Rare Hemophilia Factors Market Size 2024-2028

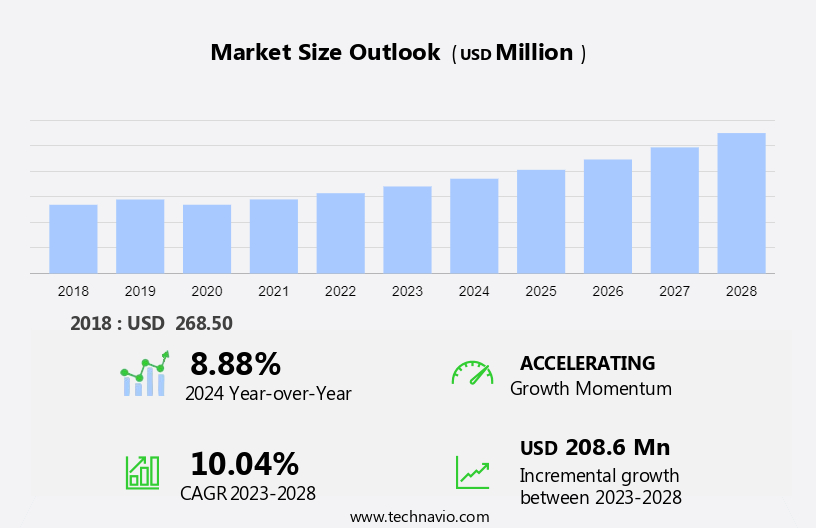

The rare hemophilia factors market size is forecast to increase by USD 208.6 million, at a CAGR of 10.04% between 2023 and 2028.

- The market is experiencing significant growth due to the approval of new treatment techniques, such as gene therapy. This innovative approach holds the potential to provide a long-term cure for hemophilia by addressing the root cause of the disease. However, the high cost and complexity of gene therapy may limit its widespread adoption. Traditional treatments, including blood plasma, hormone replacement therapy, and intravenous immunoglobulins, continue to dominate the market. The ongoing threat of HIV transmission through blood plasma-derived products remains a challenge, necessitating the development of safer alternatives. The market trends and analysis report delve deeper into these factors, providing insights into the growth prospects and challenges of the hemophilia factors market.

What will be the Size of the Rare Hemophilia Factors Market During the Forecast Period?

- The market encompasses the production and distribution of various coagulation factors, including Factor VIII (FVIII) and other clotting factors, for the treatment of hemophilia and related conditions. This market caters to a diverse patient population, including those with acquired hemophilia and autoimmune illnesses such as polymyalgia rheumatica. Key drivers for market growth include the increasing prevalence of hemophilia and the demand for effective treatment options to mitigate bleeding episodes. Funding from organizations like the World Hemophilia Federation and ongoing development efforts in biotechnology contribute to the market's expansion. Innovations such as bi-specific monoclonal antibodies and advanced therapeutics, like immunoglobulins and cryoprecipitate, are revolutionizing the treatment landscape.

- Consumption patterns are influenced by factors such as patient outcomes and the availability of alternative treatment options, like plasma transfusion using fresh frozen plasma. The adjacent market for hepatitis C virus treatment also impacts the market due to the potential for co-infection among patients. Overall, the market is poised for significant revenue growth as advancements in technology and therapeutics continue to transform the treatment landscape for hemophilia patients.

How is this Rare Hemophilia Factors Industry segmented and which is the largest segment?

The rare hemophilia factors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Method

- Fresh frozen plasma

- Factor concentrates

- Cryoprecipitate

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- Japan

- Rest of World (ROW)

