Plumbing Pipes Market Size 2026-2030

The plumbing pipes market size is valued to increase by USD 40.23 billion, at a CAGR of 18.3% from 2025 to 2030. Growing real estate industry will drive the plumbing pipes market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 37.1% growth during the forecast period.

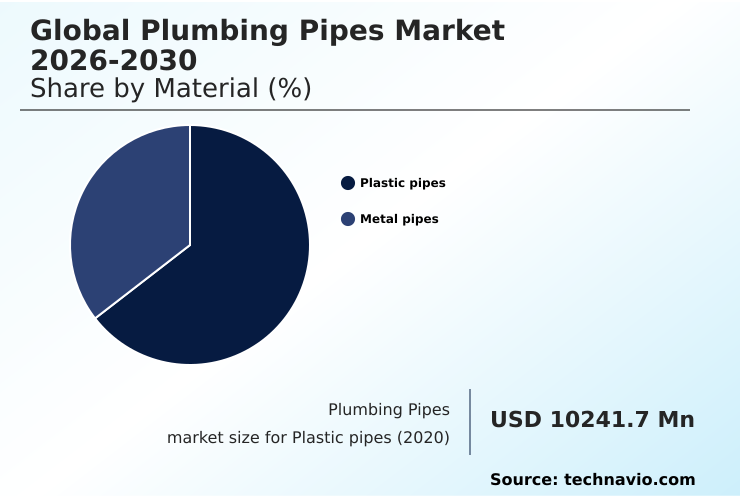

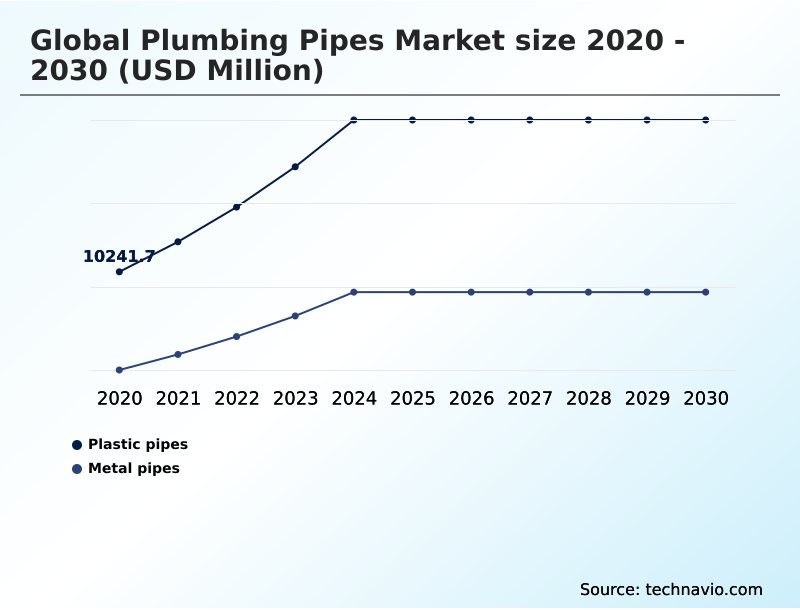

- By Material - Plastic pipes segment was valued at USD 17.38 billion in 2024

- By Application - Residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 54.87 billion

- Market Future Opportunities: USD 40.23 billion

- CAGR from 2025 to 2030 : 18.3%

Market Summary

- The plumbing pipes market is undergoing a significant transformation, driven by advancements in material science and a global push for infrastructure modernization. The shift from traditional metals to high-performance polymers such as pex, cpvc, and multilayer composite pipes is reshaping installation practices and system longevity, offering enhanced corrosion resistance and thermal stability.

- Demand is propelled by the expanding real estate sector and large-scale public sanitation projects focused on aging infrastructure replacement. For instance, a water utility can optimize its supply chain logistics by adopting trenchless installation methods for hdpe pipes, reducing project timelines and minimizing public disruption. However, the industry navigates challenges from raw material price volatility and stringent lead-free plumbing regulations.

- Trends toward smart plumbing solutions and the integration of building information modeling (BIM) are creating new opportunities, pushing manufacturers to innovate beyond basic conveyance to offer integrated systems that improve water conservation and operational efficiency.

