Middle East and Africa Steel Building Market Size 2026-2030

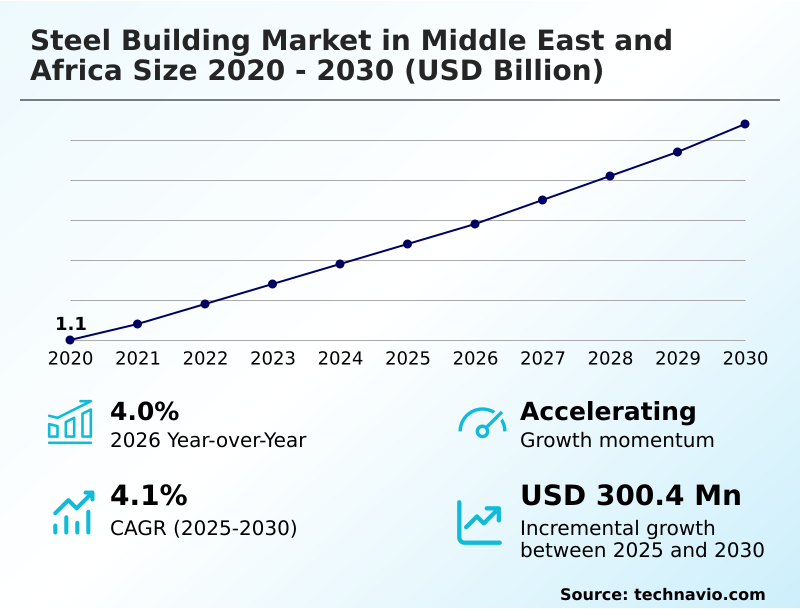

The middle east and africa steel building market size is valued to increase by USD 300.4 million, at a CAGR of 4.1% from 2025 to 2030. Escalation of industrialization and logistics hub expansion in Africa will drive the middle east and africa steel building market.

