Stool Testing Market Size 2024-2028

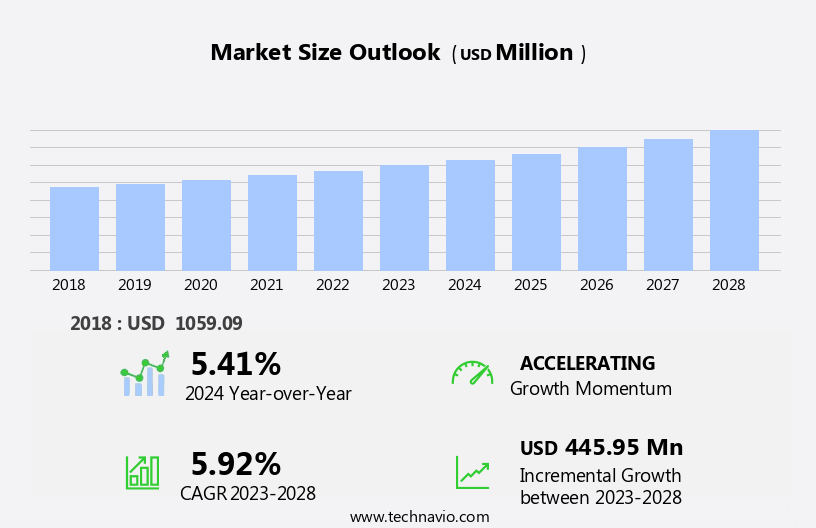

The stool testing market size is forecast to increase by USD 445.95 million at a CAGR of 5.92% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing prevalence of gastrointestinal (GI) diseases and colorectal cancer worldwide. According to various studies, GI disorders affect millions of people globally, with colorectal cancer being one of the leading causes of cancer-related deaths. This situation has created a high demand for accurate and early diagnosis methods, making stool testing an essential tool in healthcare. Moreover, favorable initiatives from governments and private organizations to increase awareness and accessibility of diagnostic tests, particularly in emerging markets, are expected to boost market growth. However, high treatment costs associated with GI disorders and colorectal cancer pose a significant challenge to market expansion.

- To capitalize on the market opportunities and navigate these challenges effectively, companies should focus on developing cost-effective testing solutions while ensuring accuracy and reliability. Additionally, partnerships with healthcare providers and insurers can help increase market penetration and patient access to these tests. Overall, the market presents a high growth potential, particularly in emerging markets, and offers significant opportunities for companies to make a positive impact on public health.

What will be the Size of the Stool Testing Market during the forecast period?

- The market encompasses a range of technologies and applications, primarily focused on the analysis of biological samples for diagnostic purposes. Key market dynamics include advances in device performance, such as barrier height engineering and the development of MISFETs, reflective contacts, and ohmic contacts. These innovations contribute to improved specific contact resistivity and Schottky contact performance, enhancing the overall efficiency and accuracy of stool testing devices. High-power electronics, including HEMTs and AlGa/GaN heterostructures, are driving growth in the market due to their increased use in advanced analytical instruments. Ternary alloys, epitaxial growth techniques, and III-nitrides are also gaining traction, as they enable the fabrication of nanostructures and metal-semiconductor contacts with enhanced thermal stability and lattice thermal conductivity.

- First-principles modeling, quantum confinement, and thermal transport studies are essential in the fundamental properties of stool testing devices, including phonon distributions and thermal properties of n-type and p-type GaN. Transparent contacts and quantum perturbation theory are further advancing the field, offering potential solutions for enhancing device performance and expanding the scope of applications in the market.

How is this Stool Testing Industry segmented?

