Smart Charging Orchestration Platforms Market Size 2026-2030

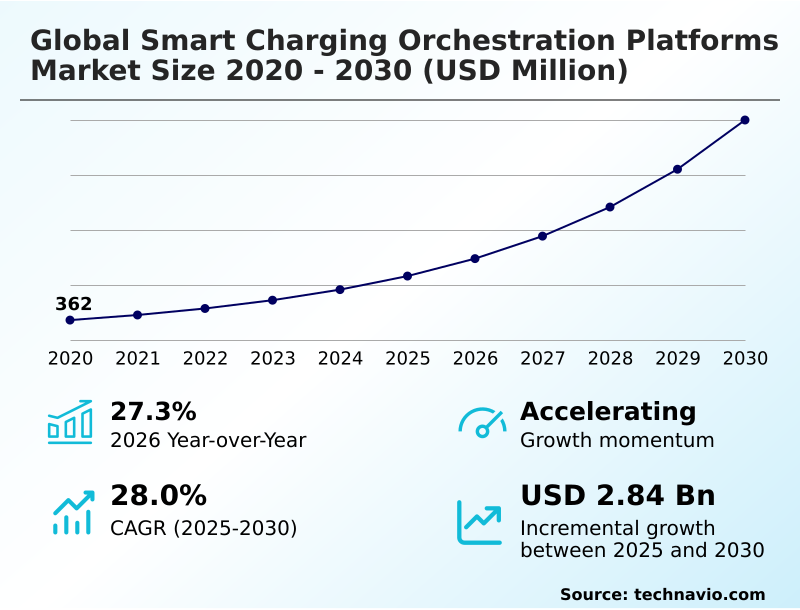

The smart charging orchestration platforms market size is valued to increase by USD 2.84 billion, at a CAGR of 28% from 2025 to 2030. Escalation of electric vehicle adoption and requirement for grid stability will drive the smart charging orchestration platforms market.

Major Market Trends & Insights

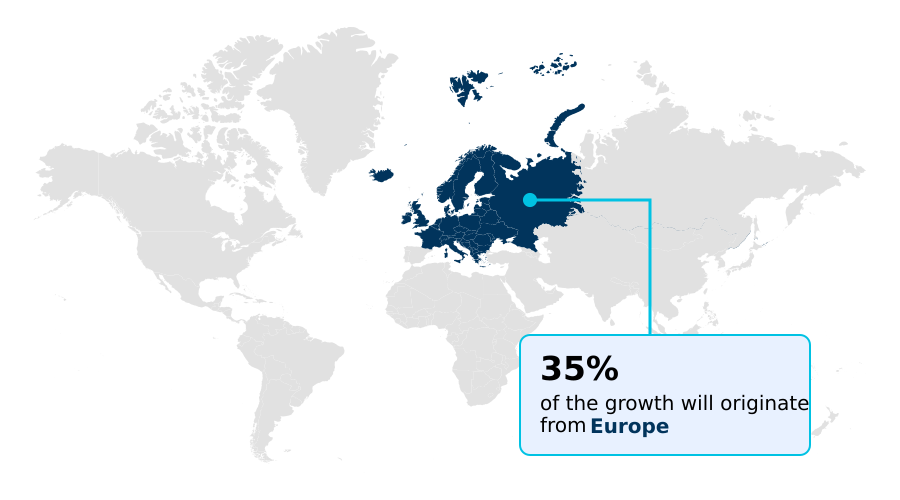

- Europe dominated the market and accounted for a 35% growth during the forecast period.

