Transportation Management Systems Market Size 2026-2030

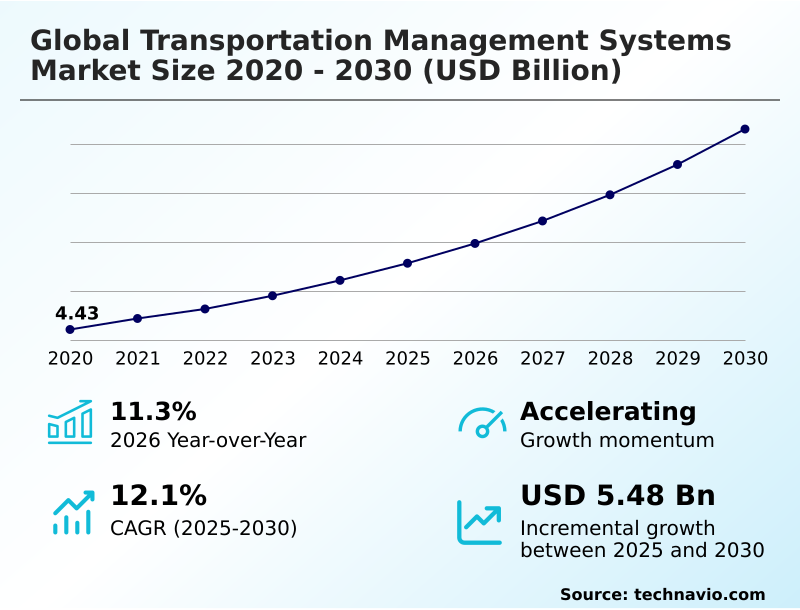

The transportation management systems market size is valued to increase by USD 5.48 billion, at a CAGR of 12.1% from 2025 to 2030. Increasing adoption of AI and machine learning for predictive logistics will drive the transportation management systems market.

Major Market Trends & Insights

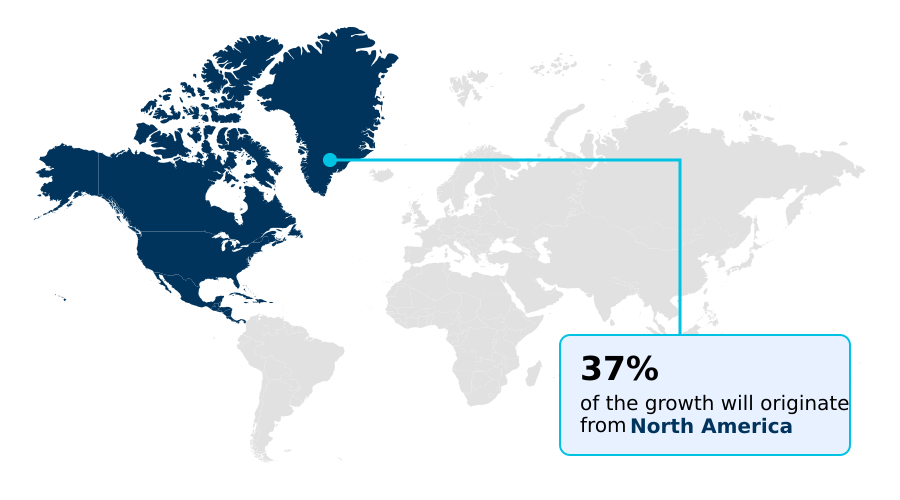

- North America dominated the market and accounted for a 36.7% growth during the forecast period.

