Semiconductor Clock Market Size 2024-2028

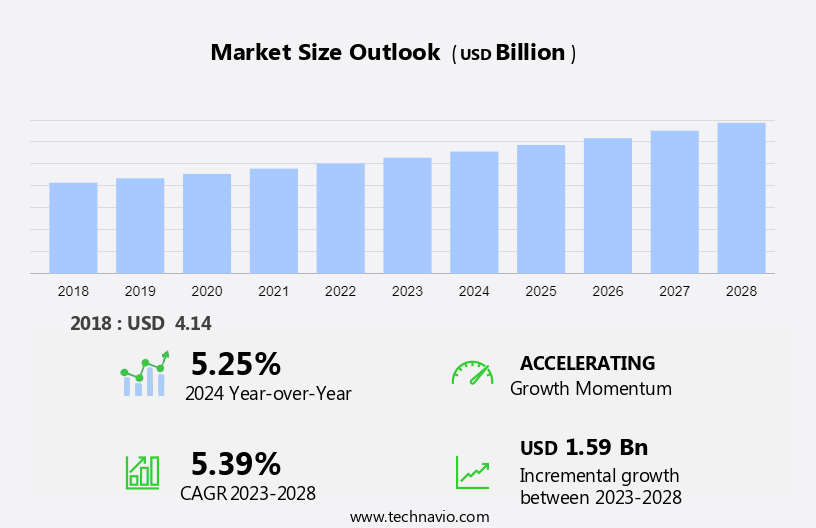

The semiconductor clock market size is forecast to increase by USD 1.59 billion at a CAGR of 5.39% between 2023 and 2028. The market is experiencing significant growth due to the increasing adoption of automotive electronics and advanced driver-assistance systems (ADAS), which rely heavily on precise timing provided by semiconductor clocks. Furthermore, the integration of advanced timing technologies, such as MEMS oscillators and crystal oscillators, in semiconductor clocks is driving market growth. However, global chip shortages pose a major challenge to market growth, as the production of semiconductor clocks and other electronic components is impacted. Despite this challenge, the market is expected to continue expanding due to the growing demand for high-performance electronic devices in various industries, including automotive, telecommunications, and consumer electronics.

The market is driven by the increasing demand for timekeeping solutions in electronic devices, embedded systems, servers, personal computers, and various new-age electronic devices. Real-time clocks (RTCs) integrated in semiconductors play a crucial role in ensuring accurate timekeeping for these devices. The market is witnessing significant growth due to the increasing use of semiconductor clocks in time-critical operations, industrial devices, computing devices, consumer electronics, automotive systems, industrial automation, aerospace, telecommunications networks, and various new-age electronic devices such as smartphones, smart TVs, electric vehicles, and security systems. MEMS technologies, specifically MEMS oscillators, are gaining popularity due to their low power consumption and high precision.

Further, time base oscillators, such as crystal oscillators, continue to be widely used in semiconductor clock ICs. The automotive automation, chip production, and security systems industries also contribute to the growth of the market. The integration of semiconductor clock ICs in system-on-chip (SOC) and mems-based oscillators in AI applications is expected to further boost market growth.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Type