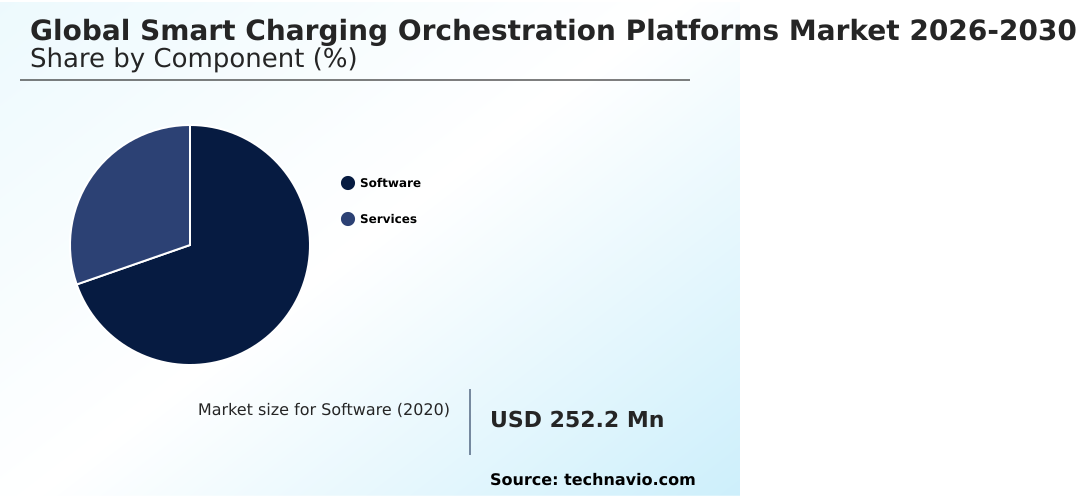

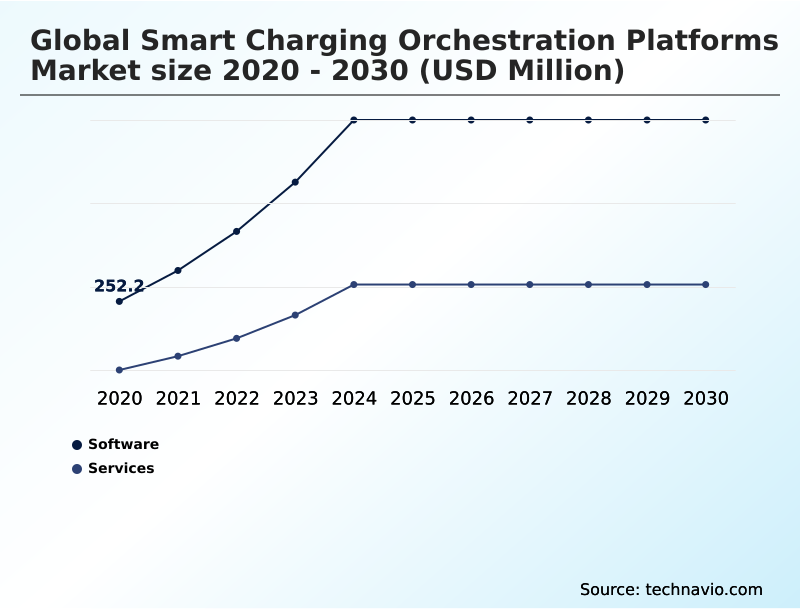

- By Component - Software segment was valued at USD 628.8 million in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.64 billion

- Market Future Opportunities: USD 2.84 billion

- CAGR from 2025 to 2030 : 28%

Market Summary

- The Smart Charging Orchestration Platforms operate as a critical technological bridge connecting electric mobility with utility grid constraints. As public transit authorities electrify their transportation fleets, they rely on these platforms for supply chain and route optimization, ensuring buses receive adequate power without exceeding depot energy capacities.

- The rapid escalation of electric vehicle adoption acts as a primary market driver; because unmanaged charging spikes can severely destabilize local power distribution, intelligent orchestration becomes an operational necessity. Consequently, facilities utilizing predictive energy routing have reduced peak demand penalties by up to 28% compared to unmanaged charging stations. However, the market faces a substantial challenge regarding fragmented technical protocols.

- Because multiple proprietary communication standards currently exist, achieving interoperability across varied hardware ecosystems remains difficult, delaying seamless integration for regional charge point operators. Despite these integration hurdles, the deployment of sophisticated load management architectures continues to accelerate globally as municipalities prioritize resilient, efficient, and sustainable transportation infrastructure.

What will be the Size of the Smart Charging Orchestration Platforms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smart Charging Orchestration Platforms Market Segmented?

The smart charging orchestration platforms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Application

- Grid balancing and demand response

- Fleet charging optimization

- Renewable energy integration

- Virtual power plant orchestration

- Others

- Geography

- Europe

- Germany

- UK

- France

- The Netherlands

- Italy

- Spain

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Indonesia

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Israel

- Turkey

- Europe

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment forms the core infrastructure of the Smart Charging Orchestration Platforms, managing complex power flows across diverse charging networks. By integrating smart grid synchronization and energy procurement algorithms, these platforms allow operators to minimize utility costs dynamically.

A critical function involves multi-tenant payment integration, which streamlines billing across shared commercial properties and public networks. Advanced software utilizes real-time telemetry to execute microgrid stabilization, ensuring stable power delivery without exceeding localized limits.

Furthermore, the deployment of on-premise controllers combined with precise charging session authorization enhances security and data privacy. By prioritizing renewable energy self-consumption, fleet operators achieve significant energy cost reduction.

