Tin Market Size 2025-2029

The tin market size is valued to increase USD 876.6 million, at a CAGR of 2.1% from 2024 to 2029. Growing demand for canned foods and beverages will drive the tin market.

Major Market Trends & Insights

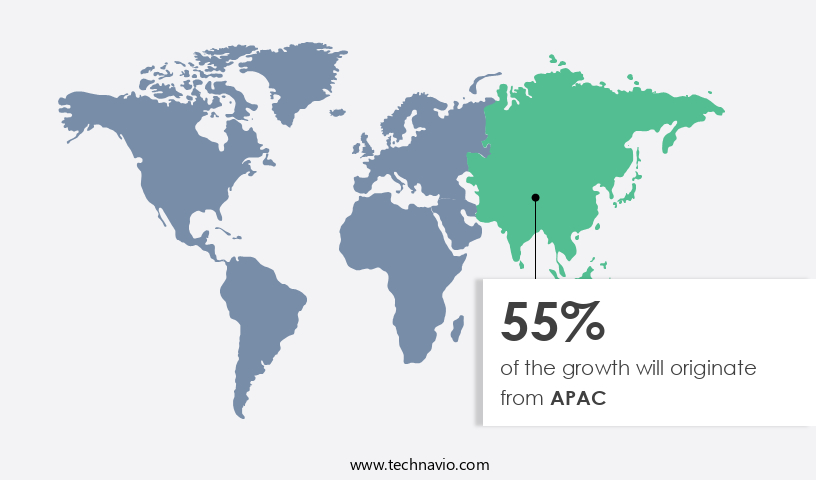

- APAC dominated the market and accounted for a 55% growth during the forecast period.

