Thermocouple Temperature Sensors Market Size 2024-2028

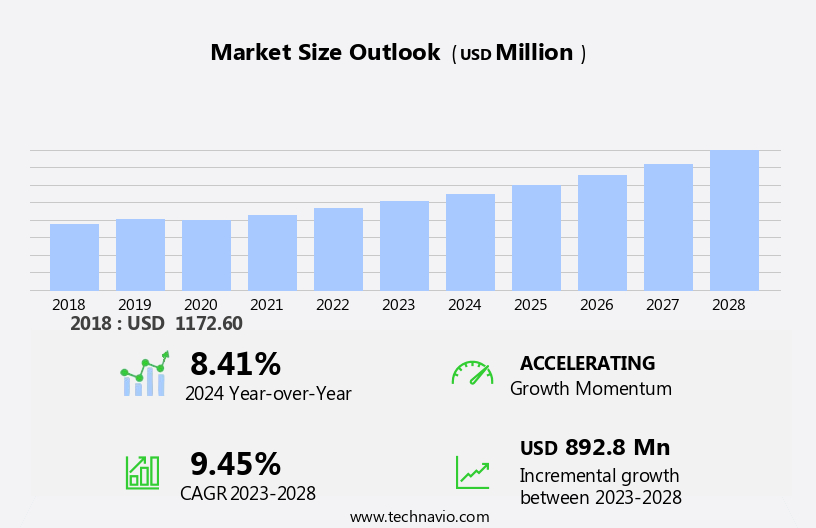

The thermocouple temperature sensors market size is forecast to increase by USD 892.8 million at a CAGR of 9.45% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing demand for sensors in various industries. In sectors like electric vehicles, the expansion of EV charging infrastructure and the rise of autonomous vehicles are driving the market's growth. Thermocouple temperature sensors play a crucial role In thermal management systems for EV batteries and HVAC systems in EVs. Additionally, the semiconductor industry's growth, fueled by the production of batteries for EVs and renewable energy, is also contributing to the market's expansion. Moreover, the demand for thermocouple temperature sensors is increasing In the oil and gas industry for crude oil and natural gas production processes.

- In medical devices, these sensors are used for temperature monitoring in various applications. The aviation industry also utilizes thermocouple temperature sensors for engine and fuel system temperature monitoring. However, the high cost of thermocouple temperature sensors remains a significant challenge for the market's growth. To address this challenge, the market is witnessing the increasing demand for wireless temperature sensing solutions, which can reduce installation and maintenance costs. Furthermore, the adoption of Industry 4.0 and automation in various industries is also expected to increase the demand for thermocouple temperature sensors. Additionally, the construction industry is utilizing thermocouple temperature sensors for boiler temperature monitoring, and the filters industry is using them for temperature monitoring in filtration processes.

What will be the Size of the Thermocouple Temperature Sensors Market During the Forecast Period?

- The market encompasses the production and sales of sensors that convert temperature differences into electrical signals. These sensors are widely used in various industries due to their ability to function effectively in harsh climatic conditions. Key end-use sectors include aerospace and the petrochemical industry, where real-time temperature monitoring is crucial for ensuring process efficiency and safety. Smart devices and data collection systems are driving the market's growth, enabling remote monitoring and improved thermal management. The increasing adoption of green building practices and stringent emission norms in various industries further boosts demand for thermocouple temperature sensors. In the automotive sector, thermocouple temperature sensors play a significant role in automatic transmission systems and electric vehicle charging infrastructure.

- Renewable energy applications, such as solar and wind power, also require temperature monitoring, which is driving the demand for thermocouple temperature sensors. Overall, the market is expected to continue growing due to the increasing demand from various industries and the development of cost-effective solutions.

- The rise of autonomous and zero-emission vehicles is also expected to fuel market growth. Both base metal and noble metal thermocouples cater to diverse applications, with the former offering cost-effectiveness and the latter providing high accuracy and durability. The thermocouple sensors market is expected to expand steadily, driven by technological advancements, increasing demand for temperature monitoring, and regulatory compliance. Smart sensors and advanced thermal management solutions are anticipated to be key trends shaping the market's future.

How is this Thermocouple Temperature Sensors Industry segmented and which is the largest segment?