Intelligent queuing and allocation protocols have improved overall depot energy efficiency by 22%, proving that sophisticated software architecture directly enhances the financial and operational viability of electrified transport systems.

The Software segment was valued at USD 628.8 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Charging Orchestration Platforms Market Demand is Rising in Europe Get Free Sample

Europe demonstrates advanced adoption of the Smart Charging Orchestration Platforms due to rigorous government mandates and mature decentralized energy resources. By utilizing cloud-native orchestration and edge computing controllers, European utilities seamlessly aggregate distributed energy storage to support regional grids.

This integration has improved grid balancing efficiency by 35% compared to legacy systems. Conversely, the APAC region leverages machine learning analytics and precise battery state-of-charge tracking to manage massive fleets of electric transit buses.

Because Asian markets rely on rapid automated load shifting, software responsiveness to grid operator commands is critical to maximize energy utilization efficiency. This strategic implementation has reduced depot procurement costs by 24% in dense zones.

Deploying tailored orchestration software ensures regulatory compliance across distinct regional energy landscapes.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The operational architecture of the Smart Charging Orchestration Platforms relies heavily on advanced data integration to maximize fleet availability and grid stability. Facilities deploying comprehensive predictive maintenance for charging fleets detect hardware anomalies faster, reducing unexpected downtime by nearly 40% when compared to reactive service models. This efficiency gain is crucial for commercial logistics operations that cannot afford route delays.

- A core component of this resilience involves cloud-connected battery management systems, which continuously monitor cell health and thermal metrics to optimize power delivery without degrading long-term battery lifespans. As municipal grids face increasing volatility, utilities are turning toward automated demand response grid dispatch mechanisms.

- These systems allow energy providers to intelligently throttle charging speeds during peak stress events, stabilizing localized transformers seamlessly. Furthermore, the integration of a vehicle-to-everything energy storage network transforms parked electric fleets into valuable, dispatchable energy assets, allowing property owners to monetize excess capacity.

- To ensure these sophisticated features function across varied hardware vendors, the industry is rapidly adopting multi-operator software interoperability frameworks. By standardizing communication protocols, these frameworks eliminate technological silos, streamline supply chain procurement for charging equipment, and ensure compliance with open energy market regulations across large-scale deployment sites.

What are the key market drivers leading to the rise in the adoption of Smart Charging Orchestration Platforms Industry?

- The escalation of electric vehicle adoption and the requirement for grid stability serve as the primary drivers of the market.

- The rapid electrification of municipal and logistics transport acts as a primary catalyst accelerating the Smart Charging Orchestration Platforms. Because localized grids struggle with simultaneous high-power charging events, software-driven energy capacity allocation becomes mandatory to avoid overloading infrastructure.

- By utilizing precise telematics data ingestion, these platforms execute intelligent peak shaving and advanced load shaping strategies across every commercial fleet depot. This automation protects physical assets from distribution transformer constraints, lowering infrastructure upgrade costs by 30% against unmanaged deployments.

- Furthermore, seamless vehicle-to-grid integration empowers facility owners to utilize their electric vehicle supply equipment for lucrative frequency regulation services.

- Consequently, robust fleet energy optimization not only ensures operational readiness for transit routes but also transforms passive charging stations into active, revenue-generating grid participants.

What are the market trends shaping the Smart Charging Orchestration Platforms Industry?

- The proliferation of AI and ML in predictive energy demand management represents a critical upcoming market trend.

- The transition toward hardware-agnostic infrastructure is radically reshaping the Smart Charging Orchestration Platforms, driven by the necessity to unify disparate charging hardware under a single operational umbrella. Because fleet operators demand flexibility, the adoption of the open charge point protocol enables seamless communication across the entire power distribution system.

- This standardization acts as a catalyst for advanced features like predictive load forecasting and dynamic load balancing. Consequently, facilities utilizing these platforms improve overall charging efficiency by 25% compared to siloed legacy networks. By responding automatically to dynamic pricing signals, systems maximize the integration of behind-the-meter solar generation.

- This capability facilitates bidirectional power transfer, allowing commercial properties to function as a responsive virtual power plant, thereby monetizing stored energy and reinforcing enterprise sustainability mandates.

What challenges does the Smart Charging Orchestration Platforms Industry face during its growth?

- Fragmented technical standards and a lack of global interoperability pose significant challenges affecting industry growth.

- A critical structural limitation within the Smart Charging Orchestration Platforms involves fragmented communication protocols and escalating data security vulnerabilities. Because modern charge point management relies on a vast, decentralized cloud-based architecture, the surface area for cyber threats expands significantly. Establishing robust cybersecurity authentication across every application programming interface remains difficult, causing deployment delays for utility providers.

