Sulfur Recovery Technology Market Size 2024-2028

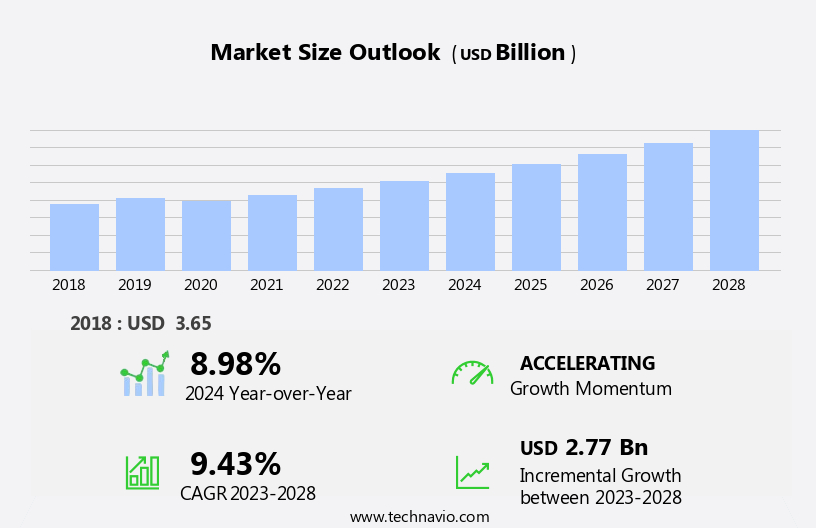

The sulfur recovery technology market size is forecast to increase by USD 2.77 billion, at a CAGR of 9.43% between 2023 and 2028.

- The market is driven by stringent emissions regulations aimed at reducing sulfur dioxide emissions. This trend is expected to persist as governments worldwide prioritize environmental sustainability. Another key driver is the increasing number of sulfur recovery contracts, indicating a growing demand for sulfur and sulfuric acid. However, the high initial costs associated with setting up sulfur recovery units pose a significant challenge for market growth.

- These costs can deter potential entrants and limit the expansion of existing players. Companies seeking to capitalize on market opportunities must carefully weigh the benefits of entering against the substantial investment required. Effective strategic planning and cost management will be essential for navigating this challenge and thriving in the market.

What will be the Size of the Sulfur Recovery Technology Market during the forecast period?

The sulfur recovery market is characterized by its continuous evolution, driven by the ever-changing dynamics of various industries and the ongoing quest for optimal sulfur recovery solutions. Sulfur recovery operations are integral to numerous sectors, including oil and gas production, power generation, and chemical manufacturing. The Claus process, a widely used sulfur recovery technology, continues to undergo development and optimization. Tail gas treatment, a crucial aspect of Claus plant operation, is a focus area for enhancing sulfur recovery efficiency and reducing emissions. Hydrogen sulfide, a key component in the Claus process, presents ongoing challenges in terms of safe handling and efficient utilization.

Sulfur recovery optimization is a priority for companies seeking to minimize costs, improve sustainability, and adhere to increasingly stringent regulations. Innovations in sulfur recovery technologies, such as automation and simulation, are driving advancements in sulfur recovery system design and operation. Sulfur recovery lifecycle considerations, including maintenance and investment, are essential elements in the overall sustainability and profitability of sulfur recovery units. The future of the sulfur recovery industry lies in continued research and development, with a focus on enhancing efficiency, reducing emissions, and ensuring safety and compliance with evolving regulations.

How is this Sulfur Recovery Technology Industry segmented?

The sulfur recovery technology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Claus process

- Tail gas treatment

- Others

- Application

- Oil Refineries

- Gas Processing Plants

- Chemical Plants

- Power Plants

- End-User

- Oil & Gas Industry

- Chemical Industry

- Power Generation

- Process

- Sulfur Recovery Units (SRU)

