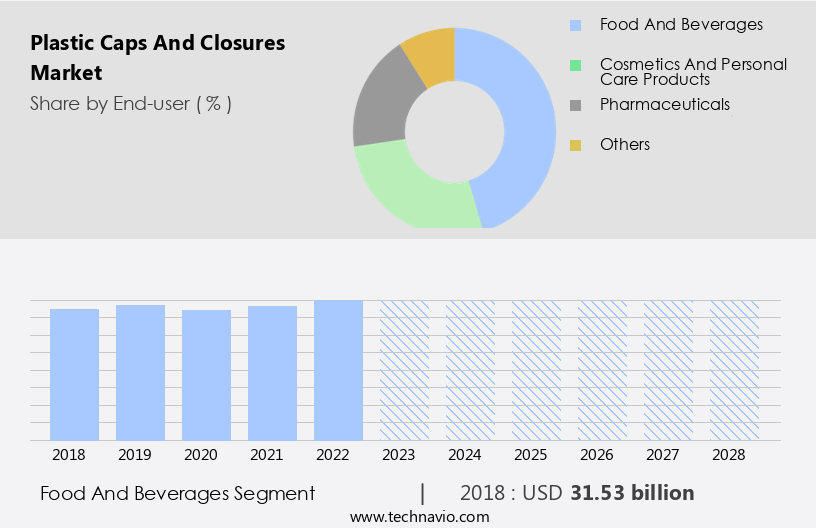

By End-user Insights

The food and beverages segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, particularly in the food and beverage industry. HDPE, Polypropylene (PP), LDPE, and other thermoplastic resins dominate the market due to their user-friendly packaging, enhanced functionality, and anti-corrosive property. In the food and beverage segment, carbonated soft drinks, juices, bottled water, sports and energy drinks, and other beverages are driving market growth. Consumer preferences are leaning towards convenient, tamper-evident caps and closures, dispensing mechanisms, and pierceable shell designs for various applications. The home care industry, make-up industry, and FMCG companies are also adopting plastic caps and closures for their products due to their sophistication and environmental welfare.

The evolving food industry and changing lifestyle are major factors contributing to the market's growth. The market faces stringent regulations to ensure hygiene, safety, and contamination prevention. Innovative packaging solutions, such as pump closures and dispensing closures, are gaining popularity due to their convenience and enhanced functionality. The market is expected to continue growing as consumers seek convenient and sophisticated packaging solutions for various applications.

Get a glance at the market report of share of various segments Request Free Sample

The Food and beverages segment was valued at USD 31.53 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