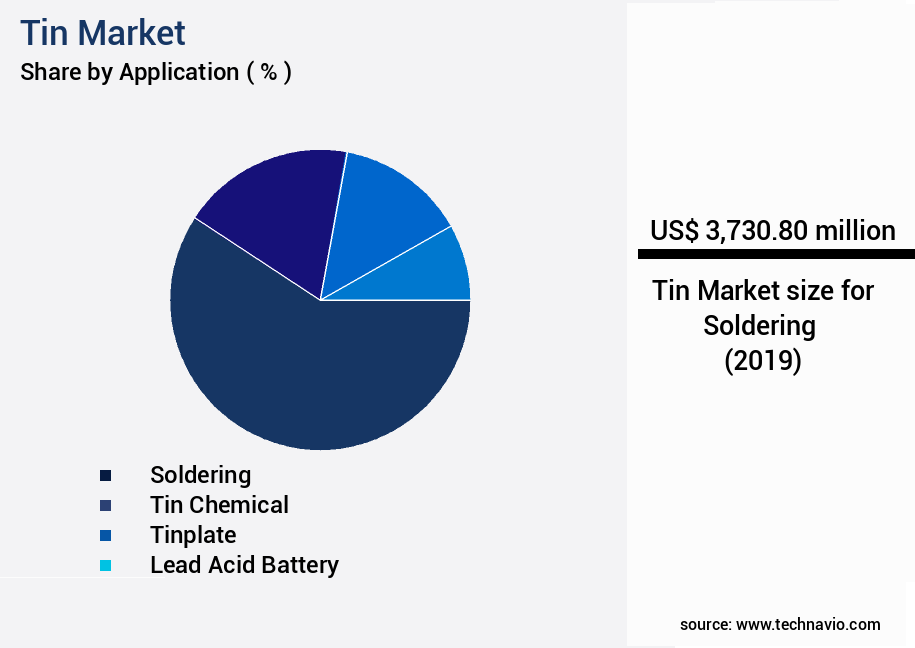

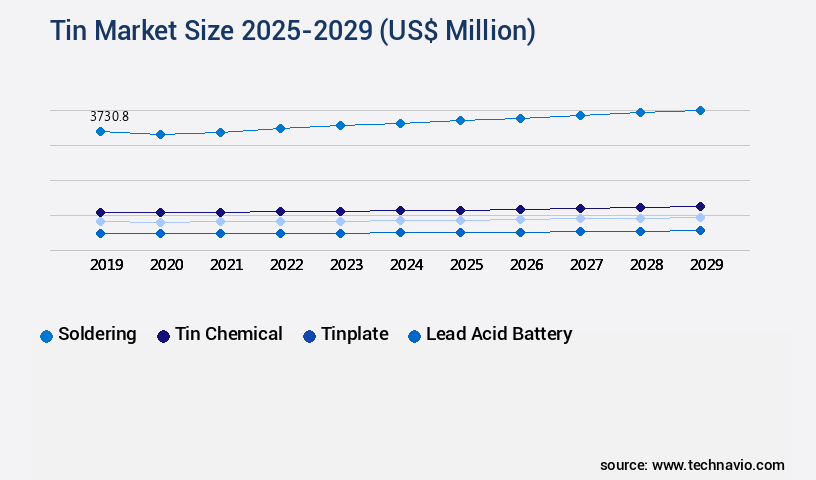

- By Application - Soldering segment was valued at USD 3730.80 million in 2023

- By End-user - Electronics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 17.76 million

- Market Future Opportunities: USD 876.60 million

- CAGR : 2.1%

- APAC: Largest market in 2023

Market Summary

- The market is a dynamic and evolving entity that continues to shape the global economy, particularly in the realm of core technologies and applications. With the growing demand for canned foods and beverages, the market for tin is experiencing a significant surge. According to recent reports, the global market share for canned food and beverages is projected to reach 30% by 2026. Simultaneously, there is a noticeable shift toward recycling of tin, making it an increasingly sustainable choice for various industries.

- Another key trend is the rise of tin-free steel in the packaging industry, which may challenge the market's growth trajectory. Regulations, such as the European Union's Circular Economy Package, further influence the market's evolution by promoting the circular use of resources. These factors, among others, contribute to the ongoing unfolding of market activities and evolving patterns in the market.

What will be the Size of the Tin Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Tin Market Segmented and what are the key trends of market segmentation?

The tin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Soldering

- Tin chemical

- Tinplate

- Lead acid battery

- Others

- End-user

- Electronics

- Automotive

- Packaging

- Glass

- Others

- Product Type

- Metal

- Alloy

- Compounds

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The soldering segment is estimated to witness significant growth during the forecast period.

The market holds significant importance in various industries, particularly in the realm of soldering applications. Soldering, a process used to bond components on a printed circuit board (PCB), accounts for the largest share in terms of volume. Tin is a crucial metal employed in soldering pastes, which are essential for facilitating electrical connections between components. Commonly used alloys include tin-lead, tin-antimony, and tin-silver-copper. These alloys find extensive applications in semiconductors and PCBs for consumer electronics, marine, automotive, and aerospace components. The global demand for electronic devices, such as smartphones, computers, tablets, laptops, medical testing equipment, nuclear detection systems, and weather analysis equipment, drives the need for PCBs and soldering pastes.

Furthermore, seed treatment technologies have emerged as a promising area for the market. Tin compounds are used as fungicides to enhance nutrient uptake efficiency and promote fruit production increase. In-furrow application of these compounds can stimulate root development, while biofertilizer application methods can improve nutrient use efficiency and crop stress tolerance. Precision farming techniques and foliar application strategies are other evolving trends in the market. Humic acid fertilizers, nitrogen fixation bacteria, phosphorus solubilizing fungi, microbial inoculants, and photosynthesis enhancement are key components of these farming practices. These techniques aim to optimize crop production, improve soil health, and enhance crop quality.

Environmental sustainability is a significant focus in the agricultural sector, leading to the adoption of sustainable agriculture practices. The market players are increasingly investing in yield enhancement technology, soil nutrient cycling, and biotic stress resistance to meet the growing demand for sustainable farming methods. The market for tin is expected to witness substantial growth, with an estimated 22% of the global tin demand originating from the electronics industry. Additionally, the agricultural sector is projected to account for approximately 35% of the global tin demand by 2025. The increasing adoption of precision farming techniques, disease suppression agents, and water use efficiency measures will further fuel the market growth.

Moreover, the market is witnessing advancements in soil amendment techniques, pest resistance mechanisms, plant growth regulators, and plant hormone modulation. These developments are expected to enhance crop production optimization and improve plant vigor, leading to higher yields and better-quality produce.

