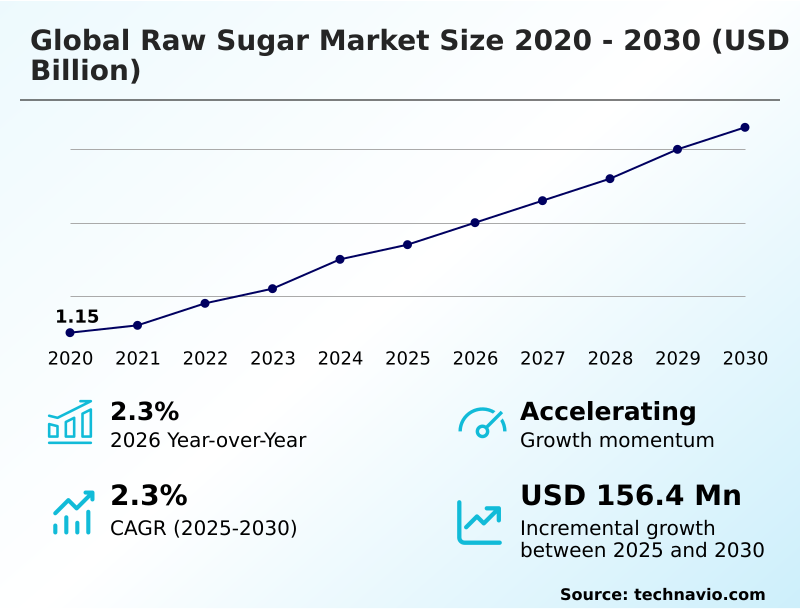

Raw Sugar Market Size 2026-2030

The raw sugar market size is valued to increase by USD 156.4 million, at a CAGR of 2.3% from 2025 to 2030. Global production surpluses and industrialization of stock recovery will drive the raw sugar market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.7% growth during the forecast period.

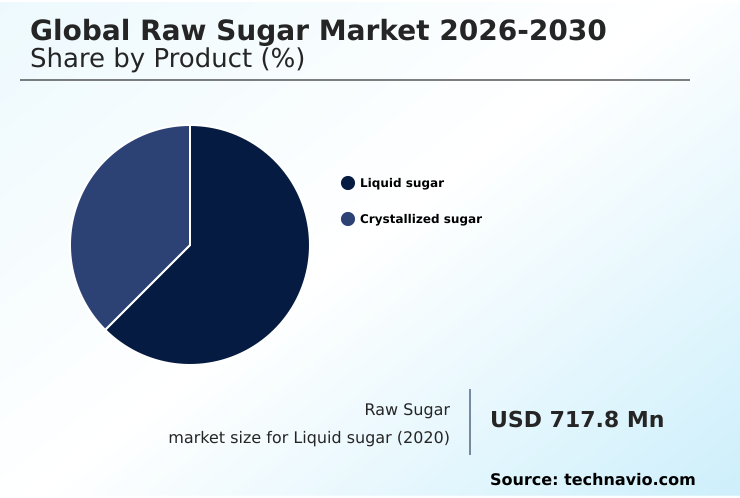

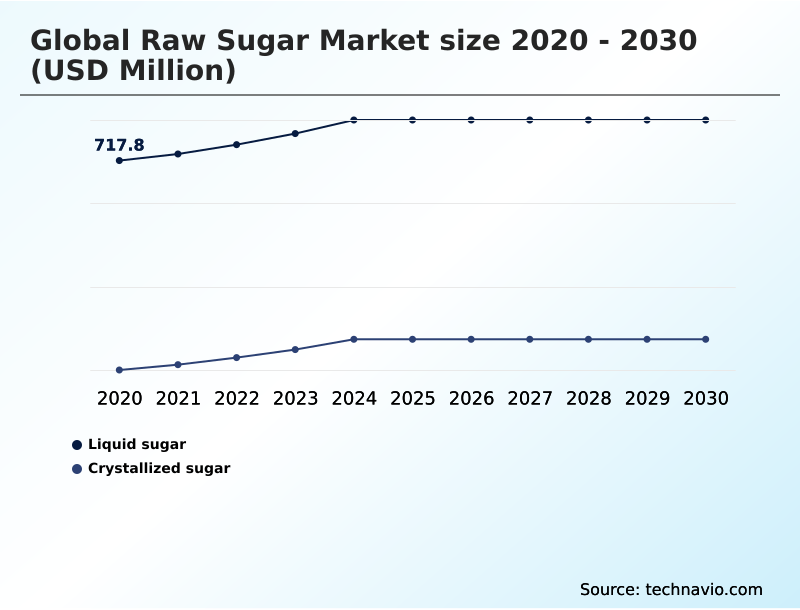

- By Product - Liquid sugar segment was valued at USD 773.4 million in 2024

- By Type - Conventional segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 282.3 million

- Market Future Opportunities: USD 156.4 million

- CAGR from 2025 to 2030 : 2.3%

Market Summary

- The raw sugar market is undergoing a fundamental shift, moving from supply tightness to a period of structural surplus, which is reshaping price dynamics and competitive strategies. This transition is driven by favorable agricultural yields in key production zones and the strategic flexibility of mills to divert sugarcane between sugar and ethanol production.

- A key trend transforming the sector is the integration of digital technologies, such as AI-driven precision agriculture, which enhances cane-to-mill logistics and improves extraction efficiency. Concurrently, the industry is navigating significant challenges, including downward price pressure from oversupply and escalating regulatory scrutiny aimed at curbing sugar consumption.

- For instance, a global beverage manufacturer must now leverage advanced supply chain analytics to source traceable, sustainably certified sugar to comply with new ESG mandates, mitigating risks from both climate volatility and shifting consumer health preferences. This environment favors producers who can master cost optimization, embrace regenerative agriculture, and innovate toward value-added specialty sugars to maintain profitability.

What will be the Size of the Raw Sugar Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Raw Sugar Market Segmented?

The raw sugar industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Liquid sugar

- Crystallized sugar

- Type

- Conventional

- Organic

- Application

- Beverages

- Confectionery and bakery

- Dairy products

- Others

- Geography

- APAC

- India

- China

- Australia

- South America

- Brazil

- Argentina

- Europe

- France

- Germany

- UK

- North America

- US

- Mexico

- Canada

- Middle East and Africa

- South Africa

- Turkey

- Israel

- Rest of World (ROW)

- APAC

By Product Insights

The liquid sugar segment is estimated to witness significant growth during the forecast period.

The liquid sugar segment caters to industrial users requiring rapid solubility and precise blending, particularly in beverage and pharmaceutical applications.

This segment, including liquid sucrose and invert sugar syrups, streamlines manufacturing by eliminating the energy-intensive dissolution phase associated with crystallized sugar. Adoption is driven by operational efficiencies, such as improving blending precision by up to 15% in automated facilities.

Enhanced food safety protocols, due to enclosed handling systems, and the demand for high-clarity syrups for clear beverages also fuel growth.

While specialized transport adds complexity, the logistical benefits of automated dosing in modern smart factories provide a compelling economic case for this high-growth category, which uses high-intensity sweeteners and is subject to feedstock flexibility.

The Liquid sugar segment was valued at USD 773.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Raw Sugar Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by distinct regional dynamics. APAC is the primary center for consumption growth, accounting for over 40% of the market's incremental growth, driven by industrial demand in China and India.

South America, led by Brazil, acts as the global balancing supplier, with its unique mill flexibility influencing global price benchmarks. The regional market is also seeing increased use of commodity trading software.

In contrast, Europe's market is defined by a mature beet sugar industry facing a 5% decline in production, increasing its reliance on raw cane sugar imports that meet stringent sustainability standards.

North America operates under a managed quota system, balancing domestic production with strategic imports. These regional distinctions, including different approaches to sugarcane-to-ethanol flexibility, shape global trade flows and investment priorities for market participants.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the raw sugar market now centers on navigating a complex web of agricultural and economic factors. Optimizing the sugarcane crush mix for ethanol production requires sophisticated analysis of energy market parity against sugar futures.

- Furthermore, the adoption of regenerative agriculture and soil carbon sequestration is no longer a niche practice but a core component of securing premium contracts with global food brands. As part of this, managing ratoon crop degradation through advanced soil health techniques is essential for long-term yield stability.

- Companies are also investing in the sugarcane bagasse valorization into bioplastics, creating new revenue streams from what was once waste. The ability to produce low-glycemic index (GI) cane sugars and other differentiated specialty sugar ingredients allows producers to capture value in health-conscious markets.

- Implementing satellite-based precision harvesting in sugarcane farming has become critical, with integrated systems improving logistical efficiency by over 15% compared to traditional methods. Simultaneously, addressing the impact of GLP-1 medications on sugar demand requires a strategic pivot toward industrial applications and emerging economies.

- Effective feedstock utilization strategies for raw sugar and the management of government import quotas in Asia are fundamental to maintaining market share in this evolving landscape.

What are the key market drivers leading to the rise in the adoption of Raw Sugar Industry?

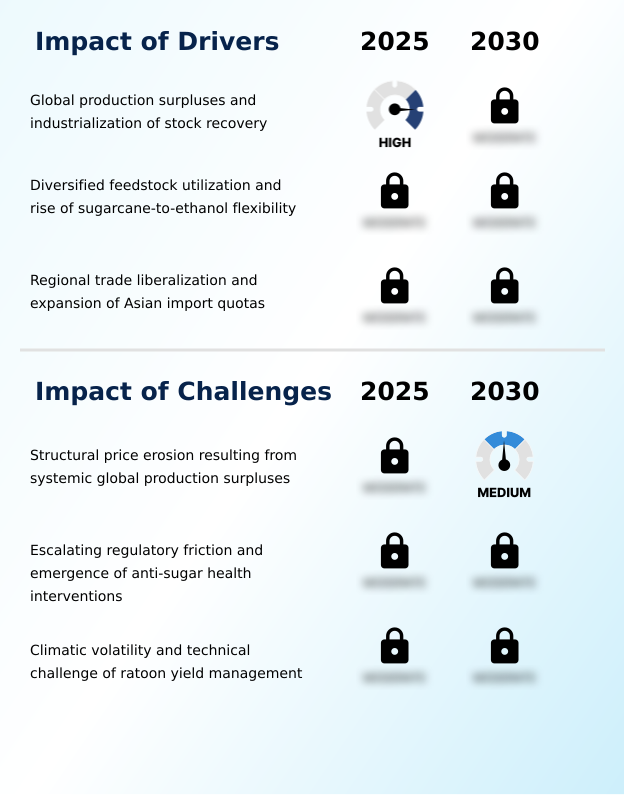

- A key market driver is the emergence of global production surpluses, which facilitates the industrialization of stock recovery and reshapes supply-side dynamics.

- Market growth is significantly influenced by a structural shift toward a global production surplus, which is stabilizing raw material costs for industrial users after years of supply tightness.

- This surplus, estimated at over 10 million metric tons, is a direct result of favorable yields in major producing regions.

- Another powerful driver is the enhanced feedstock utilization strategies, particularly the ability of mills in Brazil and India to pivot between raw sugar and ethanol based on energy market parity.

- This flexibility allows producers to hedge against price declines, with Brazilian mills recently increasing their sugar mix to over 50%.

- Furthermore, regional trade liberalization, such as the management of Asian import quotas, provides critical outlets for excess production and maintains fluidity in the seaborne trade.

What are the market trends shaping the Raw Sugar Industry?

- The integration of AI and satellite-based precision harvesting is emerging as a key trend. This technology optimizes the cane-to-mill logistics chain and maximizes juice extraction efficiency.

- Key trends are reshaping the market's competitive landscape. The integration of AI and remote sensing is optimizing the entire cane-to-mill logistics chain, with predictive models improving yield forecasts by over 20% and ensuring peak juice extraction efficiency. This digital transformation is reducing operational waste.

- Another significant trend is the expansion of regenerative agriculture, where practices like cover cropping and the use of bio-organic fertilizers are helping rebuild soil health. Leading producers adopting these methods report a 5% annual increase in soil carbon, which is crucial for meeting corporate ESG goals.

- The market is also diversifying with the emergence of differentiated specialty sugars and other functional ingredients, including non-gmo specialty sugars, driven by consumer demand for clean-label and healthier alternatives.

What challenges does the Raw Sugar Industry face during its growth?

- Structural price erosion, stemming from systemic global production surpluses, presents a significant challenge to industry growth and profitability.

- The market confronts several significant challenges, led by structural price erosion from a persistent global production surplus. This oversupply has caused raw sugar futures to decline by as much as 35% from the prior year, severely impacting the profitability of producers, especially those with higher operational costs.

- Another major headwind is the escalating regulatory friction, with governments worldwide implementing sugar taxes and front-of-package warning labels. Compounding this, climatic volatility and the technical difficulty of ratoon yield management present ongoing agricultural risks.

