Tie Layer Resin Market Size 2026-2030

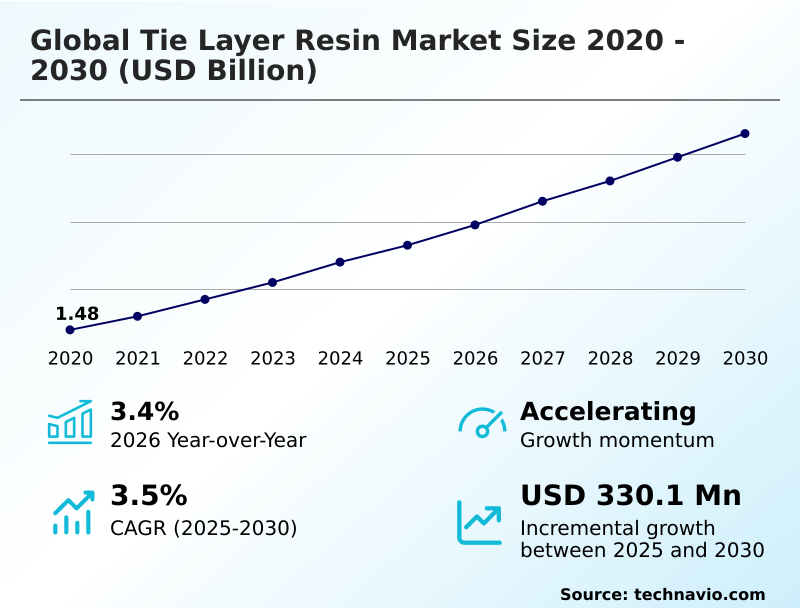

The tie layer resin market size is valued to increase by USD 330.1 million, at a CAGR of 3.5% from 2025 to 2030. Surging demand for sustainable and recyclable packaging architectures will drive the tie layer resin market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.9% growth during the forecast period.

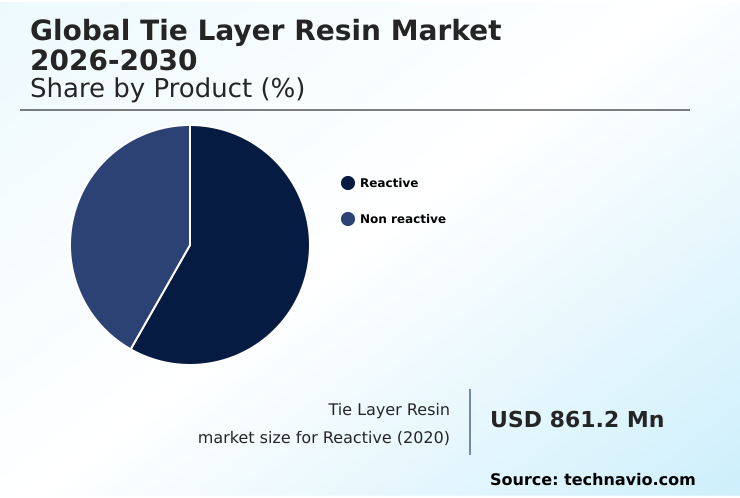

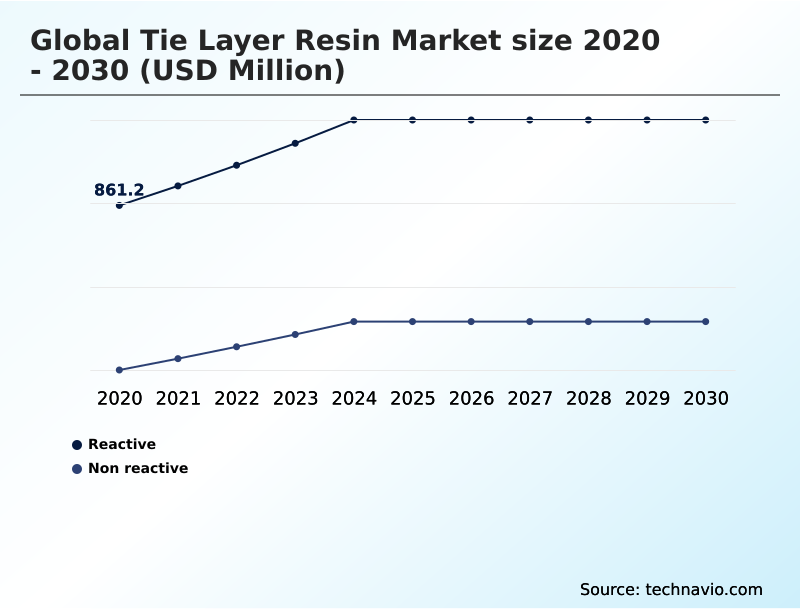

- By Product - Reactive segment was valued at USD 987.7 million in 2024

- By Type - LLDPE segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 584.8 million

