Robotic Medical Imaging Systems Market Size 2026-2030

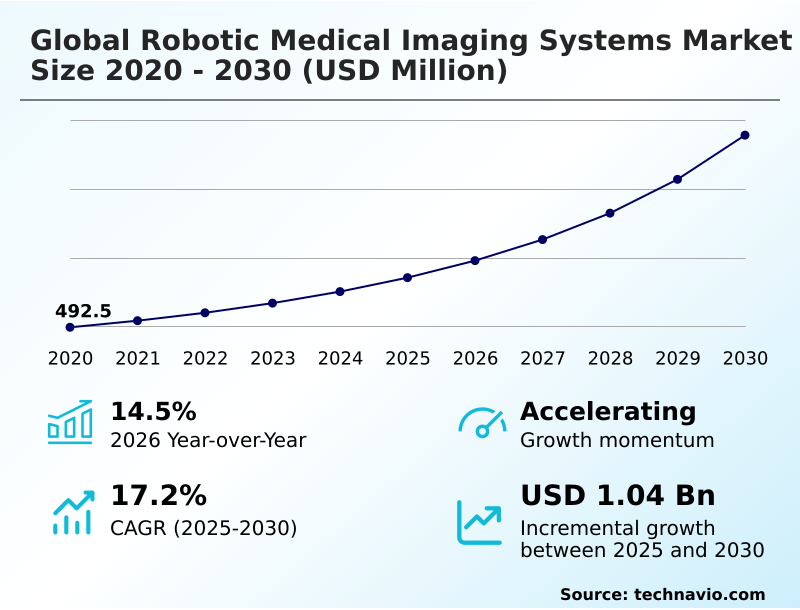

The robotic medical imaging systems market size is valued to increase by USD 1.04 billion, at a CAGR of 17.2% from 2025 to 2030. Technological integration of AI and automation will drive the robotic medical imaging systems market.

Major Market Trends & Insights

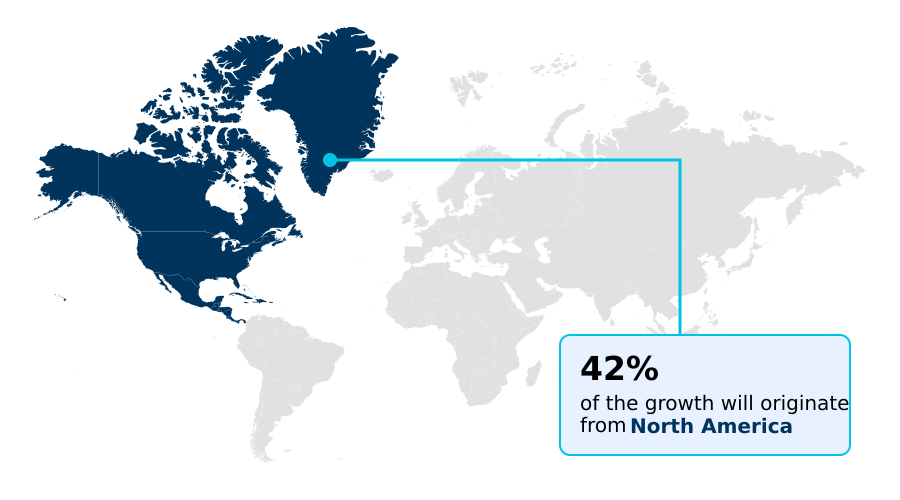

- North America dominated the market and accounted for a 42.4% growth during the forecast period.