The stool testing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- GI

- Fecal occult

- End-user

- Hospitals

- Diagnostic centres and laboratories

- Clinics and others

- Geography

- North America

- US

- Canada

- Europe

- UK

- Asia

- Rest of World (ROW)

- North America

By Type Insights

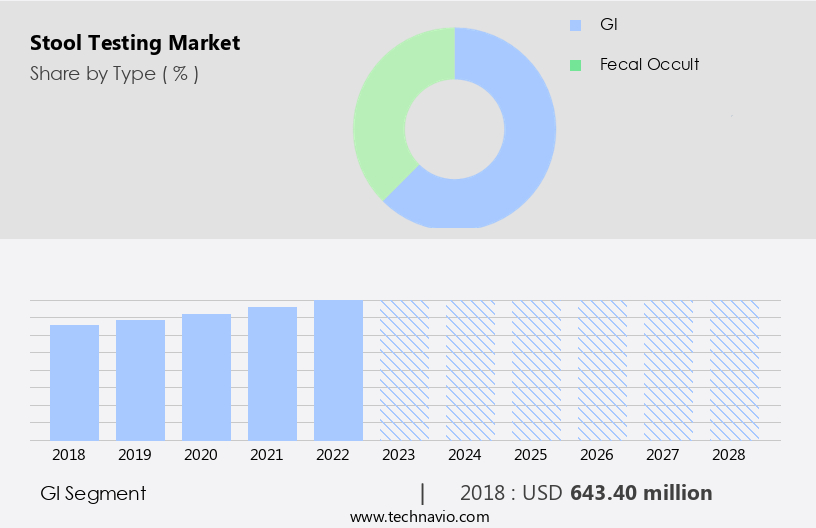

The GI segment is estimated to witness significant growth during the forecast period. Stool testing is a diagnostic method used to identify gastrointestinal (GI) disorders by examining the stool for various indicators. This test is essential for detecting pathogens, such as bacteria, viruses, and microorganisms, that can cause GI distress and systemic symptoms. The analysis of stool samples provides insights into digestion efficiency, gut bacterial types, dysbiosis, parasites or worms, and immune system strength. GI disorders that may necessitate stool testing include hemorrhoids, peptic ulcers, esophageal inflammation, diverticulosis and diverticulitis, ulcerative colitis and Crohn's disease, colonic polyps, and potential colon, stomach, or esophageal cancers. Advancements in technology have led to improvements in stool testing, with the integration of Carbon footprint-conscious practices, Radio Frequency (RF) technology, and Power amplifiers in Low-voltage applications.

Schottky Contacts and Metal-Semiconductor Contacts enhance the efficiency of Fast chargers and Light-emitting diodes (LEDs), while Cadence and Ohmic Contacts ensure Electronic designs' stability. High-temperature operation and Terahertz (THz) devices are crucial for enhancing the diagnostic capabilities of stool testing, with First-Principles Modeling and Electrothermal Modeling playing a significant role in the Thermal Properties and Thermal Stability of nanostructures like Ternary Alloys and Quantum Confinement materials. Stool testing applications extend beyond healthcare, with Automotive, Aerospace, data centers, and Industry sectors benefiting from the technology's efficiency and sustainability. Transparent Contacts, P-Type GaN, and Quantum Perturbation Theory are essential for enhancing the performance of Light-Emitting Diodes, High-Power Electronics, and Laser diodes.

Stool testing's environmental friendliness and energy savings make it an attractive solution for various sectors, with a focus on reducing Carbon emissions and improving Energy efficiency. The technology's miniaturization and integration into various applications, such as Sensor Applications and Power supplies, further increase its importance.

Get a glance at the market report of share of various segments Request Free Sample

The GI segment was valued at USD 643.40 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