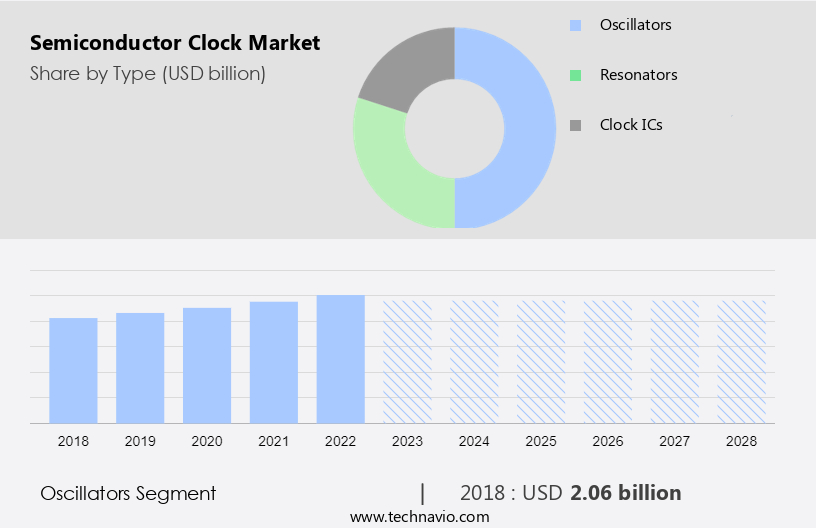

- Oscillators

- Resonators

- Clock ICs

- End-user

- Consumer electronics

- Telecom

- Automobile

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- South America

- Middle East and Africa

- APAC

By Type Insights

The oscillators segment is estimated to witness significant growth during the forecast period. Semiconductor clock oscillators, also known as Real-time clocks (RTC) or timebase oscillators, play a crucial role in microprocessors and microcontrollers by supplying the essential timing signals for instruction execution and synchronizing the operation of central processing units in electronic devices and embedded systems. In the realm of consumer electronics, semiconductor clock oscillators are indispensable components in various devices such as smartphones, tablets, smart TVs, and audio systems. These oscillators ensure precise timekeeping for the functioning of processors, memory, and other components. In the telecommunications sector, semiconductor clock oscillators are instrumental in maintaining synchronization and facilitating data transmission. They are employed extensively in networking equipment, including switches, routers, hubs, base stations, and other telecommunications devices.

Moreover, these clock oscillators provide synchronized clock signals for efficient data transmission and network coordination. Industrial applications, such as industrial automation, aerospace, and automotive systems, also heavily rely on semiconductor clock oscillators for time-critical operations. MEMS (Micro-Electro-Mechanical Systems) technologies, including MEMS oscillators, have emerged as a popular choice due to their low power consumption and high accuracy. Semiconductor clock ICs, which incorporate these MEMS-based oscillators, are increasingly being adopted in various applications, from computing devices and consumer electronics to industrial devices and new-age electronic devices. Semiconductor clock oscillators are also essential components in the production of chips, as they provide precise timing during the manufacturing process.

Get a glance at the market share of various segments Request Free Sample

The oscillators segment was valued at USD 2.06 billion in 2018 and showed a gradual increase during the forecast period. Furthermore, in the context of automotive automation, semiconductor clock oscillators ensure accurate timekeeping for various systems, including engine control, powertrain management, and safety systems. In the realm of security systems, semiconductor clock oscillators provide precise timing for various functions, including access control and alarm systems. The semiconductor sales landscape is significantly influenced by the demand for semiconductor clock oscillators, as they are integral components in various electronic devices, computing devices, consumer electronic devices, industrial devices, telecommunications networks, automotive systems, industrial automation, aerospace, and system-on-chip (SoC) applications. With the ongoing advancements in AI and other emerging technologies, the demand for semiconductor clock oscillators is expected to continue growing.