Major Market Trends & Insights

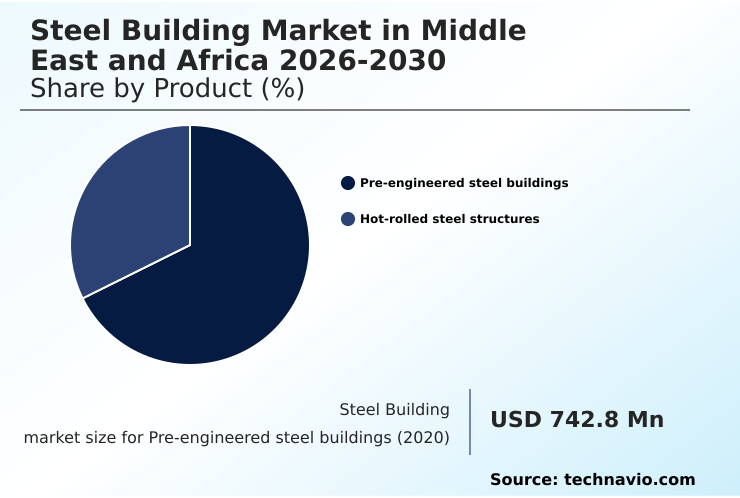

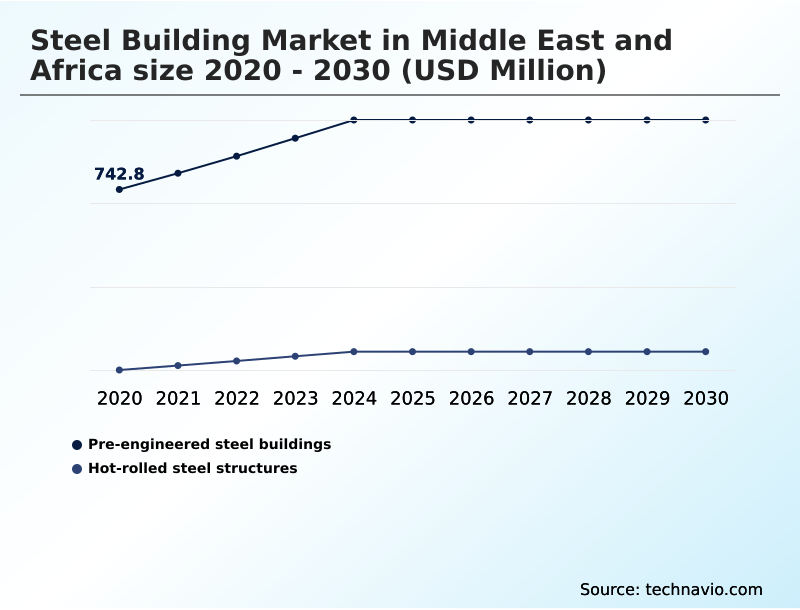

- By Product - Pre-engineered steel buildings segment was valued at USD 892 million in 2024

- By Application - Industrial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 540.3 million

- Market Future Opportunities: USD 300.4 million

- CAGR from 2025 to 2030 : 4.1%

Market Summary

- The steel building market in Middle East and Africa is advancing through the rapid adoption of pre-engineered buildings and sophisticated structural steel frames. This evolution is propelled by national diversification agendas mandating high-speed construction for logistics centers, industrial hubs, and large-scale urban developments.

- Key trends include the integration of high-strength, low-alloy steels to enhance seismic resilience and corrosion resistance, which is critical for ambitious coastal and desert megaprojects. Concurrently, the market is shifting toward sustainable practices, with a growing emphasis on green steel and compliance with carbon emission standards.

- For instance, a contractor for a large-scale desalination plant may leverage modular steel frameworks and building information modeling to accelerate construction timelines, ensuring project delivery adheres to both budgetary constraints and stringent environmental regulations. However, the industry grapples with challenges such as raw material price volatility and shortages of skilled labor capable of managing complex, digital-integrated construction environments.

- Success hinges on a firm's ability to balance structural durability with cost-efficient, modular design, ensuring steel remains an indispensable component of the region's modern economic landscape.

What will be the Size of the Middle East and Africa Steel Building Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Middle East and Africa Steel Building Market Segmented?

The middle east and africa steel building industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Pre-engineered steel buildings

- Hot-rolled steel structures

- Application

- Industrial

- Commercial

- Residential

- End-user

- Construction and infrastructure

- Energy and power

- Transportation and logistics

- Defense and aerospace

- Geography

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Middle East and Africa

By Product Insights

The pre-engineered steel buildings segment is estimated to witness significant growth during the forecast period.

The pre-engineered steel buildings segment is defined by sophisticated and efficient structural design, where components are engineered in a factory setting for rapid on-site assembly.

This methodology, integral to industrial steel buildings and commercial steel structures, uses built-up sections to optimize material usage, reducing on-site labor requirements by up to 35%.

The versatility of these systems makes them the preferred choice for applications requiring large, column-free spaces.

For turnkey construction services, the integration of building information modeling (BIM) with these structural steel systems streamlines the entire process from design to steel building erection.

This approach is increasingly applied to residential steel construction and even modular tent systems, showcasing the adaptability of prefabricated space solutions and industrial fabrication services beyond just hot-rolled steel structures.

The Pre-engineered steel buildings segment was valued at USD 892 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The steel building market in Middle East and Africa is increasingly defined by specialized applications and advanced manufacturing techniques. The use of pre-engineered buildings for logistics hubs is becoming standard, offering speed and scalability that traditional methods cannot match.

- For urban development, hot-rolled structures for high-rise construction remain critical, though now often integrated with seismic resistant design for steel buildings to enhance safety in vulnerable zones. A significant trend is the adoption of green steel for sustainable city projects, a move that aligns with global environmental mandates and often involves low-carbon steel for green building certification.

- In the residential sector, light-gauge framing for residential structures and modular steel frames for affordable housing are addressing housing deficits with efficient, cost-effective solutions. The market is also seeing a rise in comprehensive service offerings, such as turnkey services for industrial steel buildings and erection services for heavy steel structures.

