Support Services Market Size 2025-2029

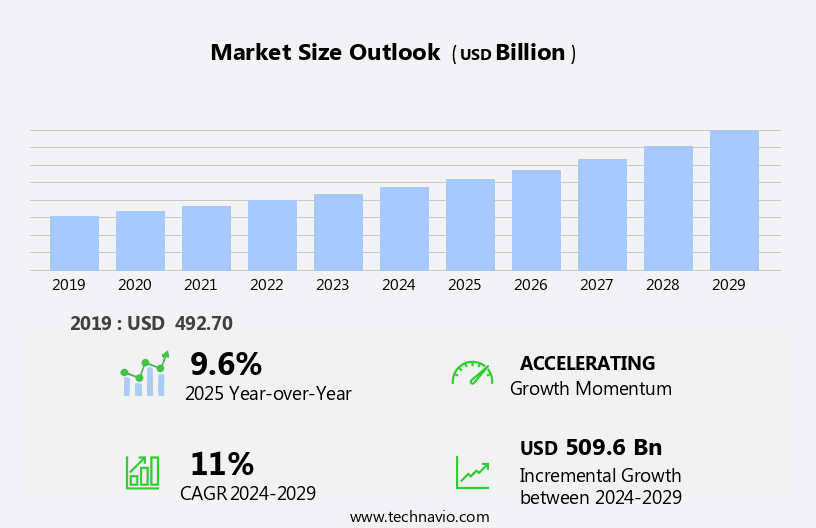

The support services market size is forecast to increase by USD 509.6 billion at a CAGR of 11% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing demand from the aviation industry. This sector's reliance on efficient and effective support services is crucial for maintaining operational excellence and ensuring customer satisfaction. Another key trend shaping the market is the adoption of artificial intelligence (AI) models in support services. By automating routine tasks and providing personalized solutions, AI is transforming the way businesses deliver support services. Regulatory standards and data security concerns continue to shape the market, with ITIL frameworks and incident response plans ensuring compliance and business continuity.

- Companies must invest in robust security measures and contingency plans to mitigate these risks and maintain customer trust. To capitalize on the opportunities presented by this dynamic market and navigate the challenges effectively, businesses must stay informed about the latest trends and developments in support services. However, this market is not without challenges. Technological disruptions, such as cybersecurity threats and system failures, pose significant risks to the smooth operation of support services. However, the market also faces challenges from technological disruptions, such as cybersecurity threats and the need for continuous innovation to keep up with evolving customer needs and expectations.

What will be the Size of the Support Services Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- In today's business landscape, exceptional customer support is crucial for retaining clients and ensuring business continuity. The market is evolving rapidly, with trends leaning towards omnichannel and multi-channel support to cater to diverse customer preferences. Virtual agents and machine learning are revolutionizing support processes, enabling proactive engagement and predictive analytics for support cost optimization. Mobile support apps and self-service portals have become essential tools for on-the-go assistance, while knowledge management systems facilitate efficient problem resolution.

- Service desk outsourcing and customer journey mapping are popular strategies for optimizing support processes, while online support communities and artificial intelligence enable 24/7 assistance. Disaster recovery and ITIL frameworks ensure business continuity, while support contract negotiation and customer experience remain key focus areas for organizations. Proactive support and support process improvement are critical for reducing customer churn, with AI and ML-powered tools enabling personalized, timely interventions. Virtual reality and augmented reality are emerging technologies enhancing customer experience, while predictive analytics and incident response plans enable effective issue resolution. Regardless of industry, businesses must adapt to these trends to stay competitive, focusing on support cost optimization, data security, and customer retention.

How is this Support Services Industry segmented?

