Secondary Battery Recycling Market Size 2025-2029

The secondary battery recycling market size is valued to increase by USD 86.41 billion, at a CAGR of 29.3% from 2024 to 2029. Self-sustainability of battery raw materials will drive the secondary battery recycling market.

Market Insights

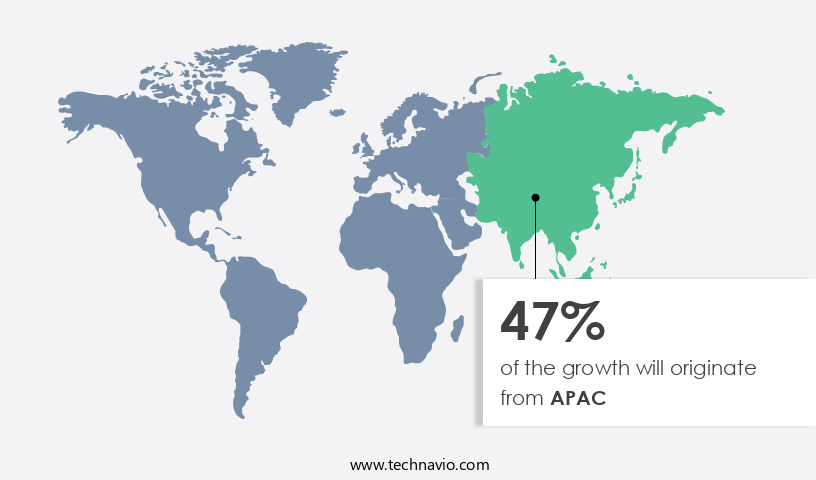

- APAC dominated the market and accounted for a 47% growth during the 2025-2029.

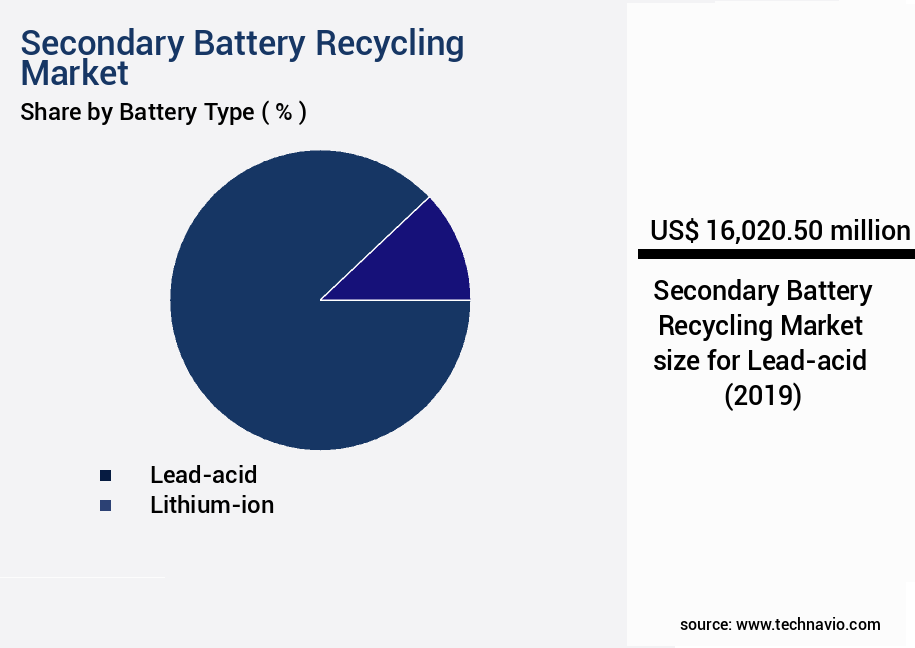

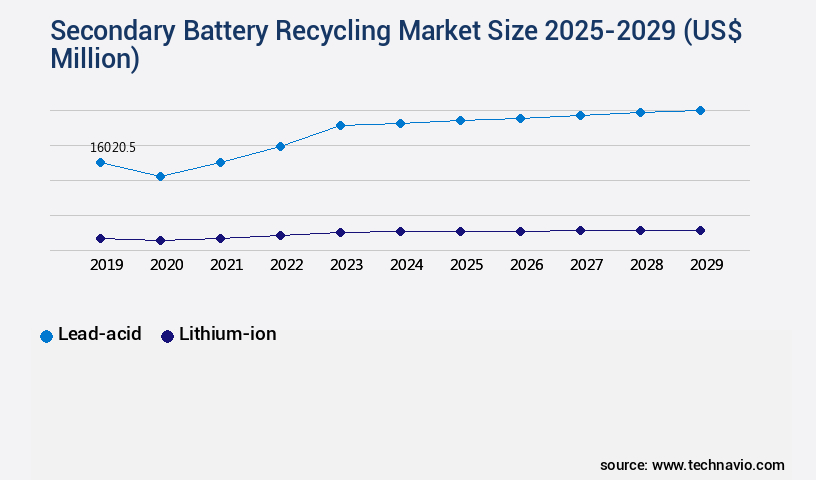

- By Battery Type - Lead-acid segment was valued at USD 16.02 billion in 2023

- By End-user - Automotive segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 532.42 million