The thermocouple temperature sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Base metal thermocouple temperature sensor

- Noble metal thermocouple temperature sensor

- Application

- Oil and gas

- Food and beverages

- Automotive

- Chemical and petrochemical

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- France

- North America

- US

- Middle East and Africa

- South America

- APAC

By Type Insights

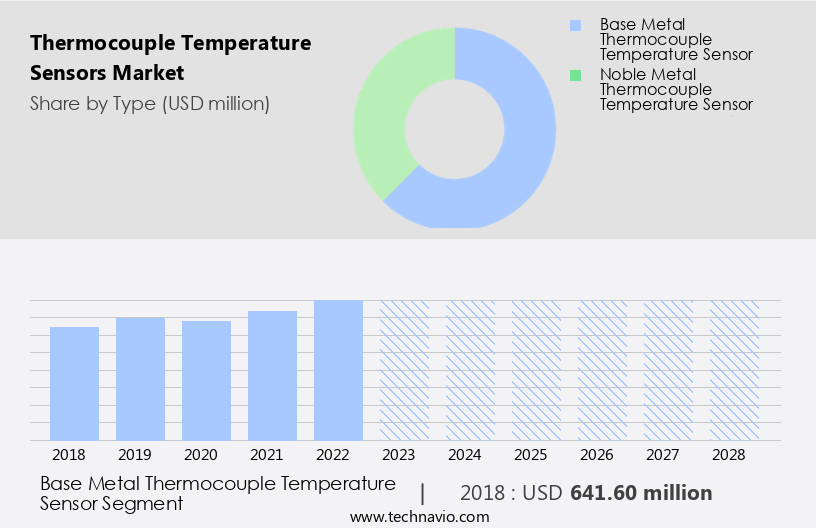

- The base metal thermocouple temperature sensor segment is estimated to witness significant growth during the forecast period.

Base metal thermocouple temperature sensors are essential components in various industries for measuring temperatures in harsh environments. These sensors, comprised of dissimilar metals like nickel and chromium, generate a voltage based on the temperature difference between them, enabling accurate temperature measurement. Base metal thermocouples are widely adopted in sectors such as automotive and petrochemicals due to their affordability and versatility.

In the automotive industry, they are utilized for engine temperature monitoring and exhaust gas temperature management. Additionally, they find applications in industries exposed to extreme temperatures, such as aerospace, renewable energy, and cryogenic temperatures. Base metal thermocouples are also employed in green building practices, thermal management systems, and automatic transmission systems to ensure efficient temperature control.

In the context of electric vehicles (EVs), they play a crucial role in battery charging, temperature-sensing elements, and life of devices. The market for thermocouple temperature sensors is anticipated to grow significantly due to the increasing demand for real-time monitoring, smart devices, data collection, and remote monitoring in various industries. Policymakers' emphasis on emission norms and the proliferation of autonomous and electric vehicles further boost the market growth. STMicroelectronics, a leading automotive sensor solutions provider, offers advanced powertrain controllers and automotive sensor solutions to cater to the growing demand for intelligent sensor technology.

Get a glance at the Thermocouple Temperature Sensors Industry report of share of various segments Request Free Sample

The Base metal thermocouple temperature sensor segment was valued at USD 641.60 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

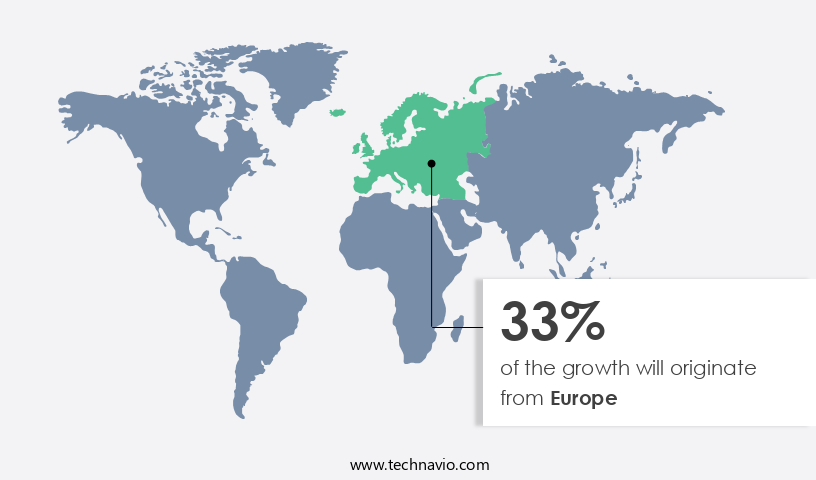

- Europe is estimated to contribute 33% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market experienced significant growth in APAC in 2023 due to the region's high industrialization rate. Industrial equipment, including HVAC, boilers, oil and pipelines, motors, and electrical components, are subjected to temperature fluctuations and expansion or contraction, which may impact precision and performance. Regular temperature checks are essential to prevent operational errors and ensure buyer confidence. With the largest concentration of manufacturing industries globally, APAC's demand for thermocouple temperature sensors is robust. These sensors are critical in various industries, such as aerospace, petrochemical, renewable energy, and automotive, where real-time monitoring, data collection, and remote monitoring are crucial. Thermocouple sensors are also integral to green building practices, thermal management, and electric vehicle charging infrastructure.