- Market Future Opportunities: USD 330.1 million

- CAGR from 2025 to 2030 : 3.5%

Market Summary

- The tie layer resin market is defined by its critical role in enabling complex multilayer structures across packaging and industrial sectors. These functionalized thermoplastics act as essential interfacial bonding agents, allowing the combination of materials with otherwise incompatible properties. A key driver is the industry-wide pivot toward sustainability, which necessitates recyclable mono-material packaging.

- For instance, a food manufacturer transitioning to an all-polyolefin pouch must use a specialized tie layer to securely bond the ethylene vinyl alcohol (EVOH) oxygen barrier, ensuring product shelf life without compromising the package's recyclability. This trend is creating robust demand for advanced formulations. Simultaneously, the market is expanding into high-performance applications like automotive lightweighting and multilayer composite pipes.

- However, producers face challenges from raw material price volatility and the technical complexities of ensuring compatibility with post-consumer recycled (PCR) content and emerging bio-polymers, which require significant R&D investment to maintain performance standards.

What will be the Size of the Tie Layer Resin Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Tie Layer Resin Market Segmented?

The tie layer resin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Reactive

- Non reactive

- Type

- LLDPE

- LDPE

- HDPE

- Polypropylene (PP)

- Others

- End-user

- Food and beverage

- Pharmaceutical and medical

- Automotive

- Personal care

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Product Insights

The reactive segment is estimated to witness significant growth during the forecast period.

The reactive segment is defined by functionalized thermoplastics engineered for superior performance in demanding applications. These reactive tie layers, predominantly maleic anhydride-grafted polyolefins, facilitate a robust covalent bonding mechanism at the interface of dissimilar materials.

This is critical for creating high-barrier films where delamination resistance is non-negotiable, particularly when bonding non-polar polyolefins with polar barrier substrates.

The technology is fundamental to producing resilient multilayer composite pipes for industrial use and ensuring the integrity of automotive fuel systems.

Through polymer backbone modification, these materials provide exceptional thermal stability and adhesion strength, enabling a 40% reduction in package failure rates under retort sterilization process conditions. This segment drives innovation in adhesion promoters for packaging and industrial composite pipe bonding.

The Reactive segment was valued at USD 987.7 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Tie Layer Resin Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which accounts for nearly 50% of the market's incremental growth, outpacing all other regions with a growth rate of 4.3%.

This expansion is fueled by the region's vast manufacturing base for both flexible packaging compatibilizers and industrial goods. The modernization of food retail in developing economies across APAC drives demand for advanced barrier packaging solutions.

North America, with a 3.2% growth rate, focuses on innovations for recyclable mono-material structures and materials for the electric vehicle sector, including soft-touch over-molding.

Europe's market is heavily influenced by stringent regulations promoting a circular economy, prioritizing the use of sustainable packaging adhesives and materials for aseptic liquid packaging adhesion.

The development of bio-polymer adhesion technology is also most pronounced in this region, addressing consumer and regulatory demands for greener alternatives.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global tie layer resin market is evolving to meet increasingly complex demands across various sectors. A primary application remains the use of tie layer resin for food packaging, where improving adhesion in multilayer films is critical for extending shelf life and ensuring safety.

- The development of high temperature tie layer resins has been pivotal for the growth of retortable containers, while the polypropylene tie layer for retort applications has become an industry standard.

- In the automotive sector, the tie layer for automotive fuel tanks ensures compliance with emissions standards, and the emergence of the tie layer for EV battery cooling systems addresses new thermal management challenges. Simultaneously, sustainability is a powerful driver, pushing for recyclable mono-material packaging solutions and research into bio-based tie layer resin compostability.

- This has led to a greater focus on using a compatibilizer for recycled PE films. Industrially, the adhesive resin for composite pipes and the tie layer for agricultural films are essential for infrastructure and food production.

