Point Of Care Data Management Software Market Size 2024-2028

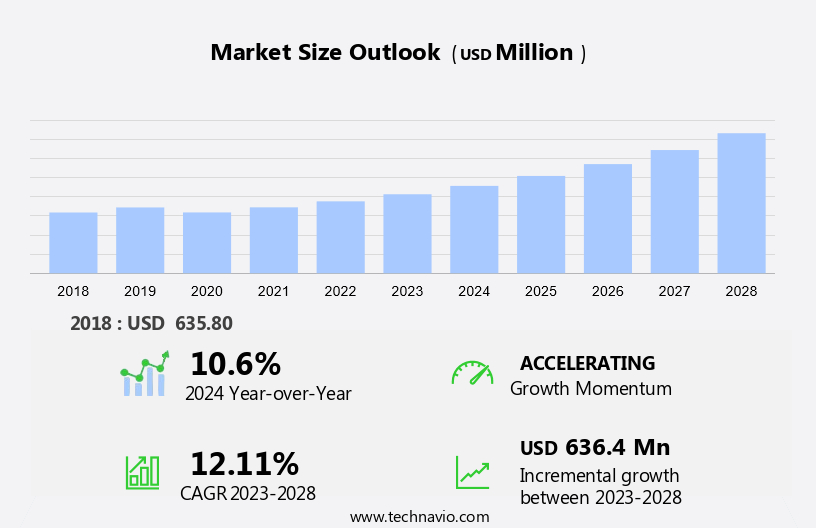

The point of care data management software market size is forecast to increase by USD 636.4 million, at a CAGR of 12.11% between 2023 and 2028.

- The market is experiencing significant growth due to several key drivers. Firstly, the elimination of human errors in data entry and processing is a major advantage, leading to improved accuracy and efficiency in healthcare delivery. Secondly, the rising initiatives for the adoption of Electronic Health Records (EHRs) have created a demand for POC data management software, enabling seamless data access and sharing among healthcare providers. However, privacy and security concerns remain a challenge, as sensitive patient information must be protected. Market trends include the integration of artificial intelligence and machine learning technologies to enhance data analysis and decision-making capabilities, as well as the increasing use of cloud-based solutions for remote access and real-time data sharing. Overall, the POC data management software market is expected to continue its growth trajectory, driven by these factors and the increasing need for efficient and accurate data management in healthcare.

What will be the Size of the Market During the Forecast Period?

- The market is witnessing significant growth due to the increasing adoption of POC testing in hospitals and clinics. POC testing allows doctors and nurses to make quick decisions based on real-time patient data, especially in critical care units such as ICUs. The market is driven by the rising prevalence of infectious diseases, lifestyle-related diseases, and cardiac diseases, which require timely diagnosis and treatment. POC testing is increasingly being used for diseases like diabetes, where continuous monitoring of blood glucose levels is essential. The market for home-based POC devices is also growing rapidly, especially for diabetes patients who require regular monitoring.

- Electronic Health Records (EHR) and healthcare data analytics are essential components of POC data management software, enabling patient-centered care and population health management. The market for POC data management software includes various types of devices such as blood gas analyzers, SmartICUs, and rapid tests. Chronic lower respiratory diseases are a significant application area for POC testing and data management software. Medical centers and critical care units are the major end-users of POC data management software, and the market is expected to grow at a steady pace in the coming years.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

- On-premises

- Cloud

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

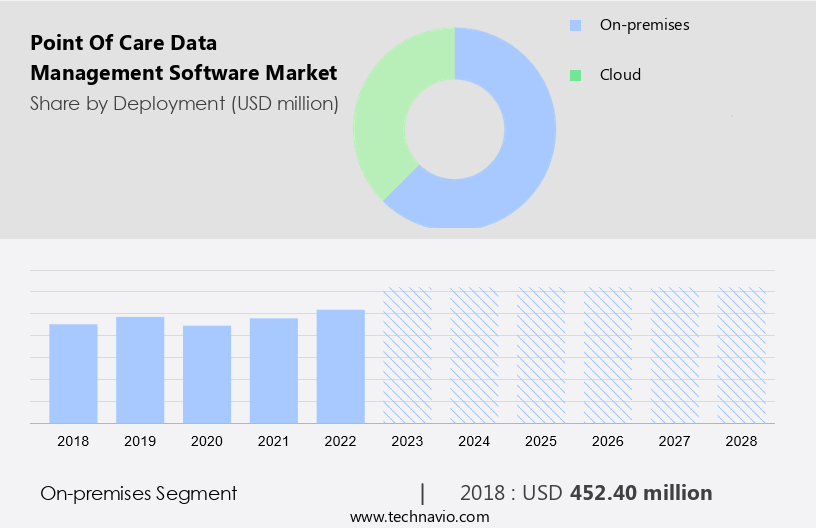

By Deployment Insights

- The on-premises segment is estimated to witness significant growth during the forecast period.

