Semiconductor Sensors Market Size 2025-2029

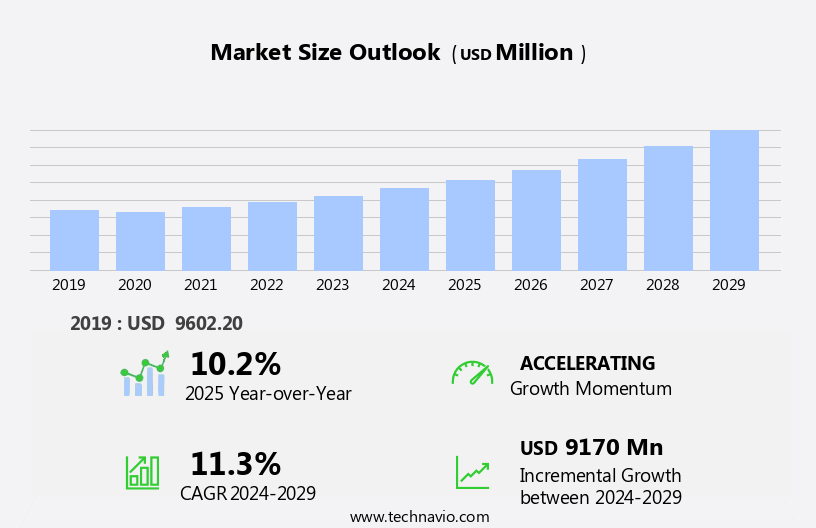

The semiconductor sensors market size is forecast to increase by USD 9.17 billion, at a CAGR of 11.3% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing demand for smart devices. The proliferation of Internet of Things (IoT) technology and the integration of sensors in various applications, from automotive to healthcare, fuel this trend. Technological advancements in semiconductor sensor technology further boost market growth, enabling smaller, more efficient, and cost-effective sensors. However, the semiconductor industry faces challenges, including the impact of trade wars on global supply chains and component pricing.

- Geopolitical tensions can lead to tariffs and import/export restrictions, disrupting the flow of raw materials and finished goods. Companies must navigate these challenges by diversifying their supply chains, investing in local manufacturing, and building strategic partnerships to mitigate risks and maintain competitiveness.

What will be the Size of the Semiconductor Sensors Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in wireless communication, embedded systems, and packaging technologies. These innovations enable new applications across various sectors, including defense, healthcare monitoring, precision agriculture, aerospace, environmental sensing, and automotive. Wireless communication plays a crucial role in enabling real-time data acquisition and transfer, while embedded systems facilitate the integration of sensors into various devices. Packaging technologies ensure the durability and reliability of sensors in harsh environments. Optical sensors, pressure sensors, temperature sensors, and flow sensors are among the various types of sensors that find applications in these sectors. Calibration methods, signal processing, and data analytics are essential for ensuring accurate and reliable sensor performance.

Defense applications require sensors with high environmental robustness and operating temperature range. Healthcare monitoring demands sensors with low power consumption and miniaturization. Precision agriculture requires sensors that can detect humidity and temperature levels in soil. Aerospace applications necessitate sensors with high response time and chemical sensing capabilities. Environmental sensing requires sensors that can detect gas levels and noise reduction. Automotive applications require sensors that can withstand high temperatures and provide real-time data. Semiconductor materials, etching techniques, and interface protocols are among the ongoing research areas that aim to improve sensor performance and reduce power consumption. Machine learning and artificial intelligence are also being integrated into sensors to enhance data processing and analysis capabilities.

In summary, the market is characterized by continuous innovation and evolving patterns, driven by advancements in wireless communication, embedded systems, and packaging technologies. These innovations enable new applications across various sectors, from defense and healthcare to agriculture and automotive. The market's dynamism is reflected in ongoing research in areas such as semiconductor materials, etching techniques, and artificial intelligence.

How is this Semiconductor Sensors Industry segmented?