What will be the Size of the Plumbing Pipes Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Plumbing Pipes Market Segmented?

The plumbing pipes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Plastic pipes

- Metal pipes

- Application

- Residential

- Commercial

- Others

- Usage

- Supply line

- Drainage line

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Material Insights

The plastic pipes segment is estimated to witness significant growth during the forecast period.

The plastic pipes segment, including those made with advanced extrusion technology, is integral to modern plumbing. Materials are selected for properties like thermal stability and corrosion resistance, crucial for high-pressure pipe systems.

Innovations in polymer science are producing specialized products like acoustic piping systems designed to reduce noise, and solutions for fire protection piping. For example, developments in molecular alignment allow for a 50% reduction in pipe wall thickness without sacrificing strength.

This drives adoption in applications where space and weight are critical.

The segment's evolution is further influenced by the need for advanced solutions like trenchless installation methods and integrated leak detection systems, catering to both new construction and infrastructure retrofitting with greater efficiency.

The Plastic pipes segment was valued at USD 17.38 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Plumbing Pipes Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the plumbing pipes market is shaped by regional construction activity and infrastructure priorities.

APAC leads market expansion, contributing 37.1% of the incremental growth, driven by extensive urbanization and public sanitation projects in countries like China and India.

North America, accounting for 27.18% of growth, focuses on residential plumbing renovation and upgrading aging water systems, with a strong emphasis on meeting stringent ASTM standards and ensuring water quality assurance.

Europe's market is driven by retrofitting existing buildings for energy efficiency and compliance with strict environmental regulations. The Middle East and Africa are witnessing a surge in large-scale commercial and industrial fluid transport projects.

In South America, the focus is on expanding basic water and sanitation access. Across all regions, the demand for ductile iron pipes in high-pressure applications and adherence to specific pressure rating standards remain critical.

Market Dynamics

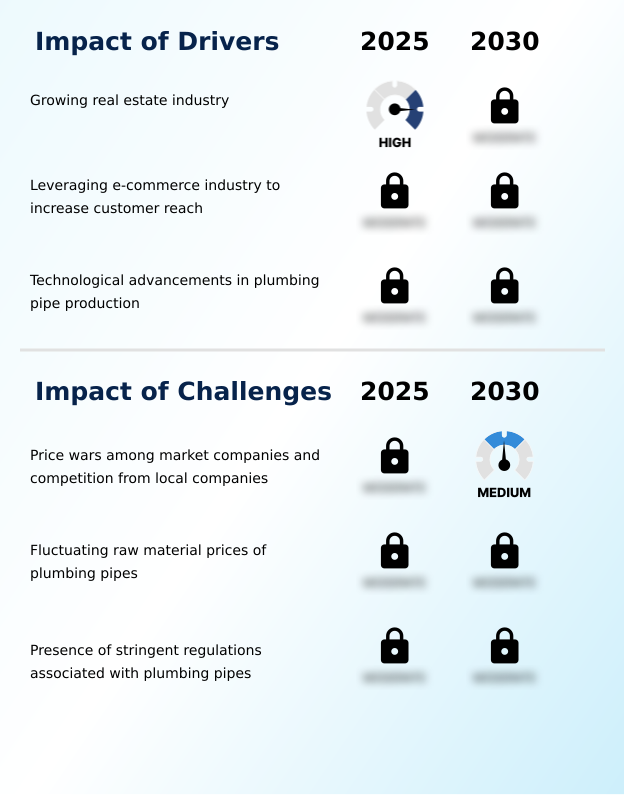

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning for modern construction requires a deep understanding of plumbing material trade-offs. The benefits of pex over copper pipes, such as flexibility and lower cost, are weighed against copper's longevity in a thorough cost-benefit analysis of multilayer pipes. For project managers, the pvc-o pipe manufacturing process explained in technical datasheets reveals advancements in strength and material efficiency.

- Choosing the best pipe material for hot water systems often involves evaluating the thermal resistance of cpvc piping. Installation methodology is another critical factor, where a mechanical coupling vs fusion welding methods comparison can highlight significant labor savings; some installation time for push-fit vs solvent weld systems can be reduced by more than half, directly impacting project budgets.