The support services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Service Type

- Hardware

- Software

- End-user

- Small and medium enterprises

- Large enterprises

- Delivery Mode

- Online

- Offline

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

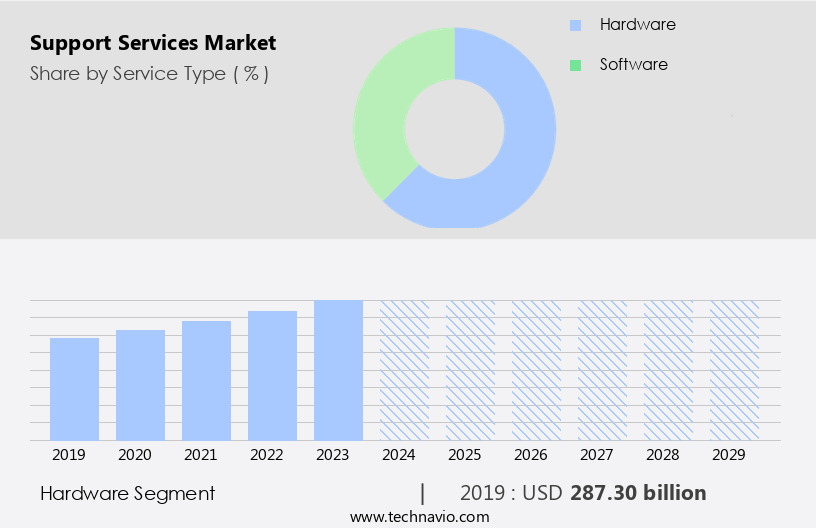

By Service Type Insights

The hardware segment is estimated to witness significant growth during the forecast period. The market is undergoing substantial changes, with a focus on enhancing customer experience and optimizing operational efficiency. Service desk automation and incident management solutions are gaining popularity, streamlining processes and reducing response times. In the hardware sector, there is a shift towards subscription-based models, allowing businesses to access advanced technology with predictable costs and flexibility. This trend is especially prevalent in industries that demand rugged devices, where continuous upgrades and maintenance are crucial for productivity. Additionally, the market is witnessing an increase in staff augmentation services, providing businesses with skilled professionals to address their support needs.

Customer satisfaction remains a top priority, driving the adoption of user-friendly help desk software, knowledge base management, and remote support solutions. Change management and problem resolution are also critical areas of focus, with IT support teams leveraging performance monitoring, security support, integration services, consulting services, and field technicians to ensure seamless implementation and maintenance of systems. Remote access solutions and cloud support are becoming essential for businesses seeking to enable their workforce to operate from anywhere. The market is further evolving with the integration of artificial intelligence and machine learning, enabling proactive problem resolution and personalized customer experiences. A key trend driving market expansion is the integration of advanced technologies, such as artificial intelligence (AI) models into customer support systems.

Overall, the market is continuously adapting to meet the evolving needs of businesses and consumers, with a strong emphasis on innovation and customer satisfaction.

The Hardware segment was valued at USD 287.30 billion in 2019 and showed a gradual increase during the forecast period.

The Support Services Market is evolving with robust third-party support, offering businesses specialized assistance. The ITIL framework ensures streamlined service management, while an effective incident response plan enhances operational resilience. Customer Relationship Management (CRM) strengthens engagement, integrating a knowledge management system for efficient issue resolution. Innovations in machine learning (ML) refine predictive support, while augmented reality (AR) and virtual reality (VR) enhance interactive troubleshooting. The rise of self-service portals empowers users, backed by omnichannel support for seamless communication. Prioritizing customer experience (CX) drives higher Net Promoter Score (NPS) and Customer Effort Score (CES), reflecting service quality and satisfaction. Outsourcing trends indicate a growing reliance on business support services for administrative functions, customer interactions, and data analytics.

