Polyurethane Dispersions Market Size 2024-2028

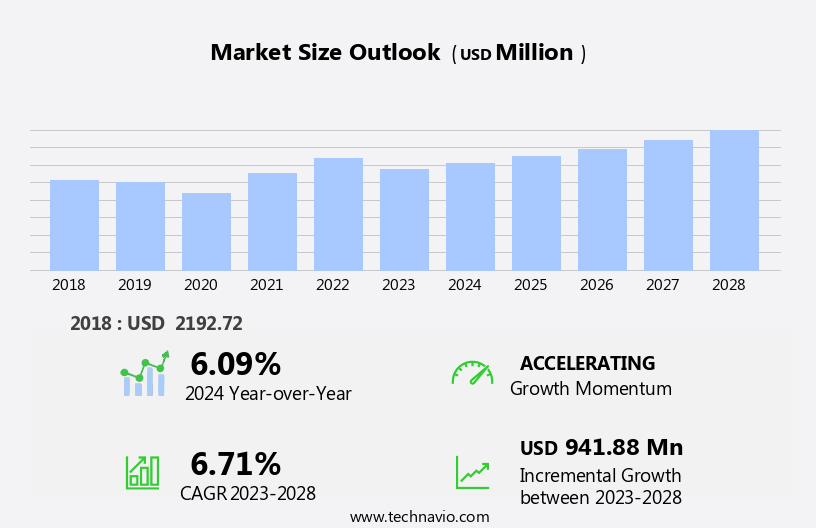

The polyurethane dispersions market size is forecast to increase by USD 941.88 million, at a CAGR of 6.71% between 2023 and 2028.

- The market is experiencing significant growth, driven by the high utilization of these dispersions in various industries, particularly in paints and coatings, due to their superior properties such as excellent adhesion, flexibility, and resistance to chemicals and weather conditions. However, the market faces challenges from increasing regulations on Volatile Organic Compounds (VOC) emissions, which may limit the use of certain types of polyurethane dispersions. To mitigate this, market players are expanding their production facilities to manufacture low-VOC and waterborne polyurethane dispersions. Another trend in the market is the increasing use of acrylic and epoxy resins as alternatives to traditional solvent-borne coatings, which is expected to boost the demand for polyurethane dispersions in this application area.

- Companies seeking to capitalize on market opportunities should focus on developing innovative, eco-friendly products that meet the evolving regulatory requirements while maintaining the desired performance characteristics. Additionally, strategic collaborations and partnerships can help companies expand their reach and enhance their competitive position in the market.

What will be the Size of the Polyurethane Dispersions Market during the forecast period?

The market continues to evolve, driven by the diverse applications across various sectors. Solvent-based polyurethane finds extensive use in roller coating for amusement parks, while biodegradable polyurethane gains traction in the furniture industry. Continuous production methods, such as injection molding and brush coating, are increasingly adopted for their efficiency and cost savings. Colloid chemistry plays a crucial role in the production of moisture cure dispersions, ensuring solid content and dispersion stability. Particle engineering and process optimization are key focus areas for enhancing the performance of high-performance polyurethane in protective coatings, sealants, and adhesives. Flame-retardant polyurethane is a critical component in the electronics industry, providing essential safety regulations compliance.

In the building and construction sector, water-based polyurethane is a sustainable alternative to solventborne dispersions, offering environmental benefits. The chemical resistance and weather resistance properties of polyurethane resins make them ideal for decorative coatings, coatings and paints, and industrial coatings. The application methods and quality control measures in polymer chemistry are continually refined to meet evolving industry standards. Biocompatible polyurethane is a growing area of interest in the medical and healthcare sectors, with one-component dispersions and high solids dispersions offering improved tensile strength and shore hardness. Anti-corrosion coatings and textile finishing also benefit from the use of UV-curable dispersions and vinyl acetate dispersions.

