Residential Faucets Market Size and Growth Forecast 2026-2030

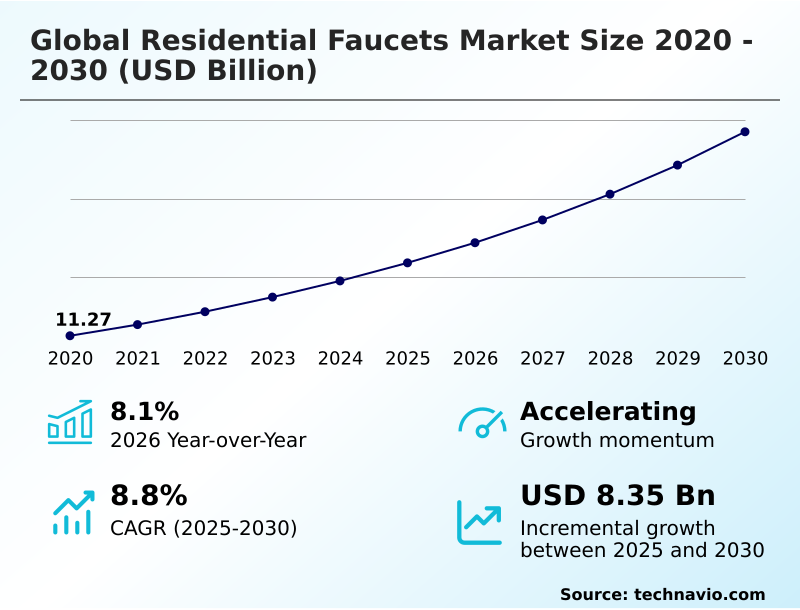

The Residential Faucets Market size was valued at USD 15.91 billion in 2025 growing at a CAGR of 8.8% during the forecast period 2026-2030.