Point of Care (POC) technologies have revolutionized healthcare by enabling real-time diagnosis and treatment of various diseases at the bedside or in clinics. Hospitals and diagnostic clinics are major end-users of POC data management software, which facilitates patient flow, improves communication between doctors and nurses, and enhances patient-centered care. POC testing plays a crucial role in managing infectious diseases, lifestyle-related diseases, and chronic conditions such as diabetes, cardiac diseases, and respiratory diseases like COPD and asthma. Home-based POC devices have gained popularity among diabetes patients, enabling self-monitoring and remote monitoring by healthcare providers. Electronic Health Records (EHR) and healthcare data analytics are integral components of POC data management software, allowing for population health management and critical care units' effective management.

ICUs and critical care units require real-time data analysis to ensure optimal patient care, making POC data management software indispensable. Blood gas analyzers, such as SmartICU, are essential POC devices used in critical care units to monitor patients' oxygen levels and acid-base balance. NTT DATA, Roche, Glytec, MEDITECH, and DataLink Software are prominent players in the POC data management market. Rapid tests for infectious diseases and chronic lower respiratory diseases are also critical applications of POC data management software. The market for POC data management software is expanding in geographic markets, with CLIA-waived tests and PRM solutions gaining popularity.

Get a glance at the market report of share of various segments Request Free Sample

The on-premises segment was valued at USD 452.40 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

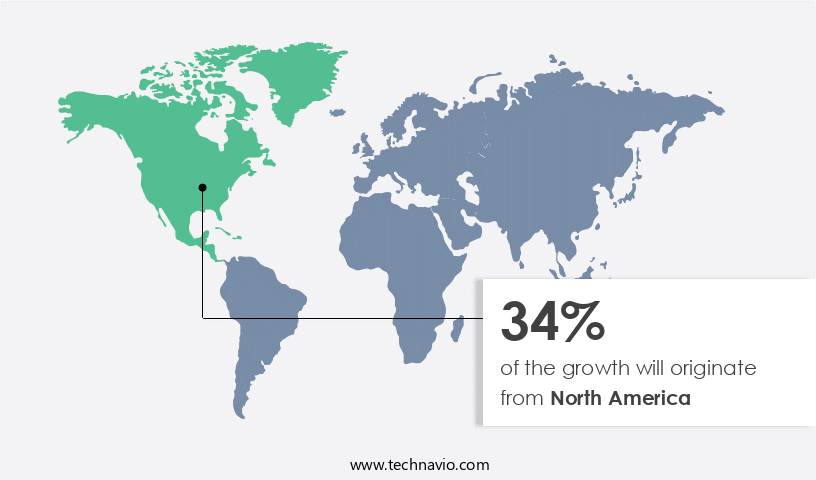

- North America is estimated to contribute 34% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Point of Care (POC) technologies have revolutionized healthcare delivery in hospitals and clinics by enabling quick and accurate diagnosis of various conditions, including infectious diseases, cardiac diseases, diabetes, and lifestyle-related diseases. Doctors and nurses in ICUs and critical care units can now make informed decisions in real-time using POC testing devices such as blood gas analyzers and smart ICUs. POC technologies are not limited to hospitals; home-based POC devices are increasingly popular, particularly among diabetes patients for insulin management. Electronic Health Records (EHR) and healthcare data analytics play a crucial role in patient-centered care and population health management. POC technologies integrate seamlessly with EHR systems, providing real-time data access.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Point Of Care Data Management Software Market?

POC data management software eliminates human errors is the key driver of the market.

- The management of extensive patient data in healthcare settings, particularly for Point of Care Tests (POCT), can be a labor-intensive and costly process when done manually. Traditional methods for maintaining healthcare records are unreliable and prone to human error and data loss. To address these challenges, healthcare providers are increasingly adopting Point of Care Data Management Software. This technology enables the maintenance and management of medical histories and data from various POCT devices, including ultrasound and imaging data, across diverse healthcare and home-based settings. With the rising prevalence of clinical conditions such as diabetes, affecting approximately 425 million adults worldwide, according to the International Diabetes Federation, the demand for POC devices is anticipated to rise.