- North America

By Method Insights

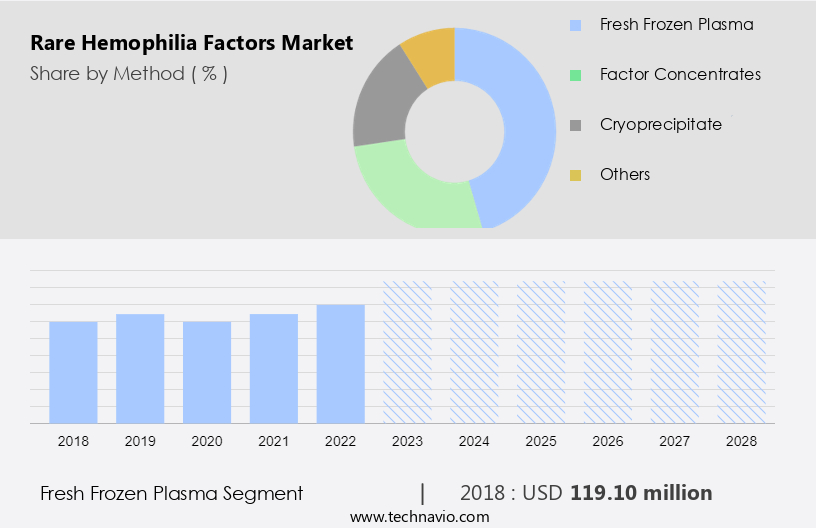

- The fresh frozen plasma segment is estimated to witness significant growth during the forecast period.

Fresh Frozen Plasma (FFP), derived from the liquid component of whole blood, is a vital blood product used to address low levels of clotting factors or deficient blood proteins in patients, indicated by prolonged International Normalized Ratio (INR) and activated Partial Thromboplastin Time (aPTT) values exceeding 1.5 and 2 times the normal range, respectively. FFP increases coagulation factors by approximately 3% in an average-sized adult, making it an essential treatment for coagulopathic bleeding, typically requiring a dose of 10 to 15 ml/kg (approximately four units). However, FFP should not be used for intravascular volume expansion and is often overutilized in cardiac surgery patients, where the primary hemostatic issue is usually platelet dysfunction.

Autoimmune illnesses, such as Autoimmune Hemophilia and Polymyalgia Rheumatica, and conditions like Hepatitis C virus, can lead to the need for FFP. Development of therapeutics like Bi-specific monoclonal antibodies, immunoglobulins, and clotting factors, as well as plasma transfusion alternatives, are ongoing to improve patient outcomes and reduce FFP consumption. The market is influenced by various macro and micro trends, including funding, geopolitical influences, natural disasters, climate change, economic impact, economic policies, social and ethnic concerns, demographic changes, and supply chain dynamics. The market is expected to experience revenue growth in the biotechnology and life sciences sectors, driven by ongoing development efforts and increasing treatment options for bleeding disorders like Hemophilia.

Get a glance at the Rare Hemophilia Factors Industry report of share of various segments Request Free Sample

The fresh frozen plasma segment was valued at USD 119.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

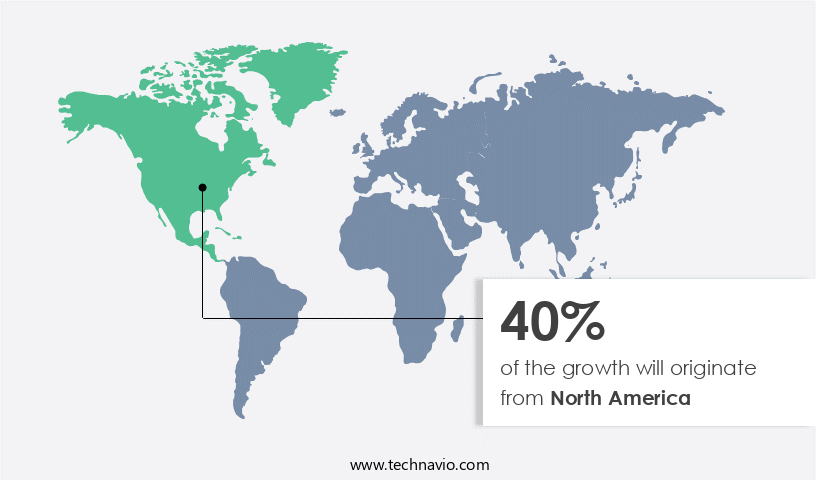

- North America is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is experiencing steady growth due to the significant patient population afflicted with hemophilia, an inherited disorder that impairs the production of clotting factors In the body. Approximately 20,000 individuals In the United States have hemophilia A, a common type of hemophilia that predominantly affects males, leading to prolonged bleeding during injuries. Acquired hemophilia, autoimmune illnesses like polymyalgia rheumatica, hepatitis C virus, and other factors can also contribute to the need for hemophilia factor treatments. North America holds the largest market share, with the US accounting for a substantial portion of the revenue. Development of therapeutics, such as bi-specific monoclonal antibodies, FVIII, and immunoglobulins, is a key trend driving market growth.