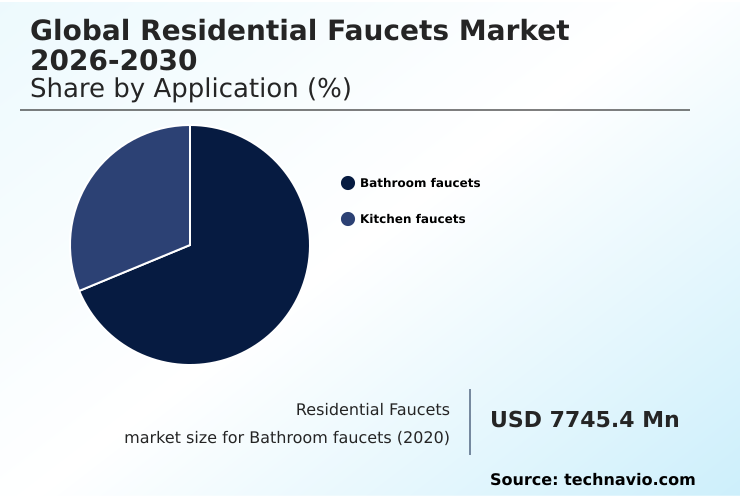

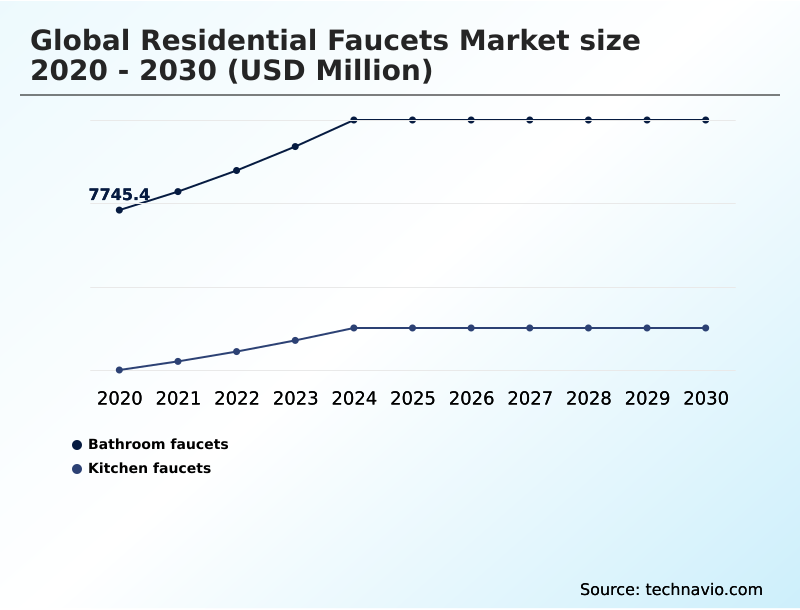

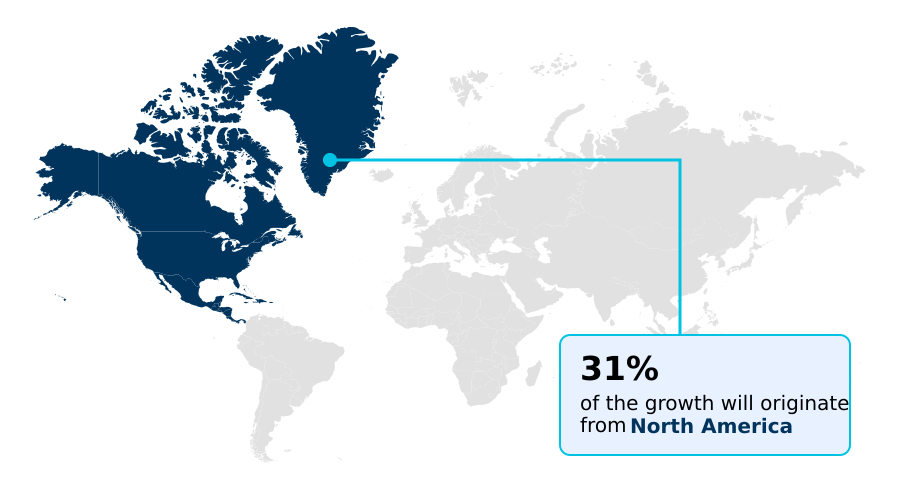

North America accounts for 30.9% of incremental growth during the forecast period. The Bathroom faucets segment by Application was valued at USD 10.13 billion in 2024, while the Offline segment holds the largest revenue share by Distribution Channel.

The market is projected to grow by USD 12.99 billion from 2020 to 2030, with USD 8.35 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Residential Faucets Market Overview

The residential faucets market is experiencing a significant transformation, with year-over-year growth reaching 8.1% as demand shifts toward technologically advanced and sustainable fixtures. This evolution is defined by the convergence of smart home interoperability and stringent water conservation goals, compelling manufacturers to innovate beyond traditional mechanics. For instance, in a new multi-family housing development pursuing green building certifications like LEED, the specification of water-efficient fixtures is non-negotiable. These projects now favor touchless sensory technology and faucets made from lead-free brass to enhance hygiene and ensure regulatory compliance. In practice, equipping a 200-unit building with such systems not only reduces water consumption but also aligns with tenant expectations for modern, connected living spaces. The market is also accommodating a robust do-it-yourself segment, with manufacturers simplifying DIY faucet installation procedures for renovations and bathroom upgrades, thereby broadening the consumer base.

Drivers, Trends, and Challenges in the Residential Faucets Market

Procurement decisions in the residential faucets market are increasingly complex, balancing long-term performance with evolving technological and regulatory demands. The impact of raw material volatility on faucet pricing remains a primary concern for supply chain managers, influencing the cost analysis of brass versus plastic faucets and the economic viability of using premium materials.