- Erratic weather patterns can reduce sugar recovery rates by up to 10% in a single season, making long-term production planning exceptionally difficult and threatening supply chain stability and commodity price stabilization.

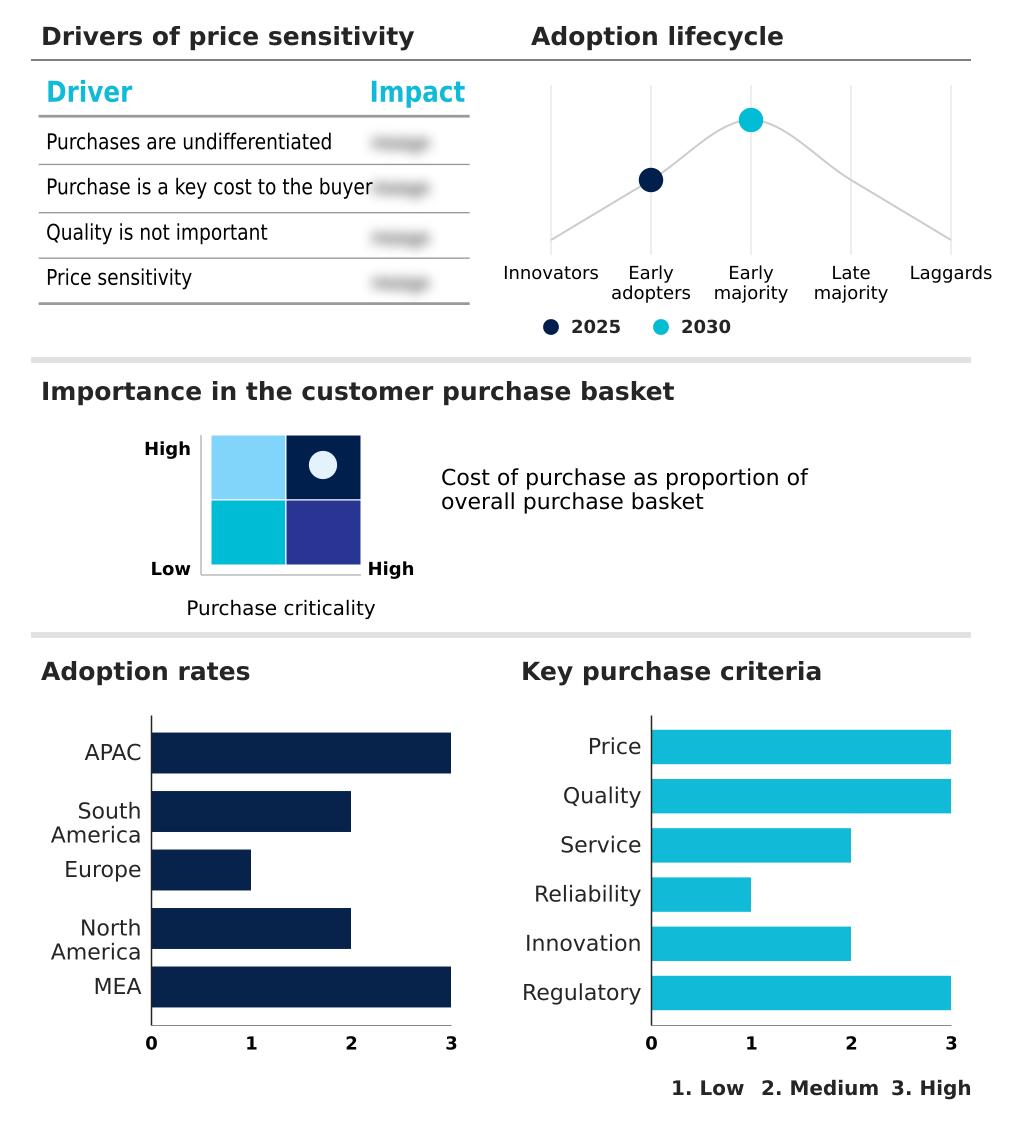

Exclusive Technavio Analysis on Customer Landscape

The raw sugar market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the raw sugar market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Raw Sugar Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, raw sugar market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adecoagro SA - Offerings include sustainably produced cane sugar integrated with renewable energy and ethanol operations, focusing on vertically integrated supply chain efficiency and commodity-grade feedstock.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adecoagro SA

- Balrampur Chini Mills Ltd.