- Sulfur Removal

- Gas Sweetening

- Geography

- North America

- US

- Canada

- South America

- Argentina

- Brazil

- Middle East and Africa

- UAE

- Europe

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Technology Insights

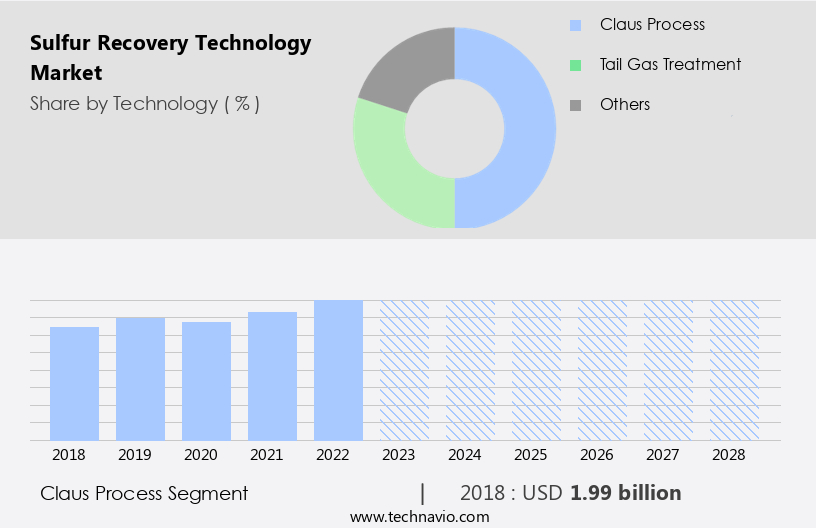

The claus process segment is estimated to witness significant growth during the forecast period.

The Claus process is a crucial sulfur recovery technology that effectively converts hydrogen sulfide (H2S) gas streams into elemental sulfur. Widely adopted in refineries, natural gas processing plants, and other H2S handling facilities, this process plays a significant role in reducing sulfur emissions, ensuring environmental compliance, and generating valuable elemental sulfur. The Claus reactor, a key component of this process, utilizes a catalyst, typically alumina-based, to facilitate the conversion of H2S into elemental sulfur. The catalyst, which consists of aluminum oxide combined with other substances like titanium oxide, enhances performance and process economics. Sulfur recovery challenges, such as varying H2S concentrations and process conditions, necessitate continuous optimization and monitoring.

Sulfur recovery efficiency, a critical metric, is influenced by factors like catalyst selection, operating conditions, and tail gas treatment. Sulfur recovery development is ongoing, with research focusing on improving efficiency, reducing costs, and enhancing sustainability. The sulfur recovery industry employs various technologies, including amine treating and Claus plant optimization, to optimize performance and minimize emissions. Sulfur recovery modeling and simulation are essential tools for understanding the process dynamics and optimizing operations. Sulfur recovery safety is paramount, with regulations and standards in place to ensure safe and efficient operations. The sulfur recovery lifecycle encompasses design, operation, maintenance, and investment, with each stage requiring careful consideration to maximize efficiency and minimize costs.

Sulfur recovery capacity is a key consideration for operators, with the ability to process large volumes of H2S gas a significant advantage. The future of sulfur recovery lies in automation, innovation, and sustainability, with a focus on reducing emissions, improving efficiency, and minimizing costs.

The Claus process segment was valued at USD 1.99 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

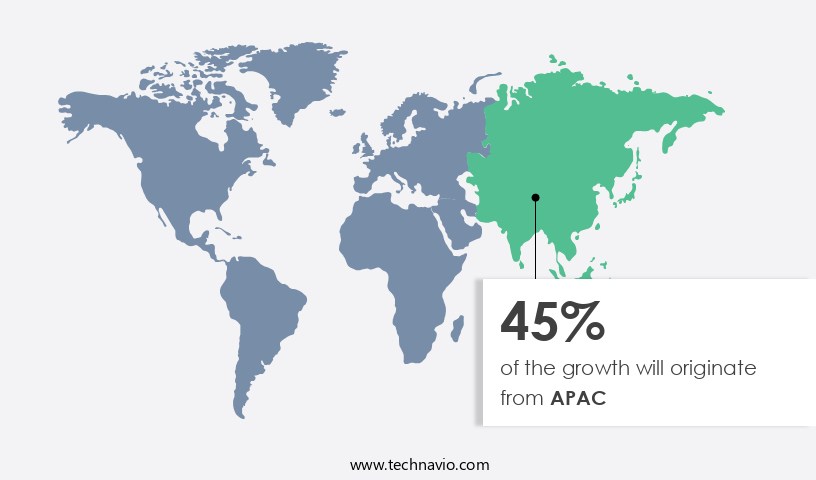

APAC is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing notable growth, with China and India leading the charge. The region's economic expansion and population growth have resulted in increased energy demands, making oil refineries and natural gas processing plants essential components of the industrial landscape. Sulfur recovery processes are crucial in these industries to comply with environmental regulations and promote sustainability. The Claus process, a widely used sulfur recovery technology, is undergoing optimization to enhance efficiency and reduce emissions. Tail gas treatment, a critical aspect of sulfur recovery, is being advanced through simulation and modeling to improve the overall sulfur recovery lifecycle.

Hydrogen sulfide, a byproduct of sour gas, is being addressed through amine treating and other sulfur recovery solutions. Sulfur recovery challenges, such as safety concerns and high costs, are being addressed through automation, innovation, and maintenance strategies. The sulfur recovery industry is continuously evolving, with a focus on sustainability, efficiency, and compliance with regulations and standards. Sulfur recovery capacity is expanding, driven by investments in new technologies and upgrades to existing units. The future of sulfur recovery lies in advanced technologies and optimized processes that minimize emissions and maximize efficiency.

Market Dynamics

The Sulfur Recovery Technology market is crucial for environmental protection and resource management, with the Claus Process and Tail Gas Treatment being central to operations. These technologies are primarily implemented in Sulfur Recovery Units (SRU), often alongside Acid Gas Removal (AGR) systems in critical sectors. Oil & Gas Refineries and Natural Gas Processing plants are major end-users, driving demand for efficient hydrogen sulfide removal and overall emissions reduction sulfur. The market relies heavily on specialized sulfur recovery catalysts and is constantly evolving to meet stringent environmental compliance sulfur regulations. Innovations like modular sulfur recovery plants and liquid redox sulfur recovery are gaining traction, while advanced process control SRU systems optimize operations. The ultimate goal is effective sulfur dioxide abatement across various industries, including petrochemical plants sulfur, with solutions for sour gas treatment and overall sulfur plant optimization, also leveraging waste heat boilers SRU for energy efficiency in industrial sulfur recovery.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Sulfur Recovery Technology Industry?

- The stringent emissions standards, which focus on reducing sulfur dioxide emissions, serve as the primary market driver.

- Sulfur recovery technologies play a vital role in the refining and processing of crude oil and natural gas to meet stringent emission regulations. The removal of sulfur compounds, specifically hydrogen sulfide (H2S) and sulfur dioxide (SO2), is essential for reducing air pollution during fuel combustion. In the US and globally, regulations, such as the Federal Clean Air Act and the Environmental Protection Agency's standards, mandate sulfur reduction in various fuel products, including marine fuel and ultra-low-sulfur diesel. The European Union (EU) also enforces regulations under the Industrial Emissions Directive (IED), setting emission limit values for sulfur dioxide from various industrial installations.

- Sulfur recovery innovations, such as automation and claus plant optimization, have significantly improved the efficiency and sustainability of sulfur recovery units. Sulfur recovery modeling has enabled better understanding and prediction of sulfur recovery processes, leading to reduced maintenance costs and improved operational performance. Sulfur recovery equipment manufacturers continue to invest in research and development to create more efficient and cost-effective technologies. Sustainability remains a key focus, with an emphasis on reducing energy consumption and minimizing waste. These advancements contribute to the overall growth and evolution of the sulfur recovery market.

What are the market trends shaping the Sulfur Recovery Technology Industry?

- The trend in the sulfur recovery market is marked by an increasing number of contracts being signed. This growth is a reflection of the industry's continuing demand for effective sulfur recovery solutions.

- Sulfur recovery systems have gained significant importance due to stringent environmental regulations mandating the reduction of sulfur dioxide emissions. These regulations have driven the demand for efficient sulfur recovery solutions across various industries. Technip Energies N.V., a leading engineering company, recently announced a contract to enhance sulfur recovery facilities at Aramco Riyadh Refinery. Under this agreement, Technip Energies N.V. Will install three new tail gas treatment (TGT) units to optimize the performance of existing sulfur recovery units (SRUs). This development underscores the growing market for sulfur recovery processes and technologies. The focus on increasing sulfur recovery rates and adhering to sulfur recovery standards is a key trend in the industry.

- Companies are investing in advanced sulfur recovery processes and designs to meet these requirements and capitalize on the demand for sulfur recovery applications. This contract marks a significant milestone in the partnership between Technip Energies N.V. And Aramco, highlighting the importance of sulfur recovery systems in today's industrial landscape.

What challenges does the Sulfur Recovery Technology Industry face during its growth?

- The high initial costs incurred during the setup of sulfur recovery units pose a significant challenge to the industry's growth trajectory. This financial hurdle, which is an inherent aspect of the sulfur recovery process, can significantly impact the profitability and competitiveness of companies operating in this sector.