- This trend is expected to fuel the adoption of POC data management software to streamline daily POC operations and ensure effective patient treatment courses. In addition, the Japanese Nursing Association and various healthcare systems have granted Emergency Use Authorization for rapid molecular tests, further increasing the need for efficient POC data management systems. Electronic Medical Records (EMR) and POCT management systems are being integrated to enhance the overall functionality of healthcare systems, making POC data management software an indispensable tool for healthcare providers.

What are the market trends shaping the Point Of Care Data Management Software Market?

Rising initiatives for the adoption of Electronic Health Records is the upcoming trend in the market.

- The adoption of digital health collaboration and Point of Care Testing (POCT) management systems is gaining momentum in healthcare, driven by initiatives such as the Health Information Technology for Economic and Clinical Health (HITECH) Act of 2009 in the US, which promotes the use of electronic health records (EHR) in healthcare facilities. In 2015, the Centers for Medicare and Medicaid Services (CMS) and the Office of the National Coordinator for Health IT (ONC) in the US endorsed the concept of EHR-meaningful use, which mandates the use of certified EHR technology to facilitate efficient electronic exchange of healthcare-related information. This, in turn, enhances patient outcomes and improves clinical conditions.

- POCT management systems, including those for imaging data from ultrasound and other diagnostic tools, are increasingly being integrated into home-based POC devices. Companies like Glucommander and Ambra Health are leading the way in this area. The International Diabetes Federation and the Japanese Nursing Association are also advocating for the use of POCT systems to manage chronic conditions. Rapid molecular tests are also being given emergency use authorization, further expanding the scope of POCT systems in healthcare. The integration of POCT systems with EMRs in healthcare systems is expected to streamline workflows and improve patient care.

What challenges does Point Of Care Data Management Software Market face during the growth?

Privacy and security concerns is a key challenge affecting the market growth.

- Point of Care (POC) data management software plays a crucial role in digital health collaboration by facilitating the efficient handling of imaging data from ultrasounds, home-based POC devices, and rapid molecular tests. Companies such as Glucommander and Ambra Health are leading providers of POC data management systems, enabling seamless integration with electronic medical records (EMR) and healthcare systems. These systems enable clinical conditions to be monitored and patient outcomes to be optimized.

- However, the increasing use of POC data management software raises concerns regarding data privacy and security, as it involves the collection and storage of sensitive personal information. The implementation of regulations like the General Data Protection Regulation (GDPR) in the European Union (EU) necessitates that companies comply with stringent data protection standards, ensuring that they only collect and use data with the explicit consent of individuals. In emergency situations, POC data management systems may receive emergency use authorization to facilitate rapid and effective care.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Danaher Corp.

- DataLink Software LLC

- Esaote Spa

- F. Hoffmann La Roche Ltd.

- Hedera Biomedics SRL

- Orchard Software Corp.

- Radiometer Medical ApS

- Randox Laboratories Ltd.

- Seaward Electronic Ltd.

- Siemens Healthineers AG

- TELCOR Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Point of Care (POC) technologies have revolutionized healthcare by enabling quick and accurate diagnosis and monitoring of various health conditions. These technologies are increasingly being adopted in hospitals and clinics to improve patient flow, reduce turnaround time for test results, and enhance patient-centered care. POC testing is particularly useful in managing infectious diseases, cardiac diseases, diabetes, and lifestyle-related diseases such as chronic lower respiratory diseases like COPD and asthma. Doctors and nurses in ICUs and critical care units benefit significantly from POC technologies, with blood gas analyzers and SmartICU systems being popular choices. Home-based POC devices, such as those used for diabetes management, enable patients to monitor their health conditions in real-time and manage their insulin levels effectively.

Further, electronic Health Records (EHR) and healthcare data analytics play a crucial role in POC data management. Companies are at the forefront of developing advanced POC technologies and data management solutions. These solutions help in population health management by providing real-time patient data, enabling timely interventions, and improving overall patient outcomes. Geographic markets like North America and Europe are expected to dominate the POC technologies market due to the presence of well-established healthcare infrastructure and a large patient population. Rapid tests and CLIA-waived tests are also gaining popularity due to their ease of use and quick turnaround time.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.11% |

|

Market growth 2024-2028 |

USD 636.4 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

10.6 |

|

Key countries |

US, China, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -