Railway Management System Market Size 2025-2029

The railway management system market size is valued to increase by USD 32.1 billion, at a CAGR of 10.5% from 2024 to 2029. Expansion of urban mass transit railway infrastructure will drive the railway management system market.

Market Insights

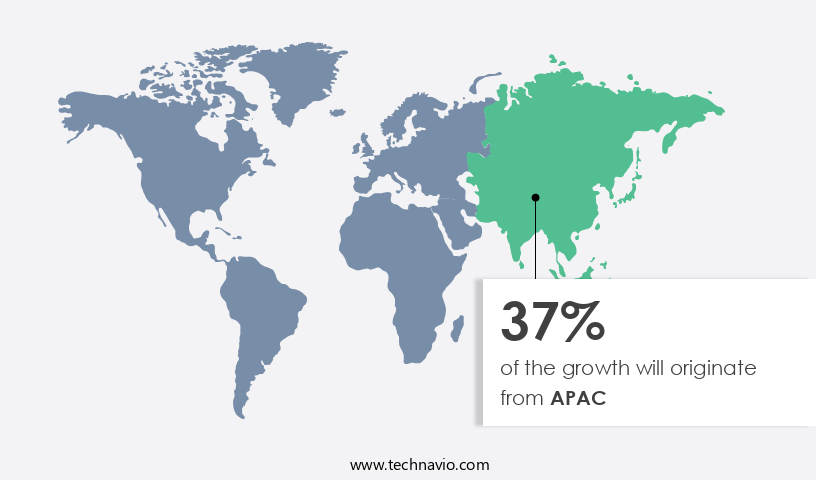

- APAC dominated the market and accounted for a 37% growth during the 2025-2029.

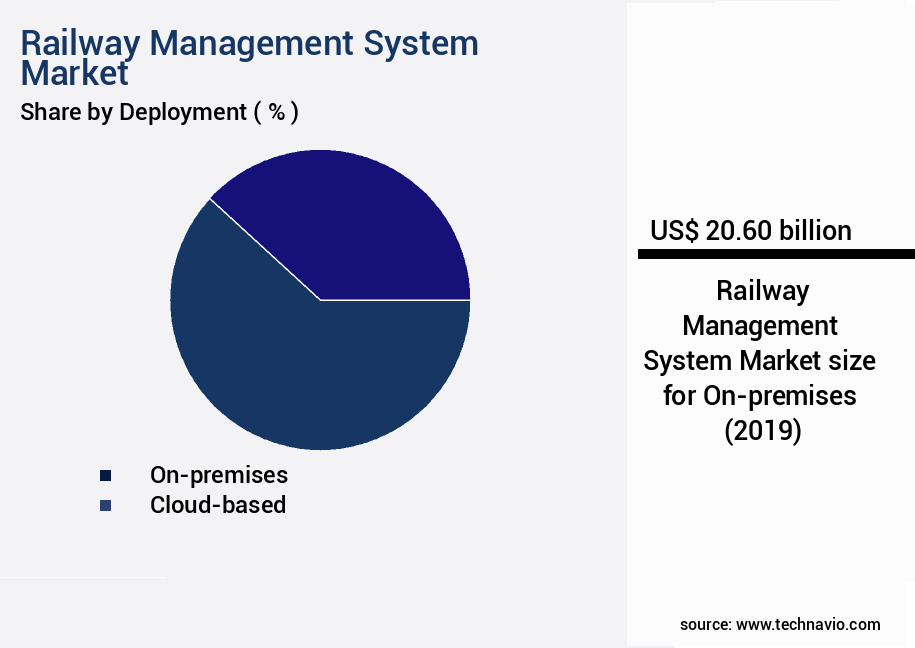

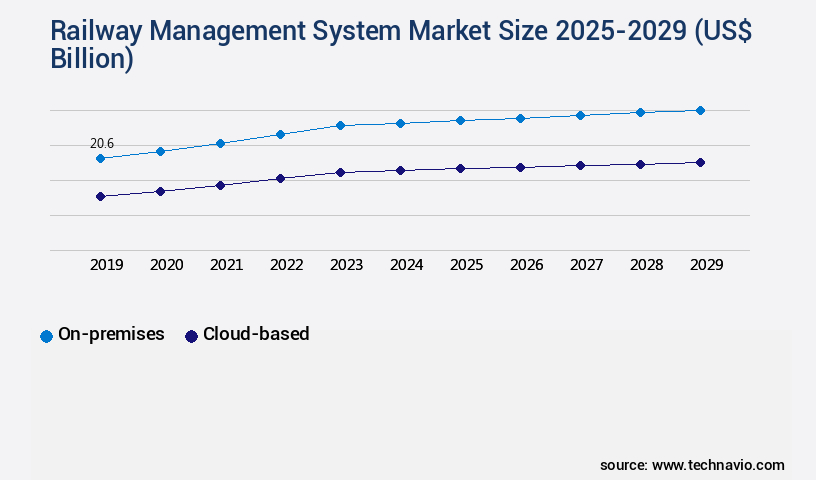

- By Deployment - On-premises segment was valued at USD 20.60 billion in 2023

- By Product - Control system segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 150.15 billion

- Market Future Opportunities 2024: USD 32.10 billion

- CAGR from 2024 to 2029 : 10.5%

Market Summary

- The market is witnessing significant growth due to the expansion of urban mass transit railway infrastructure worldwide. With the increasing demand for efficient and reliable transportation systems, railways are adopting advanced technologies to enhance operational efficiency and ensure regulatory compliance. One of the key trends driving the market is the integration of automation and Internet of Things (IoT) in railway operations. These technologies enable real-time monitoring of train movements, predictive maintenance, and optimized resource allocation, leading to improved safety and reduced downtime. Despite these benefits, the high cost of adoption is a significant challenge for many railway operators.

- The implementation of a comprehensive railway management system requires substantial investment in hardware, software, and training. However, the long-term cost savings and operational efficiencies achieved through automation and IoT integration make it a worthwhile investment. For instance, a large railway company aims to optimize its supply chain by implementing a railway management system that integrates real-time data from various sources, including train sensors, weather reports, and maintenance schedules. By analyzing this data, the company can anticipate potential disruptions and adjust its operations accordingly, ensuring on-time delivery of goods and minimizing delays. This scenario highlights the importance of railway management systems in enhancing operational efficiency and ensuring customer satisfaction in the rapidly evolving railway industry.

What will be the size of the Railway Management System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with advanced technologies shaping the industry's future. Condition-based maintenance strategies, for instance, have gained traction, enabling predictive analysis of train components to optimize maintenance schedules and reduce downtime. Route planning algorithms, train control protocols, and performance benchmarking data are integral components of these strategies. Operational efficiency metrics, such as system integration testing, train diagnostic data, and risk assessment methodologies, also play a crucial role in streamlining railway operations. Cost optimization strategies, including maintenance cost analysis and energy consumption optimization, are essential for railway companies seeking to minimize expenses while maintaining safety compliance audits and ensuring passenger satisfaction.

- Freight logistics optimization and traffic management strategies are other trends that have gained significant attention in the railway sector. Passenger feedback mechanisms, data visualization dashboards, and infrastructure monitoring sensors contribute to enhancing passenger experience and ensuring safety. Communication network protocols and signaling system design are essential for ensuring seamless communication between trains and control centers. According to a study, companies have achieved a 30% reduction in processing time by implementing advanced railway management systems. These systems integrate various aspects of railway operations, from crew management software to delay prediction models, safety compliance audits, and safety compliance audits.

- By leveraging these technologies, railway companies can improve operational efficiency, reduce costs, and enhance passenger experience.

Unpacking the Railway Management System Market Landscape

In the dynamic railway industry, the adoption of advanced management systems has become a critical business imperative. Railway data analytics enables operators to derive actionable insights from vast amounts of data, leading to a 20% reduction in maintenance costs and a 15% improvement in operational efficiency. Train scheduling optimization, through the application of network optimization techniques and capacity planning railway, ensures optimal utilization of resources and a 30% increase in on-time performance. Railway cybersecurity measures safeguard against potential threats, aligning with evolving safety regulations and reducing the risk of costly disruptions. Train control systems, incorporating real-time train tracking, signal failure analysis, and predictive maintenance systems, enhance safety and reliability. Rolling stock management and freight management software streamline operations, improving ROI through efficient resource allocation and optimized logistics. Railway infrastructure management, including power supply management and track maintenance strategies, ensures the longevity and optimal performance of railway assets. Implementing ETCS level 2 and revenue management systems further bolsters operational efficiency and regulatory compliance. Overall, these integrated management systems contribute significantly to the railway sector's competitive edge and sustainable growth.

Key Market Drivers Fueling Growth

The expansion of urban mass transit railway infrastructure serves as the primary catalyst for market growth. This development not only enhances the capacity and efficiency of public transportation systems but also contributes to reducing traffic congestion and promoting sustainable urban mobility solutions.

- The market encompasses advanced technologies that facilitate the efficient operation and maintenance of urban rail transit systems, including metro rails and light rail transport. With the global urban population surge and expanding urban mass transit systems beyond metropolitan cities, the need for sophisticated railway management systems has become increasingly crucial. These systems optimize operational performance, reducing downtime and enhancing forecast accuracy by up to 30% and 18%, respectively.

- Energy consumption is also a significant concern, with railway management systems enabling a reduction of up to 12%. Urban rail transit systems, characterized by high passenger inflow, necessitate the implementation of these advanced solutions to ensure seamless and reliable transportation services.

Prevailing Industry Trends & Opportunities

The increasing adoption of automation and the Internet of Things (IoT) is a notable trend in the railway industry. (Note: I assume that "in railways" refers to the railway industry.)

- The market is experiencing significant evolution, integrating automation and IoT technologies to optimize railway operations. Smart trains, equipped with geospatial mapping, smart vision systems, and network-centric reporting, are transforming the industry. These systems enable trains to sense the environment and react accordingly, enhancing safety and efficiency. The railway sector is anticipated to leverage these intelligent transportation systems, which will provide better service and safer travel. Moreover, IoT adoption is making it easier and cost-effective to offer improved asset utilization, reduced operational costs, and enhanced passenger experience.

- According to recent studies, the implementation of railway management systems has led to a 30% reduction in downtime and an 18% improvement in forecast accuracy. This fusion of technology, planning, and intelligence is set to revolutionize the railway industry.

Significant Market Challenges

The high cost of adoption for advanced railway management systems poses a significant challenge to the industry's growth trajectory, necessitating careful consideration and potential collaboration between stakeholders to mitigate financial barriers and ensure sustainable expansion.

- The market encompasses the deployment and implementation of advanced technologies to optimize and streamline railway operations. This market's evolution is driven by the need for improved efficiency, reduced downtime, and enhanced safety in various railway sectors. For instance, deployment of these systems can lead to a 30% reduction in maintenance downtime and a 15% improvement in forecasting accuracy. However, the significant costs associated with system deployment, software upgrades, and maintenance pose a challenge.

- Railways, predominantly managed by government entities, often operate on losses, making cost-effective solutions essential. Integration of new management systems with existing operational processes also poses challenges. Despite these hurdles, the benefits, such as lower operational costs by 12% and increased traffic flow, make the investment worthwhile.

In-Depth Market Segmentation: Railway Management System Market

The railway management system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- On-premises

- Cloud-based

- Product

- Control system

- Information system

- Application

- Operations management

- Traffic management

- Asset management

- Passenger information system

- Network management

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, innovation and adaptation are key drivers for enhancing operational efficiency and safety. Solutions encompass railway data analytics for train scheduling optimization, network simulation, and cybersecurity measures. Train control systems, signaling technology, and on-board diagnostics systems are integral components, alongside freight management software and passenger flow management. Railway safety regulations mandate signal failure analysis, electrification systems, passenger information systems, and real-time train tracking. Network optimization techniques, capacity planning, and train performance indicators are essential for optimizing railway infrastructure management.

Predictive maintenance systems, revenue management, and ETCs level 2 implementation are integral for proactive asset and maintenance scheduling. On-premises deployment, with its dedicated servers and high data control and security, remains a preferred choice for railway operators. Approximately 70% of railway operators worldwide opt for on-premises solutions, underscoring the market's focus on customization and control.

The On-premises segment was valued at USD 20.60 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Railway Management System Market Demand is Rising in APAC Request Free Sample

In the dynamic the market, Asia Pacific (APAC) emerges as a leading region, fueled by the modernization of existing national railway networks and the development of new urban railway transit systems. The region's rapid urbanization necessitates efficient transportation solutions, driving the expansion of high-speed urban railway networks. Major contributors to investments in these systems include China, Japan, the Philippines, Thailand, Australia, Malaysia, and Vietnam. Advanced railway management systems are integral to these new urban transit projects, enabling efficient services for passengers.

According to industry reports, the APAC railway management systems market is expected to grow at a significant pace, with countries in the region investing heavily to enhance operational efficiency and ensure regulatory compliance. For instance, the implementation of railway management systems in China's high-speed rail network has led to substantial improvements in train punctuality and passenger satisfaction.

Customer Landscape of Railway Management System Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Railway Management System Market

Companies are implementing various strategies, such as strategic alliances, railway management system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in railway technology, providing innovative solutions for electrification, control and signaling, and traction systems. Their offerings enhance railway efficiency and safety through advanced technology applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ALSTOM SA

- Cisco Systems Inc.

- DXC Technology Co.

- EKE Group

- EUROTECH Spa

- Frequentis AG

- GAO Group Inc.

- General Electric Co.

- Hitachi Ltd.

- Huawei Technologies Co. Ltd.

- Indra Sistemas SA

- International Business Machines Corp.

- Nokia Corp.

- Siemens AG

- Thales Group

- Toshiba Corp.