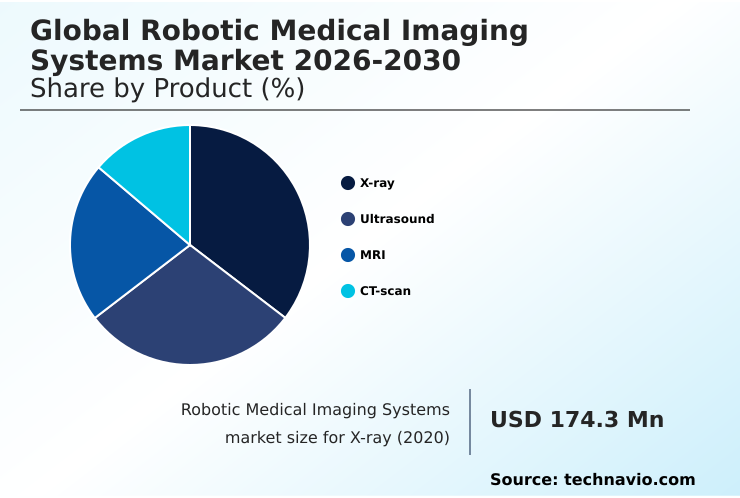

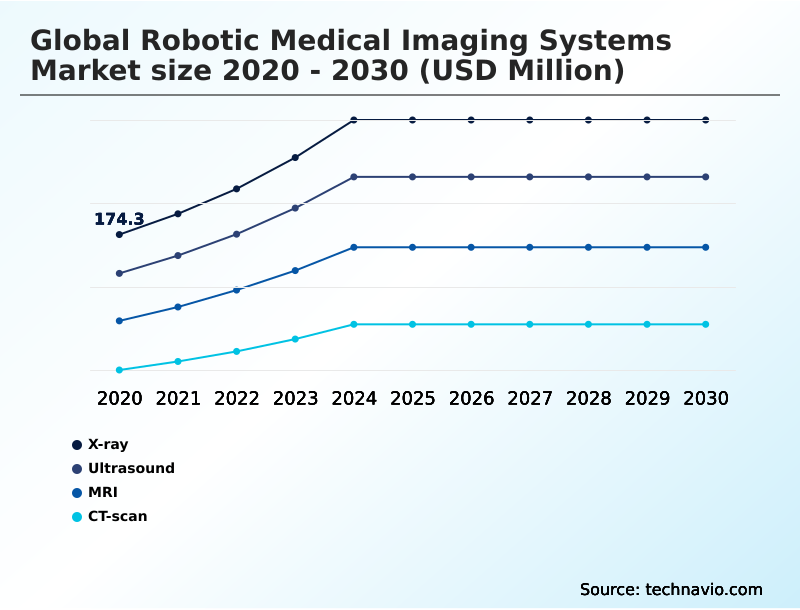

- By Product - X-ray segment was valued at USD 264.3 million in 2024

- By Application - Interventional radiology segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.40 billion

- Market Future Opportunities: USD 1.04 billion

- CAGR from 2025 to 2030 : 17.2%

Market Summary

- The robotic medical imaging systems market is transitioning from standalone devices to integrated platforms that combine robotics with AI-driven analytics. This evolution is driven by the need for enhanced precision in minimally invasive procedures, the rising prevalence of chronic diseases, and persistent workforce shortages in radiology.

- By leveraging technologies like robotic c-arm positioning and AI-driven workflow automation, these systems standardize complex procedures and reduce operator-dependent variability. For example, a hospital can optimize its operating room throughput by using an image-guided intervention platform that automates patient setup and image acquisition, shortening procedure times and allowing for more surgeries to be performed daily.

- While the high capital investment remains a significant barrier, the clinical and operational benefits, including improved patient outcomes and greater efficiency, continue to fuel adoption. The technology is critical for enabling tele-robotic ultrasound and other remote diagnostic capabilities, expanding access to specialized care. These systems are foundational to the future of data-driven, precision medicine.

What will be the Size of the Robotic Medical Imaging Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Robotic Medical Imaging Systems Market Segmented?

The robotic medical imaging systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- X-ray

- Ultrasound

- MRI

- CT-scan

- Application

- Interventional radiology

- Orthopedic and spine surgery

- Neurosurgery

- Others

- End-user

- Hospitals

- Specialty clinics

- Ambulatory surgical centers

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The x-ray segment is estimated to witness significant growth during the forecast period.

The robotic medical imaging systems market is segmented by product, application, end-user, and geography. The X-ray segment is evolving with the adoption of systems featuring robotic c-arm positioning and a self-driving mobile c-arm, which enhance precision in surgical settings.

These platforms, including the laser-guided mobile gantry, are designed for AI-driven workflow automation, significantly improving operational efficiency. The integration of surgical navigation tools and autonomous diagnostic imaging addresses the need for greater accuracy and reduced manual intervention.

For instance, advanced systems reduce procedural radiation exposure for staff by up to 50%.

This focus on workflow efficiency in radiology and improved patient throughput optimization reflects a broader shift towards value-based healthcare technology and safer, more effective interventional radiology robotics and computer-assisted surgery.

The X-ray segment was valued at USD 264.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Robotic Medical Imaging Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the robotic medical imaging systems market is led by North America, which accounts for over 42% of incremental growth, driven by high healthcare spending and early technology adoption.

The region sees widespread use of advanced primary and revision capabilities in orthopedics and minimally invasive tumor ablation in oncology. Europe follows, with strong government support for digital surgical ecosystems and precision oncology robotics.

