Hepatitis B and C Diagnostics Market Size 2024-2028

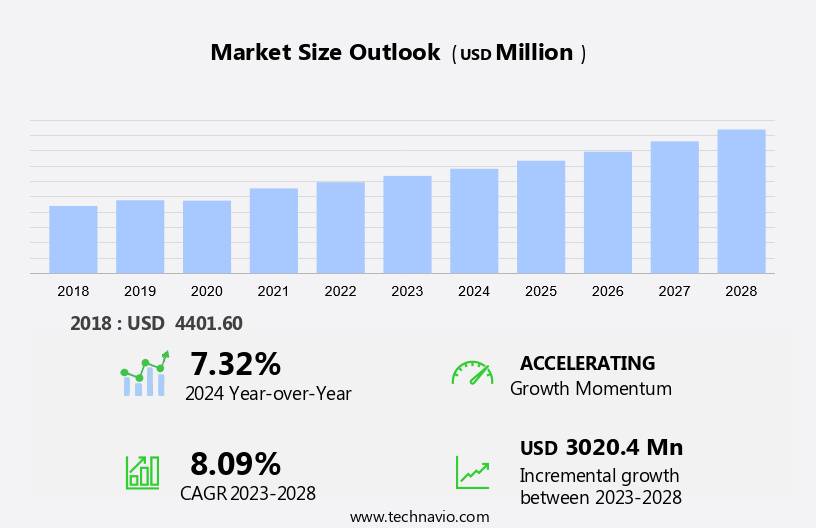

The hepatitis B and C diagnostics market size is estimated to increase by USD 3.02 billion at a CAGR of 8.09% between 2023 and 2028. Market expansion hinges on several critical factors, such as increasing demand for molecular diagnostics in diagnosing HBV and HCV infections, healthcare organizations' strategies to streamline diagnostic procedures, and the rising popularity of point-of-care (POC) diagnostic. These elements collectively drive market evolution, influencing demand dynamics and technological advancements. The growing adoption of molecular diagnostics reflects a broader trend towards precision medicine and enhanced disease management. Healthcare organizations are prioritizing simplification and efficiency in diagnostic workflows to improve patient outcomes and operational efficiency. Concurrently, the demand for POC diagnostics is driven by the need for rapid and decentralized testing solutions that facilitate timely clinical decisions. As these trends shape the market landscape, stakeholders navigate a complex environment characterized by innovation, regulatory considerations, and evolving healthcare needs, positioning the market for sustained growth and adaptation to emerging opportunities in diagnostic technologies.

What will be the size of the Market During the Forecast Period?

To learn more about this report, View Report Sample

Market Dynamics

The market is driven by advancements in nucleic acid assays and rapid diagnostic tests, essential for detecting chronic HBV infection and chronic HCV infection. Blood samples are pivotal in nucleic acid tests and enzyme assays, crucial for accurate HBsAg testing and HCV RNA detection. The market benefits from POC instruments and kits that enable quick diagnoses, supporting public health concerns and vaccination coverage efforts. Biotechnology and biopharmaceutical industries innovate new HCV antiviral treatments, complemented by awareness campaigns promoting blood donation and transfusion safety. As demand grows, liver biopsy remains fundamental in chronic HBV consultations, enhancing treatment decisions. The market's future hinges on technological innovations in nucleic acid testing, catering to global healthcare needs and advancing diagnostic accuracy in Hepatitis B and C management.

Key Market Driver

The growing demand for molecular diagnostics in the diagnosis of HBV and HCV is notably driving market growth. Globally, nearly 600 hospital laboratories and 200 independent laboratories undertake high-volume testing that requires automated molecular diagnostic testing platforms to simplify and facilitate sample preparation. The popular applications of molecular diagnostics include the identification and profiling of causative agents of infection and the quantification of pathogens to monitor the durability of therapy.

The sales of molecular diagnostics for infectious diseases, such as HBV and HCV, hold a major share of the overall molecular diagnostics market. Real-time polymerase chain reaction (PCR) is the standard recommended molecular diagnostics method for HCV RNA and HBV DNA in clinical samples. Hence, the huge potential for the application of molecular biology techniques in the clinical diagnosis of HBV and HCV will drive the growth of the market during the forecast period.