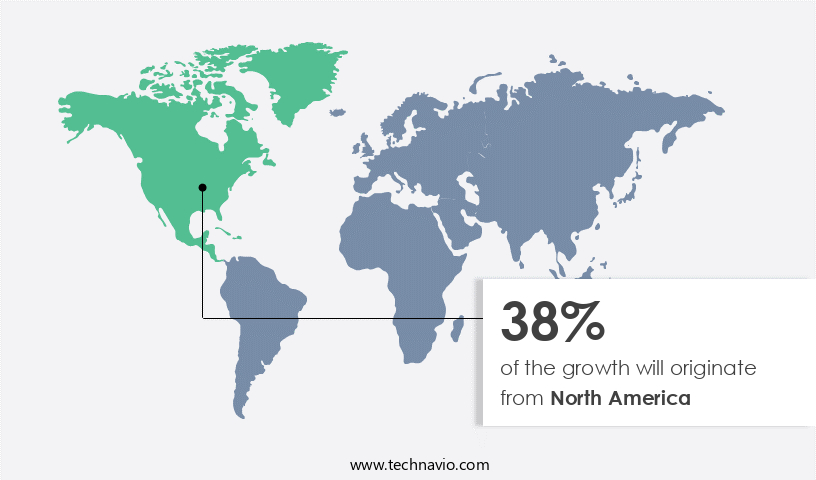

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market has experienced significant growth in the Asia Pacific region, particularly in countries like India, China, Japan, Singapore, and Australia. This expansion can be attributed to changing lifestyles and urbanization, leading consumers to prefer packaged and fresh food and beverages. The food and beverage processing industry in emerging economies such as Japan, India, and China has seen growth due to evolving consumer habits. The trend of convenience and on-the-go consumption has boosted the demand for packaged food products. In the beverage sector, plastic caps and closures, including tamper-evident seals, are increasingly used for bottled beverages, fresh juices, soft drinks, fruit beverages, bottled water, energy drinks, sports drinks, and ready-to-drink beverages.

The home care industry also utilizes plastic caps and closures for various products like shampoos, conditioners, detergents, and cleaning agents. Plastics like HDPE, LDPE, PP, and PE are commonly used for manufacturing these caps and closures due to their convenient packaging, enhanced functionality, and anti-corrosive property. The market also offers various types of closures, such as plastic screw closures, dispensing closures, and pump closures, which cater to the diverse needs of various industries. Environmental welfare concerns have led to the development of eco-friendly packaging solutions like pouches made of thermoplastic resins and elastomers. The market also caters to the needs of the make-up industry, FMCG companies, and the drug and medicines sector, offering child-resistant closures and pierceable shell designs.

The packaging waste issue is a concern for consumers and governments, leading to stringent regulations and the adoption of sustainable practices. The market is also witnessing the development of sophisticated dispensing mechanisms and delivery water bottles made of metal and paperboard. The evolving food industry and the increasing standard of living, especially in the context of hectic lifestyles, have led to the demand for convenient packaging solutions. The market also caters to various industries, including the food industry, dairy, sauces, and condiments, which require harsh chemicals for processing. In , the market is witnessing growth due to changing consumer habits, urbanization, and the evolving food industry.

The market offers a wide range of products catering to diverse industries and consumer needs, with a focus on convenience, sustainability, and functionality.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Plastic Caps And Closures Industry?

- Growing demand for packaged beverages is the key driver of the market.

- The growing urbanization and changing consumer lifestyles have led to an increase in demand for packaged beverages, particularly on-the-go products. In Q3 2022, sales of packaged beverages in convenience stores experienced a significant growth of over 12% year over year. This trend is not limited to developed economies; emerging markets such as Brazil, China, India, South Africa, and Vietnam are also witnessing a rise in demand due to the increasing disposable incomes of consumers. Moreover, the global consumption of bottled water has significantly contributed to the sales of packaged beverages.

- As beverage packaging companies cater to this demand, they rely on plastic caps and closures to seal fluids or liquids in various containers. This reliance is expected to continue as the demand for packaged beverages persists.

What are the market trends shaping the Plastic Caps And Closures Industry?

- Increase in mergers and acquisitions (M and A) is the upcoming market trend.

- Plastic caps and closures companies are strategically pursuing inorganic growth to capitalize on expanding markets in countries like India, Brazil, China, and South Africa. To strengthen their market presence and broaden product offerings, these manufacturers are engaging in mergers and acquisitions (M&A). M&A transactions enable businesses to enhance their market positioning and expand their reach. For instance, in August 2022, O.Berk West LLC announced the acquisition of E.D.

- Luce Packaging, a California-based wholesale distributor of bottles, jars, vials, containers, prescription packaging, and pharmaceutical supplies. This acquisition will augment O.Berk West's product portfolio and expand its customer base. Similarly, other market players are also leveraging M&A to fortify their positions in the competitive landscape.

What challenges does the Plastic Caps And Closures Industry face during its growth?

- Competition from closure-less packaging is a key challenge affecting the industry growth.

- The market may experience limited growth due to the increasing preference for closure-less packaging solutions, such as stand-up pouches and blister packs, in various industries. These packaging options offer benefits like ease of use, storage, and flavor preservation, making them suitable for food and beverage products that do not require closures. One such packaging solution is the retort pouch, which consists of multiple layers of laminates and is designed without caps or closures. Retort pouches are commonly used for sterile packaging of milk, juices, and convenience food products.