- Furthermore, navigating lead-free regulations for potable water pipes is non-negotiable. For specialized needs, engineers must consider specifications for high-pressure pipe for industrial use and noise reduction with acoustic drainage pipes. In sustainable projects, selecting sustainable materials for green building plumbing and understanding the circular economy impact on pvc pipe recycling are key.

- Smart plumbing for water leak prevention is becoming standard, while challenges in replacing aging iron pipes with hdpe pipe for municipal water supply are addressed through trenchless pipe replacement cost factors. Even specific applications like pipe selection for radiant floor heating and ensuring uv resistance in outdoor pipe installations demand careful evaluation.

What are the key market drivers leading to the rise in the adoption of Plumbing Pipes Industry?

- The primary driver propelling market growth is the expanding global real estate industry, which fuels demand for plumbing systems in new construction and renovation projects.

- Market growth is significantly driven by urbanization and technological integration in construction. The expansion of commercial building infrastructure and large-scale residential projects creates sustained demand for reliable potable water systems.

- Innovations like cross-linked polyethylene (PEX) and high-density polyethylene (HDPE) with push-fit fittings are accelerating project timelines, with some systems demonstrating a 30% faster installation compared to traditional methods.

- The use of building information modeling (BIM) allows for the integration of prefabricated plumbing modules, improving on-site efficiency. Furthermore, smart plumbing solutions are transitioning from niche to mainstream, offering enhanced monitoring and control.

- Compliance with standards like NSF/ANSI 61 certification remains a critical driver, ensuring safety and quality in all water-related applications and reinforcing the need for continuous product development and quality assurance in the industry.

What are the market trends shaping the Plumbing Pipes Industry?

- A significant trend shaping the market is the increasing demand for sustainable building materials, compelling manufacturers to innovate with eco-friendly and recyclable piping solutions.

- Key market trends are centered on sustainability and material science advancements. The increasing adoption of green building certifications is fueling demand for sustainable plumbing materials and eco-friendly piping solutions. This includes multilayer composite pipes and polypropylene (PP-R) systems, which offer recyclability and a lower environmental footprint.

- Innovations in chlorinated polyvinyl chloride (CPVC) are enhancing its use in both hot water lines and DWV applications due to its durability and resistance to degradation. The push for water conservation plumbing is also significant, with systems designed to minimize leakage and waste.

- For example, using polybutylene (PB) in certain applications has been shown to reduce material waste by 15% during installation compared to more rigid alternatives. The focus on a circular economy is prompting manufacturers to develop products that are easier to recycle, further aligning with market-wide sustainability goals.

What challenges does the Plumbing Pipes Industry face during its growth?

- A key challenge affecting industry growth is the intense price competition among established vendors, coupled with the rising pressure from low-cost local companies.

- The primary challenges facing the market stem from economic pressures and regulatory complexities. Persistent raw material price volatility creates significant uncertainty in production costing, impacting profit margins and forcing difficult pricing decisions. This is compounded by intense competition, where manufacturers must innovate while managing costs.

- Navigating the evolving landscape of lead-free plumbing regulations requires substantial investment in reformulating products like polyvinyl chloride (PVC) and upgrading manufacturing processes. For example, the transition to compliant solvent weld joints and developing stable UV resistance formulation adds complexity to supply chain logistics.

- Adopting smart manufacturing principles can mitigate some costs by improving efficiency, but the initial capital outlay is considerable. Furthermore, the extensive need for aging infrastructure replacement presents a logistical challenge, even as it creates long-term demand, with project costs increasing by as much as 20% in some regions due to labor shortages.