The Soldering segment was valued at USD 3730.80 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 55% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Tin Market Demand is Rising in APAC Request Free Sample

In the dynamic the market, APAC holds a significant role as the largest producer and consumer. With numerous tin mines in this region and the presence of major industry players, economic growth in APAC has fueled the expansion of key end-user industries like automotive, electrical equipment, electronics components, packaging, and industrial machinery. The demand for tin increases due to its essential role in enhancing product durability and resistivity.

Foreign investments, advanced manufacturing machinery, and equipment contribute to the growth of the manufacturing sector in APAC countries. Electronics manufacturing in APAC is a major center for tin usage, as it is a crucial component in soldering due to its low melting point and strong bonding properties.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of applications, from industrial manufacturing to agricultural advancements. One significant area of research in this sector is the role of rhizosphere microbial community analysis in enhancing plant growth and nutrient availability. Plant growth promoting bacteria identification and mycorrhizal fungal network development are key focuses, as they contribute to soil organic carbon sequestration rates and plant hormone signaling transduction pathways. These biological processes play a crucial role in abiotic stress tolerance mechanisms in plants, such as nitrogen use efficiency in grain crops and phosphorus acquisition strategies in legumes. The impact of soil pH on nutrient availability is also a critical factor, as is the effect of salinity on plant growth parameters.

Water stress mitigation strategies for crops, including drought resistance mechanisms in cereals and heat shock protein expression in plants, are essential for maintaining productivity under challenging conditions. Additionally, heavy metal accumulation in plants and phytoextraction efficiency of different plants are vital aspects of sustainable soil management practices. Biological control of plant diseases and integrated pest management strategies are integral to reducing the environmental impact of farming. Precision agriculture technologies and crop yield optimization strategies further enhance agricultural productivity while minimizing resource consumption. Comparatively, a substantial portion of research efforts in the market are directed towards understanding and addressing the environmental impact assessment of farming practices.

For instance, the industrial application segment accounts for a significantly larger share of the market applications compared to the academic segment, reflecting the growing demand for sustainable and efficient agricultural practices.

What are the key market drivers leading to the rise in the adoption of Tin Industry?

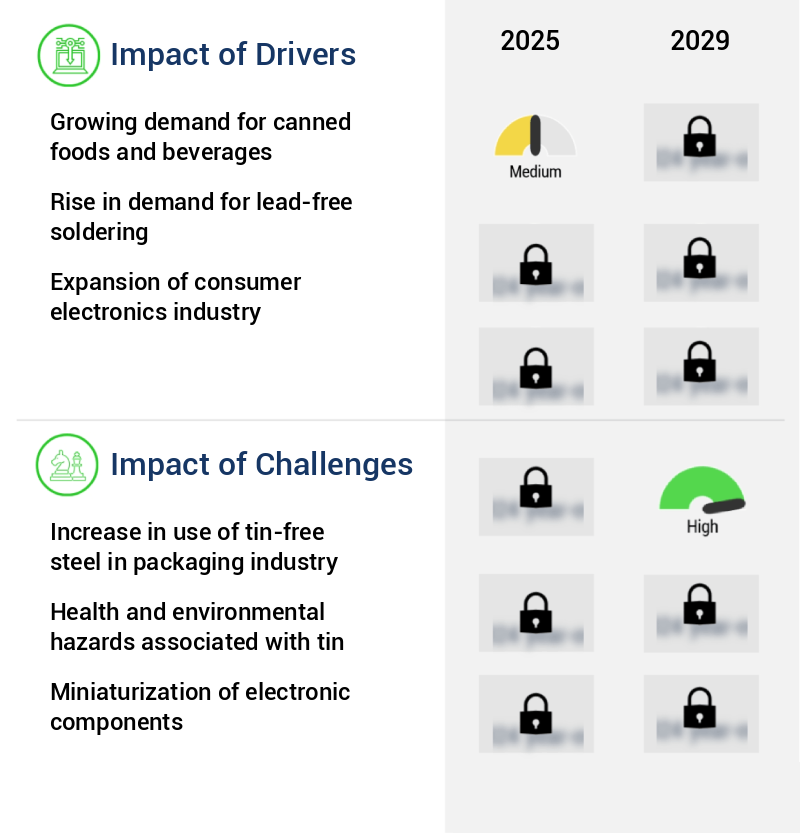

- The surge in consumer preference for convenient and long-lasting food and beverage options, as reflected in the increasing demand for canned products, is the primary market growth driver.