- Their compact, convenient, and lightweight nature makes them an ideal choice for maintaining the freshness of contents. Despite the advantages of these closure-less packaging solutions, the market still holds significance due to their widespread use in various applications where a secure seal is essential.

Exclusive Customer Landscape

The plastic caps and closures market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the plastic caps and closures market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, plastic caps and closures market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albea Services SAS - The company specializes in supplying plastic caps and closures, including flip-top PE slim caps, for various industries. Our product range caters to diverse packaging needs, ensuring optimal functionality and protection. With a focus on innovation and quality, we provide customizable solutions that enhance the user experience. Our caps are engineered for durability and compatibility with various container sizes and shapes. By utilizing advanced manufacturing techniques and materials, we deliver cost-effective and sustainable options. Our commitment to excellence and customer satisfaction sets us apart in the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albea Services SAS

- Amcor Plc

- AptarGroup Inc.

- Berry Global Inc.

- Caprite Australia

- Chemco Group

- Closure Systems International Inc.

- Coral Products Plc

- Crown Holdings Inc.

- Guala Closures SpA

- HERTI JSC

- HQC Inc.

- MJS Packaging

- O.Berk Co. LLC

- Pelliconi and C SpA

- Premier Vinyl Solutions Ltd.

- Secure Industries Pvt. Ltd.

- Silgan Holdings Inc.

- TriMas Corp.

- United States Plastic Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of products used to seal and protect various containers in numerous industries. These components play a crucial role in ensuring the freshness, safety, and convenience of packaged goods. In the beverage sector, high-density polyethylene (HDPE) and polypropylene (PP) caps and closures are commonly used for bottled beverages, including fresh juices, soft drinks, fruit beverages, and bottled water. In the home care industry, plastic caps and closures made from PE and PP are utilized for containers holding cleaning supplies and personal care products. The demand for user-friendly packages that cater to the sophisticated lifestyle of consumers continues to drive growth in this market.

The market also serves the food industry, where PP and PE caps and closures are employed for packaging condiments, sauces, and ready-to-drink beverages. The convenience offered by these packages is a significant factor in catering to the hectic lifestyle of consumers. The evolution of the food industry and changing lifestyle trends have led to an increased focus on convenient packaging solutions. Dispensing closures and mechanisms, such as pumps and pierceable shell designs, are becoming increasingly popular in the market. These closures offer enhanced functionality and convenience for consumers. Environmental welfare is another critical factor influencing the market. The use of thermoplastics, such as PP and PE, in place of glass and metal, reduces the overall weight and volume of packaging waste.

Additionally, the development of biodegradable and recyclable materials is gaining traction in the market. The beverage packaging sector is subject to stringent regulations regarding contamination and food safety. Plastic caps and closures must meet specific standards to ensure the safety and quality of the packaged goods. The use of anti-corrosive properties in plastic caps and closures is essential in preventing contamination and maintaining the integrity of the packaged product. The market also caters to various industries, including the FMCG sector, pharmaceuticals, and the makeup industry. In the pharmaceutical industry, child-resistant closures are essential to ensure the safety of drugs and medicines.

In the makeup industry, plastic screw closures made from elastomers are commonly used for makeup containers. The market for plastic caps and closures is diverse and dynamic, with ongoing advancements in materials, designs, and technologies driving growth. The convenience offered by plastic caps and closures, coupled with their ability to cater to various industries and lifestyle trends, makes them an indispensable component in the packaging industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2024-2028 |

USD 12 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.18 |

|

Key countries |

US, China, Germany, Russia, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Plastic Caps And Closures Market Research and Growth Report?

- CAGR of the Plastic Caps And Closures industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the plastic caps and closures market growth of industry companies

We can help! Our analysts can customize this plastic caps and closures market research report to meet your requirements.

RIA -

RIA -