Plasma transfusion, fresh frozen plasma, and cryoprecipitate remain traditional treatment options. Disseminated intravascular coagulation, liver disease, food, and drug administration regulations, bleeding disorders, and demographic changes influence market dynamics. The market is also impacted by geopolitical influences, natural disasters, climate change, economic policies, and social, ethnic concerns. The total revenue for the market is expected to grow, with expenses primarily driven by research and development, manufacturing, and distribution costs.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Rare Hemophilia Factors Industry?

Approval of new treatment techniques is the key driver of the market.

- Coagulation disorders, including Acquired Hemophilia, are characterized by bleeding episodes that can significantly impact patients' quality of life. Traditional treatment options have included replacement therapy with whole blood, fresh frozen plasma, and specific factor concentrates. However, recent therapeutic approvals have expanded treatment choices for patients with hemophilia, offering safer and more effective solutions. One such advancement is the development of extended half-life therapeutics, which address the limitations of current prophylaxis treatments, particularly for hemophilia B. These novel therapeutics improve patient outcomes by reducing injection frequency and achieving higher trough concentrations. Autoimmune illnesses, such as Polymyalgia rheumatica, and viral infections, like Hepatitis C virus, can complicate hemophilia treatment.

- Factors such as Disseminated intravascular coagulation, Liver disease, and Food and Drug Administration (FDA) regulations also influence treatment consumption patterns. Funding, economic policies, and geopolitical influences can impact the market's economic scenario. Biotechnology and Life Sciences companies are investing In the development of new coagulation factors, including Bi-specific monoclonal antibodies, Immunoglobulins, and Clotting factors. Risk analysis, including natural disasters and climate change, can disrupt the supply chain and distribution of these essential therapeutics. The legal scenario and social, ethnic concerns also influence market trends. Demographic changes and economic impact further shape the market landscape.

What are the market trends shaping the Rare Hemophilia Factors Industry?

The advent of gene therapy is the upcoming market trend.

- The market has witnessed notable progress in addressing hemophilia treatment. Various therapeutic approaches are under development, including gene therapy. In gene therapy, the faulty gene responsible for hemophilia A or B is extracted from the patient, genetically modified, and reintroduced. The objective is to establish a stable insertion and expression of the gene. Although an approved gene therapy for hemophilia does not currently exist, ongoing research is dedicated to discovering a potential cure. Autoimmune illnesses, such as polymyalgia rheumatica, and viral infections, like Hepatitis C, can trigger bleeding episodes in hemophiliacs. These complications necessitate the consumption of coagulation factors like FVIII and immunoglobulins.

- Plasma transfusion, using fresh frozen plasma or cryoprecipitate, is a common treatment. However, the risks associated with plasma transfusion, such as the potential for disease transmission and allergic reactions, necessitate the exploration of alternative therapies. Funding from organizations like the World Hemophilia Federation and regulatory approvals from the Food and Drug Administration are crucial for the development of new therapeutics. Bi-specific monoclonal antibodies and clotting factors are among the treatment options under consideration. Disseminated intravascular coagulation, liver disease, and other complications can significantly impact patient outcomes and consumption patterns in the market. Geopolitical influences, natural disasters, climate change, economic policies, social and ethnic concerns, demographic changes, and supply chain dynamics are among the macro and micro trends shaping the market.

What challenges does the Rare Hemophilia Factors Industry face during its growth?

Cost-intensive and complex treatment is a key challenge affecting the industry growth.