The evolving nature of the market is further shaped by regulatory requirements, with safety regulations and environmental regulations influencing the development of new products and technologies. The market continues to unfold, with ongoing research and innovation in areas such as particle size, abrasion resistance, bio-based polyurethane, and thermal conductivity.

How is this Polyurethane Dispersions Industry segmented?

The polyurethane dispersions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Solvent-free

- Low-solvent

- Application

- Paints and coatings

- Adhesives and sealants

- Leather finishing

- Textile finishing

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- India

- Rest of World (ROW)

- North America

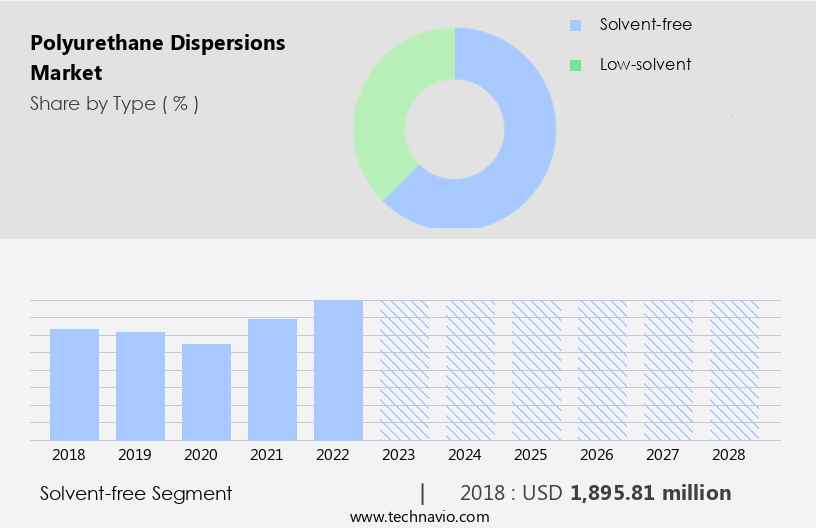

By Type Insights

The solvent-free segment is estimated to witness significant growth during the forecast period.

Low-solvent-borne polyurethane dispersions offer several advantages over traditional solvent-based coatings, making them a popular choice in various industries. In the production process, solvents dissolve the resins and additives in the coating formulation, only to evaporate upon reacting with oxygen post-application. This property enables low-solvent-borne polyurethane coatings to provide superior resistance to high temperatures and humidity in numerous applications. Industrial applications, particularly in sectors like building and construction, electronics, and automotive, heavily rely on these coatings due to their flexible application, fast-drying properties, high gloss, and ability to adhere to diverse substrates. Their exceptional protective qualities against corrosion and excellent adhesion to steel are significant factors driving their extensive usage.

The footwear and sports goods industries also benefit from the use of low-solvent-borne polyurethane dispersions in leather treatment and coatings. Biocompatible polyurethane dispersions cater to the healthcare sector, ensuring safety and sustainability. One-component and high-solids dispersions offer ease of use and reduced environmental impact, while high-performance polyurethane dispersions cater to specific industries requiring enhanced chemical resistance and weather resistance. Water-based polyurethane dispersions, an eco-friendly alternative, are gaining traction in various applications, including coatings, adhesives, and sealants. Epoxy resins and acrylic dispersions are often used in combination with polyurethane dispersions to enhance the performance and properties of the final product.

Regulations governing safety and environmental concerns continue to influence the market dynamics, pushing manufacturers to develop sustainable and biodegradable polyurethane dispersions. Polyethylene, polyvinyl acetate, and polyvinyl chloride are commonly used as raw materials in the production of polyurethane dispersions. Process optimization, particle engineering, and colloid chemistry play a crucial role in enhancing the performance and stability of polyurethane dispersions. Flame-retardant and protective coatings, silicone resins, chain extenders, and tensile strength enhancers are essential additives in the production of polyurethane resins. Injection molding, furniture manufacturing, and roller coating applications utilize continuous production methods to ensure high-quality, consistent results. Brush coating and moisture cure dispersions cater to specific application requirements, while solvent-based polyurethane dispersions maintain their relevance in certain industries.

Polymer chemistry, thermal conductivity, and green polyurethane are emerging trends in the market, as manufacturers strive to develop advanced, high-performance, and eco-friendly polyurethane dispersions. Printing inks and industrial coatings continue to adopt these advanced polyurethane dispersions to cater to diverse customer demands. Quality control, particle size, shore hardness, and abrasion resistance are essential factors that influence the selection and application of polyurethane dispersions. Ensuring dispersion stability and maintaining solid content are critical aspects of the production process.

The Solvent-free segment was valued at USD 1895.81 million in 2018 and showed a gradual increase during the forecast period.

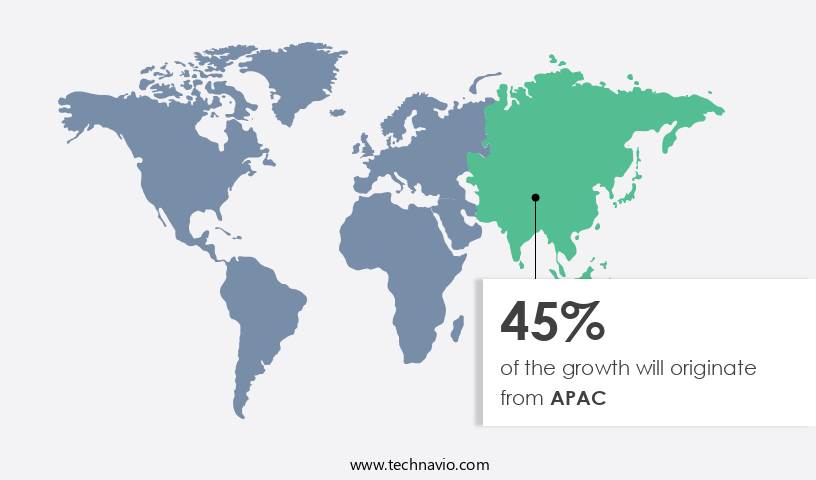

Regional Analysis

APAC is estimated to contribute 45% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth due to increasing demand from various end-use industries, including wood and furniture, electrical and electronics, automotive, and transportation. The expansion in the commercial and residential construction sector is a major driving factor, with renovation and repair projects and foreign direct investments contributing to the market's growth. In APAC, economic growth and rising per capita income have boosted demand for polyurethane dispersions. These dispersions offer advantages such as chemical resistance, weather resistance, and film formation, making them popular choices for coatings and paints, sealants and adhesives, and industrial coatings. The market also caters to specific industries, such as the footwear industry for leather treatment, the sports goods industry for biocompatible polyurethane, and the electronics industry for UV-curable dispersions.

Sustainability is a key trend, with the development of green polyurethane, biodegradable polyurethane, and waterborne dispersions. Additionally, process optimization, particle engineering, and colloid chemistry are crucial for improving solid content, dispersion stability, and particle size. Regulations regarding safety and environmental concerns continue to shape the market, with the need for flame-retardant polyurethane and anti-corrosion coatings. The market's future lies in continuous production, application methods, and polymer chemistry innovations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Polyurethane Dispersions Industry?

- Compliance with stricter regulations on Volatile Organic Compounds (VOC) emissions is the primary market driver, necessitating increased demand for products and technologies that reduce or eliminate VOC emissions.

- Polyurethane Dispersions (PUDs) are a type of waterborne coating that offers excellent chemical resistance, film formation, and surface science properties. These dispersions are gaining popularity due to their environmental benefits, as they contain low or no volatile organic compounds (VOCs), making them an eco-friendly alternative to traditional solvent-based coatings. PUDs are used extensively in various industries, including building and construction, electronics, textile finishing, and sealants and adhesives. In the building and construction sector, PUDs are used for anti-corrosion coatings and weather-resistant paints. In the electronics industry, they are employed in the production of UV-curable dispersions for coatings and printing inks.