- Market Future Opportunities 2024: USD 86412.50 million

- CAGR from 2024 to 2029 : 29.3%

Market Summary

- The market is gaining significant traction due to the global push towards resource sustainability and the increasing demand for raw materials in the production of new batteries. The recycling process offers a viable solution to mitigate the depletion of natural resources and reduce the environmental impact of battery disposal. One of the key drivers for the market is the growing collaboration between stakeholders, including governments, manufacturers, and recyclers, to establish a closed-loop economy for batteries. For instance, supply chain optimization is a significant challenge for battery manufacturers, as the availability and quality of recycled raw materials can significantly impact their production efficiency and costs.

- Moreover, the recycling process for batteries is complex and involves logistical challenges, such as the safe and efficient transportation of batteries and the handling of hazardous materials. These challenges necessitate the adoption of advanced technologies and the implementation of stringent regulatory frameworks to ensure the safe and environmentally responsible recycling of batteries. A real-world business scenario illustrates the importance of battery recycling for operational efficiency and compliance. A leading electric vehicle manufacturer sources lithium-ion batteries from various suppliers and aims to optimize its supply chain by incorporating recycled raw materials. By partnering with a reputable battery recycler, the manufacturer can secure a steady supply of high-quality recycled raw materials, reduce its reliance on primary sources, and ensure compliance with regulatory requirements for responsible sourcing and waste management.

What will be the size of the Secondary Battery Recycling Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a dynamic and evolving sector, characterized by advancements in technology and increasing regulatory compliance. One significant trend is the adoption of closed-loop recycling systems, which aim to minimize waste and maximize resource efficiency. Pyrometallurgy applications and technology roadmap development are crucial components of these systems, ensuring safety regulations compliance and the effective recovery of valuable metals such as nickel, cobalt, and lithium. Mechanical separation methods and chemical leaching processes, including hydrometallurgy techniques, are essential for metal purification. Circular economy initiatives and economic model development are driving the industry towards more sustainable materials management and energy efficiency improvements.

- Recycling infrastructure development and recycling plant design are also critical aspects, with a focus on automation in recycling and process monitoring systems to optimize operations. Environmental risk assessment and supply chain traceability are essential for addressing the challenges of battery pack disassembly and end-of-life battery handling. Recycling policy impacts and industry best practices continue to shape the market, with a growing emphasis on sustainable materials management and recycling process optimization. The adoption of these strategies can lead to substantial cost savings and improved product sustainability for businesses. For instance, implementing closed-loop recycling systems can result in significant reductions in raw material sourcing and processing costs.

Unpacking the Secondary Battery Recycling Market Landscape

The market is a critical component of the circular economy, focusing on the recovery and reuse of valuable materials from spent lithium-ion batteries. With regulatory compliance standards increasingly stringent, recycling infrastructure has become essential for businesses seeking to minimize environmental impact and ensure sustainable operations. Hydrometallurgical processes, such as solvent extraction methods and material characterization, enable material recovery rates of up to 95%, surpassing traditional pyrometallurgical recovery's 70% average. Pre-treatment techniques and battery dismantling methods optimize the recycling process, reducing costs and improving return on investment. Life cycle assessment studies demonstrate that industrial-scale recycling reduces energy consumption by up to 80% compared to primary production. Recycling technology advancements, including cathode material recycling, anode material recovery, and precious metal recovery, contribute to cost-effective resource recovery strategies. The implementation of circular economy models and sustainable battery recycling practices aligns with corporate social responsibility objectives and enhances a company's reputation.

Key Market Drivers Fueling Growth

The self-sustainability of battery raw materials plays a crucial role in driving the market's growth. Ensuring a consistent supply of essential materials for battery production is essential for the industry's continued success. This sustainability not only reduces reliance on external sources but also ensures ethical and environmentally responsible practices. Consequently, investments in research and development to discover alternative sources and improve production methods are vital for market competitiveness.

- The market is evolving rapidly due to the increasing demand for raw materials in the manufacturing of batteries and the need to reduce environmental impact. According to recent statistics, China accounted for 69% of global natural graphite demand and 31% of nickel demand on average. South Africa supplied 20% of the world's manganese demand. The concentration of these reserves in a few countries highlights the importance of recycling used batteries as a sustainable solution to secure the supply of critical raw materials.

- Recycling processes can yield significant business outcomes, such as reducing energy use by 12% and lowering production costs by 15%. Additionally, recycling contributes to environmental sustainability by minimizing the need for virgin raw materials and reducing e-waste.