Regional Insights

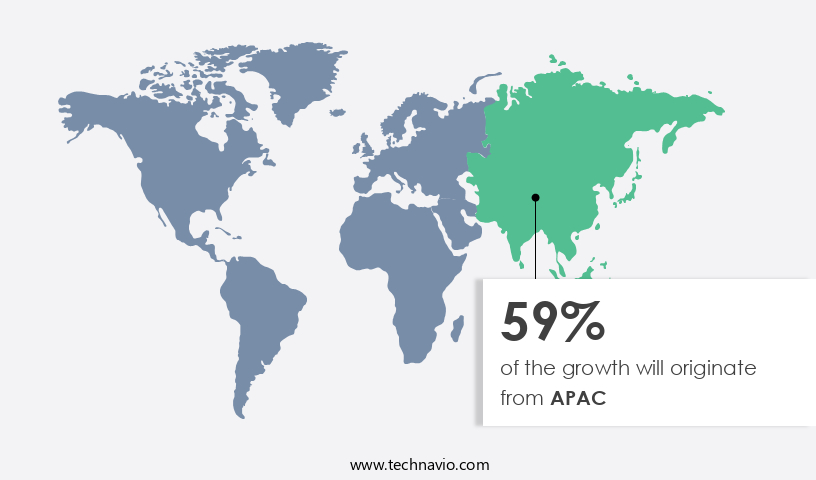

APAC is estimated to contribute 59% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in the APAC region is poised for substantial expansion due to the rapid technological advancements in the semiconductor industry. Innovations in clock technologies, such as high-frequency clocks and advanced timing solutions, are driving market growth. The region's significant consumption of electronic devices and components, fueled by the increasing demand for smartphones, tablets, wearables, and consumer electronics, necessitates precise timing solutions provided by semiconductor clocks. Moreover, the expanding middle-class population and urbanization in APAC further boost the demand for electronic devices and semiconductor components, including clocks, in various applications, such as 5G networks, IoT devices, autonomous vehicles, and advanced driver-assistance systems (ADAS).

Additionally, machine learning algorithms and high data transmission rates in these applications necessitate timing accuracy, which is ensured by advanced clock technologies like Analog Devices' crystal oscillators, MEMS oscillators, and RC oscillators. Integration challenges in these complex systems necessitate the development of low-power clocks to maintain optimal performance and prolong battery life.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Semiconductor Clock Market Driver

The growing adoption of automotive electronics and ADAS is the key driver of the market. Semiconductor clocks play a crucial role in modern electronic devices, including embedded systems, servers, personal computers, consumer electronic devices, telecommunications networks, industrial devices, automotive systems, aerospace, and system-on-chip (SoC) applications. Precise timekeeping is essential for time-critical operations, real-time data processing, and synchronization of sensors, cameras, and components. Integrated Circuit (IC) solutions, such as semiconductor clock ICs, are increasingly being adopted to meet the demands of these applications. MEMS technologies, including MEMS oscillators, have gained popularity due to their low power consumption and high stability. For instance, MEMS-based oscillators like Microchip Technology Inc.'s DSA557-03/04/05 family offer low noise jitter and high stability across a wide range of supply voltages and temperatures.

Moreover, these clocks are used in various applications, including automotive automation, ADAS technologies, and consumer electronics, such as smartphones, smart TVs, electric vehicles, and security systems. Semiconductor sales continue to grow as the demand for electronic devices and new-age electronic devices increases. Crystal oscillators and time base oscillators remain popular choices for clock generation, but MEMS-based oscillators offer advantages in terms of size, power consumption, and stability. Semiconductor clock ICs are essential components in these applications, ensuring accurate and timely responses and enabling advanced features in electronic devices.

Semiconductor Clock Market Trends

Integration of advanced timing technologies in semiconductor clocks is the upcoming trend in the market. Semiconductor clocks, integral to timekeeping in electronic devices, play a vital role in ensuring precise and synchronized operations. Real-time clocks (RTCs), a type of semiconductor clock, are widely used in embedded systems, servers, personal computers, and consumer electronic devices for maintaining accurate time. MEMS technologies, including MEMS oscillators, have emerged as a preferred choice for clock generation due to their low power consumption and high precision. In the era of IoT and AI, semiconductor clock ICs are increasingly being integrated into System-on-Chip (SoC) designs for various applications, including telecommunications networks, consumer electronics, automotive systems, industrial automation, aerospace, and more. Efficient clock distribution is essential for time-critical operations, requiring careful consideration of signal propagation, skew, and interference.

Furthermore, crystal oscillators and time base oscillators are traditional clock solutions, but MEMS-based oscillators offer advantages in terms of size, power consumption, and noise jitter. The market encompasses a diverse range of applications, from chip production and industrial devices to computing devices and consumer electronic devices, including smartphones, smart TVs, electric vehicles, and security systems.