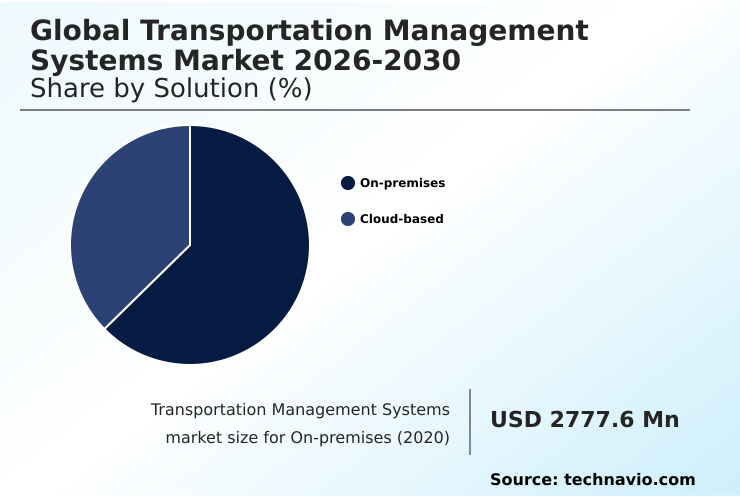

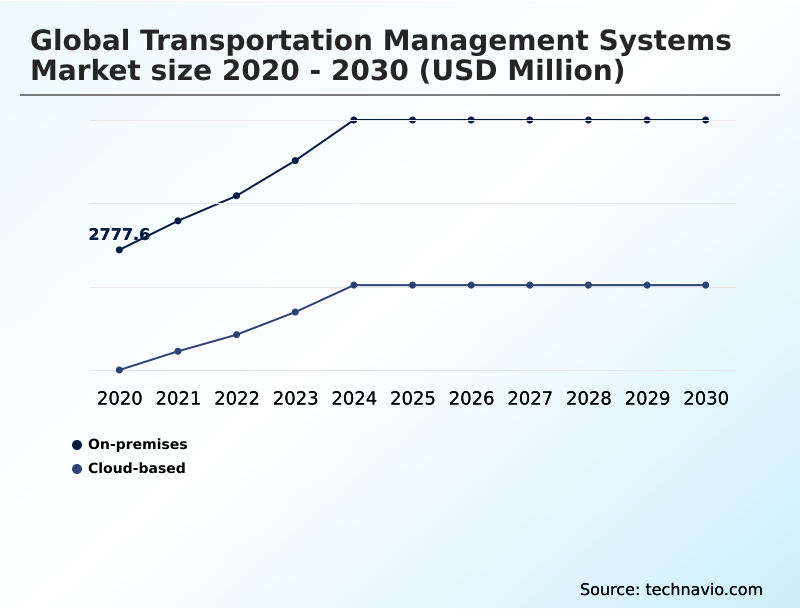

- By Solution - On-premises segment was valued at USD 3.99 billion in 2024

- By Mode of Transportation - Roadways segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.19 billion

- Market Future Opportunities: USD 5.48 billion

- CAGR from 2025 to 2030 : 12.1%

Market Summary

- The transportation management systems market is undergoing a significant transformation, driven by the need for enhanced visibility and digital integration in increasingly complex logistics networks. The adoption of cloud native tms architecture is accelerating, offering companies greater scalability and reduced operational overhead.

- As businesses grapple with volatile fuel costs and dynamic trade policies, the demand for advanced analytics and automated workflows has become critical. For instance, a global manufacturing firm can leverage a modern TMS to optimize multimodal shipping routes in real time, balancing carrier costs with delivery timelines to maintain service-level agreements.

- This involves integrating real time shipment visibility with predictive insights to mitigate the impact of port congestion or weather disruptions. Furthermore, the push for greater environmental responsibility is influencing logistics strategies, with organizations using TMS to facilitate better load consolidation and backhaul optimization strategies to reduce carbon emissions.

- The integration of AI and machine learning enables the processing of vast operational datasets, providing the predictive intelligence necessary for building more resilient and sustainable supply chains. These sophisticated management tools are no longer just operational aids but have become strategic assets for navigating the complexities of the modern global economy and achieving competitive advantage.

What will be the Size of the Transportation Management Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Transportation Management Systems Market Segmented?

The transportation management systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Solution

- On-premises

- Cloud-based

- Mode of transportation

- Roadways

- Airways

- Railways

- End-user

- Manufacturing

- Logistics

- Retail and E-commerce

- Government organizations

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Colombia

- Rest of World (ROW)

- North America

By Solution Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises solutions remain a vital component for enterprises requiring maximum data security and customized infrastructure, offering total administrative control over the software environment.

These deployments support deep integrations with legacy systems, creating cohesive supply chain execution platforms that enable a resilient supply chain design.

Organizations leverage these systems for complex last mile delivery optimization and intermodal transfer synchronization, managed by logistics operations agents that ensure seamless information flow.

While the transition to cloud is prevalent, on-premises systems provide unmatched stability for high-volume transactions, with some users reporting a 15% improvement in error detection by using customized telematics and sensor integration.

This approach supports unique business logic and what if scenario planning for smart city logistics, ensuring that system modifications align with strategic operational goals and support autonomous logistics execution.

The On-premises segment was valued at USD 3.99 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Transportation Management Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the transportation management systems market is characterized by varying levels of digital maturity, with North America leading in the adoption of cloud native tms architecture and advanced fleet management solutions.