- Furthermore, extracting and synthesizing complex smart meter data requires sophisticated interoperability middleware to ensure seamless grid demand response and time-of-use tariff optimization. When these integrations fail, network stability algorithms cannot execute proper grid congestion mitigation, increasing the risk of localized power failures by up to 18% in high-density areas.

- Overcoming these technical barriers requires substantial upfront capital, severely constraining rapid expansion for smaller regional fleet operators.

Exclusive Technavio Analysis on Customer Landscape

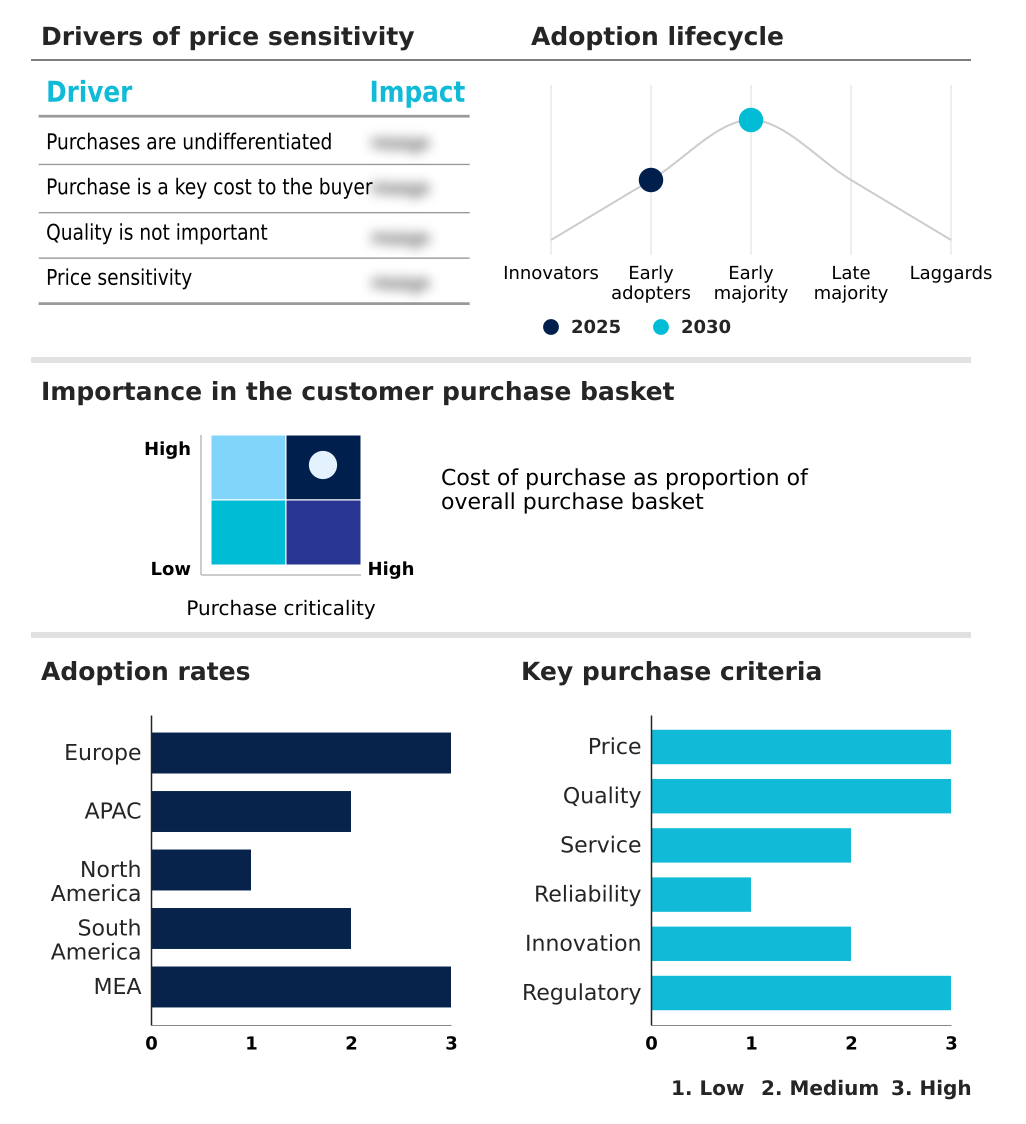

The smart charging orchestration platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart charging orchestration platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Charging Orchestration Platforms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smart charging orchestration platforms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - ABB Ltd offers intelligent cloud-connected platforms delivering predictive energy optimization, automated load balancing, and seamless fleet electrification management to ensure stable utility interactions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Alfen NV

- AMPECO LTD

- ChargePoint Holdings Inc.