The semiconductor sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product Type

- Temperature Sensor

- Pressure Sensor

- Humidity sensor

- Others

- Type

- Wireless

- Wired

- Application

- Consumer electronics

- Automotive

- Industrial

- Others

- Technology

- MEMS

- CMOS

- Optical Sensors

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

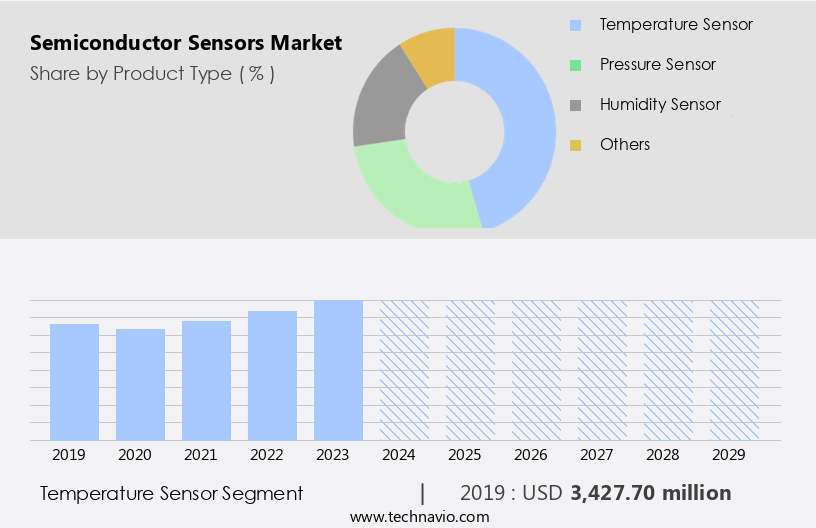

By Product Type Insights

The temperature sensor segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant advancements, with various entities playing pivotal roles in shaping its dynamics. Temperature sensors, a crucial segment, are experiencing robust growth due to their application in industries such as automotive, consumer electronics, industrial automation, and healthcare. These sensors are vital for monitoring and managing thermal conditions in systems requiring precision and reliability. Recent innovations in sensor miniaturization and digital interface integration, including I2C, SPI, and SMBus, have expanded their usage in compact and power-sensitive applications. In automotive systems, temperature sensors are increasingly integrated into battery management systems, engine control units, and cabin climate systems to ensure optimal performance and safety.

The growing trend towards electric vehicles (EVs) is further fueling demand, as thermal regulation is essential for battery longevity and efficiency. Optical sensors, another significant segment, are gaining traction due to their ability to detect light and convert it into electrical signals. They find extensive applications in industries such as industrial automation, consumer electronics, and healthcare monitoring. Cloud connectivity and data analytics are transforming the sensor landscape by enabling real-time data processing and analysis, thereby enhancing system performance and efficiency. Power consumption is a critical concern, leading to the development of power management and energy management solutions. Semiconductor materials, such as silicon, gallium arsenide, and gallium nitride, are driving advancements in sensor fabrication and integration.

Machine learning and artificial intelligence (AI) are being integrated into sensors to improve signal processing, calibration methods, and noise reduction. These technologies are revolutionizing various industries, from industrial automation and consumer electronics to healthcare monitoring and environmental sensing. The market is also witnessing the adoption of MEMS sensors, image sensors, and CMOS sensors, which offer enhanced performance and miniaturization. Pressure sensors, flow sensors, gas sensors, humidity sensors, and chemical sensors are other essential segments catering to diverse applications. Security protocols and packaging technologies are critical considerations to ensure sensor reliability and durability. The market's future growth is expected to be influenced by factors such as operating temperature range, environmental robustness, wireless communication, and defense applications.

The Temperature Sensor segment was valued at USD 3.43 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