The choice between lead-free brass vs stainless steel faucet durability is a critical specification point, particularly with the impact of the EU Drinking Water Directive on materials becoming a global benchmark. For installers, understanding the nuances of DIY installation of single-hole bathroom faucets is as important as troubleshooting magnetic docking systems on sprayers in high-end kitchens.

In the context of smart homes, the challenges of smart home interoperability for faucets and the need for smart faucet integration with Apple HomeKit are defining consumer satisfaction.

A key decision point for specifiers is choosing faucets for high-end urban housing developments, where selecting the best pull-down kitchen faucets for workstation sinks or upgrading to high-arc faucets for better clearance can significantly impact perceived value. The role of faucets in LEED green building certification is critical, driving demand for water-saving benefits of WaterSense certified faucets.

A standard faucet's flow rate of 2.2 gallons per minute is over 45% higher than a WaterSense-labeled model, a metric that directly impacts utility savings and compliance. This also extends to sourcing eco-friendly faucets with recycled materials and ensuring safety through thermostatic mixing valves for anti-scald protection.

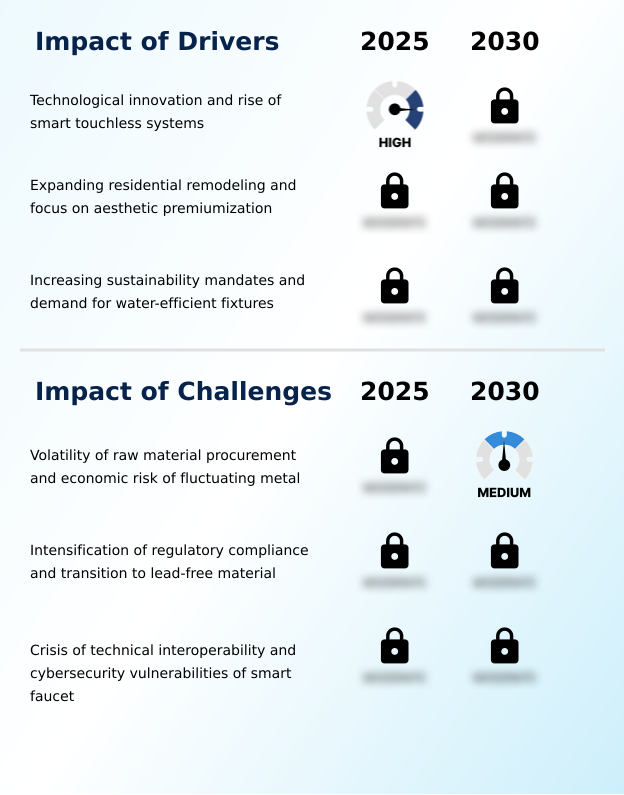

Primary Growth Driver: Technological innovation and the rise of smart, touchless systems are key drivers propelling growth in the residential faucets market.

Market growth is propelled by a dual focus on aesthetic premiumization and sustainability, particularly in high-growth regions like APAC, which is forecast to expand at 9.4%.

Homeowners globally are prioritizing minimalist aesthetics and design-led innovation, demanding fixtures that serve as architectural focal points. This driver is supported by an expanding palette of durable finishes and forms.

Simultaneously, pressing environmental concerns and the desire for utility savings are accelerating the adoption of eco-friendly residential faucets. Mandates for water conservation are pushing manufacturers to engineer high-performance aeration systems that reduce consumption without sacrificing pressure.

This convergence of style and function ensures that fixtures meet both the visual and ethical standards of modern eco-conscious residential living.

Emerging Market Trend: The integration of sensory technology and hybrid command interfaces is a defining market trend. This shift prioritizes residential sensor-based systems for enhanced hygiene and convenience.

A significant market trend is the push toward sophisticated digital integration, which introduces both opportunities and complexities. The adoption of hybrid command interfaces, which combine manual control with voice-activated dispensing, is expanding, yet the industry grapples with technical interoperability.