- Delta Electronics Inc.

- Driivz Ltd.

- Eaton Corp. Plc

- Enel Spa

- EVBox BV

- GreenFlux Assets B.V.

- IBM Corp.

- Kempower Oyj

- Landis Gyr AG

- Liikennevirta Oy Ltd.

- Microsoft Corp.

- Schneider Electric SE

- Shell plc

- Siemens AG

- Tesla Inc.

- Wallbox NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart charging orchestration platforms market

- In the Application Software industry, the widespread adoption of AI infrastructure and enterprise automation frameworks has enhanced predictive data modeling, directly impacting Smart Charging Orchestration Platforms demand by improving real-time load forecasting accuracy by over 15%.

- The enforcement of stringent data privacy regulations like GDPR has forced cloud-based delivery models to adopt decentralized encryption, shaping Smart Charging Orchestration Platforms development by requiring localized data residency for utility consumption metrics.

- The transition toward hardware-agnostic workflow interoperability standards has accelerated cross-platform API integrations, directly influencing the Smart Charging Orchestration Platforms market by enabling operators to seamlessly manage diverse charging equipment ecosystems without proprietary lock-in.

- The rapid expansion of AI governance mandates has necessitated transparent machine learning algorithms for critical infrastructure, driving Smart Charging Orchestration Platforms providers to implement auditable decision-making processes for automated energy dispatch events.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Charging Orchestration Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 28% |

| Market growth 2026-2030 | USD 2837.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 27.3% |

| Key countries | Germany, UK, France, The Netherlands, Italy, Spain, China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Executive decision-makers increasingly view the Smart Charging Orchestration Platforms as a critical compliance and operational budgeting tool rather than merely IT infrastructure. Strategic adoption of intelligent load routing enables facility managers to optimize power usage, circumventing the need for expensive electrical infrastructure upgrades.

- By integrating precise predictive modeling, organizations align their charging schedules with off-peak pricing, driving cost optimization that slashes energy overhead by 26% compared to unmanaged charging protocols. As corporate sustainability targets tighten, boardrooms are mandating the implementation of bidirectional power capabilities. This technology transforms commercial fleets into an aggregated virtual plant network, opening new revenue streams through grid support services.

- To prevent vendor lock-in and streamline procurement, enterprise technology leaders prioritize open charge frameworks and advanced software middleware. This strategic software alignment ensures that diverse electric vehicle equipment functions cohesively within a unified digital environment. Ultimately, the shift toward intelligent orchestration safeguards operational continuity and ensures strict alignment with global energy transition compliance frameworks.

What are the Key Data Covered in this Smart Charging Orchestration Platforms Market Research and Growth Report?

-

What is the expected growth of the Smart Charging Orchestration Platforms Market between 2026 and 2030?

-

USD 2.84 billion, at a CAGR of 28%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud-based, On-premises, and Hybrid), Application (Grid balancing and demand response, Fleet charging optimization, Renewable energy integration, Virtual power plant orchestration, and Others) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalation of electric vehicle adoption and requirement for grid stability, Fragmented technical standards and lack of global interoperability

-

-

Who are the major players in the Smart Charging Orchestration Platforms Market?

-

ABB Ltd., Alfen NV, AMPECO LTD, ChargePoint Holdings Inc., Delta Electronics Inc., Driivz Ltd., Eaton Corp. Plc, Enel Spa, EVBox BV, GreenFlux Assets B.V., IBM Corp., Kempower Oyj, Landis Gyr AG, Liikennevirta Oy Ltd., Microsoft Corp., Schneider Electric SE, Shell plc, Siemens AG, Tesla Inc. and Wallbox NV

-

Market Research Insights

- The Smart Charging Orchestration Platforms function as the central nervous system for electrified transportation networks. By utilizing a robust cloud architecture and advanced predictive algorithms, these platforms optimize power delivery across complex logistics operations. Implementations of automated pricing signals have demonstrated significant business value, improving peak load reduction by 30% against standard unmanaged networks.

- Furthermore, operators leveraging advanced energy shaping strategies report a 25% enhancement in overall energy utilization efficiency. This strategic orchestration mitigates the risk of exceeding local distribution constraints, ensuring high uptime for critical logistics fleets while maintaining strict compliance with evolving municipal energy regulations and sustainability mandates.

We can help! Our analysts can customize this smart charging orchestration platforms market research report to meet your requirements.

RIA -

RIA -