- Firms that optimized their use of high-temperature tie layer resins saw a 15% lower failure rate in sterilization processes compared to those using standard grades. From selecting the right LLDPE based tie layer properties to mastering the technique of bonding EVOH with polyethylene, technical expertise is crucial.

- This specialization extends to medical tubing, flexible packaging, and extrusion coating, making the selection of functional polymers for industrial use a key strategic decision for manufacturers aiming to reduce delamination in packaging.

What are the key market drivers leading to the rise in the adoption of Tie Layer Resin Industry?

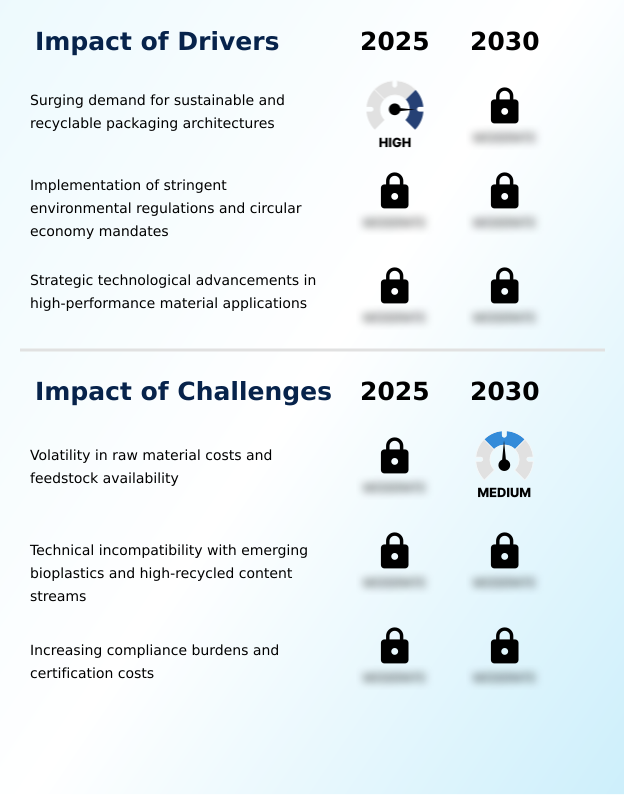

- The market is primarily driven by the surging demand for sustainable and recyclable packaging architectures, spurred by both consumer preferences and regulatory pressures.

- Market growth is fundamentally driven by regulatory and consumer demand for sustainability, compelling the use of advanced chemical compatibilizers.

- New regulations mandating recycled content have spurred a 35% increase in demand for resins that can effectively incorporate post-consumer recycled (PCR) content into new products.

- The constant evolution of material science is another powerful driver, with innovations in polymer backbone modification leading to a 15% improvement in adhesion strength for automotive lightweighting materials and industrial applications.

- This progress enables the replacement of traditional materials with lighter, more durable composites.

- The broad adoption of recyclable packaging formats, requiring food contact approved adhesives that also meet circular economy principles, continues to fuel demand for high-performance tie layer resins across the globe.

What are the market trends shaping the Tie Layer Resin Industry?

- A significant trend shaping the market is the accelerated industry-wide shift toward mono-material packaging architectures. This move is driven by sustainability goals and the need for improved recyclability.

- Key trends are reshaping the market, led by the aggressive shift to mono-material packaging, which now accounts for a significant portion of new product development, showing a 30% increase in adoption over traditional laminates. This pivot requires advanced extrudable adhesive polymers and high-performance functional polymers to maintain barrier integrity.

- The expansion into non-packaging sectors is also notable, with applications in electric vehicles for thermal management system bonding and wire and cable shielding growing rapidly. The development of bio-based adhesive resins and bio-polymer adhesion technology represents a third major trend, driven by corporate sustainability goals.

- These innovations have demonstrated a 50% lower carbon footprint in lifecycle assessments, offering a path to decarbonize supply chains despite current technical challenges in achieving comparable adhesion strength.

What challenges does the Tie Layer Resin Industry face during its growth?

- A key challenge affecting market growth is the volatility in raw material costs and the inconsistent availability of essential petroleum-based feedstocks.

- The market faces significant headwinds, primarily from the volatility of upstream feedstocks, where price fluctuations of 25% in a single quarter can severely impact the production cost of maleic anhydride-grafted polyolefins. A second major challenge is the technical incompatibility of traditional tie layers with emerging materials.