Meanwhile, the APAC region is the fastest-growing market, with investments in smart hospital infrastructure growing by 30% annually in key countries.

This expansion is supported by demand for automated tissue recognition and remote procedural control to serve a large patient base.

These platforms which use real time imaging data for surgical guidance, are becoming integral to both established and emerging healthcare systems globally, with a focus on improving diagnostic-grade image capture and standardizing surgical outcome standardization.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic adoption of robotic medical imaging systems requires a thorough cost-benefit analysis of robotic bronchoscopy and similar specialized platforms. Healthcare leaders must evaluate the impact of AI on robotic imaging accuracy and understand the training requirements for robotic surgery systems to ensure successful integration.

- A key consideration is the potential for workflow improvements with automated imaging, which often outperform legacy systems by a two-to-one margin in high-volume settings. When comparing robotic vs. manual biopsy precision, data consistently favors automated platforms.

- The ROI of robotic imaging in orthopedic surgery is significant, driven by improved patient outcomes in robotic joint replacement and enhanced robotic spine surgery navigation accuracy. Furthermore, these systems play a crucial role in reducing radiation with robotic c-arm systems.

- The future of autonomous medical imaging systems depends on resolving challenges like data interoperability for robotic platforms and establishing robust security protocols for remote robotic surgery. For institutions aiming to expand care, tele-robotic ultrasound for rural healthcare access offers a transformative solution.

- Integrating robotic imaging with hospital PACS is critical for a seamless workflow, as is understanding the regulatory pathways for AI-enabled imaging devices.

- Ultimately, the focus is on leveraging robotic systems for minimally invasive oncology and robotic imaging for cardiovascular interventions, addressing the ergonomic benefits for sonographers using robotics, and utilizing MRI-compatible robotics for neurosurgery and AI-powered image analysis in robotic systems.

What are the key market drivers leading to the rise in the adoption of Robotic Medical Imaging Systems Industry?

- The technological integration of AI and automation is a primary driver for the robotic medical imaging systems market, enhancing diagnostic capabilities and workflow efficiency.

- Market growth is primarily driven by the integration of AI and the urgent need for operational efficiency. AI-driven workflow automation and autonomous diagnostic imaging are transforming radiology departments, improving diagnostic throughput by up to 40%.

- The adoption of CT-based navigation and real-time image fusion allows for sub-millimeter accuracy in complex procedures, a key factor in neurosurgical navigation systems and interventional radiology. Furthermore, these systems standardize image quality, which reduces retake rates by 25%.

- The demand for remote real-time ultrasound examinations is met by platforms that incorporate clinical decision support tools, helping to bridge the expertise gap in underserved areas.

- This convergence of technologies is making robotic-assisted procedures safer and more consistent, directly impacting patient care and hospital workflows.

What are the market trends shaping the Robotic Medical Imaging Systems Industry?

- The integration of machine learning is a key trend, enhancing precision in robotic medical imaging systems. This shift transforms static hardware into intelligent, data-driven platforms.

- Key trends in the robotic medical imaging systems market are centered on intelligent automation and remote capabilities. The integration of image recognition software and robotic needle positioning is enabling a new level of precision in robotic biopsy guidance, enhancing needle placement accuracy by 20%.

- Advancements in tele-robotic ultrasound and tele-sonography systems, often equipped with a haptic feedback mechanism and remote real-time ultrasound examinations, are addressing workforce shortages and expanding diagnostic reach. These automated medical imaging platforms reduce procedure times by 15%.

- This shift toward AI in medical diagnostics and robotic microsurgery systems is creating more efficient and accessible healthcare solutions, with a strong focus on improving surgical outcome standardization and remote diagnostic imaging.

What challenges does the Robotic Medical Imaging Systems Industry face during its growth?

- The high cost of acquisition and maintenance presents a significant challenge, impacting the adoption rate of advanced robotic medical imaging systems.

- Significant challenges in the robotic medical imaging systems market include high initial costs and complex technical integration. The implementation of a complete cardiovascular workspace or platforms with force-sensing technology requires a capital outlay that can be 3-5 times higher than conventional equipment.

- Integrating these systems into existing hospital IT infrastructures, or achieving seamless digital twin integration, can increase project timelines by up to 60%. The development of digital surgical ecosystems and ensuring compatibility with various intraoperative imaging solutions present ongoing hurdles.