The market encompasses various types, including Base Metal Thermocouples, Noble Metal Thermocouples, and contactless sensors, catering to diverse temperature ranges and harsh climatic conditions, including cryogenic temperatures and radiofrequency interference. Smart sensors and intelligent sensor technology are also gaining popularity for their ability to enhance thermal management, powertrain controllers, and emission norms compliance In the automotive sector.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Thermocouple Temperature Sensors Industry?

Increasing demand for thermocouple temperature sensors is the key driver of the market.

- The market experiences continuous expansion due to their increasing application in various industries, particularly in sectors like petrochemicals and chemicals. The integration of advanced industrial IoT technologies has fueled the adoption of smart temperature sensors, enabling real-time monitoring and wireless data transmission. This innovation plays a pivotal role in ensuring product quality and process efficiency in industries such as automotive, electrical, and electronics. The automotive sector represents a significant market for thermocouple temperature sensors. In this industry, these sensors are employed in various applications, including thermal management, automatic transmission systems, emission norms compliance, and electric vehicle charging infrastructure. Thermocouple temperature sensors are essential for electric and autonomous vehicles, as they monitor heating issues and assist in battery charge management.

- Intelligent sensor technology integrated into these sensors enhances their functionality and extends the life of devices. Additionally, thermocouple temperature sensors find applications in industries like aerospace, renewable energy, and construction. In the aerospace sector, these sensors are utilized in harsh climatic conditions and extreme temperatures, such as cryogenic temperatures and radiofrequency interference (RFI). In renewable energy, they are employed in wind farms and green building practices. In construction, they are used for temperature measurement in various applications, including grounded, exposed, and ungrounded thermocouples. The temperature range of thermocouple temperature sensors caters to various industries, including metals and mining, oil and gas, life science, and household applications.

- Furthermore, they are increasingly being used in wearable devices and smart sensors.

What are the market trends shaping the Thermocouple Temperature Sensors Industry?

Increasing demand for wireless temperature sensing is the upcoming market trend.

- The market is experiencing significant growth due to the increasing demand for real-time temperature monitoring and data collection in various industries. These sensors are particularly useful in harsh climatic conditions and extreme temperatures, making them ideal for sectors such as aerospace, petrochemical, and power generation. In the aerospace industry, thermocouple temperature sensors are used to monitor engine temperatures and ensure optimal performance. In the petrochemical sector, they are employed to measure temperatures in cryogenic conditions and during chemical reactions. Moreover, the automotive sector is adopting thermocouple temperature sensors for thermal management in automatic transmission systems, emission norms compliance, and intelligent sensor technology for electric and autonomous vehicles.

- Renewable energy applications, such as wind farms, also utilize thermocouple temperature sensors for monitoring battery charges and temperature-sensing elements to maintain optimal performance. In the construction industry, thermocouple temperature sensors are used for green building practices and household applications. Smart devices, such as wearable devices, are increasingly integrating thermocouple temperature sensors for contactless temperature measurement. The temperature range of thermocouple temperature sensors makes them suitable for various industries, including metals and mining, oil and gas, life science, and more. Despite their advantages, thermocouple temperature sensors must be designed to withstand radiofrequency interference (RFI) and operate efficiently in harsh environments.

- STMicroelectronics offers automotive sensor solutions that address these challenges, providing reliable and accurate temperature measurement for powertrain controllers and heating issues. By adopting advanced sensor technology, manufacturers can extend the life of their devices, ensuring optimal performance and reliability. In summary, the market is driven by the increasing demand for real-time temperature monitoring and data collection in various industries, particularly those with harsh operating conditions and extreme temperatures. The ability of thermocouple temperature sensors to provide accurate temperature measurement and withstand harsh environments makes them an essential component in various applications, from aerospace and automotive to renewable energy and construction.

What challenges does the Thermocouple Temperature Sensors Industry face during its growth?

High cost of thermocouple temperature sensors is a key challenge affecting the industry growth.

- Thermocouple temperature sensors play a crucial role in various industries for precise temperature measurement under harsh climatic conditions. These sensors are widely used in sectors like Aerospace, Petrochemical, and Renewable Energy, including wind farms, due to their ability to function effectively in extreme temperatures and environments. Real-time monitoring and data collection are essential for industries to optimize processes and ensure efficiency. Thermocouple temperature sensors, with their smart devices and intelligent sensor technology, cater to these needs. However, the high cost of these sensors, which can be attributed to the sophisticated materials and complex manufacturing processes, poses a challenge for industries with limited budgets.