- Technologically, BIM integration in steel building design and automated fabrication for structural steel are optimizing project workflows, demonstrating a reduction in design-related errors by more than 25% compared to conventional methods. Specialization is also evident in material science, with corrosion protection for coastal steel structures and energy-efficient panels in pre-engineered buildings becoming key differentiators.

- Furthermore, demand for high-strength alloys for specialized infrastructure and heavy steel fabrication for energy projects underscores the market's technical depth, moving beyond simple steel framing for commercial building projects to complex, engineered systems.

What are the key market drivers leading to the rise in the adoption of Middle East and Africa Steel Building Industry?

- The escalation of industrialization and the expansion of logistics hubs across Africa are key drivers fueling market growth.

- Market growth is fundamentally driven by large-scale government initiatives and a structural shift toward sustainable industrialization. The rapid development of gigaproject infrastructure and sustainable smart cities is fueling immense demand for green steel structures and low-carbon construction frameworks.

- This has spurred investment in advanced manufacturing, with some regional producers boosting output of eco-certified steel components by nearly 12% to meet demand.

- The expansion of logistics and mining hubs, particularly for heavy industrial use, relies heavily on the speed and efficiency of pre-engineered buildings.

- To support this, there is a growing adoption of electric arc furnace production and direct reduced iron processes, often powered by renewable energy infrastructure.

- This strategic pivot toward low-carbon steel production is essential for constructing the next generation of industrial and commercial facilities.

What are the market trends shaping the Middle East and Africa Steel Building Industry?

- A key market trend is the transition toward high-strength steel alloys and seismic-resistant architectural designs. This shift addresses the increasing demand for structures with enhanced ductility and load-bearing capacity.

- Key trends in the steel building market are centered on advanced engineering and off-site fabrication methods. The industry is witnessing a definitive transition toward high-strength steel alloys and specialized steel alloys to enable complex, high-rise structural engineering and meet stringent seismic-resistant design codes.

- This adoption of advanced framing solutions allows for significant material savings, in some cases up to 15%, without compromising structural integrity. Concurrently, the industrialization of modular and pre-engineered systems, managed through digital-integrated construction platforms, is accelerating project timelines for critical aviation and maritime infrastructure.

- The use of computer numerical control machinery ensures precision in thermomechanically rolled steel components, reducing on-site rework by over 20%. This focus on precision and resilience is critical for advanced structural applications and shaping the future of seismic-resistant architecture.

What challenges does the Middle East and Africa Steel Building Industry face during its growth?

- Heightened geopolitical volatility and critical logistics disruptions pose a key challenge to industry growth.

- The steel building market faces significant operational and economic headwinds, primarily from logistical disruptions and skill shortages. Geopolitical instability has led to severe supply chain interruptions, contributing to a potential loss in output growth of 0.2 percentage points in some economies and project abandonment activity increasing by over 88% year-over-year.

- These issues are compounded by a lack of technical expertise in digital-integrated construction, which is necessary for managing heavy steel fabrication and automated fabrication processes. The resulting delays impact everything from large-scale infrastructure facilities to affordable housing solutions using light-gauge steel framing.

- Furthermore, the high initial cost of insulated panel systems and advanced steel framing systems creates a barrier for smaller contractors, squeezing profit margins and hindering the broader adoption of more efficient turnkey construction solutions.