- Central Romana Corp.

- Dalmia Bharat Sugar Ltd

- Dhampur Bio Organics Ltd.

- EID Parry India Ltd.

- Florida Crystals Corp.

- Illovo Sugar

- Ingenio Magdalena

- Mackay Sugar

- Mitr Phol Group

- Pantaleon

- Shree Renuka Sugars Ltd.

- Sudzucker AG

- Tereos Participations

- Thai Roong Ruang Group

- Triveni Industries Ltd.

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Raw sugar market

- In September 2024, a leading South American producer announced the full-scale deployment of an AI-powered satellite monitoring system across its plantations to optimize harvest timing, projecting a 10% increase in total recoverable sugar.

- In November 2024, a major European refiner entered a strategic partnership with a technology firm to implement a blockchain-based traceability platform, ensuring end-to-end verification of its fair-trade and non-GMO sugar supply chains.

- In February 2025, an APAC-based agricultural conglomerate acquired a portfolio of organic sugar brands to expand its presence in the high-value specialty ingredients market, catering to rising clean-label demand in North America and Europe.

- In April 2025, a global commodity trader announced it had secured USD 500 million in green financing to upgrade its milling facilities, focusing on sugarcane bagasse valorization projects to produce bioplastics and bio-composites.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Raw Sugar Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.3% |

| Market growth 2026-2030 | USD 156.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.3% |

| Key countries | India, China, Australia, Indonesia, Japan, South Korea, Brazil, Argentina, Chile, France, Germany, UK, The Netherlands, Spain, Italy, US, Mexico, Canada, South Africa, Turkey, Israel, UAE and Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The raw sugar market is being reshaped by the convergence of digital innovation and sustainability mandates. Core operational processes like vacuum-pan crystallization and centrifugal separation are now augmented by advanced analytics to maximize sucrose content and ensure consistent sucrose polarization.

- This technological shift, which can improve total recoverable sugar by up to 8%, is a critical boardroom focus, influencing capital expenditure on refinery modernization. The industry is moving beyond traditional commodity production, with a focus on high-polarity sugar and specialty products.

- Producers are leveraging techniques from precision agriculture, including soil moisture monitoring and drip irrigation, to manage crop health and mitigate the effects of climatic volatility. This pivot is essential for maintaining a competitive edge in a market where factors like ratoon crop management and the development of organic raw sugar define profitability.

- The institutionalization of these high-tech systems is creating a more resilient supply chain, capable of navigating both economic shifts and agricultural challenges while meeting demands for industrial sugar and consumer goods.

What are the Key Data Covered in this Raw Sugar Market Research and Growth Report?

-

What is the expected growth of the Raw Sugar Market between 2026 and 2030?

-

USD 156.4 million, at a CAGR of 2.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Liquid sugar, and Crystallized sugar), Type (Conventional, and Organic), Application (Beverages, Confectionery and bakery, Dairy products, and Others) and Geography (APAC, South America, Europe, North America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, South America, Europe, North America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Global production surpluses and industrialization of stock recovery, Structural price erosion resulting from systemic global production surpluses

-

-

Who are the major players in the Raw Sugar Market?

-

Adecoagro SA, Balrampur Chini Mills Ltd., Central Romana Corp., Dalmia Bharat Sugar Ltd, Dhampur Bio Organics Ltd., EID Parry India Ltd., Florida Crystals Corp., Illovo Sugar, Ingenio Magdalena, Mackay Sugar, Mitr Phol Group, Pantaleon, Shree Renuka Sugars Ltd., Sudzucker AG, Tereos Participations, Thai Roong Ruang Group, Triveni Industries Ltd. and Wilmar International Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the dual pressures of commodity price fluctuation and the need for greater supply chain resilience. Producers are adopting flexible production models, with the ability to shift between sugar and biofuel energy mix outputs improving financial returns by over 20% during periods of oil price volatility.

- The pivot toward sustainable agri-input and fair-trade certification is creating new value streams, as premium products command higher margins. Investment in sugar beet logistics and refinery energy consumption optimization is critical, as operational efficiency gains can reduce costs by 12%.

- Advanced agricultural practices, including the use of drone surveillance and onboard harvester sensors, are becoming standard for managing crop health and ensuring consistent industrial-grade sweeteners for the global market.

We can help! Our analysts can customize this raw sugar market research report to meet your requirements.

RIA -

RIA -