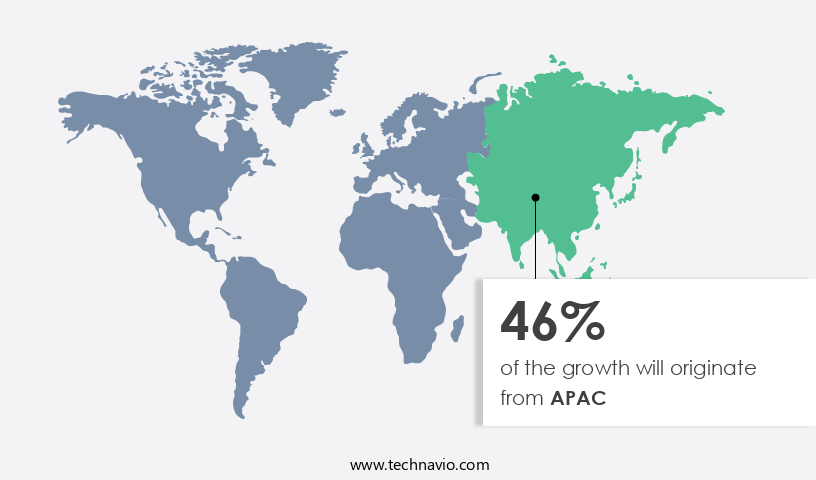

APAC is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC), comprising countries like China, Japan, South Korea, India, and Taiwan, is experiencing significant growth. Key drivers include the presence of prominent semiconductor manufacturers, increasing consumer electronics demand, and the integration of advanced technologies such as automation and 5G networks. In May 2025, an HCL-Foxconn joint venture received approval from the Indian Union Cabinet to build a Rs.3,706 crore (approx. USD445 million USD) semiconductor facility in Uttar Pradesh. This plant will produce 36 million display driver chips monthly for various devices, including mobile phones, laptops, and automobiles. APAC's the market is further characterized by advancements in technology, with innovations in areas such as Analog-to-digital conversion (ADC), temperature compensation, optical sensors, industrial automation, interface protocols, proximity sensors, signal processing, calibration methods, thin-film deposition, pressure sensors, data analytics, sensor fabrication, sensor integration, temperature sensors, data acquisition, flow sensors, security protocols, software algorithms, consumer electronics, power consumption, smart cities, operating temperature range, environmental robustness, wireless communication, embedded systems, packaging technologies, defense applications, healthcare monitoring, precision agriculture, aerospace applications, environmental sensing, noise reduction, gas sensors, etching techniques, automotive applications, chemical sensors, semiconductor materials, response time, image sensors, machine learning, power management, humidity sensors, MEMS sensors, CMOS sensors, artificial intelligence (AI), and energy management.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Semiconductor Sensors Industry?

- The surge in consumer preference for intelligent devices serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing integration of technology into everyday life and the expanding Internet of Things (IoT) ecosystem. Semiconductor sensors are integral to the functionality of smart devices, enabling data acquisition for temperature, flow, and other applications. The IoT's ability to connect devices and systems has led to the development of smart homes, cities, and other intelligent environments. Key factors driving the market include the need for real-time data acquisition, energy efficiency, and security protocols. Software algorithms and advanced sensor fabrication techniques have improved sensor performance and reduced power consumption.

- Consumer electronics, industrial automation, and automotive industries are major end-users of semiconductor sensors. Semiconductor sensors offer environmental robustness and a wide operating temperature range, making them suitable for various applications. The market's future growth is expected to be driven by advancements in sensor integration, miniaturization, and the increasing demand for wearable devices and autonomous vehicles. The market is a dynamic and evolving industry, with continuous innovation and technological advancements shaping its future.

What are the market trends shaping the Semiconductor Sensors Industry?

- The current market trend reflects a significant focus on technological advancements in semiconductor sensor technology. This sector is poised for growth due to its innovative capabilities and potential applications.

- The market has witnessed significant growth in recent times, fueled by the expanding use of wireless communication in various sectors and the integration of sensors in embedded systems. The adoption of advanced packaging technologies, defense applications, healthcare monitoring, precision agriculture, aerospace, environmental sensing, and noise reduction are key market drivers. Gas sensors, particularly those based on etching techniques, have gained prominence due to their high sensitivity and selectivity.

- The market's growth is further propelled by the increasing demand for semiconductor sensors in automotive applications, including advanced driver assistance systems and electric vehicles. Despite the challenges of supply shortages and price increases due to high demand, the market continues to evolve, offering opportunities for innovation and growth.

What challenges does the Semiconductor Sensors Industry face during its growth?

- The semiconductor industry faces significant challenges to its growth due to the impact of trade wars. This geopolitical issue poses a major threat to the industry's expansion, requiring close attention and strategic adaptation from industry professionals.

- The market is experiencing significant fluctuations due to geopolitical tensions, particularly the trade war between major global players. This conflict has resulted in tariffs and restrictions on various goods, including semiconductor materials and electronic components. The increased cost of these materials has led to a rise in the average selling price (ASP) of semiconductor sensors, affecting demand in both the US and China. This imbalance between supply and demand could hinder the growth plans of semiconductor manufacturers, potentially reducing the market's expansion during the forecast period. Semiconductor sensors play a crucial role in various industries, including chemical sensing, image sensing, and humidity detection, among others.