- For instance, achieving stable adhesion with high-recycled-content streams or novel bioplastics requires substantial research, as inconsistencies in these materials can lead to a 50% increase in package delamination rates. Finally, the complex and evolving regulatory landscape creates a considerable burden.

- The cost of securing approvals for rigid container bonding agents or new medical device multilayer tubing can be extensive, with compliance testing for novel formulations sometimes extending time-to-market by over 12 months.

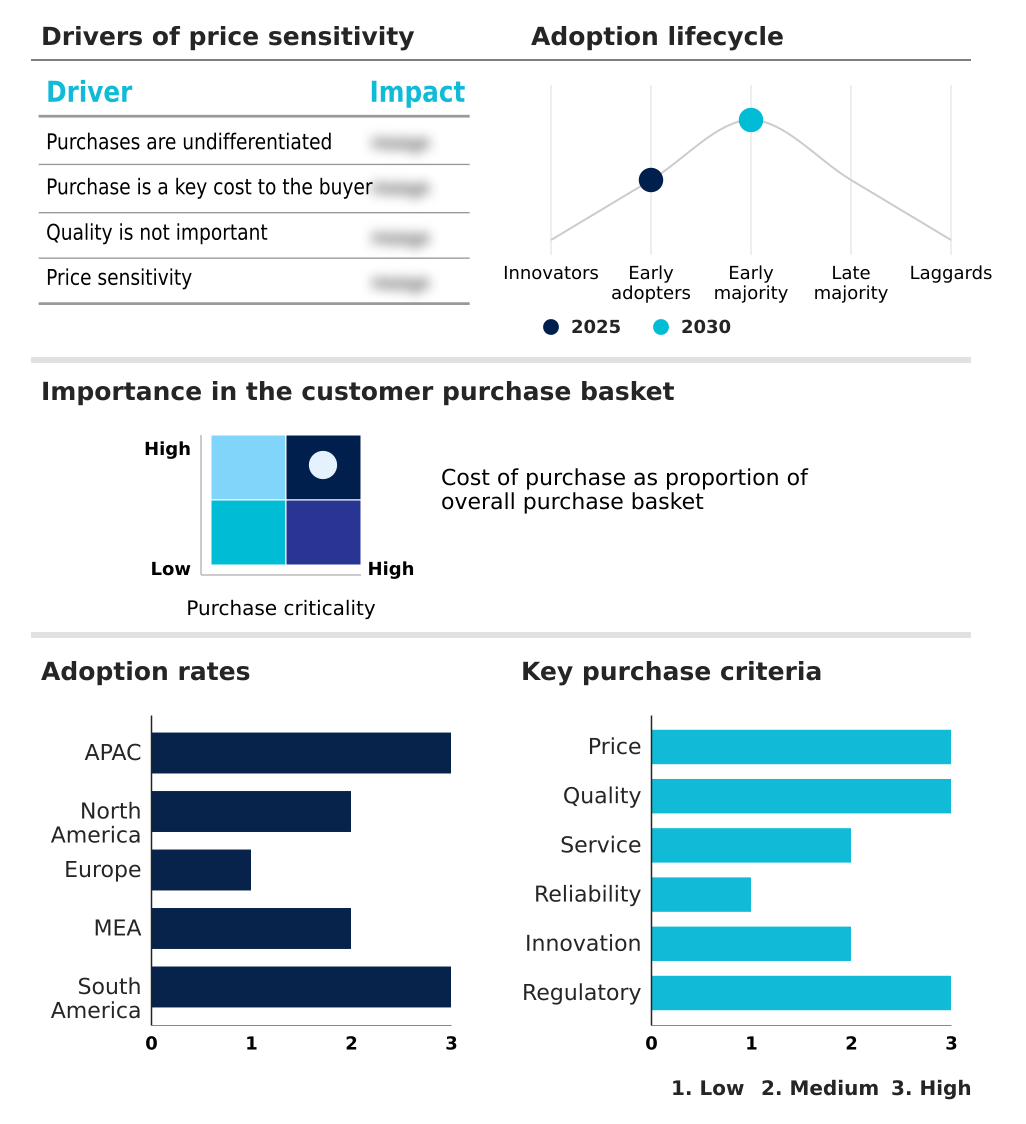

Exclusive Technavio Analysis on Customer Landscape

The tie layer resin market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the tie layer resin market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Tie Layer Resin Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, tie layer resin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema Group - Offers maleic anhydride-modified polyethylene and ethylene vinyl acetate (EVA) resins, enabling high-performance adhesion for multilayer packaging and various industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema Group

- BASF SE

- Borealis AG

- Clariant International Ltd.