- Metal can packaging plays a crucial role in preserving food and beverages, contributing to the expansion of the global canned food and beverages market. Factors fueling this growth include the rising consumption of convenience food products, economic development, the recyclability of metal cans, evolving lifestyles, and consumer preferences. Metal cans are primarily composed of aluminum, tin-coated steel, tin-free steel, and other materials. Tinplate steel, in particular, is widely used for canned food and beverage packaging due to its corrosion resistance, cost-effectiveness, and physical strength.

- Market players employ tin coating as a strategic differentiator to cater to consumers' demands. This professional, data-driven analysis underscores the significance of metal can packaging in various sectors and its ongoing role in shaping the canned food and beverages market.

What are the market trends shaping the Tin Industry?

- The focus is increasingly shifting toward the recycling of tin in the market. This trend is expected to gain momentum in the upcoming period.

- Tin, a versatile metal with both beneficial and hazardous properties, is increasingly being recycled and reused to mitigate environmental concerns. Companies are adopting this approach for tin cans, scrap, and residue from manufacturing processes. Recycling tin products, whether in-house or through external scrap-processing firms, is a strategic business move. Metals, including tin, are valuable resources due to their inherent properties and economic viability.

- The International Council on Mining and Metals (ICMM) advocates for metal recycling to enhance business efficiency. This practice leads to reduced emissions, improved resource productivity, and effective waste disposal. By recycling tin, 76% of the energy required to produce new tin is conserved. This data underscores the significance of tin recycling in today's business landscape.

What challenges does the Tin Industry face during its growth?

- The use of tin-free steel in the packaging industry poses a significant challenge to its growth, as this material's increasing adoption necessitates industry adjustments in terms of production processes, cost management, and technological innovation.

- Tin-free steel (TFS), also known as electrolytic chromium-coated steel or black plate steel, is increasingly replacing tinplate in the packaging industry. This shift is driven by TFS's advantages, including superior lacquer adhesion, printability, and corrosion resistance. TFS is utilized extensively in various packaging applications, such as drawn cans, candy tins, can ends, spray cans, photographic film cases, and protective material for optical fiber cables. The packaging industry's adoption of TFS has resulted in a significant market trend, posing a challenge to the growth of the market.

- According to recent industry data, the tinplate market share is projected to decrease by approximately 2% annually over the next five years. This trend underlines the evolving nature of the packaging industry and the ongoing competition between alternative materials and traditional tinplate.

Exclusive Customer Landscape

The tin market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the tin market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Tin Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, tin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABM Metal Tech - The company specializes in manufacturing and supplying a range of tin products for various industries. Their offerings include packing tin containers, printed tin containers, slip lip tin cans, ointment packaging tin containers, and tin container lids, among others. These high-quality tin products cater to diverse market needs, ensuring sustainable and cost-effective solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABM Metal Tech

- ArcelorMittal

- Aurubis AG

- Bharat Tin Works

- Bharat Ultimate Packaging Pvt. Ltd.

- DuPont de Nemours Inc.

- Empresa Metalurgica Vinto

- Hindustan Tin Works Ltd.

- Indium Corp.

- Malaysia Smelting Corp. Berhad

- Minsur SA

- Nikitha Containers Pvt. Ltd.

- PT TIMAH Persero Tbk

- Saksham Containers Pvt. Ltd.

- Suraj Containers Ltd.

- Swastik Tins Pvt. Ltd.

- Thailand Smelting and Refining Co. Ltd.

- Yunnan Tin Group Holding Co. Ltd.

- Zenith Tins Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tin Market

- In January 2024, leading tin producer, Tsingshan Holding Group, announced the completion of its new 20,000-ton per year tin smelter in Indonesia. This expansion marked a significant increase in the company's production capacity and strengthened its position as a major player in The market (Tsingshan Holding Group press release).

- In March 2024, tin mining company, Mines de Tinting, entered into a strategic partnership with battery manufacturer, Saft Groupe S.A. This collaboration aimed to explore opportunities for the recycling of tin from used batteries, addressing the growing demand for sustainable tin sources (Mines de Tinting press release).

- In May 2024, tin mining company, PT Timah Tbk, secured a USD100 million investment from a consortium led by Trafigura Group. The funds were earmarked for the expansion of PT Timah's Bangka Tin Mine in Indonesia, increasing its production capacity by 15,000 tons per year (PT Timah Tbk press release).