- Technological advancements in machine learning and artificial intelligence (AI) are driving innovation in this sector, with applications in power management and energy efficiency. MEMS (Micro-Electro-Mechanical Systems) and CMOS (Complementary Metal-Oxide-Semiconductor) sensors are gaining popularity due to their high sensitivity, low power consumption, and compact size. However, the escalating trade tensions pose a challenge to the market's growth trajectory. Semiconductor sensors are integral to numerous applications, including healthcare, automotive, industrial, and consumer electronics. The market's dynamics are influenced by factors such as response time, power management, and miniaturization. Despite the current challenges, the long-term outlook remains positive, with continued advancements in technology and increasing demand for energy-efficient and cost-effective sensors.

Exclusive Customer Landscape

The semiconductor sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, semiconductor sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Eaton Corp. plc - This company specializes in semiconductor sensor technology, featuring the innovative EVT Series VoltageWatch voltage sensors and VoltageWatch sensors. These advanced products monitor and detect voltage levels with precision, contributing significantly to the global market for semiconductor sensors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Eaton Corp. plc

- Fuji Electric Co. Ltd.

- Infineon Technologies AG

- Littelfuse Inc.

- Mitsubishi Electric Corp.

- Nexperia BV

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- STMicroelectronics NV

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Corp.

- Vishay Intertechnology Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Semiconductor Sensors Market

- In January 2024, Infineon Technologies AG, a leading semiconductor manufacturer, announced the launch of its new RaspiSense⢠sensor platform, integrating microcontrollers and sensors for Internet of Things (IoT) applications (Infineon press release, 2024). This development marks Infineon's expansion into the IoT sensor market, aiming to provide comprehensive solutions for smart home and industrial automation.

- In March 2024, STMicroelectronics and Bosch Sensortec, two major semiconductor sensor players, announced a strategic collaboration to develop and manufacture MEMS microphones for automotive and consumer applications (STMicroelectronics press release, 2024). This partnership combines STMicroelectronics' semiconductor expertise with Bosch Sensortec's sensor technology, targeting the growing demand for voice-activated devices and advanced driver assistance systems.

- In May 2024, ON Semiconductor Corporation completed the acquisition of Fujitsu Semiconductor Limited's 200mm wafer fabrication facility in Aizu, Japan (ON Semiconductor press release, 2024). This strategic move enables ON Semiconductor to expand its manufacturing capacity for image sensors and other semiconductor products, addressing the increasing demand for advanced sensors in various industries.

- In April 2025, Texas Instruments Incorporated unveiled its new MSP432P401R microcontroller, featuring a built-in sensor fusion engine and improved power management capabilities (Texas Instruments press release, 2025). This technological advancement enables more efficient and accurate sensor data processing for IoT and industrial applications, positioning Texas Instruments as a key player in the semiconductor sensor market.

Research Analyst Overview

- The market encompasses various types of sensors, including optical fiber sensors, electrochemical sensors, piezoresistive sensors, capacitive sensors, inductive sensors, thermoelectric sensors, and quantum sensors. One notable trend is the integration of system-on-a-chip (SOC) technology, which enables advanced functionalities and cost reduction. Testing and validation plays a crucial role in ensuring sensor quality and compliance with technical documentation and industry standards. Intellectual property protection is another key consideration, as companies strive to differentiate their offerings through innovation. Multi-sensor fusion and product lifecycle management are essential strategies for optimizing sales channels and meeting customer demands. Cost reduction and low-power design are also critical factors, as sensors increasingly permeate various industries, from automotive to healthcare.

- Supply chain management and standards compliance are essential for maintaining a competitive edge, as companies navigate the complexities of manufacturing, logistics, and regulatory requirements. Customer support and after-sales services are also vital for building long-term relationships and fostering repeat business. Sensor arrays and pricing strategies are other areas of focus, as companies seek to offer comprehensive solutions and maximize revenue while maintaining profitability. Overall, the market is characterized by continuous innovation, intense competition, and evolving customer needs.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Semiconductor Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

213 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.3% |

|

Market growth 2025-2029 |

USD 9170 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

10.2 |

|

Key countries |

US, China, Japan, UK, South Korea, India, Germany, France, Taiwan, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Semiconductor Sensors Market Research and Growth Report?

- CAGR of the Semiconductor Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the semiconductor sensors market growth of industry companies

We can help! Our analysts can customize this semiconductor sensors market research report to meet your requirements.

RIA -

RIA -