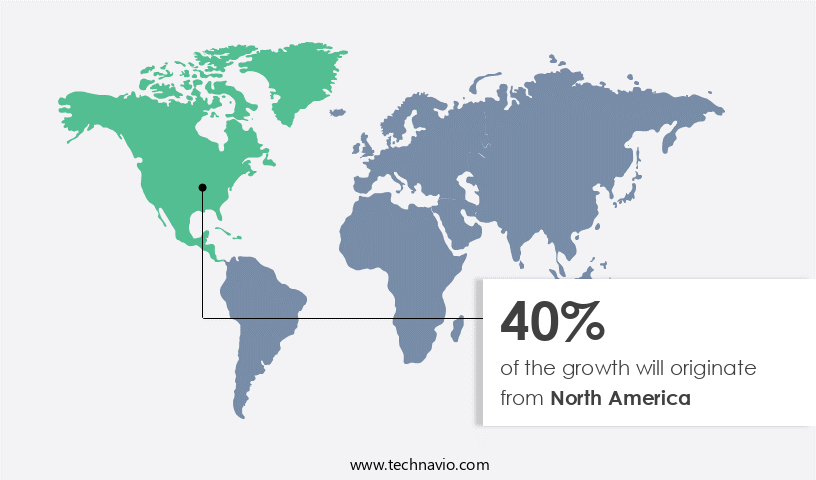

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in North America is experiencing steady growth, driven by the increasing adoption of advanced technologies for the diagnosis and treatment of GI bleeding. This trend is fueled by a high demand for technology, rising prevalence of GI diseases such as stomach, colon, and pancreatic cancer, an aging population, and favorable reimbursement policies for endoscopic procedures. The market expansion is further by the growing presence of major players in the region, committed to developing innovative endoscopic devices. The need for GI bleeding treatment is escalating due to the increasing incidence of chronic diseases, necessitating efficient and effective diagnostic tools.

In the realm of technology, advancements in power amplifiers, Schottky Contacts, and Ohmic Contacts are crucial for enhancing the performance of stool testing devices. These components play a significant role in reducing carbon footprint, improving efficiency, and ensuring thermal stability in high-power electronics. Moreover, the development of Terahertz (THz) devices, Quantum devices, and Light-Emitting Diodes (LEDs) is paving the way for faster charging, higher data transfer rates, and improved energy efficiency in various applications, including data centers, automotive, aerospace, and consumer electronics. First-Principles Modeling and Electrothermal Modeling are essential in designing and optimizing the thermal properties of nanostructures, ternary alloys, and III-Nitrides, ensuring thermal transport, thermal stability, and breakdown field reliability for high-voltage applications.

The market in North America is poised for growth, driven by the increasing need for advanced diagnostic tools, technological advancements, and the commitment of major players to innovation. The focus on sustainability, energy efficiency, and thermal properties will continue to shape the market landscape.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Stool Testing Industry?

- Favorable initiatives and the increasing prevalence of gastrointestinal diseases is the key driver of the market. The market is experiencing significant growth due to the rising incidence of gastrointestinal (GI) diseases. Esophageal and pancreatic cancers, biliary diseases, and Barrett syndrome are among the conditions contributing to market expansion. Additionally, the prevalence of esophageal, colorectal, gastric cancers, and colon polyps is increasing, further fueling market growth. Increased awareness among physicians and patients regarding GI bleeding is another key factor driving market expansion.

- The increasing burden of chronic GI disorders, such as stomach cancers, has led to rising healthcare costs worldwide. This trend is expected to continue, making stool testing a crucial diagnostic tool in the healthcare industry.

What are the market trends shaping the Stool Testing Industry?

- High growth potential in emerging markets is the upcoming market trend. The market is experiencing significant growth due to the increasing focus of market companies on emerging economies. These economies offer substantial opportunities for expansion, as they provide access to capital, first-mover advantage, better economic growth, government initiatives, and improved healthcare infrastructure. For instance, in Japan, the government is promoting the adoption of advanced medical devices and procedures in emerging economies by collaborating with companies to spread awareness of their benefits. This strategic approach is enabling companies to expand their reach and generate higher revenue.

- Additionally, the increasing prevalence of gastrointestinal disorders and the growing awareness of early disease detection are further driving the growth of the market. Market companies are investing in research and development to introduce innovative testing methods and technologies, which is expected to boost market growth in the coming years.

What challenges does the Stool Testing Industry face during its growth?

- High treatment costs associated with GI disorders and colorectal cancer is a key challenge affecting the industry growth. The market is experiencing continuous expansion, driven by the increasing prevalence of gastrointestinal (GI) disorders and the growing awareness of early disease detection. However, high costs associated with diagnostic tools, such as stool testing kits and treatment for GI bleeding, pose a significant challenge, particularly in price-sensitive markets. Small hospitals and private clinics in both developed and developing economies may forego endoscopic kits due to budget constraints.