- As the industry moves toward value-based healthcare technology, justifying the high costs of systems with specialized features like a robotic-assisted knee and hip replacements or advanced imaging and informatics tools remains a primary focus for healthcare administrators.

Exclusive Technavio Analysis on Customer Landscape

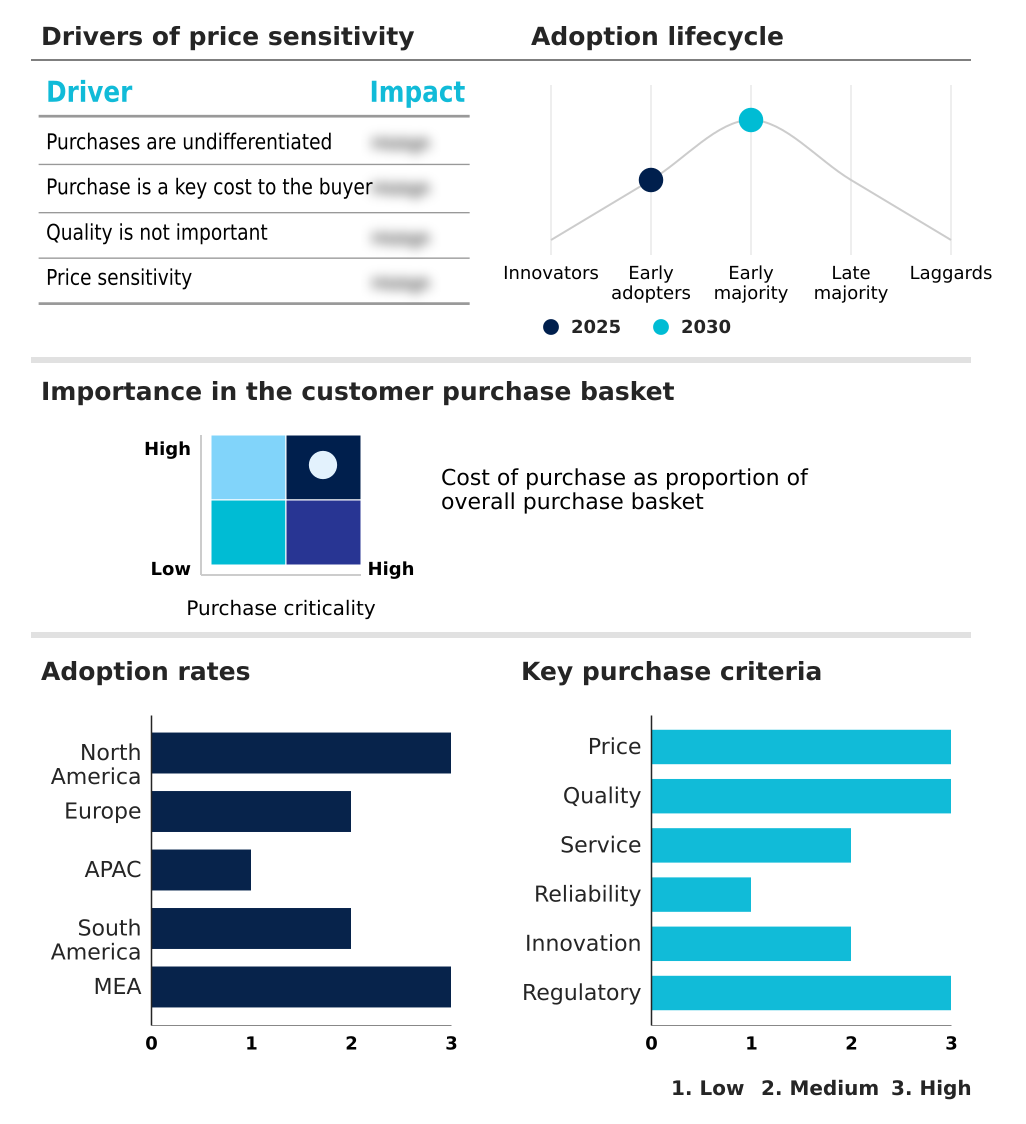

The robotic medical imaging systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the robotic medical imaging systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Robotic Medical Imaging Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, robotic medical imaging systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdEchoTech - Delivers advanced telerobotic ultrasound systems, enabling remote, real-time diagnostic examinations through proprietary, internally designed and manufactured solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdEchoTech

- Asensus Surgical US Inc.

- Brainlab AG

- General Electric Co.

- Globus Medical Inc.

- Intuitive Surgical Inc.