Exclusive Technavio Analysis on Customer Landscape

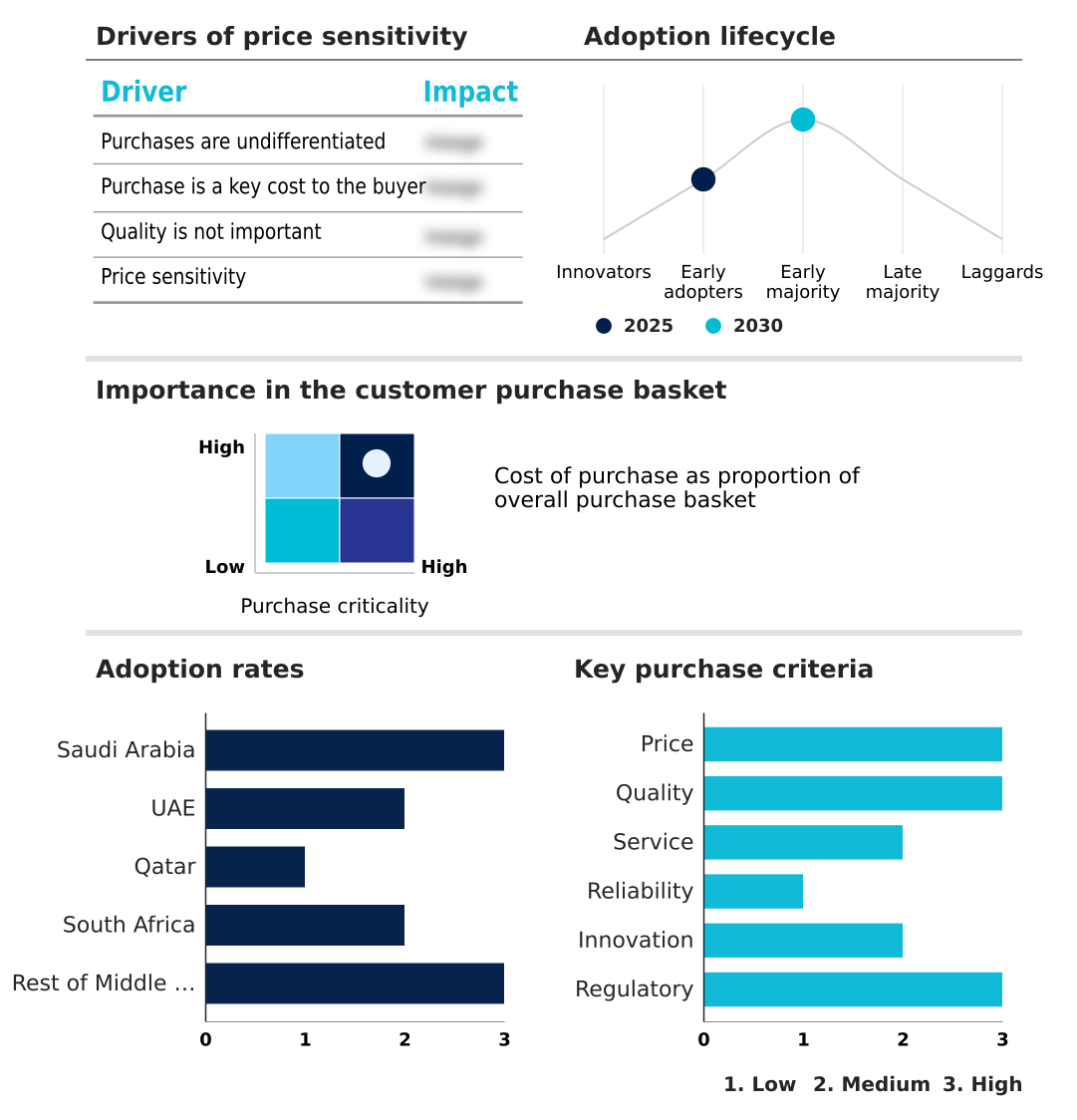

The middle east and africa steel building market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the middle east and africa steel building market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Middle East and Africa Steel Building Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, middle east and africa steel building market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albaddad Capital - Key offerings focus on the design and fabrication of pre-engineered steel buildings, providing scalable and rapidly deployable structural systems for a wide range of construction projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albaddad Capital

- AMANA Building

- Arabian International Company

- Azzazza Steel

- Dorman Long Engineering Ltd

- Falcon Steel Industries LLC

- Gulf Steel Industries

- Hidayath Group Steel Division

- Kirby Building Systems LLC

- Kwikspace Pty Ltd.

- Mabani Steel LLC

- Mammut Building Systems FZC

- PEBCO Pre Engineered Buildings

- Red Sea International Co.