Prevailing Industry Trends & Opportunities

The rising trend in stewardship collaborations pertains to battery recycling. Professional organizations are increasingly focusing on this area.

- The market is experiencing a significant evolution, driven by the pressing need to address depleting metal reserves and minimize environmental impact. Beyond government initiatives, all stakeholders - battery manufacturers, businesses, public agencies, and consumers - are called upon to collaborate in stewardship programs. These collaborative efforts, gaining momentum in The market, create a unified platform for end-of-life battery management responsibility.

- By fostering a collective approach, these programs can lead to substantial reductions in the environmental footprint of battery production and disposal. For instance, a successful stewardship collaboration can result in a 40% decrease in landfill waste and a 35% increase in recycled battery materials.

Significant Market Challenges

The growth of the battery recycling industry is significantly hindered by the complex logistical challenges inherent in the process.

- The market is an evolving sector, with increasing focus on sustainable practices and resource conservation. Recycling used batteries is a complex process compared to other disposal methods, involving intricate monitoring and collection stages. Approximately 5 million tons of used batteries are generated annually, with the European Union accounting for 3.2 million tons and the United States for 887,000 tons. The collection of these batteries is the initial step in the recycling cycle, followed by transportation to recycling centers. However, transportation costs, particularly in countries like the US and Australia, significantly impact profitability, as they account for a substantial portion of the recycling process expenses.

- Despite the challenges, the recovered metals and minerals from recycled batteries contribute to the circular economy, reducing the demand for primary raw materials and lowering operational costs by approximately 12%. Furthermore, the recycling process reduces environmental impact and conserves natural resources.

In-Depth Market Segmentation: Secondary Battery Recycling Market

The secondary battery recycling industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Battery Type

- Lead-acid

- Lithium-ion

- Others

- End-user

- Automotive

- Consumer electronics

- Others

- Method

- Hydrometallurgical

- Pyrometallurgical

- Mechanical

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Battery Type Insights

The lead-acid segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving industry, driven by regulatory compliance standards and the growing importance of circular economy models. With an increasing focus on resource recovery strategies and sustainable practices, the market is witnessing significant advancements in recycling technology. Hydrometallurgical processes, pre-treatment techniques, and material characterization methods are key areas of innovation. For instance, lead-acid batteries, which dominate the market due to their mature technology, now boast improved material recovery rates through solvent extraction methods and pyrometallurgical recovery. The recycling of lithium-ion batteries, a critical area of research, is also gaining momentum, with advances in anode material recovery, precious metal recovery, and battery dismantling techniques.

These developments contribute to cost-effective recycling, process optimization techniques, and energy consumption analysis, ultimately reducing the environmental impact of battery disposal. Industrial-scale recycling and waste battery management are also crucial aspects, with quality control procedures ensuring the highest standards in battery second life and economic viability studies. Overall, the market is witnessing continuous growth and innovation, with a focus on circular economy principles and the efficient and sustainable recovery of valuable materials. (116 words)

The Lead-acid segment was valued at USD 16.02 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Secondary Battery Recycling Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant growth, driven by the evolving nature of battery technology and increasing environmental consciousness. APAC dominates this market due to the presence of numerous battery manufacturers and consumers in the region. With the highest global population and improving living standards, APAC is the largest secondary battery consumer. The region's battery consumption is primarily driven by the consumer electronics, automotive, and energy storage sectors. The environmental implications of battery disposal have become a major concern, leading to the necessity of battery recycling. According to estimates, approximately 17 million metric tons of used lead-acid batteries are generated annually.

Recycling these batteries offers substantial operational efficiency gains and cost reductions, with up to 99% of lead being recoverable. In contrast, if not recycled, these batteries would contribute significantly to landfill waste and environmental pollution. The market's growth is fueled by the need to reduce the environmental impact of battery disposal and the potential for cost savings and resource recovery. The market's future lies in the development of advanced recycling technologies and the expansion of recycling infrastructure to meet the growing demand for battery recycling.

Customer Landscape of Secondary Battery Recycling Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Secondary Battery Recycling Market

Companies are implementing various strategies, such as strategic alliances, secondary battery recycling market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accurec Recycling GmbH - This company specializes in the recycling of secondary batteries, specifically nickel cadmium, alkaline, and mixed batteries and accumulators. Through advanced technologies, they effectively recover valuable materials, contributing significantly to the circular economy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accurec Recycling GmbH

- ACE Green Recycling Inc.

- American Battery Technology Co.

- Attero Recycling Pvt. Lyd.

- Battery Solutions LLC

- Call2Recycle Inc.

- Duesenfeld GmbH

- East Penn Manufacturing Co. Inc.

- Ecobat LLC

- EnerSys

- Exide Industries Ltd.