As digital water networks become more common, nearly 30% of consumer dissatisfaction in the premium segment stems from the failure of smart faucets to connect seamlessly with diverse home automation platforms. This fragmentation creates significant cybersecurity vulnerabilities, turning a simple plumbing fixture into a potential network entry point.

Consequently, manufacturers are under pressure to standardize communication protocols and invest in robust firmware to build consumer trust in connected home ecosystems.

Key Industry Challenge: The volatility of raw material procurement and the economic risk associated with fluctuating metal prices present a key challenge to industry growth.

The most pressing market challenges stem from supply chain volatility and stringent regulatory compliance. The fluctuating cost of raw material procurement, particularly for brass and zinc, directly impacts profitability and pricing stability.

Concurrently, the global transition toward lead-free plumbing mandates, such as the requirement for a maximum lead content of 0.25% in components contacting drinking water, forces costly redesigns and retooling. This necessitates rigorous validation of alternative materials like 304 stainless steel or specialized polymers.

For popular finishes like PVD-coated matte black, ensuring consistency and durability while managing rising input costs is a significant operational hurdle. These pressures are further compounded by the technical demands of integrating electronics for hands-free operation, creating a complex manufacturing landscape.

Explore Full Market Dynamics Analysis Request Free Sample

Residential Faucets Market Segmentation

The residential faucets industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Application Segment Analysis

The bathroom faucets segment is estimated to witness significant growth during the forecast period.

The bathroom faucets segment, which accounts for over two-thirds of the residential market, is driven by a focus on personal wellness and aesthetic upgrades.

Homeowners are increasingly specifying premium configurations like widespread faucets and wall-mounted faucets to achieve spa-like environments, moving beyond purely functional hardware. This trend elevates the importance of thermostatic mixing valves for anti-scald protection and precision temperature control.

The industry-wide adoption of ceramic disc valves has become a standard, significantly enhancing durability and reducing maintenance.

Concurrently, a push towards sustainability is fueling demand for advanced water-saving technologies that comply with stringent environmental standards without compromising the user experience, supporting the market's ongoing aesthetic premiumization.

The Bathroom faucets segment was valued at USD 10.13 billion in 2024 and showed a gradual increase during the forecast period.

Residential Faucets Market by Region: North America Leads with 30.9% Growth Share

North America is estimated to contribute 30.9% to the growth of the global market during the forecast period.

The geographic landscape of the residential faucets market is characterized by a close rivalry between mature and emerging regions. North America contributes 30.9% of the growth, driven by a strong appetite for smart touchless systems and hygienic touchless systems.

In parallel, APAC, contributing 29.9% of the growth, is fueled by rapid urbanization and new construction, where professional-grade quality is increasingly sought.

Across these diverse regions, there is a common thread of tightening sustainability mandates, which elevates the importance of durable and corrosion-resistant finishes that extend product lifecycles.

Compliance with these environmental standards, alongside the integration of smart home automation, has become a critical factor for manufacturers aiming to secure market share in both high-end renovations and large-scale residential developments.