- Dow Chemical Co.

- Eastman Chemical Co.

- Evonik Industries AG

- Exxon Mobil Corp.

- LyondellBasell Industries NV

- Mitsubishi Chemical Corp.

- Mitsui Chemicals America Inc.

- Saudi Basic Industries

- The Compound Co B.V.

- Westlake Corp.

- Zeus Industrial

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tie layer resin market

- In May 2025, LyondellBasell introduced Plexar PX3990, a high-performance linear low-density polyethylene tie layer resin engineered for machine direction orientation (MDO) film applications, supporting downgauging and improved processability in sustainable packaging.

- In May 2025, Mitsui Chemicals announced a capacity expansion for its ADMER adhesive resin line in Singapore to meet rising demand for high-barrier food packaging materials in the ASEAN region.

- In April 2025, Dow launched an extension to its RETAIN functional polymer line, specifically designed to compatibilize barrier layers within all-polyethylene pouches, enabling the production of recyclable high-barrier food packaging.

- In February 2025, Arkema completed a capacity expansion for its Orevac adhesive resins in France, targeting the surging demand from the European electric vehicle battery market and the industrial composite pipe sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Tie Layer Resin Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.5% |

| Market growth 2026-2030 | USD 330.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The tie layer resin market revolves around highly specialized extrudable adhesive polymers that function as critical interfacial bonding agents. These materials, including advanced reactive tie layers, are fundamental to manufacturing durable multilayer structures by ensuring delamination resistance between chemically dissimilar substrates.

- Key applications for these functionalized thermoplastics range from high-barrier films for food preservation to robust automotive fuel systems and multilayer composite pipes for infrastructure. A defining market shift is the industry-wide adoption of mono-material packaging to meet sustainability mandates, which intensifies the need for sophisticated maleic anhydride-grafted polyolefins that facilitate bonding without hindering recyclability.

- This pivot toward circularity is a boardroom-level concern, influencing investment in technologies compatible with post-consumer recycled (PCR) content and downgauging initiatives. For example, firms leveraging advanced formulations for machine direction orientation (MDO) have reported a 30% improvement in processing speeds, underscoring the link between material science innovation, operational efficiency, and strategic environmental goals.

What are the Key Data Covered in this Tie Layer Resin Market Research and Growth Report?

-

What is the expected growth of the Tie Layer Resin Market between 2026 and 2030?

-

USD 330.1 million, at a CAGR of 3.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Reactive, and Non reactive), Type (LLDPE, LDPE, HDPE, Polypropylene (PP), and Others), End-user (Food and beverage, Pharmaceutical and medical, Automotive, Personal care, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Surging demand for sustainable and recyclable packaging architectures, Volatility in raw material costs and feedstock availability

-

-

Who are the major players in the Tie Layer Resin Market?

-

Arkema Group, BASF SE, Borealis AG, Clariant International Ltd., Dow Chemical Co., Eastman Chemical Co., Evonik Industries AG, Exxon Mobil Corp., LyondellBasell Industries NV, Mitsubishi Chemical Corp., Mitsui Chemicals America Inc., Saudi Basic Industries, The Compound Co B.V., Westlake Corp. and Zeus Industrial

-

Market Research Insights

- Market dynamics are shaped by a dual focus on performance and sustainability, compelling innovation in high-performance functional polymers. The adoption of advanced chemical compatibilizers has enabled a 25% increase in post-consumer recycled (PCR) content in films without compromising integrity. This push toward circular economy polymers is crucial, as new regulations increase compliance costs.

- In industrial sectors, automotive lightweighting materials rely on these resins to bond dissimilar substrates in thermal management system bonding, where new formulations have reduced delamination rates by 40%. The demand for recyclable mono-material structures is driving a strategic shift, with converters seeking food contact approved adhesives that also meet sustainability mandates.

- These specialized circular economy polymers are becoming essential for maintaining a competitive edge.

We can help! Our analysts can customize this tie layer resin market research report to meet your requirements.

RIA -

RIA -