- These devices are expensive and classified as capital items, necessitating extensive procurement procedures and budget allocation considerations. Equipment maintenance further adds to the financial burden for end-users. Despite these challenges, the market's growth is expected to continue, fueled by advancements in technology and growing demand for non-invasive diagnostic methods.

Exclusive Customer Landscape

The stool testing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the stool testing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, stool testing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdvaCare Pharma - The company introduces a cutting-edge stool testing device engineered for efficient sample preparation, enabling nucleic acid extraction of viruses, bacteria, and parasites. This innovative tool enhances laboratory workflows and boosts diagnostic accuracy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdvaCare Pharma

- bioMerieux SA

- Cardinal Health Inc.

- Cenogenics Corp.

- Danaher Corp.

- DiaSorin SpA

- Eiken Chemical Co. Ltd.

- Epitope Diagnostics Inc.

- Exact Sciences Corp.

- Genova Diagnostics Inc.

- Helena Laboratories Corp.

- Hologic Inc.

- McKesson Corp.

- Meridian Bioscience Inc.

- Pinnacle BioLabs

- Polymedco CDP LLC

- Quest Diagnostics Inc.

- Quidelortho Corp.

- CTK Biotech Inc.

- ScheBo Biotech AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses various technologies and applications that focus on improving the efficiency and performance of electronic devices. One significant area of research is the development of power amplifiers for low-voltage applications. These amplifiers are essential in numerous industries, including telecommunications and consumer electronics, where energy efficiency and miniaturization are key priorities. Schottky contacts, a type of contact used in power electronics, have gained attention due to their ability to reduce thermal resistance and enhance device performance. These contacts operate at high frequencies, such as radio frequency (RF), and are crucial in applications requiring fast charging and high-power operation.

In the realm of high-temperature applications, ternary alloys and nanostructures have emerged as potential solutions for thermal properties improvement. These materials exhibit unique electrical and thermal characteristics, enabling the design of quantum confinement structures and quantum devices. First-principles modeling and electrothermal modeling are essential tools in the development of these advanced materials. The quest for energy efficiency and sustainability has led to the exploration of carbon footprint reduction in various industries, including data centers and automotive applications. High-power electronics, such as power supplies and high-voltage applications, are significant contributors to carbon emissions. To address this challenge, researchers are focusing on power conversion technologies, thermal transport, and thermal stability.

Transparent contacts and reflective contacts are gaining popularity in optoelectronics due to their potential to increase the efficiency of light-emitting diodes (LEDs) and laser diodes. These contacts enable the integration of electronic and optical components, leading to miniaturization and improved device performance. The aerospace industry is another sector that benefits from advancements in high-power electronics. The development of high-efficiency power supplies and energy savings technologies is crucial for reducing the weight and improving the performance of aerospace systems. Sustainability is a critical factor in the design of electronic devices, especially in the context of consumer electronics.

Energy efficiency, thermal properties, and thermal stability are essential considerations in the development of these devices. Silicon-based materials continue to be the foundation of electronic designs due to their versatility and cost-effectiveness. High-electron-mobility transistors (HEMTs) and metal-semiconductor field-effect transistors (MISFETs) are essential components in high-power electronics. The optimization of these devices' thermal transient testing and breakdown field properties is crucial for their successful implementation in various applications. The market is a dynamic and diverse field that encompasses various technologies and applications. The focus on energy efficiency, sustainability, and miniaturization is driving the development of advanced materials, power amplifiers, and electronic designs.

The pursuit of high-performance, low-power devices is a common thread in numerous industries, from telecommunications and consumer electronics to aerospace and automotive applications. The ongoing research in this area is expected to yield significant advancements in the near future.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.92% |

|

Market growth 2024-2028 |

USD 445.95 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.41 |

|

Key countries |

US, Canada, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Stool Testing Market Research and Growth Report?

- CAGR of the Stool Testing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the stool testing market growth of industry companies

We can help! Our analysts can customize this stool testing market research report to meet your requirements.

RIA -

RIA -