Customer Landscape Analysis for the Residential Faucets Market

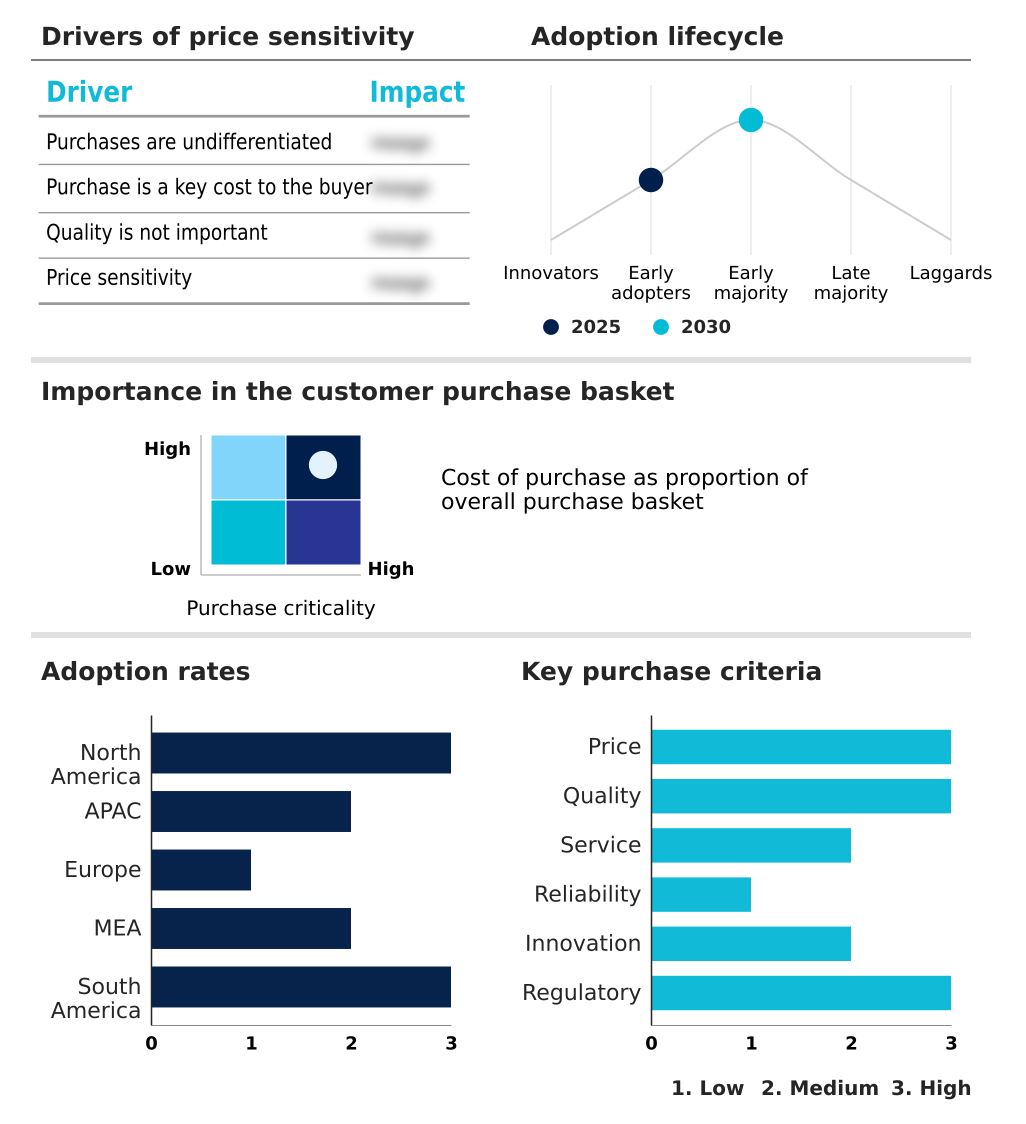

The residential faucets market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the residential faucets market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Residential Faucets Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the residential faucets market industry.

BLANCO GmbH and Co. KG - Delivers innovative residential fixtures, integrating touch-activated technology and water-efficient designs for contemporary kitchen and bathroom applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BLANCO GmbH and Co. KG

- Brizo kitchen and bath Co.

- Delta Faucet Co

- Dornbracht GmbH and Co. KG

- Duravit AG

- Elkay Manufacturing Co.

- Fortune Brands Innovations Inc.

- FRANKE Holding AG

- Geberit International AG

- Gerber Plumbing Fixtures LLC

- Jaquar Group

- Kohler Co.

- LIXIL Corp.

- Moen Inc.

- Oras Ltd.

- Roca Sanitario S.A.

- Speakman

- Symmons Industries Inc.

- Toto Ltd.

- Villeroy and Boch AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Residential Faucets Market

- In October, 2024, Delta Faucet Co. enhanced its smart home offerings by adding full Apple HomeKit compatibility to its VoiceIQ system, expanding its connected faucet ecosystem for a larger user demographic.