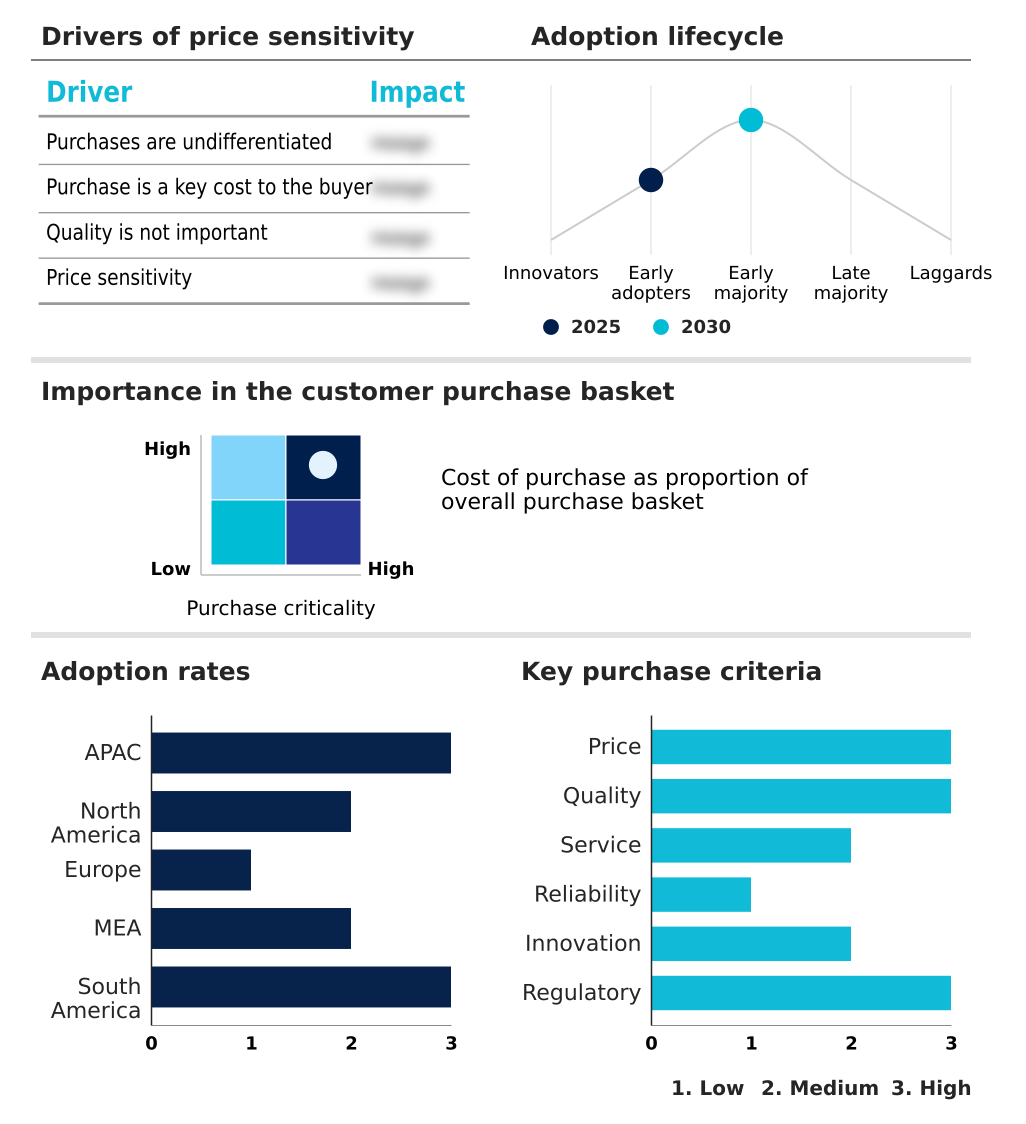

Exclusive Technavio Analysis on Customer Landscape

The plumbing pipes market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the plumbing pipes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Plumbing Pipes Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, plumbing pipes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aliaxis Holdings SA - Analysis reveals a portfolio of advanced piping systems for building, infrastructure, industrial, and agricultural applications, designed for broad market and solutions coverage.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aliaxis Holdings SA

- Apollo Pipes Ltd.

- Astral Ltd.

- Chevron Phillips Chemical Co.

- China Lesso Group Holdings

- Dutron Polymers Ltd.

- Finolex Industries Ltd.

- Geberit International AG

- IPEX BRANDING INC.

- JM Eagle Inc.

- Kubota Corp.

- McWane Inc.

- Pipelife International GmbH

- Polypipe Ltd.

- RIFENG Enterprise Co Ltd.