- In textile finishing, they are utilized for imparting desirable properties such as water repellency and wrinkle resistance. Sealants and adhesives also benefit from PUDs' chemical resistance and film-forming capabilities. Regulatory bodies are increasingly focusing on reducing VOC emissions due to their contribution to air pollution and smog. For instance, the Volatile Organic Compound Concentration Limits for Certain Products Regulations in Canada under the Canadian Environmental Protection Act, 1999, set maximum concentration limits and emission potentials for VOCs in specific product categories. These regulations are essential for manufacturers and importers to ensure compliance and reduce the environmental impact of their products.

- Polyurethane Dispersions offer a solution to these regulations by providing high-performance coatings with minimal VOC emissions. They are also subject to various safety regulations to ensure safe handling and disposal. Vinyl acetate dispersions and acrylic dispersions are common types of PUDs used in various applications due to their excellent chemical resistance and film formation properties. Polyethylene (PE) and polyvinyl acetate (PVA) are often used as raw materials for producing these dispersions. Overall, the market for Polyurethane Dispersions is expected to grow due to their versatility, environmental benefits, and increasing regulatory requirements.

What are the market trends shaping the Polyurethane Dispersions Industry?

- Market trends indicate an essential expansion of production facilities among market companies. This growth is a significant development in the industry.

- The market is witnessing significant growth due to the increasing demand from various industries, including paints and coatings, automotive, construction, furniture, and others. In response to this trend, companies are expanding their production capacity for polyurethane dispersions. For instance, Covestro recently completed the construction of a new production facility for waterborne polyurethane dispersions in Shanghai, China. This facility will cater to the rising demand for eco-friendly coatings and adhesives in the Asia Pacific region, serving industries such as automotive, construction, furniture, footwear, and packaging. The new production facility will produce waterborne polyurethane dispersions, which offer similar performance profiles as solvent-based dispersions but with improved environmental compatibility.

- Colloid chemistry plays a crucial role in the production of these dispersions, ensuring dispersion stability and particle engineering for optimal process conditions. Additionally, moisture cure dispersions and flame-retardant polyurethane dispersions are gaining popularity in protective coatings applications, particularly in the furniture industry. Silicone resins and chain extenders are commonly used in the production process to enhance the properties of polyurethane dispersions. Overall, the market dynamics are driven by factors such as process optimization, increasing demand for biodegradable polyurethane dispersions, and the growing adoption of continuous production methods in various industries.

What challenges does the Polyurethane Dispersions Industry face during its growth?

- The significant reliance on acrylic and epoxy resins in paint and coating production poses a substantial challenge to the industry's growth trajectory.

- Polyurethane dispersions are a type of polymer resin that offers superior properties for various applications in coatings and paints, printing inks, and industrial coatings. These dispersions are characterized by their small particle size, which allows for easy application using various methods, including air spraying, roll coating, and dip coating. The resulting coatings exhibit excellent tensile strength, shore hardness, abrasion resistance, and thermal conductivity. Polyurethane dispersions are produced through the reaction of polyols and isocyanates in the presence of water. The resulting polymer chemistry provides unique benefits, such as excellent adhesion to various substrates and good chemical resistance.

- Moreover, the use of green polyurethane, which is derived from renewable resources, adds to their environmental appeal. The particle size of polyurethane dispersions is critical for their performance. Smaller particle sizes ensure better dispersion stability and improved flow properties, leading to more uniform coatings. Quality control is essential in the production process to ensure consistent particle size and properties. Compared to traditional solvent-borne polyurethane resins, waterborne dispersions offer several advantages, including reduced VOC emissions, improved health and safety, and easier application. Additionally, bio-based polyurethane dispersions are gaining popularity due to their lower carbon footprint and sustainable production methods.