Significant Trends

High demand for biomarker-based tests is the primary trend in the market. Biomarkers are proteins, genes, hormones, and other molecular entities that detect the absence or presence of a disease. Sophisticated R&D in proteomics, nucleic acid expression, and genome sequencing has led to the emergence of molecular biomarkers. Technological advancements are driving manufacturers to develop assays that identify biomarkers in high-growth clinical areas such as infectious diseases, including hepatitis and retroviruses.

Biomarker-based tests will likely replace conventional drug therapeutics and account for increased revenue and sales from personalized test devices. To better reach the market, companies are developing cost-effective biomarker-based tests. Increased approvals for medical devices and a rise in product launches are expected to propel the market growth and trends during the forecast period.

Major Challenge

Low penetration of HBV and HCV diagnostic tests is one of the challenges impeding market growth. The presence of a large population of undiagnosed individuals with hepatitis C infections indicates a low penetration of the diagnostics. According to the World Hepatitis Alliance, only around 5% of individuals with the conditions in low-income countries are diagnosed.

The low penetration could be due to the lack of awareness and appropriate tools, as well as delivery issues. For instance, less than 1% of these individuals are likely to be aware of their diagnosis. Some other major issues are the absence of government policies and the lack of funding from government agencies. Furthermore, these diagnostics are costly, which affects their adoption rate in low-income countries. Also, treatment regimens are complex, affecting the diagnosis rates. Such issues will hinder the growth of the market during the forecast period.

Customer Landscape

The market research report includes the adoption lifecycle of the market research and growth, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth and forecasting strategies.

Market Customer Landscape

Who are the Major Market Players?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Abbott Laboratories - The company offers hepatitis B and C diagnostics solutions under its brands Alinity and ARCHITECT under the medical devices and pharmaceuticals segment. The company offers products for rhythm management, electrophysiology, heart failure, vascular, structural heart, and neuromodulation.

The market report also includes detailed analyses of the competitive landscape of the market and information about 18 market players, including:

- Bio Rad Laboratories Inc.

- bioMerieux SA

- DAAN Gene Co. Ltd.

- DiaSorin SpA

- Enzo Biochem Inc.

- F. Hoffmann La Roche Ltd.

- Grifols SA

- Hologic Inc.

- MedMira Inc.

- OraSure Technologies Inc.

- PerkinElmer Inc.

- QIAGEN NV

- Quidel Corp.

- Randox Laboratories Ltd.

- Siemens AG

- Sysmex Corp.

- Xiamen Innovax Biotech Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

By Type

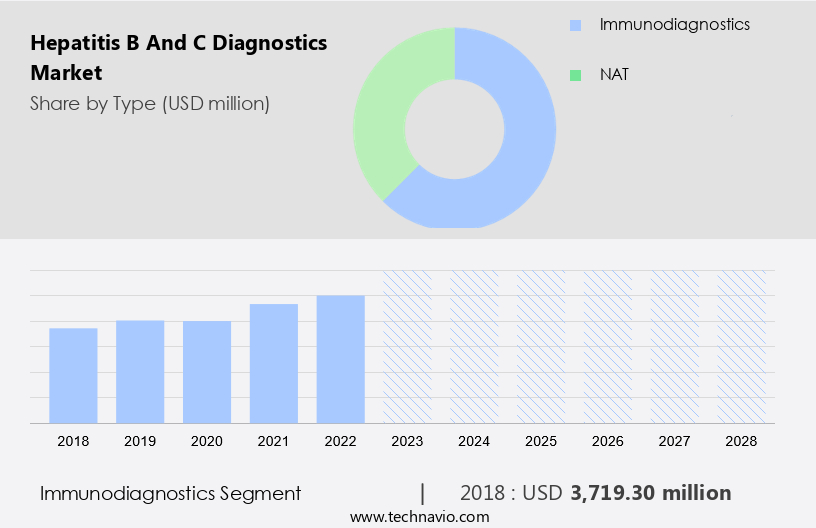

The market share growth of the immunodiagnostics segment will be significant during the forecast period. Immunodiagnostics are diagnostic tests that detect antigens or antibodies by producing an enzyme-triggered color change. Immunodiagnostics have the highest adoption rates for the diagnosis of the virus (HCV) and the B virus (HBV), owing to their established presence for an extended period.