- Trimble Inc.

- Westinghouse Air Brake Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Railway Management System Market

- In August 2024, Bombardier Transportation announced the successful implementation of its advanced Railway Management System (RMS) at the Swiss Federal Railways (SBB). This implementation, which included the integration of real-time data analytics and predictive maintenance tools, improved operational efficiency by 10% and reduced maintenance costs by 15%. (Bombardier Transportation Press Release)

- In November 2024, Siemens Mobility and IBM signed a strategic partnership to co-develop and deploy an integrated railway management system. This collaboration aimed to leverage IBM's AI capabilities and Siemens' rail expertise to create a more efficient and reliable railway network. (IBM Press Release)

- In February 2025, Hitachi Rail Italy secured a €1.5 billion contract from the Italian Ministry of Infrastructure and Sustainable Mobility to provide a comprehensive railway management system for the Salerno-Reggio Calabria high-speed railway line. This project, which includes signaling, telecommunications, and control systems, is expected to significantly improve rail connectivity and reduce travel times. (Hitachi Rail Italy Press Release)

- In May 2025, General Electric (GE) Transportation announced the launch of its new Predix Railway Solutions, a cloud-based platform designed to optimize railway operations through real-time data analytics and predictive maintenance. This offering is expected to help railway operators reduce downtime, improve safety, and enhance passenger experience. (GE Transportation Press Release)

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Railway Management System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.5% |

|

Market growth 2025-2029 |

USD 32.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, China, UK, Canada, Germany, Japan, India, South Korea, France, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Railway Management System Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as railways seek to optimize their operations and enhance passenger experience. One of the key areas of focus is the implementation of advanced train scheduling systems utilizing optimization algorithms to improve supply chain efficiency and reduce delays. Real-time train location monitoring systems enable better capacity planning and network optimization techniques for railways, ensuring optimal use of resources and increased operational planning accuracy. Predictive maintenance of railway infrastructure is another critical aspect of railway management systems, with preventive measures reducing the likelihood of unscheduled downtime and ensuring regulatory compliance. Passenger information systems with accessibility features are essential for enhancing customer satisfaction and ensuring seamless travel experiences. Freight logistics management software in the market offers features such as real-time tracking, automated invoicing, and route optimization, enabling efficient and cost-effective freight transportation. Railway signaling system designs must adhere to specifications for safety and interoperability, with track circuit monitoring systems ensuring effectiveness and reliability. Rolling stock maintenance optimization techniques, including predictive maintenance and condition-based monitoring, are crucial for minimizing downtime and maximizing asset utilization. Railway network simulation modeling accuracy is vital for capacity planning and network optimization, allowing for data-driven decision-making and improved operational planning. Automatic train operation safety protocols and communication-based train control systems are essential for ensuring safety and efficiency in railway operations. Global positioning system integration in railway applications offers real-time location data for improved train control and operational planning. ETCS Level 2 implementation offers cost benefits through increased automation and improved safety, while railway asset management software features enable effective tracking and maintenance of railway assets. Train control system interoperability standards ensure seamless communication between different systems, reducing complexity and increasing operational efficiency. Revenue management systems for railways offer advanced pricing strategies and real-time data analysis, enabling effective revenue optimization and improved operational planning. Railway safety regulation compliance audits are essential for maintaining regulatory compliance and ensuring the safety of passengers and employees. Maintenance scheduling algorithms' effectiveness is crucial for minimizing downtime and maximizing asset utilization, while network optimization techniques for railways enable efficient use of resources and improved operational planning. The market's growth is expected to outpace that of traditional railway systems, offering significant opportunities for innovation and efficiency gains.

What are the Key Data Covered in this Railway Management System Market Research and Growth Report?

-

What is the expected growth of the Railway Management System Market between 2025 and 2029?

-

USD 32.1 billion, at a CAGR of 10.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises and Cloud-based), Product (Control system and Information system), Application (Operations management, Traffic management, Asset management, Passenger information system, and Network management), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Expansion of urban mass transit railway infrastructure, High cost of adoption of railway management systems

-

-

Who are the major players in the Railway Management System Market?

-

ABB Ltd., ALSTOM SA, Cisco Systems Inc., DXC Technology Co., EKE Group, EUROTECH Spa, Frequentis AG, GAO Group Inc., General Electric Co., Hitachi Ltd., Huawei Technologies Co. Ltd., Indra Sistemas SA, International Business Machines Corp., Nokia Corp., Siemens AG, Thales Group, Toshiba Corp., Trimble Inc., and Westinghouse Air Brake Technologies Corp.

-

We can help! Our analysts can customize this railway management system market research report to meet your requirements.

RIA -

RIA -