- In January, 2025, Brondell Inc. launched its Jema Kitchen Faucet Collection at the Kitchen and Bath Industry Show, merging patented spray technology with high-arch, minimalist aesthetics to enhance both utility and style.

- In February, 2025, Delta Faucet Co. expanded its technical ecosystem by transitioning its VoiceIQ technology to a consolidated DFC at Home platform, allowing for unified control of connected water products.

- In April, 2025, The Government of India expanded its national manufacturing incentives to boost domestic production of high-precision sanitary ware, stimulating the establishment of new fabrication units for sensor-based and automated faucets.

Research Analyst Overview: Residential Faucets Market

Boardroom decisions are being shaped by the need to navigate a complex regulatory and technological environment, where the EU Drinking Water Directive is forcing a fundamental reassessment of material supply chains. The market's accelerating growth momentum is contingent on a vendor's ability to master both material science and software.

This includes the deployment of physical vapor deposition for durable, PVD-coated matte black finishes and the engineering of high-performance aeration systems. The pivot towards hygienic touchless systems and water-saving technologies is no longer optional. Firms must offer a portfolio ranging from traditional single-hole faucets and widespread faucets to advanced wall-mounted faucets with thermostatic mixing valves.

Core component quality, dictated by ceramic disc valves and lead-free brass, is paramount. Success now depends on achieving seamless smart home interoperability for features like voice-activated dispensing across digital water networks.

This requires a strategic commitment to R&D for everything from pull-down sprayers to the underlying sensory technology and hybrid command interfaces, all while meeting stringent sustainability mandates for eco-friendly residential faucets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Residential Faucets Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 8348.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Residential Faucets Market: Key Questions Answered in This Report

-

What is the expected growth of the Residential Faucets Market between 2026 and 2030?

-

The Residential Faucets Market is expected to grow by USD 8.35 billion during 2026-2030, registering a CAGR of 8.8%. Year-over-year growth in 2026 is estimated at 8.1%%. This acceleration is shaped by technological innovation and rise of smart touchless systems, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Bathroom faucets, and Kitchen faucets), Distribution Channel (Offline, and Online), Material (Brass, Stainless steel, Chrome, Bronze, and Plastic) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Bathroom faucets segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 30.9% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is technological innovation and rise of smart touchless systems, which is accelerating investment and industry demand. The main challenge is volatility of raw material procurement and economic risk of fluctuating metal, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Residential Faucets Market?

-

Key vendors include BLANCO GmbH and Co. KG, Brizo kitchen and bath Co., Delta Faucet Co, Dornbracht GmbH and Co. KG, Duravit AG, Elkay Manufacturing Co., Fortune Brands Innovations Inc., FRANKE Holding AG, Geberit International AG, Gerber Plumbing Fixtures LLC, Jaquar Group, Kohler Co., LIXIL Corp., Moen Inc., Oras Ltd., Roca Sanitario S.A., Speakman, Symmons Industries Inc., Toto Ltd. and Villeroy and Boch AG. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Residential Faucets Market Research Insights

Market dynamics are increasingly shaped by distinct consumer priorities and channel strategies. While the offline distribution channel maintains its dominance, the online sector is demonstrating accelerated growth, appealing to homeowners undertaking residential remodeling projects.

The preference for specific features is also segmenting the market; for example, the bathroom segment, which is substantially larger than the kitchen segment, is a focal point for aesthetic upgrades and water-saving innovations. Demand for antimicrobial coatings and durable ergonomic design is becoming standard, especially in fixtures intended for high-traffic family bathrooms.

Furthermore, achieving green building certifications under frameworks like LEED requires specifying water-efficient fixtures, influencing procurement decisions in new construction and making sustainability a key competitive differentiator for manufacturers.

We can help! Our analysts can customize this residential faucets market research report to meet your requirements.

RIA -

RIA -