- This can hinder the growth of the market, particularly for small and medium-sized businesses. These sensors are also used In thermal management systems, automatic transmission systems, and electric vehicle charging infrastructure, with the increasing focus on emission norms, autonomous vehicles, and electric vehicles (EV). Moreover, thermocouple temperature sensors are essential for industries dealing with cryogenic temperatures, such as Liquefied Natural Gas (LNG) and Liquid Oxygen (LOX), and are resilient against Radiofrequency interference (RFI). The automotive sector, including automotive sensor solutions, powertrain controllers, and heating issues, also relies on thermocouple temperature sensors. The life of these devices is crucial for industries, particularly In the context of EV battery charges and temperature-sensing elements.

- In summary, the high cost of thermocouple temperature sensors is a significant challenge for industries with limited budgets, but their importance in various sectors, including Aerospace, Petrochemical, Renewable Energy, Automotive, and others, ensures their continued demand. The development of affordable EV offerings and advancements in sensor technology may help address the cost issue and expand the market.

Exclusive Customer Landscape

The thermocouple temperature sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thermocouple temperature sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, thermocouple temperature sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Amphenol Advanced Sensors

- Analog Devices Inc.

- Danfoss AS

- Dwyer Instruments LLC

- Emerson Electric Co.

- Endress Hauser Group Services AG

- General Electric Co.

- Honeywell International Inc.

- Keyence Corp.

- Kongsberg Gruppen ASA

- Microchip Technology Inc.

- NXP Semiconductors NV

- Pyromation

- Siemens AG

- STMicroelectronics International N.V.

- TE Connectivity Ltd.

- Texas Instruments Inc.

- WIKA Alexander Wiegand SE and Co. KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Thermocouple temperature sensors have gained significant traction in various industries due to their ability to measure temperature accurately in harsh climatic conditions. These sensors are widely used in sectors such as aerospace and petrochemical, where precise temperature measurement is crucial for ensuring optimal performance and safety. In the aerospace industry, thermocouple temperature sensors play a vital role in real-time monitoring of engine temperatures and fuel systems. The extreme temperatures encountered in aerospace applications necessitate the use of robust and reliable temperature sensors. These sensors enable aerospace manufacturers to maintaIn the optimal operating temperature of engines, ensuring maximum efficiency and reducing the risk of failures.

Similarly, In the petrochemical sector, thermocouple temperature sensors are used extensively for process control and safety applications. The sensors are employed to monitor the temperature of reactors, pipelines, and storage tanks, ensuring that the processes are operating within safe temperature limits. The increasing adoption of smart devices and data collection systems has led to the growth of remote monitoring applications for thermocouple temperature sensors. These sensors enable real-time temperature monitoring, providing valuable data for predictive maintenance and process optimization. Moreover, the growing trend towards green building practices and renewable energy sources has led to an increased demand for thermocouple temperature sensors in wind farms.

These sensors are used to monitor the temperature of wind turbine components, ensuring optimal performance and reducing downtime. Cryogenic temperatures are another area where thermocouple temperature sensors excel. These sensors are used extensively in applications such as liquid nitrogen storage and cryogenic processing, where temperatures can drop to extremely low levels. However, the use of thermocouple temperature sensors is not without challenges. Radiofrequency interference (RFI) can affect the accuracy of temperature readings, necessitating the use of shielded cables and other mitigation strategies. The automotive sector is another significant market for thermocouple temperature sensors. These sensors are used in various applications, including thermal management, automatic transmission systems, and emission norms compliance.

With the increasing adoption of electric vehicles (EVs) and autonomous vehicles, the demand for intelligent sensor technology, including temperature sensors, is expected to grow. The life of thermocouple temperature sensors depends on various factors, including the temperature range, application, and materials used. Base metal thermocouples and noble metal thermocouples are the two most common types of thermocouples, each with its unique advantages and limitations. The increasing sales of EVs and the availability of affordable EV offerings are expected to drive the demand for thermocouple temperature sensors In the automotive sector. These sensors are used to monitor battery charges, temperature-sensing elements, and other critical components to ensure optimal performance and safety. In conclusion, the market is driven by various factors, including the need for precise temperature measurement in harsh environments, the increasing adoption of smart devices and data collection systems, and the growing trend towards renewable energy and green building practices. The challenges associated with RFI and the evolving requirements of the automotive sector present opportunities for innovation and growth In the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

190 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.45% |

|

Market growth 2024-2028 |

USD 892.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.41 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Thermocouple Temperature Sensors Market Research and Growth Report?

- CAGR of the Thermocouple Temperature Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the thermocouple temperature sensors market growth of industry companies

We can help! Our analysts can customize this thermocouple temperature sensors market research report to meet your requirements.

RIA -

RIA -