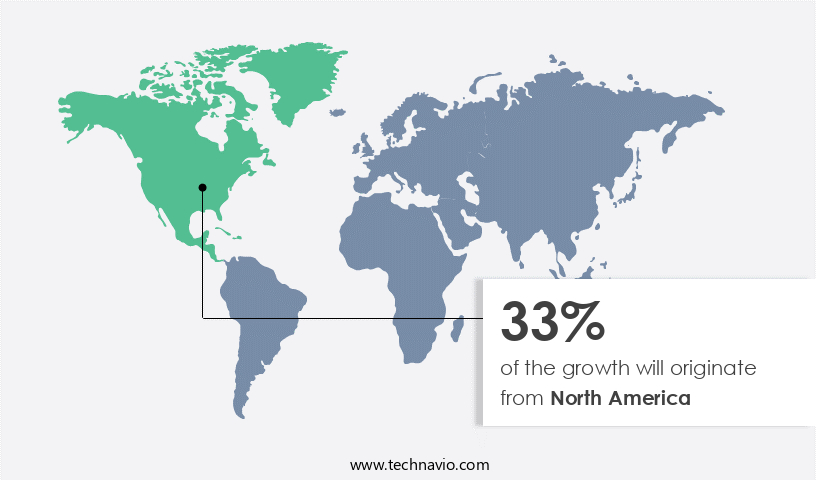

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market is undergoing considerable expansion, fueled by technological advancements and the growing demand for reliable IT infrastructure. A notable trend in this market is the modernization of enterprise IT systems. In April 2024, a critical US military command initiated a major overhaul of its IT infrastructure, securing contracts worth over USD900 million. This modernization project incorporates advanced technologies such as artificial intelligence (AI) and machine learning to optimize data management and decision-making processes. The command's transition to a new cloud computing environment aims to boost operational efficiency and agility. Service desk automation, change management, and incident management are key components of this modernization, ensuring efficient problem resolution and improved customer satisfaction. Outsourcing trends indicate a growing reliance on business support services for administrative functions, customer interactions, and data analytics.

Support engineers and help desk analysts are instrumental in implementing these solutions, while knowledge base management and technical documentation facilitate the learning process. Asset management and performance monitoring ensure optimal utilization of resources, and security support safeguards the new infrastructure. Integration services, consulting services, and managed services further enhance the value proposition of these solutions. Field service, network support, and remote support cater to diverse requirements, while community support and support forums foster collaboration and knowledge sharing. Cloud support and release management enable seamless software updates, and database support ensures data integrity. Root cause analysis and escalation management maintain service quality, and technical support teams provide ongoing assistance.

Hardware support and service request management complete the comprehensive suite of services offered in the North American market.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Support Services market drivers leading to the rise in the adoption of Industry?

- The aviation industry's growing need for support services serves as the primary market driver. In the business landscape of 2024, the market for support services experiences significant growth, fueled by technological advancements in problem resolution and operational management. Companies are embracing AI-driven solutions, automation, and multilingual support systems to deliver superior customer experiences and optimize operations. For instance, in the aviation sector, Air India has augmented its customer support infrastructure. The airline has integrated additional languages into its interactive voice response (IVR) system, catering to a broader audience. This intelligent IVR system identifies customer preferences based on mobile network data, thereby reducing response times and boosting efficiency. Moreover, Air India has set up new contact centers, providing 24/7 assistance with specialized services for premium and frequent flyers.

- Beyond this, support services encompass various aspects, including remote support, user guides, training and education, asset management, incident reporting, data center support, knowledge articles, managed services, and help desk analysts. Remote support enables businesses to address issues in real-time, while user guides and training materials ensure efficient onboarding of new employees or users. Asset management helps organizations maintain their hardware and software resources, while incident reporting facilitates tracking and resolution of issues. Data center support and knowledge articles offer critical information and assistance for technical challenges, while managed services and help desk analysts provide ongoing support and expertise.

What are the Support Services market trends shaping the Industry?

- The increasing implementation of artificial intelligence (AI) in support services signifies a significant market trend. This adoption of advanced technologies is becoming increasingly mandatory for businesses seeking to enhance customer experience and operational efficiency. The market is undergoing a significant transformation as businesses increasingly adopt artificial intelligence (AI) models to enhance customer interactions, automate tasks, and optimize operational efficiency. By 2024, AI-powered customer support systems had become more sophisticated, utilizing natural language processing and machine learning to deliver personalized and responsive assistance.

- These advanced AI solutions are revolutionizing various support services, including security, network, application, software, release management, incident management, integration, and cloud support, to name a few. The adoption of advanced support services continues to gain momentum, driven by the need for efficient problem resolution, enhanced customer experiences, and operational optimization. Companies are leveraging a range of solutions, from AI-powered systems to human support, to cater to their diverse needs and deliver value to their customers. Companies are integrating AI chatbots, virtual assistants, and automated workflows to manage a higher volume of customer inquiries with greater accuracy and speed, leading to improved customer satisfaction. A notable trend in the industry is the growing use of generative AI models, which enable businesses to offer more intuitive and context-aware support experiences.

How does Support Services market faces challenges during its growth?

- The growth of the support services industry is significantly impacted by technological disruptions, which present a key challenge in the form of instability and change to traditional operations. The market faces ongoing challenges from technological disruptions, affecting various industries. Recent incidents, including system failures at major companies such as McDonald's, United Airlines, and the London Stock Exchange, have highlighted the vulnerability of businesses to communication breakdowns and operational challenges. These disruptions were not limited to a specific region, with reports of technical issues impacting businesses in Japan, India, and the United States.

- Service catalogs and remote access solutions facilitate efficient service request management, ensuring that technical issues are addressed promptly and accurately. Onsite support remains an essential aspect of support services, particularly for complex hardware and software issues. However, remote access solutions are increasingly popular, allowing support teams to address issues more quickly and cost-effectively. IT and database support, technical support, and hardware support teams play a crucial role in addressing these disruptions. Root cause analysis and escalation management are essential components of effective support services, enabling businesses to minimize downtime and restore operations as quickly as possible.

Exclusive Customer Landscape

The support services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the support services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, support services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company provides a range of support services, including AppleCare, cloud solutions, digital content, and payment processing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Apple Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- FUJIFILM Holdings Corp.

- HCL Technologies Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- Lenovo Group Ltd.

- Microsoft Corp.

- Panasonic Holdings Corp.

- Quatrro Inc.

- S and P Global Inc.

- Samsung Electronics Co. Ltd.

- SAP SE

- Toshiba Corp.

- Wipro Ltd.

- Zenoti

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Support Services Market

- In January 2024, IBM announced the acquisition of Day One Technologies, a leading provider of IT modernization and cloud services for the public sector. The deal, valued at USD400 million, aimed to expand IBM's footprint in the government sector and enhance its cloud capabilities (IBM Press Release, 2024).

- In March 2024, Accenture and Microsoft entered into a strategic partnership to deliver industry-specific cloud solutions, combining Accenture's industry expertise with Microsoft's Azure platform. This collaboration aimed to help businesses in various sectors, including healthcare and finance, to accelerate their digital transformation (Microsoft News Center, 2024).

- In May 2024, Cognizant and Tata Consultancy Services (TCS) announced a merger of their engineering services businesses, forming a new entity called Mindtree-R&D Services. The combined entity was expected to serve over 350 clients and employ more than 45,000 professionals, making it a significant player in the engineering services market (Cognizant Press Release, 2024).

- In January 2025, Google Cloud received a major boost when the U.S. General Services Administration awarded it a spot on the Centers of Excellence (CoE) contract for cloud services. This contract, worth over USD 1 billion, would enable Google Cloud to provide services to various U.S. Government agencies, expanding its presence in the public sector (GSA Press Release, 2025).

Research Analyst Overview

The market continues to evolve, with dynamic market activities unfolding across various sectors. Entities offering security support, integration services, consulting services, field technicians, network support, support forums, cloud support, release management, software support, incident management, customer service, application support, database support, IT support, and more, are integral components of this ever-changing landscape. Service ticket systems and service desk automation streamline processes, enabling service level reporting and effective help desk management.

Change management, field service, and customer satisfaction are key areas of focus, with support engineers leveraging technical documentation and implementation services to ensure seamless integrations. Knowledge base management and problem resolution are critical for maintaining high levels of performance monitoring and security support. Regulatory and compliance changes, supply chain resilience, digital content, cybersecurity concerns, and the implementation of customized business solutions and new applications are essential considerations for businesses in the face of these disruptions.

Remote support, user guides, and training and education empower users, while asset management and incident reporting facilitate effective data center support. Managed services, help desk analysts, community support, and performance monitoring further enhance the market, ensuring continuous improvement and innovation. Root cause analysis, escalation management, and service catalog are essential elements of technical support teams, enabling hardware support and onsite support when necessary. Remote access solutions and release management are vital components of cloud support, enabling organizations to optimize their IT infrastructure and adapt to the ever-changing technological landscape. Software support, incident management, and customer service remain at the forefront of application and database support, ensuring businesses can effectively address their IT needs.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Support Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

225 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11% |

|

Market growth 2025-2029 |

USD 509.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.6 |

|

Key countries |

US, China, Germany, Canada, UK, Japan, India, South Korea, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Support Services Market Research and Growth Report?

- CAGR of the Support Services industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the support services market growth of industry companies

We can help! Our analysts can customize this support services market research report to meet your requirements.

RIA -

RIA -