Semiconductor Clock Market Challenge

Global chip shortages is a key challenge affecting the market growth. Semiconductor clocks, also known as Real-time clocks (RTC) or timebase oscillators, play a crucial role in timekeeping for various electronic devices, including embedded systems, servers, personal computers, consumer electronic devices, computing devices, industrial devices, telecommunications networks, automotive systems, industrial automation, aerospace, and system-on-chip (SoC). These Integrated Circuit (IC) components ensure accurate and reliable timekeeping for time-critical operations. Semiconductor clock sales have overflowed due to the increasing demand for electronic devices driven by trends such as remote work, online learning, and increased connectivity. MEMS technologies, specifically MEMS oscillators, have gained popularity due to their low power consumption and high precision.

However, the semiconductor industry has faced challenges in meeting the growing demand for semiconductor clocks due to chip shortages. Factors contributing to the chip shortages include increased demand, production challenges of semiconductor manufacturing, and geopolitical issues. The swell in demand for consumer electronic devices, such as smartphones, smart TVs, electric vehicles, and security systems, has outpaced the production capacity of semiconductor manufacturers. As a result, semiconductor clock manufacturers have faced challenges in fulfilling orders within expected timelines, leading to extended manufacturing lead times. Semiconductor clock manufacturers must navigate these challenges while maintaining high standards for noise jitter, power consumption, and precision.

Crystal oscillators and MEMS-based oscillators are popular choices due to their low power consumption and high precision. The market is expected to continue growing, driven by the increasing demand for electronic devices and the adoption of advanced technologies such as artificial intelligence (AI).

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Abracon LLC - The company offers semiconductor clock such as ClearClock. They also offer PLL based ClearClock solutions and Third Overtone ClearClock solutions.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adolf Wurth GmbH and Co. KG

- Analog Devices Inc.

- ASGN Inc.

- Daishinku Corp.

- ifm electronic gmbh

- Infineon Technologies AG

- KYOCERA Corp.

- MegaChips Corp.

- Microchip Technology Inc.

- MinebeaMitsumi Inc.

- Murata Manufacturing Co. Ltd.

- NXP Semiconductors NV

- Renesas Electronics Corp.

- Ricoh Co. Ltd.

- ROHM Co. Ltd.

- Seiko Epson Corp.

- STMicroelectronics International N.V.

- Texas Instruments Inc.

- TXC Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is driven by the increasing demand for real-time clock (RTC) integrated circuits (ICs) in various electronic devices. These ICs are essential for timekeeping in embedded systems, servers, personal computers, and consumer electronic devices. The market is witnessing significant growth due to the increasing usage of low power consumption clocks in time-critical operations. Mems technologies, such as mems oscillators, are gaining popularity in the market due to their high precision and low noise jitter. The semiconductor sales are expected to grow in the consumer electronic devices, computing devices, industrial devices, telecommunications networks, automotive systems, industrial automation, aerospace, and newage electronic devices sectors. However, the market faces challenges such as noise jitter and power consumption in high-frequency applications. The integration of AI and system-on-chip (SOC) technologies in semiconductor clocks is expected to provide opportunities for market growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.39% |

|

Market Growth 2024-2028 |

USD 1.59 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.25 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 59% |

|

Key countries |

US, China, Japan, Taiwan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abracon LLC, Adolf Wurth GmbH and Co. KG, Analog Devices Inc., ASGN Inc., Daishinku Corp., ifm electronic gmbh, Infineon Technologies AG, KYOCERA Corp., MegaChips Corp., Microchip Technology Inc., MinebeaMitsumi Inc., Murata Manufacturing Co. Ltd., NXP Semiconductors NV, Renesas Electronics Corp., Ricoh Co. Ltd., ROHM Co. Ltd., Seiko Epson Corp., STMicroelectronics International N.V., Texas Instruments Inc., and TXC Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- A thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -