Smoke Detector Market Size 2025-2029

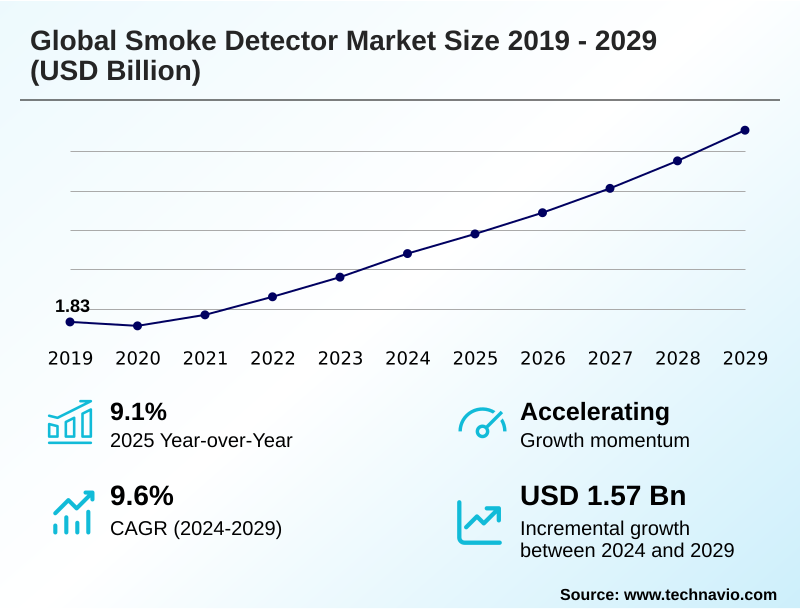

The smoke detector market size is valued to increase by USD 1.57 billion, at a CAGR of 9.6% from 2024 to 2029. Increase in residential construction will drive the smoke detector market.

Major Market Trends & Insights

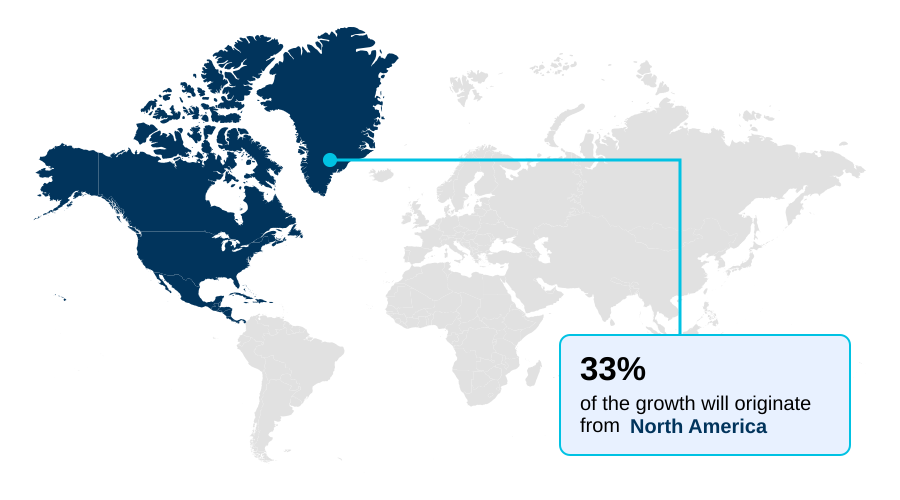

- North America dominated the market and accounted for a 33.1% growth during the forecast period.

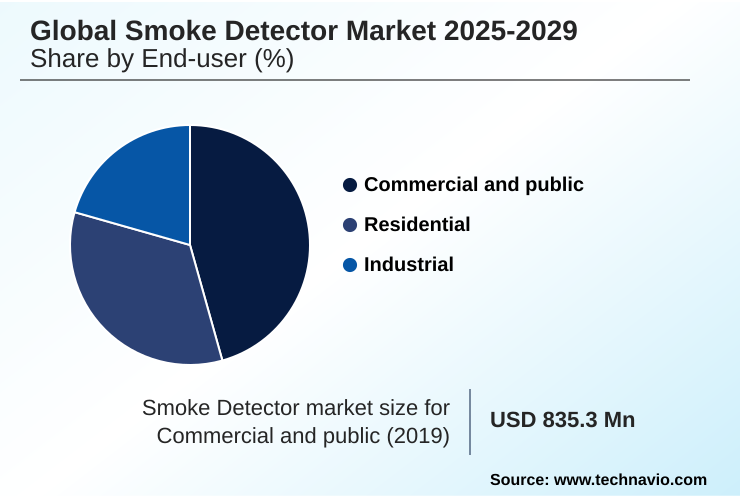

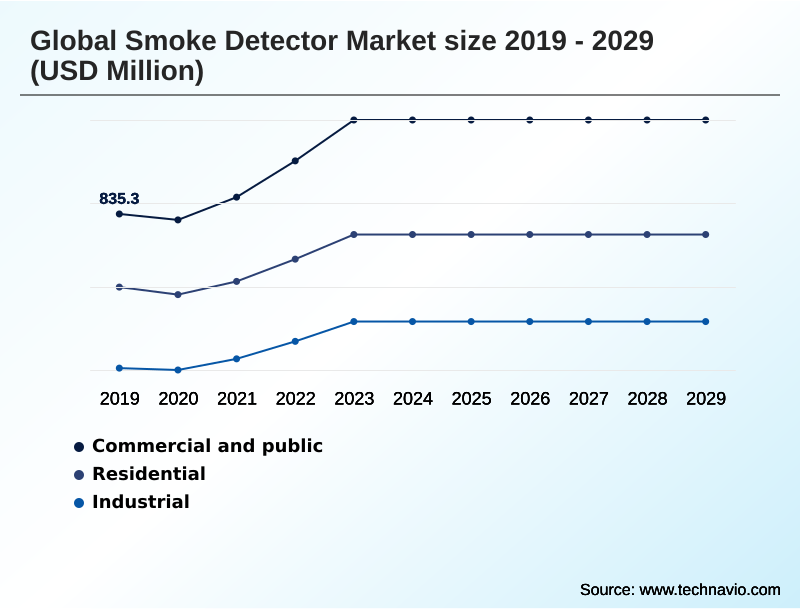

- By End-user - Commercial and public segment was valued at USD 1.11 billion in 2023

- By Type - Photoelectric segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.44 billion

- Market Future Opportunities: USD 1.57 billion

- CAGR from 2024 to 2029 : 9.6%

Market Summary

- The smoke detector market is evolving from providing simple standalone alarms to sophisticated, networked life safety systems. Growth is fundamentally driven by stringent fire safety regulations and building codes that mandate installations, coupled with a robust replacement cycle for aging devices.

- Key trends reshaping the landscape include the integration of iot-enabled smoke alarms with building automation integration and the rising adoption of multi-criteria smoke detectors. These advancements enable superior performance, such as improved smoldering fire detection, while significantly contributing to false alarm reduction. A primary challenge remains the intense price competition, which can stifle investment in innovation.

- For instance, a facility manager overseeing a portfolio of commercial properties can leverage a centralized monitoring system with predictive maintenance alerts. This cloud-based monitoring allows them to manage compliance with the ten-year replacement cycle efficiently, moving from reactive fixes to proactive asset protection strategies and ensuring operational continuity planning across all sites.

- This shift to intelligent, data-driven property protection equipment highlights the market's trajectory towards integrated, high-value solutions.

What will be the Size of the Smoke Detector Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smoke Detector Market Segmented?

The smoke detector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Commercial and public

- Residential

- Industrial

- Type

- Photoelectric

- Dual sensor

- Ionization

- Others

- Connectivity

- Standalone

- Smart

- Wireless

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The commercial and public segment is estimated to witness significant growth during the forecast period.

The commercial and public segment is expanding, driven by strict building code enforcement and the need for asset protection strategies.

The installation of addressable fire alarm systems and centralized monitoring systems is standard in new constructions like offices, malls, and hospitals.

These facilities require building automation integration to comply with NFPA 72 code and workplace safety standards, especially as fire incidents in non-residential structures account for a significant portion of property damage.

These advanced systems, often featuring emergency voice communication and sensor fusion technology, go beyond basic alerts, providing situational awareness systems for effective emergency response enhancement.

This trend is supported by insurance premium reduction incentives for properties with superior life safety systems and active fire protection system capabilities.

The Commercial and public segment was valued at USD 1.11 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smoke Detector Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, accounting for over 33% of market opportunity, driven by strict NFPA standards and high adoption of smart smoke detectors.

Europe follows, contributing nearly 27% of demand as nations mandate wireless interconnected systems for residential fire safety systems.

The APAC region, also representing over 27% of potential growth, is the fastest-growing, fueled by building code enforcement in new commercial fire detection projects. This expansion creates demand for industrial safety solutions featuring dual-sensor technology and aspirating smoke detection.

These regional dynamics influence civil defense integration and asset protection strategies, requiring advanced predictive maintenance alerts for large-scale deployments.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern fire safety landscape requires a detailed understanding of system choices and compliance. A common question is the difference between photoelectric vs ionization smoke detectors; photoelectric models excel at detecting smoldering fires, while ionization units are faster for open flames, making multi-sensor detectors a popular choice.

- The benefits of interconnected smoke alarms are significant, as they create a whole-home alert system, a feature now often included in smoke detector requirements for rentals. For tech-savvy users, a smart smoke detector with mobile alerts offers peace of mind through remote notifications, often as part of a smart home security system integration.

- Proper device placement is crucial, and following NFPA smoke alarm placement guidelines can prevent nuisance alarms, a common issue for a smoke alarm for kitchen use. End-of-life management is also a key concern, and knowing how to handle disposing of old ionization detectors is an important environmental and safety consideration.

- For property owners, replacing hardwired smoke detectors must be done every ten years to maintain effectiveness. In commercial and industrial settings, compliance with commercial building fire alarm codes and industrial fire detection system design is non-negotiable. These environments, especially hotel fire safety compliance standards and hospital fire alarm system requirements, often demand complex addressable systems.

- The initial cost of installing addressable systems is higher, but their precise alert location capabilities can reduce incident response times by over 25% compared to non-addressable systems. Specialized solutions are also available, such as a smoke detector for high ceiling spaces or aspirating smoke detection for data centers, which require specific smoke alarm testing and maintenance protocols.

- The wireless smoke alarm battery life is another factor for both residential and commercial users to consider during procurement.

What are the key market drivers leading to the rise in the adoption of Smoke Detector Industry?

- The expansion of residential construction, driven by global urbanization and government housing initiatives, serves as a primary driver for market growth.

- Stringent fire safety compliance regulations, such as the en 54-7 standard and the nfpa 72 code, are primary market drivers. These mandates necessitate the installation of residential fire safety systems in new constructions and enforce the ten-year replacement cycle.

- The growth in construction, with housing starts increasing by over 12% in some key markets, fuels demand for hardwired smoke alarms and wireless interconnected systems. Public safety awareness campaigns further encourage DIY smoke alarm installation.

- This regulatory push ensures commercial fire detection and industrial safety solutions, including fire and gas detection, meet high standards, supporting operational continuity planning and overall risk mitigation solutions.

What are the market trends shaping the Smoke Detector Industry?

- A key market trend is the increasing integration of smoke detectors with comprehensive building management systems. This convergence enhances operational efficiency and emergency response capabilities.

- The market is shifting towards multi-criteria smoke detectors and smart smoke detectors that leverage iot-enabled smoke alarms for enhanced remote notification capability. These systems utilize advanced sensor technologies and sensor fusion technology to achieve nuisance alarm immunity, reducing false alerts from non-hazardous sources by over 40% compared to traditional models.

- Cloud-based monitoring and smart home integration are becoming standard, offering remote diagnostics and control. This trend is driven by demand for better smoldering fire detection and flaming fire detection capabilities, aligning with modern fire prevention technology and occupant safety solutions to improve overall property protection equipment.

What challenges does the Smoke Detector Industry face during its growth?

- Ambiguities surrounding the proper disposal of smoke detectors, particularly those containing radioactive or toxic materials, present a significant operational and regulatory challenge to the industry.

- Intense price wars erode margins, with basic ionization smoke detectors sold for under ten dollars, pressuring even battery-powered detectors. This environment challenges investment in advanced sensor technologies and complicates fire signature analysis. A significant operational hurdle is disposing of old ionization detectors, which contain hazardous materials and lack clear federal disposal guidelines, complicating regulatory compliance management.

- These legacy systems are also prone to nuisance alarms, undermining false alarm reduction efforts. The performance gap in smoldering fire detection in older models poses a liability, affecting fire hazard assessment and occupant safety solutions, which contrasts with the 98% effectiveness of modern photoelectric smoke detection in such scenarios.

Exclusive Technavio Analysis on Customer Landscape

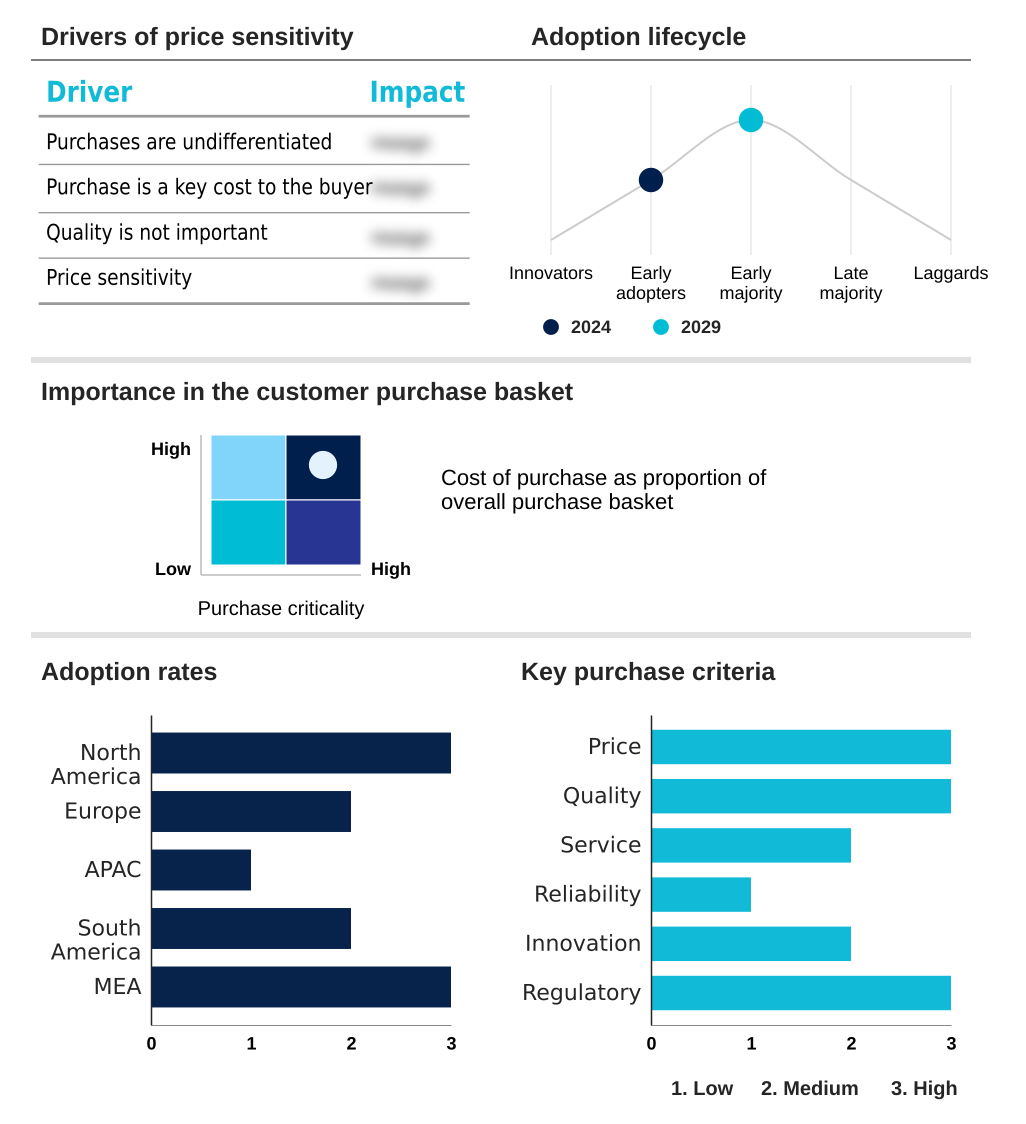

The smoke detector market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smoke detector market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smoke Detector Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smoke detector market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Delivers advanced fire detection and signaling devices, including specialized smoke detection solutions for diverse residential and commercial building applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Apollo Fire Detectors Ltd.

- Carrier Global Corp.

- Ceasefire Industries Pvt. Ltd.

- Gentex Corp.

- Hochiki Corp.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- Johnson Controls International

- Mircom Group of Co.

- Protec Fire and Security Group Ltd.

- Pyrexx GmbH

- Resideo Technologies Inc.

- Robert Bosch GmbH

- Schneider Electric SE

- Secom Co. Ltd.

- Siemens AG

- Universal Security Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smoke detector market

- In September 2024, Schneider Electric SE announced the launch of a new line of Matter-compatible smart smoke and carbon monoxide detectors, enhancing interoperability within smart home ecosystems.

- In November 2024, Johnson Controls International completed the acquisition of a European AI analytics firm, integrating predictive fire-risk algorithms into its building management platforms.

- In January 2025, Resideo Technologies Inc. entered into a strategic partnership with a leading US homebuilder to make its wireless interconnected smoke alarm systems a standard feature in all new residential communities.

- In April 2025, Siemens AG received EN 54 certification for its next-generation aspirating smoke detector, featuring enhanced sensitivity for data center and cleanroom applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smoke Detector Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.6% |

| Market growth 2025-2029 | USD 1572.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 9.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The smoke detector market is undergoing a fundamental transformation from standalone hardware to integrated life safety systems. The adoption of advanced sensor technologies such as photoelectric smoke detection and dual-sensor technology is now standard, driven by the need to detect both smoldering and flaming fires effectively.

- We are seeing a significant push toward wireless interconnected systems and iot-enabled smoke alarms that offer remote notification capability and self-testing diagnostics. These smart smoke detectors are becoming integral components of building automation integration, using protocols like bacnet communication protocol for seamless operation. For boardroom decisions, this means R&D investment must shift towards software, cloud-based monitoring, and sensor fusion technology.

- Companies that fail to adapt beyond hardwired smoke alarms and battery-powered detectors risk obsolescence.

- The integration of video image smoke detection and aspirating smoke detection in high-value commercial and industrial settings, which can reduce incident response times by up to 30%, further underscores the move toward intelligent, multi-layered active fire protection systems that comply with en 54-7 standard and ul 268 7th edition.

- This evolution also includes specialized devices like optical beam smoke detectors and systems featuring emergency voice communication managed by advanced fire alarm control panels. This ecosystem is critical for modern commercial fire detection and industrial safety solutions, with devices using ten-year sealed battery technology or laser-assisted infrared beams setting new benchmarks for high-integrity pressure protection and emergency shutdown systems.

- This also applies to fire and gas detection and centralized monitoring systems under the nfpa 72 code.

What are the Key Data Covered in this Smoke Detector Market Research and Growth Report?

-

What is the expected growth of the Smoke Detector Market between 2025 and 2029?

-

USD 1.57 billion, at a CAGR of 9.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Commercial and public, Residential, Industrial), Type (Photoelectric, Dual sensor, Ionization, Others), Connectivity (Standalone, Smart, Wireless) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increase in residential construction, Disposal of smoke detectors

-

-

Who are the major players in the Smoke Detector Market?

-

ABB Ltd., Apollo Fire Detectors Ltd., Carrier Global Corp., Ceasefire Industries Pvt. Ltd., Gentex Corp., Hochiki Corp., Honeywell International Inc., Huawei Technologies Co. Ltd., Johnson Controls International, Mircom Group of Co., Protec Fire and Security Group Ltd., Pyrexx GmbH, Resideo Technologies Inc., Robert Bosch GmbH, Schneider Electric SE, Secom Co. Ltd., Siemens AG and Universal Security Instruments Inc.

-

Market Research Insights

- The market dynamic is heavily influenced by the push for enhanced safety and connectivity, creating a clear value distinction between product tiers. For instance, the ten-year replacement cycle is now a key driver for upgrading to systems with advanced fire signature analysis, which can improve detection accuracy by over 30% compared to older models.

- This addresses a critical flaw, as outdated alarms show a significant decline in efficiency. Furthermore, while price sensitivity is high, insurance premium reduction of up to 15% for properties with certified life safety systems is encouraging investment in smarter occupant safety solutions.

- This trend supports the shift toward professional installation services for integrated systems, ensuring fire safety compliance and effective operational continuity planning for building managers.

We can help! Our analysts can customize this smoke detector market research report to meet your requirements.

RIA -

RIA -