- Roots Steel International LLC

- Safal Group

- SteelFab FZC

- Technical Supplies and Service

- Tiger Steel Engineering LLC

- Zamil Steel Holding Company Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Middle east and africa steel building market

- In January 2025, SIJ Group committed to a landmark investment to construct a new production facility in Ras Al-Khair, aimed at manufacturing specialized steel products like rolled strips and electric steel.

- In March 2025, Zamil Structural Steel initiated a major expansion of its Dammam-based fabrication plant to boost its output capacity for high-strength structural sections needed for large-scale infrastructure projects.

- In March 2025, ArcelorMittal South Africa began a strategic restructuring of its long steel business to better align its production with domestic market demand and improve operational efficiency.

- In April 2025, a leading UAE-based steel producer announced a strategic partnership with a European technology firm to pilot green hydrogen in its direct reduced iron process, aiming to produce low-carbon steel.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Middle East and Africa Steel Building Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 208 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2026-2030 | USD 300.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | Saudi Arabia, UAE, Qatar, South Africa and Rest of Middle East and Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The steel building market is undergoing a significant transformation, driven by the convergence of digital technology and sustainable mandates. Core activities are shifting from conventional construction to the deployment of modular and pre-engineered systems, utilizing technologies like computer numerical control machinery and building information modeling (BIM).

- The adoption of high-strength steel alloys and thermomechanically rolled steel is becoming standard for projects requiring advanced seismic-resistant architecture. A critical boardroom consideration is the transition to green steel structures, with green hydrogen steel production and electric arc furnace production methods gaining traction to meet environmental targets.

- This strategic shift is not without operational hurdles; approximately 56% of firms report struggles with skill shortages, particularly for complex steel building erection and automated fabrication processes.

- The market now demands a holistic approach, integrating turnkey construction services with specialized solutions like corrosion-resistant coatings, high-performance insulation panels, and advanced framing solutions to deliver resilient and efficient hot-rolled steel structures and pre-engineered steel buildings.

What are the Key Data Covered in this Middle East and Africa Steel Building Market Research and Growth Report?

-

What is the expected growth of the Middle East and Africa Steel Building Market between 2026 and 2030?

-

USD 300.4 million, at a CAGR of 4.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Pre-engineered steel buildings, and Hot-rolled steel structures), Application (Industrial, Commercial, and Residential), End-user (Construction and infrastructure, Energy and power, Transportation and logistics, and Defense and aerospace) and Geography (Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalation of industrialization and logistics hub expansion in Africa, Heightened geopolitical volatility and critical logistics disruptions

-

-

Who are the major players in the Middle East and Africa Steel Building Market?

-

Albaddad Capital, AMANA Building, Arabian International Company, Azzazza Steel, Dorman Long Engineering Ltd, Falcon Steel Industries LLC, Gulf Steel Industries, Hidayath Group Steel Division, Kirby Building Systems LLC, Kwikspace Pty Ltd., Mabani Steel LLC, Mammut Building Systems FZC, PEBCO Pre Engineered Buildings, Red Sea International Co., Roots Steel International LLC, Safal Group, SteelFab FZC, Technical Supplies and Service, Tiger Steel Engineering LLC and Zamil Steel Holding Company Ltd

-

Market Research Insights

- The steel building market is navigating a complex landscape shaped by rapid urbanization projects and a strong push for a circular construction economy. Firms are leveraging turnkey modular solutions and advanced structural applications to meet aggressive timelines for gigaproject infrastructure. This has led to efficiency gains, with some off-site fabrication methods reducing project material waste by over 15%.

- A notable dynamic is the pivot to low-carbon steel production for sustainable smart cities, where developers using eco-certified steel components report a 10% improvement in eligibility for green financing. The demand for heavy industrial use in new logistics and mining hubs is also a significant factor.

- However, these advancements are tempered by execution challenges; project abandonment rates have seen a significant year-over-year increase, primarily due to budgetary overruns and procurement delays, underscoring the gap between ambitious visions and on-the-ground project management capabilities.

We can help! Our analysts can customize this middle east and africa steel building market research report to meet your requirements.

RIA -

RIA -