- Saudi Arabian Amiantit Co.

- Tessenderlo Group NV

- The Supreme Industries Ltd.

- Uponor Corp.

- Wavin BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Plumbing pipes market

- In October 2024, Aliaxis Holdings SA announced a strategic partnership with a leading IoT firm to integrate real-time leak detection sensors into its PEX piping systems, aiming to reduce water loss in residential and commercial buildings.

- In January 2025, Wavin BV completed the acquisition of a specialized manufacturer of recycled polymer pipes for $150 million, strengthening its sustainable product portfolio and expanding its circular economy initiatives.

- In March 2025, Uponor Corp. launched a new generation of bio-attributed PEX pipes, produced using renewable feedstocks, which are certified to have a 60% lower carbon footprint compared to conventional fossil-based alternatives.

- In May 2025, China Lesso Group Holdings received NSF/ANSI 61 certification for its new line of lead-free CPVC pipes, enabling its expansion into the North American potable water systems market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Plumbing Pipes Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2026-2030 | USD 40227.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The plumbing pipes market is defined by a dynamic interplay of material innovation and evolving regulatory demands. Boardroom decisions are increasingly focused on investing in smart manufacturing principles to navigate this landscape, ensuring product lines meet diverse specifications.

- For instance, the choice between polyvinyl chloride (PVC) with solvent weld joints and cross-linked polyethylene (PEX) with push-fit fittings is no longer just about cost but also about installation speed and long-term reliability. Advanced materials like chlorinated polyvinyl chloride (CPVC), high-density polyethylene (HDPE), and polybutylene (PB) offer superior thermal stability and corrosion resistance.

- The development of multilayer composite pipes and polypropylene (PP-R) systems caters to high-performance niches. Innovations such as biaxial orientation (PVC-O) are enabling thinner pipe wall thickness without compromising pressure rating standards.

- Compliance with ASTM standards and NSF/ANSI 61 certification is critical for potable water systems, while specialized solutions like acoustic piping systems for DWV applications and durable ductile iron pipes for fire protection piping are gaining traction.

- Advanced extrusion technology and UV resistance formulation are enhancing product quality, enabling new applications like trenchless installation methods that reduce project completion times by up to 40%.

What are the Key Data Covered in this Plumbing Pipes Market Research and Growth Report?

-

What is the expected growth of the Plumbing Pipes Market between 2026 and 2030?

-

USD 40.23 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Plastic pipes, and Metal pipes), Application (Residential, Commercial, and Others), Usage (Supply line, and Drainage line) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing real estate industry, Price wars among market companies and competition from local companies

-

-

Who are the major players in the Plumbing Pipes Market?

-

Aliaxis Holdings SA, Apollo Pipes Ltd., Astral Ltd., Chevron Phillips Chemical Co., China Lesso Group Holdings, Dutron Polymers Ltd., Finolex Industries Ltd., Geberit International AG, IPEX BRANDING INC., JM Eagle Inc., Kubota Corp., McWane Inc., Pipelife International GmbH, Polypipe Ltd., RIFENG Enterprise Co Ltd., Saudi Arabian Amiantit Co., Tessenderlo Group NV, The Supreme Industries Ltd., Uponor Corp. and Wavin BV

-

Market Research Insights

- Market dynamics are increasingly shaped by a focus on efficiency and sustainability. The adoption of prefabricated plumbing modules, guided by building information modeling (BIM), is streamlining construction, while the push for green building certifications makes sustainable plumbing materials a priority.

- Smart plumbing solutions integrated with leak detection systems address water conservation plumbing goals, which is critical for both residential plumbing renovation and new commercial building infrastructure. Firms are navigating raw material price volatility and complex supply chain logistics to deliver systems for industrial fluid transport and public sanitation projects.

- The focus on water quality assurance drives compliance with lead-free plumbing regulations. For example, new joining methods reduce installation times by over 50%, a key metric in aging infrastructure replacement. Moreover, innovations in seismic resilient piping are becoming vital in vulnerable regions, showcasing the industry’s response to diverse environmental and operational demands.

We can help! Our analysts can customize this plumbing pipes market research report to meet your requirements.

RIA -

RIA -