- Sulfur recovery operations entail significant upfront investments in equipment, engineering, and installation, making it a capital-intensive process. The cost of installing a sulfur recovery unit in a refinery can vary greatly, ranging from several million to tens of millions of dollars, contingent upon the scale and complexity of the facility. For instance, a new 100-ton-per-day sulfur recovery unit, achieving a 98.5% sulfur recovery rate, may cost anywhere from USD25 million to USD30 million.

- The substantial initial costs are primarily due to the advanced technology and equipment required for efficient sulfur recovery, such as amine treating units, Claus units, and tail gas treatment units.

Exclusive Customer Landscape

The sulfur recovery technology market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sulfur recovery technology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, sulfur recovery technology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide S.A. - The company specializes in advanced sulfur recovery technology, specifically the OxyClaus system. This innovative solution enhances the capacity of existing Sulfur Recovery Units (SRUs) by up to 100%, featuring two distinct combustion zones for thorough impurity elimination. Impurities such as RSH, NH3, and hydrocarbons are effectively combusted, ensuring optimal efficiency and minimal emissions. By implementing this technology, clients can significantly improve their sulfur recovery processes while maintaining a cost-effective operation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide S.A.

- Amec Foster Wheeler

- Axens

- Bechtel Corporation

- Black & Veatch

- CB&I (McDermott)

- Chiyoda Corporation

- ExxonMobil Corporation

- Fluor Corporation

- Haldor Topsoe A/S

- Jacobs Engineering Group Inc.

- John Wood Group Plc

- KBR Inc.

- Linde AG

- Mitsui Chemicals Inc.

- Petrofac Limited

- Saipem S.p.A.

- Shell Global Solutions

- TechnipFMC

- WorleyParsons Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Sulfur Recovery Technology Market

- In February 2023, Claus Technology, a leading sulfur recovery technology provider, announced the launch of its innovative ClausCAT Catalyst, which significantly enhances the efficiency of the Claus Process by up to 10% (Claus Technology press release). This development is expected to reduce sulfur emissions and improve overall profitability for hydrogen sulfide (H2S) processing industries.

- In August 2022, ThyssenKrupp Industrial Solutions and Linde plc entered into a strategic partnership to combine their sulfur recovery technologies, creating a global market leader in this sector (ThyssenKrupp Industrial Solutions press release). This collaboration aims to offer customers a comprehensive range of sulfur recovery solutions, including the Claus Process and the Linde Sulfur Recovery Process.

- In January 2021, CB&I, a global engineering, procurement, and construction company, was acquired by McDermott International, forming a new entity called McDermott CB&I (McDermott International press release). This merger brought together CB&I's extensive sulfur recovery technology portfolio with McDermott's expertise in engineering, construction, and project management.

- In April 2019, the European Union (EU) implemented the Industrial Emissions Directive (IED), which set stricter emission limits for sulfur dioxide (SO2) and nitrogen oxides (NOx) in the European cement industry (European Commission press release). This regulatory initiative accelerated the adoption of advanced sulfur recovery technologies, such as the Claus Process, to meet the new emission standards.

Research Analyst Overview

- The sulfur recovery market encompasses various technologies for converting sulfur-containing compounds in industrial processes into marketable sulfur products. Key technologies include acid gas treating, sulfur recovery incinerators, and sulfur recovery absorbers. Thermal oxidation processes, such as sulfur recovery stack and sulfur recovery vent, are employed to convert sulfur dioxide into sulfur trioxide, which is then converted into sulfuric acid. Sulfur recovery catalysts, including selective oxidation and catalytic oxidation, play a crucial role in enhancing the efficiency of these processes. Sulfur recovery waste, a byproduct of these processes, can be further refined into elemental sulfur or sulfuric acid.

- Market trends include the integration of advanced technologies, such as membrane technology and regenerative thermal oxidation, to improve efficiency and reduce emissions. Sulfur recovery byproduct streams are increasingly being utilized as feedstocks for the production of high-value chemicals and fuels, further driving market growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sulfur Recovery Technology Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

189 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.43% |

|

Market growth 2024-2028 |

USD 2.77 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.98 |

|

Key countries |

US, Canada, China, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Sulfur Recovery Technology Market Research and Growth Report?

- CAGR of the Sulfur Recovery Technology industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the sulfur recovery technology market growth of industry companies

We can help! Our analysts can customize this sulfur recovery technology market research report to meet your requirements.

RIA -

RIA -