- Polyurethane dispersions are often compared to polyvinyl chloride (PVC) dispersions, but they offer distinct advantages, such as better flexibility and adhesion properties. The versatility of polyurethane dispersions makes them a popular choice for various industries, including automotive, construction, and electronics.

Exclusive Customer Landscape

The polyurethane dispersions market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polyurethane dispersions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polyurethane dispersions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alberdingk Boley GmbH - The company specializes in providing a range of polyurethane dispersions, including ALBERDINGK AFU 850, CUD 4820 VP, CUR 2021 VP, and CUR 920 VP.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alberdingk Boley GmbH

- BASF SE

- Bolger and Ohearn Inc.

- Bond Polymers International

- C. L. HAUTHAWAY and SONS CORP.

- Capital Resin Corp.

- CHEMCROWN GROUP

- Covestro AG

- DIC Corp.

- Dow Chemical Co.

- Lanxess AG

- Marathwada Chemicals

- Michelman Inc.

- Mitsui Chemicals Inc.

- Nan Pao Resins Co. Ltd.

- PETRONAS Chemicals Group Berhad

- PTT Global Chemical Public Co. Ltd.

- SNP Inc.

- Stahl Holdings B.V.

- The Lubrizol Corp.

- Wanhua Chemical Group Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polyurethane Dispersions Market

- In February 2023, BASF SE, a leading chemical producer, announced the expansion of its production capacity for waterborne polyurethane dispersions (PUDs) at its site in Ludwigshafen, Germany. This expansion is expected to strengthen BASF's position in the global PUD market and cater to the growing demand for sustainable coatings solutions (BASF press release, 2023).

- In November 2022, Covestro AG, another significant player in the polyurethane industry, launched a new line of low-emission, waterborne polyurethane dispersions for the coatings industry. This innovative product development aligns with the increasing market demand for eco-friendly and low-emission coatings (Covestro press release, 2022).

- In June 2021, Wanhua Chemical Group, the world's largest producer of MDI (Methylene Diphenyl Diisocyanate), entered into a strategic partnership with H.B. Fuller Company to develop and commercialize new waterborne PUD technologies. This collaboration is expected to accelerate the growth of the PUD market and offer innovative solutions to customers (Wanhua Chemical press release, 2021).

- In March 2020, Dow Inc. received approval from the European Chemicals Agency (ECHA) for the renewal of the registration of its PUD product line under REACH regulations. This approval ensures the continued availability of Dow's PUDs in the European market and demonstrates the company's commitment to regulatory compliance (Dow Inc. Press release, 2020).

Research Analyst Overview

- The polyurethane dispersions industry continues to evolve, driven by advancements in performance, formulations, and production techniques. Suppliers of polyurethane dispersions strive to meet evolving standards and specifications, ensuring the highest quality products for diverse applications. Innovation is a key focus, with research and development efforts yielding new solutions for enhanced durability and cost-effectiveness. Polyurethane dispersion characterization and testing are essential for evaluating product properties and ensuring consistency. Manufacturing processes have become more efficient, leading to increased production capacity and lower prices.

- Despite these advancements, challenges persist, including the need for sustainable production methods and addressing regulatory requirements. Polyurethane dispersion solutions continue to find opportunities in various industries, including coatings, adhesives, and sealants. The future of the industry looks promising, with ongoing developments in technology and applications. Polyurethane dispersion cost, durability, and properties remain crucial factors in the market, shaping the competitive landscape and driving growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polyurethane Dispersions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.71% |

|

Market growth 2024-2028 |

USD 941.88 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.09 |

|

Key countries |

US, China, India, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polyurethane Dispersions Market Research and Growth Report?

- CAGR of the Polyurethane Dispersions industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polyurethane dispersions market growth of industry companies

We can help! Our analysts can customize this polyurethane dispersions market research report to meet your requirements.

RIA -

RIA -