- In April 2025, the European Union (EU) passed the Circular Electronics Alliance (CEA) regulation, which included a ban on the export of certain waste materials, including tin, from EU countries. This policy change aimed to encourage the recycling of these materials within the EU and promote the circular economy (European Commission press release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Tin Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

230 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.1% |

|

Market growth 2025-2029 |

USD 876.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.1 |

|

Key countries |

China, US, India, Japan, South Korea, Germany, UK, Australia, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving world of agriculture, the market plays a pivotal role in enhancing nutrient uptake efficiency and driving fruit production increase. Seed treatment technologies, such as in-furrow applications and foliar strategies, are revolutionizing farming practices by improving root development and stimulating vegetable growth. Biofertilizer application methods, including humic acid fertilizers and microbial inoculants, are key contributors to organic matter decomposition and soil nutrient cycling. Precision farming techniques, like nitrogen fixation bacteria and phosphorus solubilizing fungi, play a crucial role in improving nutrient use and crop stress tolerance. These advancements not only lead to yield enhancement technology but also contribute to sustainable agriculture practices by mitigating abiotic stress and enhancing biotic stress resistance.

- Photosynthesis enhancement and water use efficiency are essential aspects of the market, with plant growth regulators and soil amendment techniques optimizing grain yield and plant vigor improvement. Soil health is significantly improved through the application of these technologies, leading to enhanced crop quality and pest resistance mechanisms. The market continues to unfold, with ongoing research and development in plant hormone modulation and disease suppression agents. These advancements are essential in the pursuit of sustainable agriculture practices, ensuring environmental sustainability and the continued optimization of crop production. In summary, the market is a thriving sector, driven by the continuous development and implementation of innovative technologies that enhance nutrient uptake efficiency, fruit production, and overall crop health.

- These advancements not only improve yield and quality but also contribute to sustainable agriculture practices, ensuring a more efficient and productive future for agriculture.

What are the Key Data Covered in this Tin Market Research and Growth Report?

-

What is the expected growth of the Tin Market between 2025 and 2029?

-

USD 876.6 million, at a CAGR of 2.1%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Soldering, Tin chemical, Tinplate, Lead acid battery, and Others), End-user (Electronics, Automotive, Packaging, Glass, and Others), Product Type (Metal, Alloy, and Compounds), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for canned foods and beverages, Increase in use of tin-free steel in packaging industry

-

-

Who are the major players in the Tin Market?

-

Key Companies ABM Metal Tech, ArcelorMittal, Aurubis AG, Bharat Tin Works, Bharat Ultimate Packaging Pvt. Ltd., DuPont de Nemours Inc., Empresa Metalurgica Vinto, Hindustan Tin Works Ltd., Indium Corp., Malaysia Smelting Corp. Berhad, Minsur SA, Nikitha Containers Pvt. Ltd., PT TIMAH Persero Tbk, Saksham Containers Pvt. Ltd., Suraj Containers Ltd., Swastik Tins Pvt. Ltd., Thailand Smelting and Refining Co. Ltd., Yunnan Tin Group Holding Co. Ltd., and Zenith Tins Pvt. Ltd.

-

Market Research Insights

- The market encompasses the global trade of tin, a versatile and essential mineral with numerous applications in various industries. In 2020, tin production reached approximately 350,000 metric tons, a 3% increase from the previous year. Simultaneously, tin consumption grew by 2% to around 380,000 metric tons, driven by the demand for tin in sectors such as electronics, automotive, and construction. The market's significance lies in its role in enhancing product performance and functionality. For instance, tin is a critical component in the production of solder alloys, which are essential in the electronics industry for connecting various components. Additionally, tin's ability to improve soil structure, reduce water consumption, and enhance carbon storage makes it a valuable addition to agricultural applications.

- Moreover, tin's properties contribute to its use in various industries. In the automotive sector, tin coatings protect against corrosion and improve fuel efficiency. In construction, tin is used in roofing and coating materials due to its durability and resistance to weathering. The interplay between tin production and consumption underscores the market's continuous evolution, with ongoing research exploring its potential applications in areas such as enhanced biodiversity, heavy metal detoxification, and heat stress alleviation.

We can help! Our analysts can customize this tin market research report to meet your requirements.

RIA -

RIA -