- Johnson and Johnson Services

- KUKA AG

- Medtronic Plc

- MGI Tech Co. Ltd.

- Neocis Inc.

- NeuraSignal Inc.

- Perfint Healthcare Corp.

- Renishaw Plc

- Siemens Healthineers AG

- Smith and Nephew plc

- Stereotaxis Inc.

- Stryker Corp.

- Synaptive Medical Inc.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Robotic medical imaging systems market

- In August, 2024, PROCEPT BioRobotics Corp. received FDA 510(k) clearance for its HYDROS Robotic System, which features the FirstAssist AI software for analyzing ultrasound and cystoscopy images to suggest treatment plans.

- In November, 2024, Rush University System for Health acquired the Epione robotic platform from Quantum Surgical, becoming the first hospital in the Midwest to use the technology for minimally invasive treatment of abdominal tumors.

- In March, 2025, GE HealthCare and NVIDIA announced a strategic collaboration to develop autonomous imaging systems using physical AI, enabling devices to perceive patient positioning and automate imaging protocols.

- In April, 2025, United Imaging Healthcare announced that its advanced imaging products had achieved coverage in over 70% of United States administrative regions, indicating a significant expansion of its high-end imaging modalities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Robotic Medical Imaging Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.2% |

| Market growth 2026-2030 | USD 1036.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The robotic medical imaging systems market is defined by a technological shift toward integrated, intelligent platforms. Advanced systems now incorporate not just robotic c-arm positioning and intraoperative 3d imaging but also a haptic feedback mechanism and force-sensing technology for enhanced procedural control. The use of a mobile ct scanner, augmented intelligence platforms, and a cardiovascular workspace is becoming standard.

- Key innovations include stereotactic robotic assistance, AI-based live image denoising, motion scaling algorithms, robotic digital microscopy, and robotic exoscope visualization. Platforms featuring a 3dhd vision system, cone-beam ct synchronization, and a photon-counting detector are enabling breakthroughs in image-guided intervention and tele-robotic ultrasound.

- The integration of a remote scanning solution, robotic needle positioning, and image recognition software is central to AI-driven workflow automation. In board-level strategy, a focus on platforms offering digital twin integration and a self-driving mobile c-arm is critical for future-proofing investments.

- Systems that provide automated patient positioning and real-time 3d digital joint models have demonstrated a 25% improvement in diagnostic first-pass accuracy. The market is also seeing adoption of robotic-assisted bronchoscopy and technologies like the laser-guided mobile gantry to support minimally invasive tumor ablation and advanced primary and revision capabilities.

What are the Key Data Covered in this Robotic Medical Imaging Systems Market Research and Growth Report?

-

What is the expected growth of the Robotic Medical Imaging Systems Market between 2026 and 2030?

-

USD 1.04 billion, at a CAGR of 17.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (X-ray, Ultrasound, MRI, and CT-scan), Application (Interventional radiology, Orthopedic and spine surgery, Neurosurgery, and Others), End-user (Hospitals, Specialty clinics, and Ambulatory surgical centers) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Technological integration of AI and automation, High cost of acquisition and maintenance

-

-

Who are the major players in the Robotic Medical Imaging Systems Market?

-

AdEchoTech, Asensus Surgical US Inc., Brainlab AG, General Electric Co., Globus Medical Inc., Intuitive Surgical Inc., Johnson and Johnson Services, KUKA AG, Medtronic Plc, MGI Tech Co. Ltd., Neocis Inc., NeuraSignal Inc., Perfint Healthcare Corp., Renishaw Plc, Siemens Healthineers AG, Smith and Nephew plc, Stereotaxis Inc., Stryker Corp., Synaptive Medical Inc. and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The dynamics of the robotic medical imaging systems market are shaped by the push for improved surgical outcomes and greater operational efficiency.

- The adoption of image-guided surgery and robotic-assisted procedures is driven by compelling clinical data; robotic assistance has been shown to improve procedural consistency by over 30%, while automated medical imaging workflows reduce scan setup times by an average of 15%.

- This focus on workflow efficiency in radiology is a direct response to staffing shortages and the need to maximize patient throughput. Furthermore, the integration of robotic biopsy guidance and tele-sonography systems is expanding access to high-quality diagnostics.

- Technologies that enable radiation exposure reduction and support orthopedic surgical robots are becoming standard in advanced healthcare settings, underpinning the shift toward safer and more precise interventions.

We can help! Our analysts can customize this robotic medical imaging systems market research report to meet your requirements.

RIA -

RIA -