- Hemophilia, a bleeding disorder, is characterized by deficiencies in coagulation factors, specifically Factor VIII for Hemophilia A and Factor IX for Hemophilia B. Acquired hemophilia, an autoimmune illness, can also lead to deficiencies. Treatment options include plasma transfusions, such as fresh frozen plasma, cryoprecipitate, and immunoglobulins, and clotting factors, including FVIII. However, these treatments come with challenges. Recombinant FVIII therapies can develop inhibitors, limiting their effectiveness. Plasma-based therapies carry the risk of transmission of viruses like Hepatitis C. The World Hemophilia Federation reports that approximately 30% of hemophilia A patients on therapy experience adverse immunogenic reactions. Development efforts In therapeutics include bi-specific monoclonal antibodies and other advanced treatments.

- Market dynamics include the economic impact of hemophilia treatment, geopolitical influences, natural disasters, and demographic changes. Funding and economic policies play a significant role in market growth. The total revenue for hemophilia factors is projected to grow, driven by increasing patient populations and demand for more effective, safer treatments. Market risks include legal scenarios and supply chain disruptions. Adjacent markets, such as liver disease and food, also influence market trends. Immunoglobulins and clotting factors are crucial resources in hemophilia treatment. Despite challenges, the biotechnology and life sciences industries remain committed to improving patient outcomes and addressing consumption patterns.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, rare hemophilia factors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alnylam Pharmaceuticals Inc.

- Aptevo Therapeutics Inc.

- Bayer AG

- Bio Products Laboratory Ltd.

- CSL Ltd.

- F. Hoffmann La Roche Ltd.

- Genentech Inc.

- Grifols SA

- Gyre Therapeutics Inc.

- Intermountain Healthcare

- Kedrion Spa

- Novo Nordisk AS

- Octapharma AG

- Pfizer Inc.

- Sanofi SA

- Takeda Pharmaceutical Co. Ltd.

- The Johns Hopkins Health System Corp.

- UCSF Health

- uniQure NV

- Versiti

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of coagulation factors and related therapeutics used to treat various bleeding disorders. These disorders include, but are not limited to, acquired hemophilia and autoimmune illnesses such as polymyalgia rheumatica. Hemophilia, a genetic disorder characterized by the absence or deficiency of clotting factors, is a primary focus within this market. The treatment landscape for hemophilia has evolved significantly over the past few decades, with a shift from traditional plasma-derived products like fresh frozen plasma (FFP), cryoprecipitate, and immunoglobulins towards recombinant coagulation factors, particularly Factor VIII (FVIII). This transition has been driven by advancements in biotechnology and the life sciences, enabling the production of more effective and safer therapeutic options.

Further, bi-specific monoclonal antibodies represent a promising development in the hemophilia factors market. These antibodies have the potential to target specific antigens and enhance the efficacy of FVIII, reducing the frequency of bleeding episodes and improving patient outcomes. However, the development of these advanced therapies comes with increased costs and resource requirements. The hemophilia factors market is influenced by various macro and micro trends. Macro trends include geopolitical influences, natural disasters, and climate change, which can impact supply chain and distribution. Micro trends include demographic changes, social and ethnic concerns, and economic policies, which can influence consumption patterns and revenue growth.

In addition, risk analysis plays a crucial role In the hemophilia factors market. The risk of developing hemophilia through exposure to the hepatitis C virus (HCV) is a significant concern, as HCV can lead to chronic infection and potential liver disease. Food and drug administration regulations also impact the market, ensuring the safety and efficacy of therapeutic options. The hemophilia factors market is not without challenges. Disseminated intravascular coagulation (DIC) and other complications associated with the use of coagulation factors and related therapeutics can pose risks to patients. Additionally, the high cost of these therapies and the need for ongoing treatment can create economic burdens for patients and healthcare systems.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

142 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.04% |

|

Market growth 2024-2028 |

USD 208.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.88 |

|

Key countries |

US, Germany, UK, Canada, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Rare Hemophilia Factors Market Research and Growth Report?

- CAGR of the Rare Hemophilia Factors industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the rare hemophilia factors market growth of industry companies

We can help! Our analysts can customize this rare hemophilia factors market research report to meet your requirements.

RIA -

RIA -