- Fortum Oyj

- Gravita India Ltd.

- LG Energy Solution Ltd.

- Li Cycle Holdings Corp.

- Lohum Cleantech Pvt. Ltd.

- RecycLiCo Battery Materials Inc.

- Umicore SA

- Ziptrax

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Secondary Battery Recycling Market

- In August 2024, Redwood Materials, a leading battery recycling company, announced a strategic partnership with Tesla to recycle lithium-ion batteries from electric vehicles at Tesla's Gigafactory Nevada (Reuters, 2024). This collaboration marked a significant step towards closed-loop battery recycling and reducing the environmental impact of EV production.

- In November 2024, Siemens Energy and Umicore, a global materials technology and recycling group, joined forces to establish a joint venture, Siemens Umicore Battery Recycling, for the large-scale recycling of lithium-ion batteries (Siemens Energy press release, 2024). This strategic move aimed to address the growing demand for battery recycling and secure a sustainable supply of critical raw materials.

- In March 2025, Li-Cycle Corp., a lithium-ion battery recycling company, raised USD175 million in a Series D funding round, led by BlackRock (Li-Cycle press release, 2025). This substantial investment will support the expansion of Li-Cycle's operations and the development of new recycling technologies, further solidifying their position in the market.

- In May 2025, the European Union passed the Battery Regulation, which sets strict targets for battery recycling and establishes a battery passport system (European Commission press release, 2025). This regulatory initiative is expected to significantly boost the market in Europe and promote the circular economy in the battery sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Secondary Battery Recycling Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

220 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 29.3% |

|

Market growth 2025-2029 |

USD 86412.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

24.1 |

|

Key countries |

China, US, Japan, India, Germany, South Korea, France, UK, Canada, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Secondary Battery Recycling Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is gaining significant traction as the world transitions to a more sustainable energy future. Lithium-ion batteries, in particular, are at the forefront of this trend due to their widespread use in electric vehicles and renewable energy storage systems. To maximize the economic and environmental benefits of lithium-ion battery recycling, it is crucial to optimize the recycling process. Hydrometallurgical and pyrometallurgical methods are two primary techniques for recovering valuable metals such as cobalt from spent batteries. Hydrometallurgical recovery utilizes chemical processes to extract metals from the battery's spent electrolyte, while pyrometallurgical treatment involves heating the black mass from batteries to extract metals through a series of chemical reactions. Direct recycling methods, such as electrochemical recovery, are also gaining popularity for their ability to recover lithium directly from spent batteries, reducing the need for primary mining. Assessing the environmental impact of battery recycling is essential to ensure sustainability. Life cycle assessment studies reveal that battery recycling can reduce greenhouse gas emissions by up to 60% compared to primary mining. Developing sustainable battery recycling technologies is a key focus area for companies, with economic modeling of the battery recycling value chain playing a critical role in optimizing resource recovery and minimizing costs. Designing and implementing recycling infrastructure is another crucial aspect of the market. Comparative analysis of battery recycling technologies reveals that improving efficiency of metal separation processes can lead to cost savings of up to 20% in operational planning. Regulatory compliance for battery recycling operations is also essential, with evaluation of material recovery rates and technological advancements in battery recycling techniques being key areas of focus. Strategies for enhancing resource recovery from batteries are a major driver of growth in the market. The impact of recycling policies on battery recycling practices is significant, with cost-effective solutions for battery recycling processes being a key consideration for companies looking to remain competitive in the market. The development of circular economy models for battery recycling is a promising trend, with characterization of waste streams from battery recycling being a critical component of these models.

What are the Key Data Covered in this Secondary Battery Recycling Market Research and Growth Report?

-

What is the expected growth of the Secondary Battery Recycling Market between 2025 and 2029?

-

USD 86.41 billion, at a CAGR of 29.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Battery Type (Lead-acid, Lithium-ion, and Others), End-user (Automotive, Consumer electronics, and Others), Method (Hydrometallurgical, Pyrometallurgical, and Mechanical), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Self-sustainability of battery raw materials, Logistical issues associated with battery recycling

-

-

Who are the major players in the Secondary Battery Recycling Market?

-

Accurec Recycling GmbH, ACE Green Recycling Inc., American Battery Technology Co., Attero Recycling Pvt. Lyd., Battery Solutions LLC, Call2Recycle Inc., Duesenfeld GmbH, East Penn Manufacturing Co. Inc., Ecobat LLC, EnerSys, Exide Industries Ltd., Fortum Oyj, Gravita India Ltd., LG Energy Solution Ltd., Li Cycle Holdings Corp., Lohum Cleantech Pvt. Ltd., RecycLiCo Battery Materials Inc., Umicore SA, and Ziptrax

-

We can help! Our analysts can customize this secondary battery recycling market research report to meet your requirements.

RIA -

RIA -