In this region, end to end supply chain visibility is paramount, with companies leveraging digital freight matching to improve carrier selection and asset utilization.

The focus on efficiency is driving a 35% increase in the use of automated dispatching systems for less than truckload shipping, which reduces manual errors.

In contrast, APAC is the fastest-growing market, where the focus is on scaling operations and managing complex cross-border trade with tools like digital air waybills and automated clearance processes.

Europe emphasizes sustainability and regulatory compliance, where integrated integrated freight cost management is crucial.

Across all regions, the demand for platforms enabling multimodal shipment planning and real time asset tracking underscores a global move toward more connected and intelligent logistics networks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of transportation management systems is increasingly focused on addressing highly specific operational pain points. For shippers, managing complex multimodal shipment logistics is no longer a manual process but one driven by platforms that offer deep analytical capabilities.

- A key area of innovation is in optimizing last mile delivery networks, where advanced algorithms can reduce fuel consumption by over 15% compared to static routing models. This is achieved by integrating ai for predictive logistics, which anticipates delays and suggests alternative paths.

- The concept of a unified platform for supply chain visibility has become a strategic imperative, unifying transportation and warehouse data to create a single source of truth. This integration is crucial for effective agentic orchestration for autonomous logistics and supports real time exception handling in transportation.

- Furthermore, tms implementation for green logistics and sustainability reporting in transportation management are now core requirements, not optional features. Businesses are adopting cloud native tms architecture benefits to support tms support for autonomous vehicle fleets and facilitate multi enterprise supply chain connectivity.

- Simultaneously, mitigating cybersecurity risks in logistics has become a top priority, alongside navigating the geopolitical impact on supply chain networks. The automation of back-office functions like automating freight audit and payment and leveraging real time trade intelligence compliance frees up resources for more strategic tasks, such as enhancing carrier collaboration via tms and improving fleet management with telematics.

- Ultimately, managing freight spend with tms through predictive analytics for freight rates and integrating iot for shipment visibility provides a significant competitive advantage.

What are the key market drivers leading to the rise in the adoption of Transportation Management Systems Industry?

- The increasing adoption of AI and machine learning for predictive logistics is a key driver propelling market growth.

- The primary market driver is the critical need for comprehensive, real-time data to manage complex global logistics, pushing the adoption of advanced analytical tools.

- The integration of autonomous logistics network modeling and energy efficient routing algorithms is helping businesses reduce fuel costs by up to 15%.

- Demand for platforms featuring an inventory twin platform and yard management unification is surging, as these tools eliminate operational silos and improve asset utilization.

- Green logistics initiatives are also compelling the adoption of systems with embedded greenhouse gas measurement and carbon tracking integration, with some achieving a 10% reduction in overall emissions.

- The shift toward autonomous agent capabilities for tasks like automated freight procurement and real time exception handling streamlines workflows. Moreover, iot enabled shipment visibility and predictive market rate insights empower organizations to make smarter, data-driven decisions for predictive backhaul optimization.

What are the market trends shaping the Transportation Management Systems Industry?

- Advancements in agentic logistics orchestration and autonomous decision support are key upcoming trends. These innovations are reshaping how transportation networks are managed and optimized.

- Market trends are defined by a convergence of agentic logistics orchestration and holistic visibility, moving organizations toward predictive operations. The adoption of a unified control tower architecture has enabled a 30% reduction in information latency between warehouse and transport divisions.

- Innovations in autonomous decision support and predictive logistics execution are central, with intelligent automation in logistics improving forecast accuracy by over 25%. Key advancements include platforms that offer multi modal synchronization as a native feature, providing a single source of truth data model.

- This is complemented by a strong focus on sustainability, where integrated carbon tracking and sustainability tracking metrics are no longer optional. The use of logistics network modeling and what if scenario planning allows for proactive risk management, creating more resilient and efficient supply chains through a unified logistics platform.

What challenges does the Transportation Management Systems Industry face during its growth?

- Geopolitical instability and supply chain fragmentation present a key challenge affecting industry growth and operational continuity.

- Navigating market challenges requires advanced digital capabilities to counter geopolitical instability and escalating cyber threats. The reliance on real time shipment visibility is critical, yet fragmented data systems hinder a unified response, with disruptions causing lead time variability of over 25% in affected regions.

- To combat this, businesses are adopting intelligent orchestration engines for dynamic route optimization and ai driven freight planning. However, the complexity of real time trade intelligence and regulatory compliance creates significant administrative burdens. Implementing automated freight audit and automated carrier tendering can improve efficiency, but requires clean data.

- Furthermore, enhancing cybersecurity within a versionless software architecture is a persistent challenge, as a single breach can halt operations entirely. Tools offering a cognitive logistics loop and automated milestone monitoring help mitigate risks, but the threat landscape demands constant vigilance and investment.

Exclusive Technavio Analysis on Customer Landscape

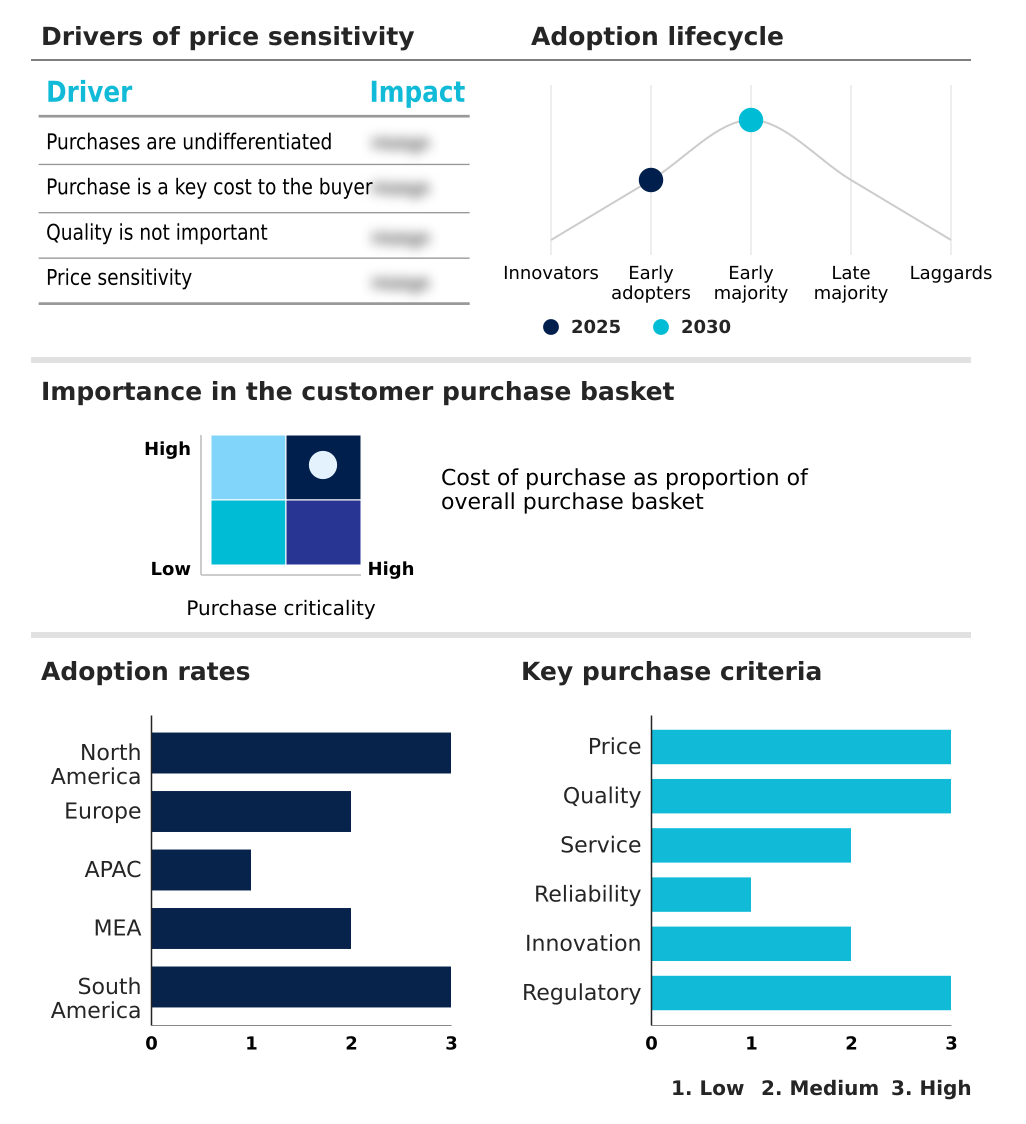

The transportation management systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the transportation management systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Transportation Management Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, transportation management systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpega SA NV - Key offerings include cloud-based modular systems for planning, execution, freight settlement, and analytics, featuring machine learning-based routing to optimize logistics networks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpega SA NV

- Blue Yonder Group Inc.

- Descartes Systems Group Inc.

- E2open Parent Holdings Inc.

- Elemica Inc.

- FreightPOP

- Generix Group

- Infor Inc.

- IntelliTrans

- Koerber AG

- Logility SCS Inc.

- Magaya Corp.

- Manhattan Associates Inc.

- Oracle Corp.

- RateLinx

- SAP SE

- Shipwell

- Softeon

- Trimble Inc.

- Uber Freight

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Transportation management systems market

- In November 2024, Blue Yonder suffered a significant ransomware attack, causing major disruptions to its managed services hosted environment for several retail and consumer goods companies.

- In March 2025, Descartes Systems Group acquired 3GTMS for approximately USD 115 million to strengthen its cloud-native transportation management offerings and optimize over-the-road domestic shipments.

- In March 2025, Manhattan Associates announced the integration of generative AI and yard management unification into its cloud-native platform to help companies resolve complex transportation challenges.

- In April 2025, Oracle introduced advanced AI innovations within its transportation management platform, providing autonomous logistics network modeling and what-if scenario planning capabilities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Transportation Management Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.1% |

| Market growth 2026-2030 | USD 5483.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.3% |

| Key countries | US, Canada, Mexico, Germany, France, UK, The Netherlands, Italy, Spain, China, India, Japan, South Korea, Australia, Singapore, Saudi Arabia, UAE, South Africa, Egypt, Turkey, Brazil, Colombia and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The transportation management systems market is advancing beyond simple execution tools to become the central nervous system for modern supply chains. The shift toward agentic logistics orchestration and autonomous decision support allows for proactive management rather than reactive problem-solving.

- A key trend influencing boardroom strategy is the integration of sustainability tracking metrics and integrated carbon tracking, which directly impacts environmental, social, and governance reporting mandates. Platforms now offer autonomous logistics network modeling and energy efficient routing algorithms to balance costs with corporate sustainability goals.

- Technologies facilitating multi modal synchronization and a unified control tower architecture provide end to end supply chain visibility, which is critical for building a resilient supply chain design. For instance, businesses using predictive logistics execution have reported up to a 20% improvement in on-time delivery rates.

- This evolution is driven by the need for greater agility, with solutions offering real time exception handling, automated freight procurement, and ai driven freight planning becoming standard. These capabilities, including yard management unification and dynamic route optimization, empower organizations to navigate disruptions and optimize performance continuously.

What are the Key Data Covered in this Transportation Management Systems Market Research and Growth Report?

-

What is the expected growth of the Transportation Management Systems Market between 2026 and 2030?

-

USD 5.48 billion, at a CAGR of 12.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Solution (On-premises, and Cloud-based), Mode of Transportation (Roadways, Airways, and Railways), End-user (Manufacturing, Logistics, Retail and E-commerce, Government organizations, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of AI and machine learning for predictive logistics, Geopolitical instability and supply chain fragmentation

-

-

Who are the major players in the Transportation Management Systems Market?

-

Alpega SA NV, Blue Yonder Group Inc., Descartes Systems Group Inc., E2open Parent Holdings Inc., Elemica Inc., FreightPOP, Generix Group, Infor Inc., IntelliTrans, Koerber AG, Logility SCS Inc., Magaya Corp., Manhattan Associates Inc., Oracle Corp., RateLinx, SAP SE, Shipwell, Softeon, Trimble Inc. and Uber Freight

-

Market Research Insights

- The dynamics of the transportation management systems market are defined by a move toward intelligent automation and unified data models. Real time visibility platforms are becoming standard, with adoption rates increasing by over 40% among mid-sized enterprises in the last two years.

- The integration of a single source of truth data model allows for enhanced intelligent automation in logistics, leading to a 25% reduction in decision-making latency for shipment rerouting. Green logistics initiatives are also gaining traction, with platforms offering carbon tracking integration to help businesses align with regulatory mandates, improving compliance reporting efficiency by up to 30%.

- These systems are evolving from siloed tools into a central unified logistics platform, enabling cohesive management of transportation, warehousing, and inventory. This shift toward autonomous agent capabilities and a cognitive logistics loop is foundational for building agile, cost-effective, and resilient supply chains.

We can help! Our analysts can customize this transportation management systems market research report to meet your requirements.

RIA -

RIA -