Get a glance at the market contribution of various segments View the PDF Sample

The immunodiagnostics segment was valued at USD 3.72 billion in 2018. There is an increased need for quantification diagnostic tests owing to their ability to determine the stage of infection. The higher demand for viral core antigen testing, which is essential for effective and accurate diagnosis, is expected to fuel market growth for the market.

By Region

For more insights on the market share of various regions Download PDF Sample now!

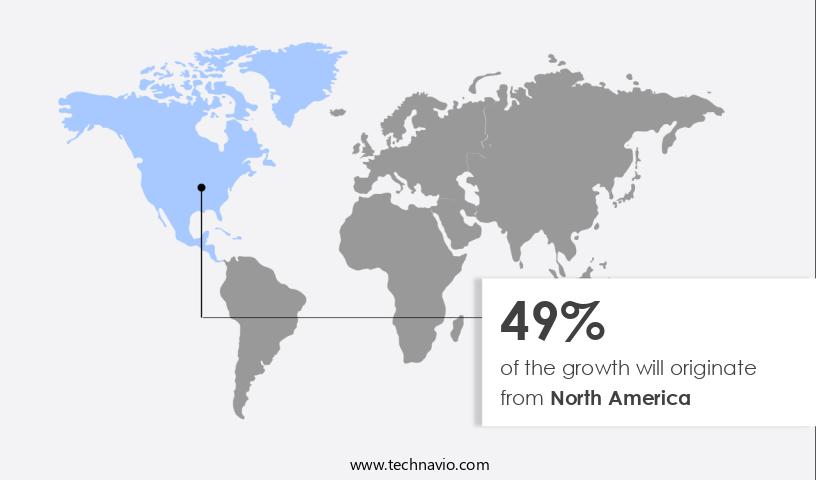

North America is estimated to contribute 49% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional market trends and analysis and drivers that shape the market during the forecast period. The market in North America is witnessing high adoption of these tests for HBV. Increasing blood transfusions in North America has driven the need for the diagnosis of the B variant. Around 4.5 million people living in the US and Canada need blood transfusions each year. The implementation of POC testing methods has also increased in the region, as these products are highly accessible and easy to use. Biomarker-based POC tests and initiatives by non-profit and government institutes, such as the National Institute of Health (NIH), are expected to drive market growth.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion " for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type Outlook

- Immunodiagnostics

- NAT

- Disease Type Outlook

- Hepatitis B

- Hepatitis C

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- Asia

- China

- India

- Rest of World (ROW)

- Brazil

- Argentina

- Rest of the Middle East & Africa

- North America

Market Analyst Overview

The market thrives on a range of technologies and services, including blood sample analysis, enzymes, reagents and kits, enzyme-linked immunosorbent assay (ELISA), and isothermal nucleic acid amplification tests. Blood tests and imaging tests play crucial roles in pathogen detection and diagnosing conditions like chronic hepatitis C virus infection and severe acute hepatitis in adolescents and children. Hospitals, diagnostic laboratories, and clinical laboratories utilize immunoassay instruments and consumables handled by skilled technicians for sample procurement, storage, and transportation. Advances such as Next-Generation Sequencing enhance laboratory space efficiency while addressing challenges like cross-contamination. Public health concerns drive demand for improved HBV DNA testing methods, ensuring accurate diagnoses and effective management strategies in the ongoing fight against hepatitis B and C infections.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2023-2027 |

USD 3.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

7.32 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 49% |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abbott Laboratories, Bio Rad Laboratories Inc., bioMerieux SA, DAAN Gene Co. Ltd., DiaSorin SpA, Enzo Biochem Inc., F. Hoffmann La Roche Ltd., Grifols SA, Hologic Inc., MedMira Inc., OraSure Technologies Inc., PerkinElmer Inc., QIAGEN NV, Quidel Corp., Randox Laboratories Ltd., Siemens AG, Sysmex Corp., and Xiamen Innovax Biotech Co. Ltd. |

|

Market dynamics |

Parent market growth analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the market forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market report during the forecast period

- Detailed information of market analysis and report on factors that will drive the growth of the market between 2023 and 2027

- Precise estimation of the size of the market and its contribution in focus to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -